PHM - M.D.C. Holdings: The Recovery Is Well Underway

2023-11-20 09:26:30 ET

Summary

- M.D.C. Holdings is a homebuilder with a focus on single-family detached homes and financial services operations.

- The company has seen an increase in revenue and profits in recent years, driven by growth in the number of homes sold and higher pricing.

- But this year is looking bad based on a plunge in demand for homes that has caused revenue, profits, and cash flows to sink.

- The good news is that the recovery for the business is now comfortably underway and now might be a good time to buy.

Fundamentally speaking, the housing market has been on a heck of a roller coaster of a ride over the past few years. Leading up to and through most of 2021, there was a significant surge in demand for housing. But as home prices continued to rise in response to supply chain issues and, then, in response to high interest rates aimed at combating inflation, new orders in the industry plunged and backlog declined as existing orders got completed and cancellation rates surged. Earlier this year, I fully expected this to last for at least a year. Frankly, I wouldn't have been surprised if it lasted two years. But by the middle of 2023, signs began to emerge that the housing market was starting to recover. That recovery is not yet complete, but it is continuing into the present day. And along the way, it has opened up a number of interesting opportunities. One firm that investors should definitely pay attention to that is in this space is M.D.C. Holdings ( MDC ). My own assessment reveals that while the stock is not extraordinary compared to similar firms out there, it is appealing enough to warrant a ‘buy’ rating at this time.

An interesting homebuilder

According to the management team at M.D.C. Holdings, the company’s operations really center around two different lines of business. The primary one is the home building portion of the enterprise. Through this, the company builds and sells homes, mostly single-family detached homes, for its customers. The company operates in multiple states across the country, including Arizona, California, Nevada, New Mexico, Oregon, Texas, Washington, Colorado, Idaho, Utah, Alabama, Florida, Maryland, Pennsylvania, Tennessee, and Virginia. The largest state by exposure is undoubtedly California, which was responsible for 22% of the home deliveries and 26% of the home sale revenues that the company generated in 2022. Its next largest concentration is to the state of Arizona, with these numbers coming in at 17% and 14%, respectively.

The other portion of the business is known as its financial services operations. Although there are many activities under this umbrella, this largely focuses on the company working with customers to act as a full-service mortgage lender and principal originator of mortgage loans for its home buyers. It also includes certain insurance operations and title operations. In the grand scheme of things, this is a very small portion of the company, accounting for only 2.3% of the firm's revenue in 2022. However, it is disproportionately profitable, accounting for 9.4% of its pre-tax profits.

{kind=link}

Author - SEC EDGAR Data

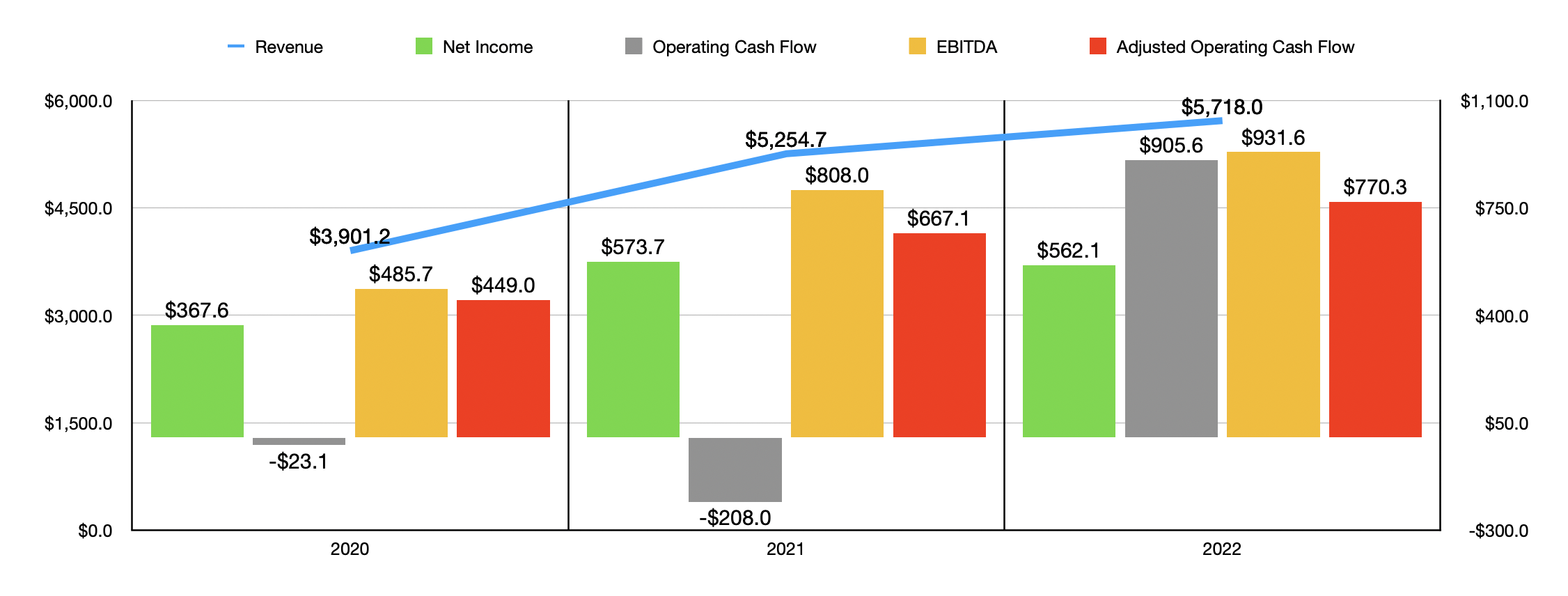

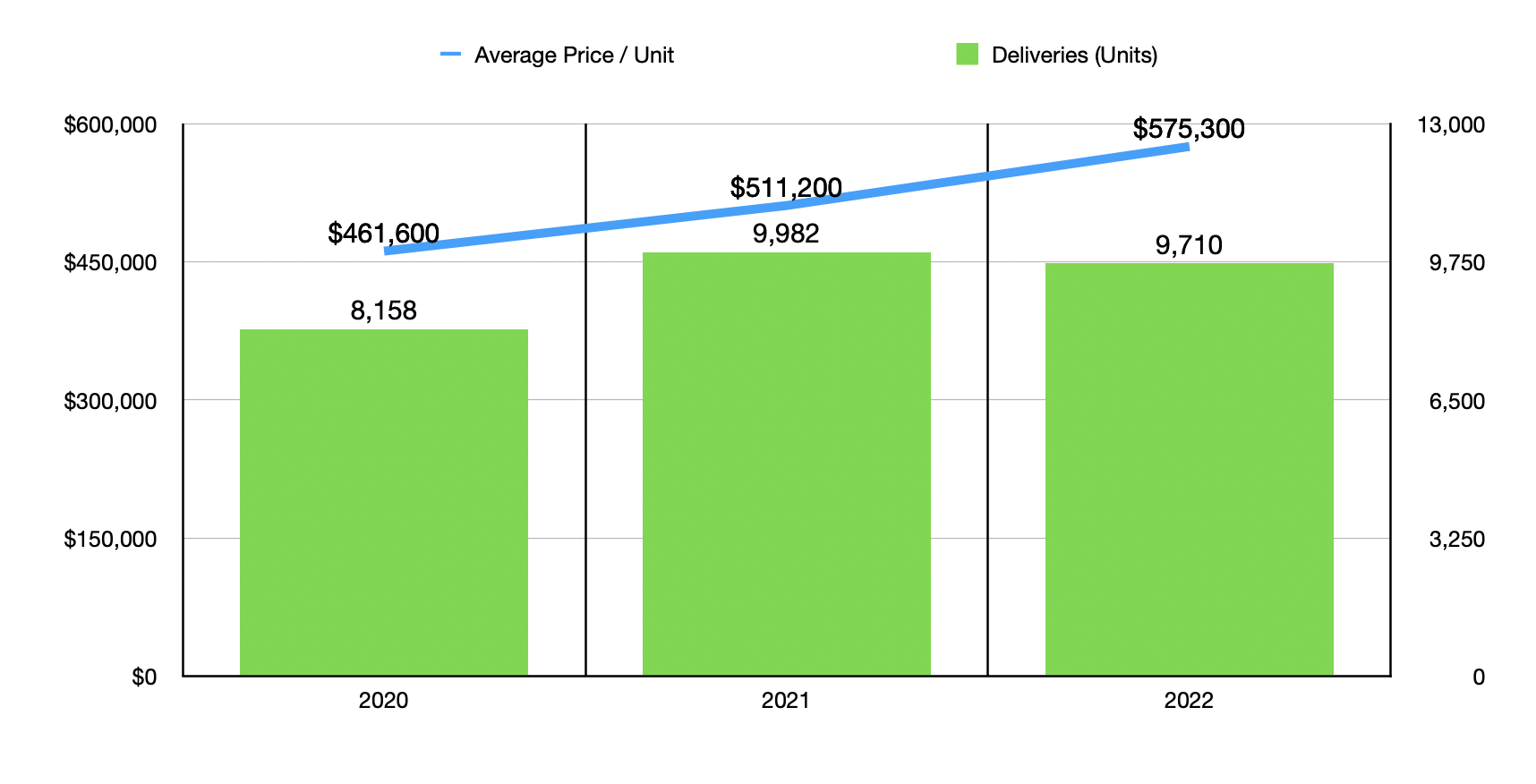

Over the past few years, the revenue picture for M.D.C. Holdings has been quite bullish. Revenue jumped from $3.90 billion in 2020 to $5.72 billion in 2022. This increase in revenue was driven largely by a growth in the number of homes that the business sold. The number of homes delivered in 2020 came in at only 8,158. Two years later, in 2022, it totaled 9,710. But what's important to note here is that you can already begin to see cracks in the picture when you compare 2022 to 2021. That's because, in 2021, the company hit an all-time high for the number of homes delivered of 9,982. The only reason why revenue increased from that year to last year was because pricing for the homes that it sold continued to grow as well. In 2020, the average price for a home was $461,600. This jumped to $511,200 in 2021 before surging further to $575,300 last year.

{kind=link}

Author - SEC EDGAR Data

On the bottom line, we can see something similar to this. Net profits jumped from 2020 to 2021. But 2022 represented a slight decline for the business compared to what it saw the year prior. It is true that operating cash flow hit a new high last year. But if we adjust for changes in working capital, we would actually see an increase from $667.1 million in 2021 to $770.3 million in 2022. Meanwhile, EBITDA for the company exploded in 2022 to an all-time high of $931.6 million. Even as fewer homes were delivered, the higher pricing worked wonders for profit margins.

{kind=link}

Author - SEC EDGAR Data

{kind=link}

Author - SEC EDGAR Data

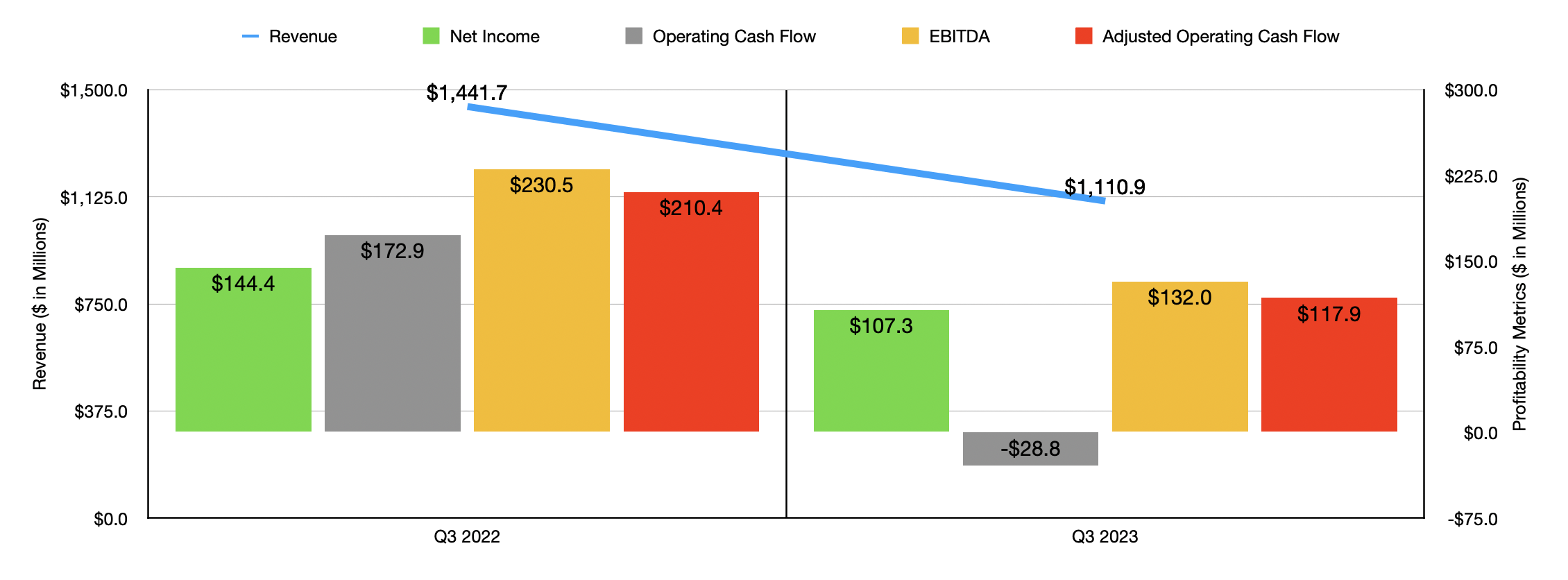

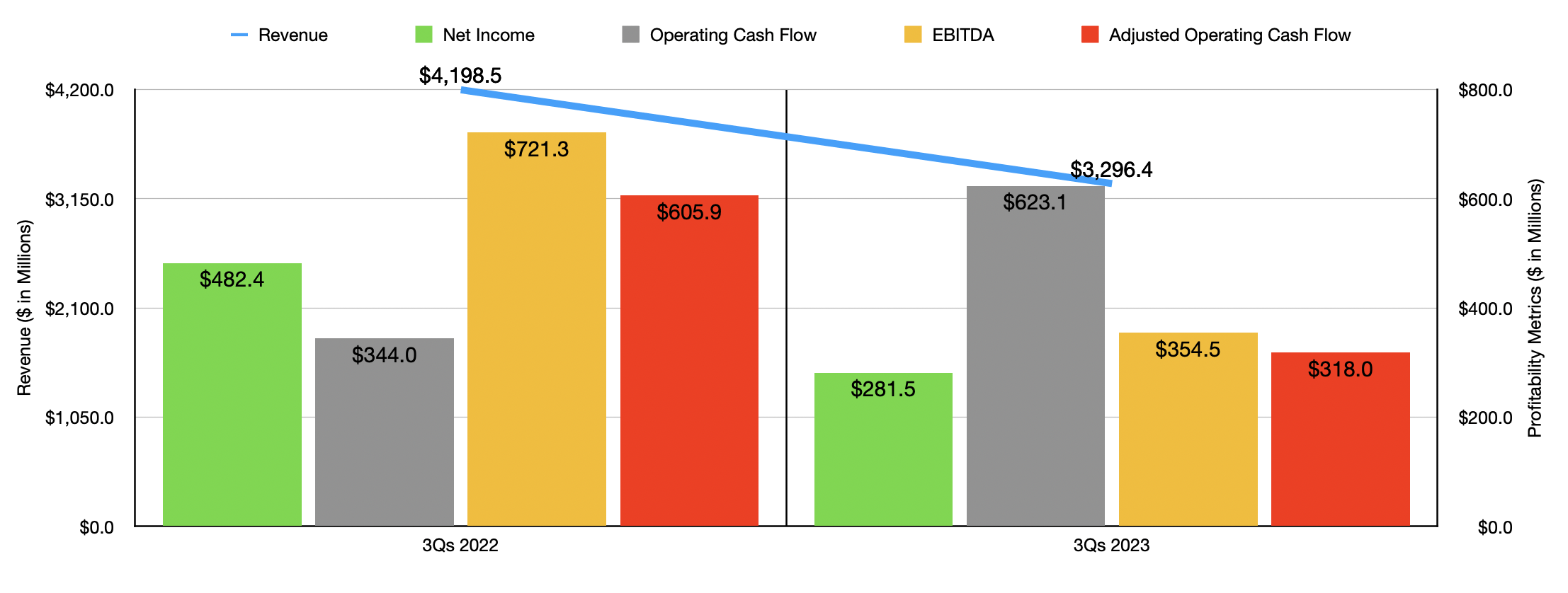

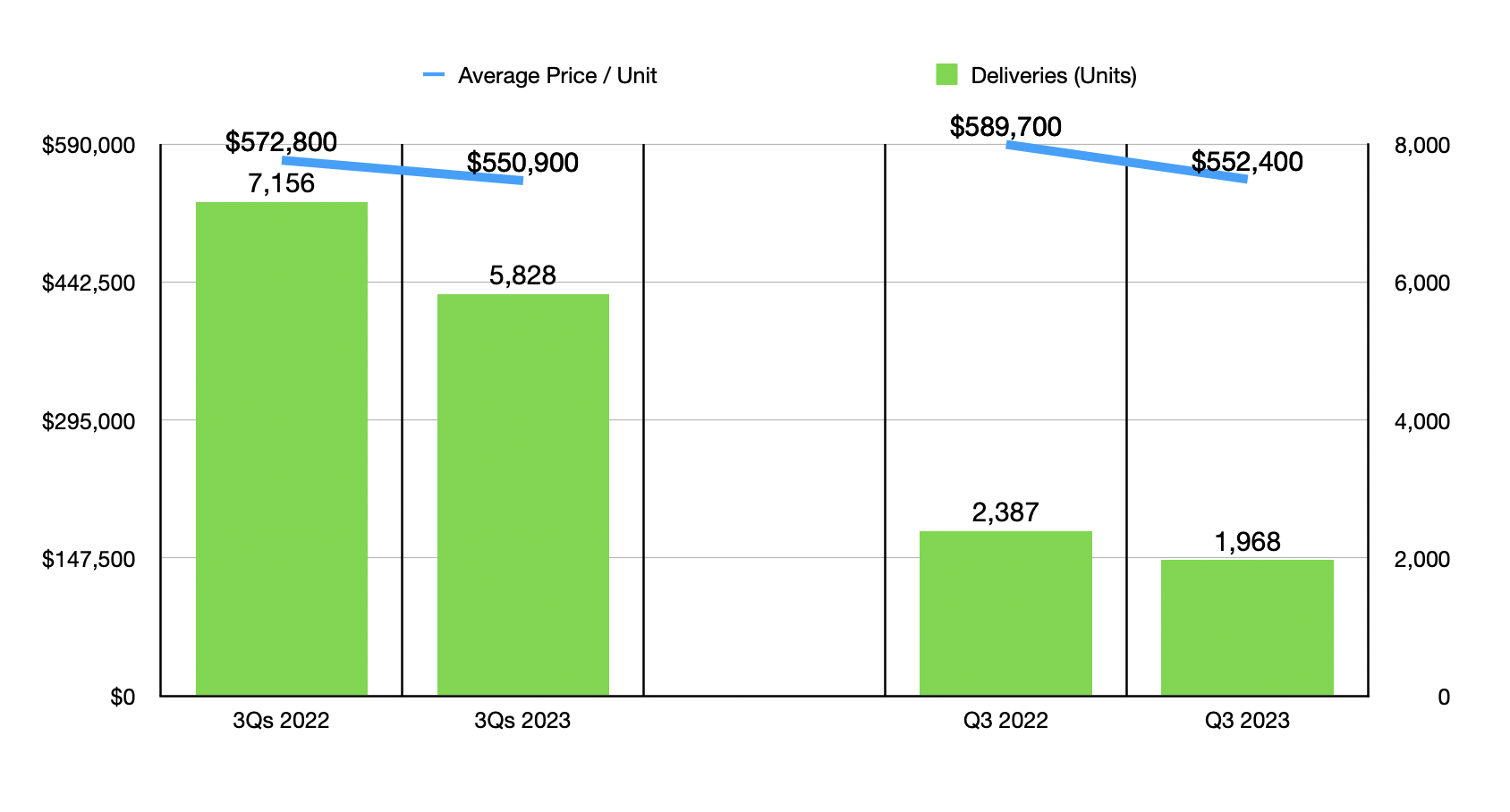

As great as it is to see bottom line results thrive, the 2023 fiscal year has been anything but great for shareholders. As you can see in both charts above, results not only for the first nine months of the year , but for the most recent quarter alone, show significant declines in revenue, profits, and cash flows. This is all, unfortunately, the result of a plunge in deliveries. You can also see that, as deliveries worsened, the average price per home delivered also dropped. This would certainly have been in response to the weakness in orders and management's goal to get business even if it meant that new contracts would be less profitable than prior ones had been.

{kind=link}

Author - SEC EDGAR Data

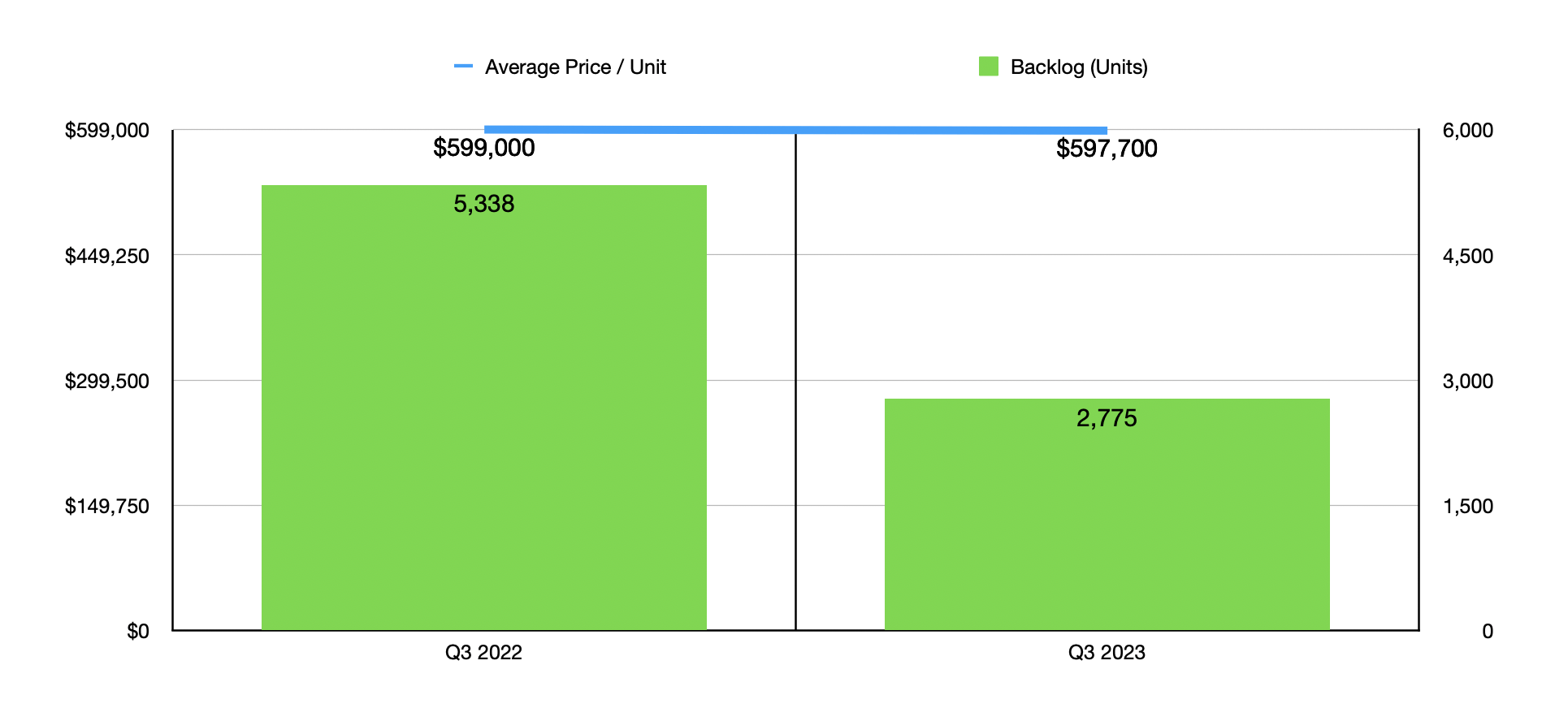

Those who are bearish about the business might point out, and rightfully so, that backlog still remains depressed. As you can see in the chart below, backlog ended the most recent quarter at only 2,775 homes. That's down substantially from the 5,338 homes reported one year earlier. Although it's not as drastic, the price per home in backlog also declined from $599,000 to $597,700. Absent something changing for the better, this indicates significant pain ahead. The good news for investors is that we are finally seeing that positive thing in the form of net new orders.

{kind=link}

Author - SEC EDGAR Data

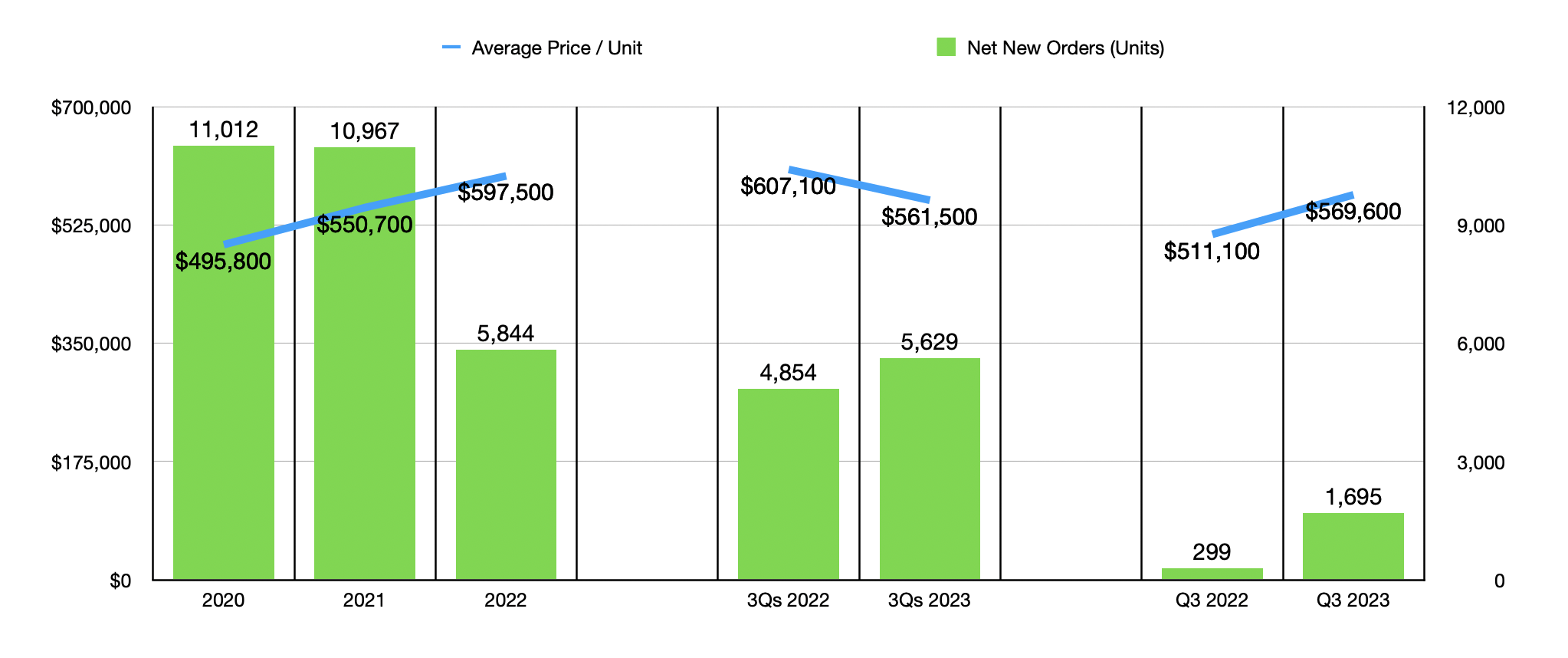

In the chart below, you can see net new orders reported by M.D.C. Holdings, not only for 2020 through 2022, but also for the first nine months of this year as a whole and for the most recent quarter relative to the same time last year. This year, we have started to see a nice recovery in orders. This is particularly clear when you look at the most recent quarter. For the third quarter of 2023, the company brought in net new orders of 1,695 homes. That is significantly higher than the 299 homes reported the same time last year. In the same chart, the average price per home ordered is showing an improvement as well. That's not the case for the first nine months as a whole. But it is true for the third quarter, with the average price of $569,600 comfortably surpassing the $511,100 reported the same time last year.

{kind=link}

Author - SEC EDGAR Data

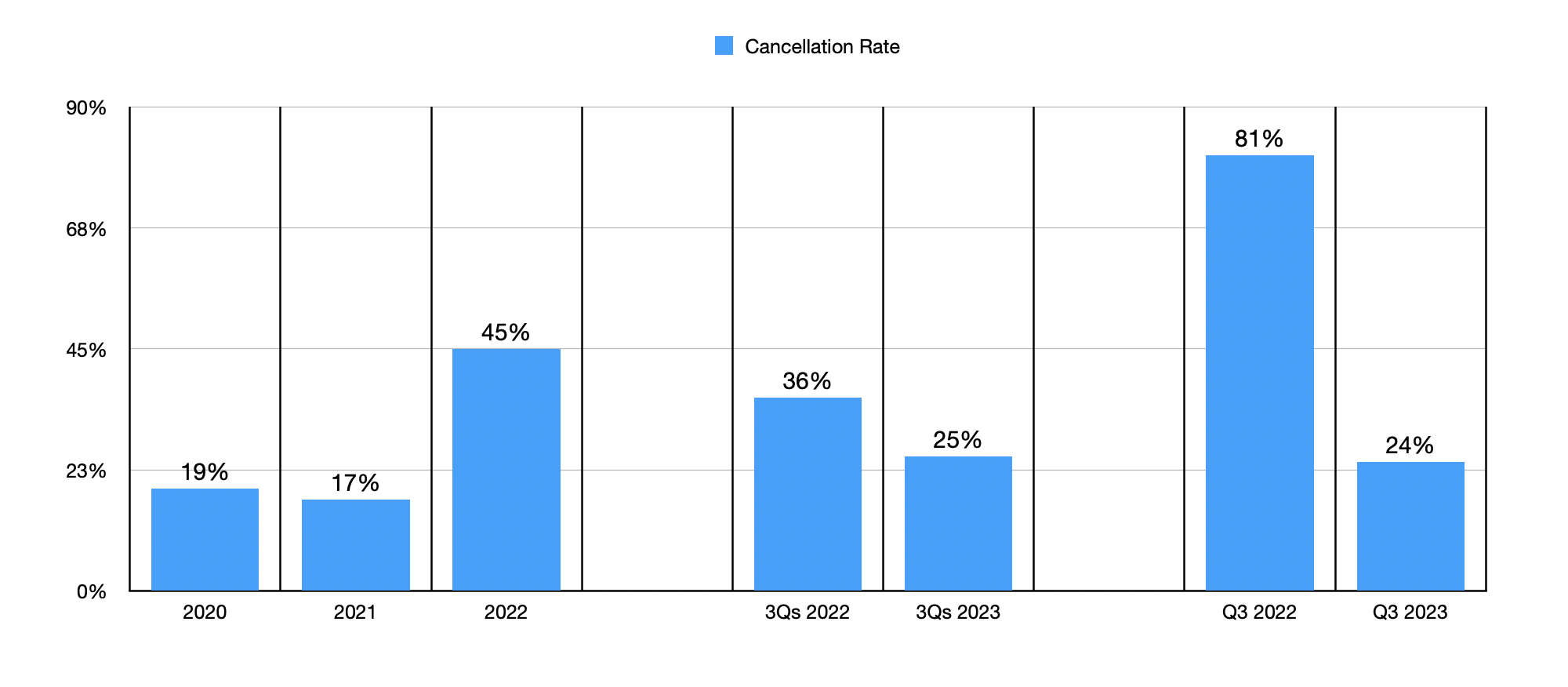

There is one more datapoint that I would like to point to here, and that would involve the cancellation rate. In 2020 and 2021, the cancellation rate for the company was between 17% and 19%. This skyrocketed to 45% in 2022 , b ut that wasn't the worst of it. In the third quarter of last year, the cancellation rate was as high as 81%. I can't say that this is the highest for the industry. But off the top of my head, it is higher than any other firm that I can recall. And I have analyzed most of the players in this space by this point. What the data does show is that we are seeing a big improvement in the cancellation rate. Although still elevated compared to historical data, it stood at 24% in the third quarter of this year.

{kind=link}

Author - SEC EDGAR Data

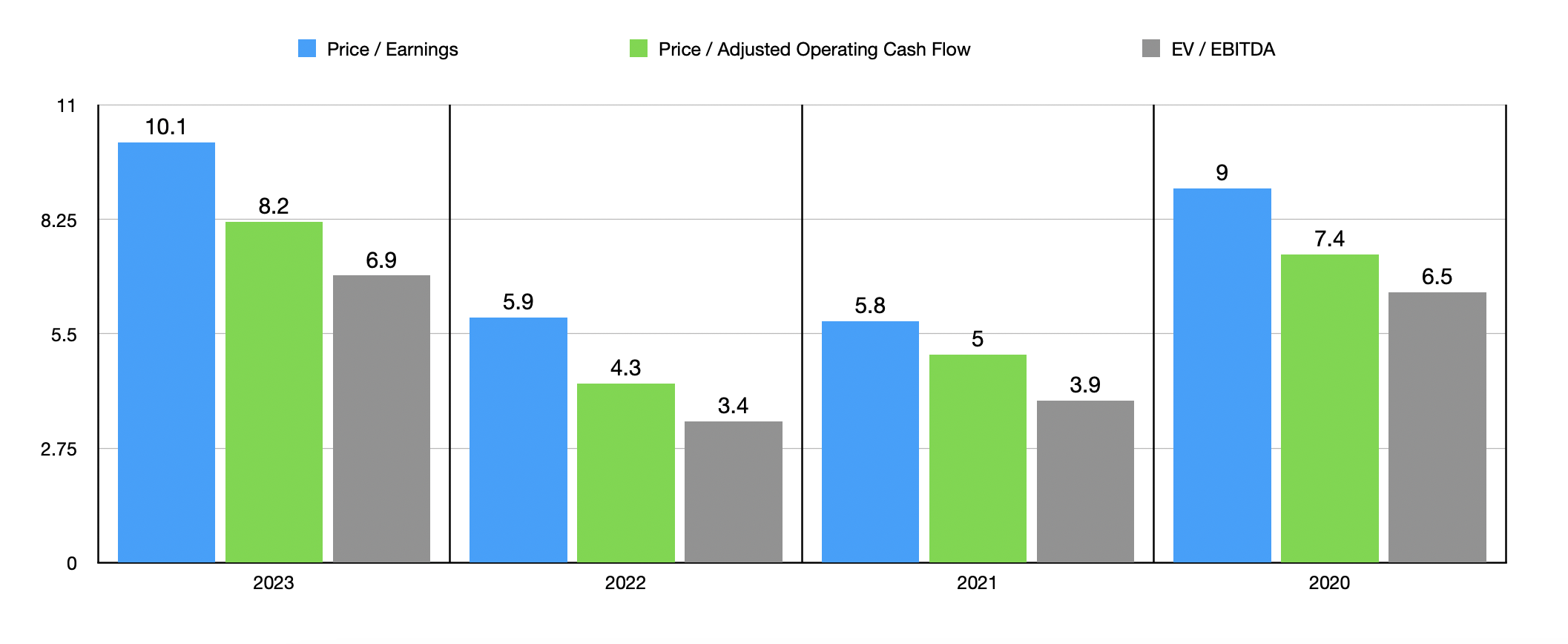

When we are seeing such radical changes in fundamental performance, it really is impossible to know where things will land. So to address this, I decided to price the company based on data from four different fiscal years. That would be the 2020 through 2022 fiscal years, as well as on a forward basis for 2023. The 2023 data is simply based on me annualizing the results that we've experienced so far for this year. Realistically speaking, I would say that assuming a stabilization similar to what was seen in 2020 might not be that bad an idea. While I suspect that the industry will do quite well moving forward, it is better to err on the side of caution and assume that the picture will be worse than it realistically will be.

{kind=link}

Author - SEC EDGAR Data

During this, we end up with a scenario where shares are more or less fairly valued, or might be slightly pricey, compared to other players in the space right now. As you can see in the table below, I compared M.D.C. Holdings to five similar firms. Using the price to earnings approach, I found that three of the five companies were cheaper than it. This number drops to two of the five if we use the EV to EBITDA approach. Though when it comes to the price to operating cash flow approach, M.D.C. Holdings ended up being the most expensive of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| M.D.C. Holdings |

| 9.0 |

| 7.4 |

| 6.5 |

| PulteGroup ( PHM ) |

| 7.1 |

| 6.8 |

| 5.2 |

| Meritage Homes ( MTH ) |

| 6.6 |

| 5.1 |

| 4.8 |

| Beazer Homes USA ( BZH ) |

| 4.9 |

| 2.7 |

| 7.0 |

| Century Communities ( CCS ) |

| 9.4 |

| 5.6 |

| 9.3 |

| Dream Finders Homes ( DFH ) |

| 9.2 |

| 6.4 |

| 7.0 |

Takeaway

Based on the data currently available, I would argue that while recent results for M.D.C. Holdings have been discouraging, the longer-term outlook for shareholders is positive. The worst seems to be over and I suspect that orders will continue to rise from this point on. When you consider how shares are priced, both on an absolute basis and relative to similar firms, you find that it is a decent operator that likely warrants a soft ‘buy’ rating at this time.

For further details see:

M.D.C. Holdings: The Recovery Is Well Underway