SKHSY - M.D.C. Sells To Sekisui At An Attractive Price; Further Upside Is Unlikely

2024-01-18 15:22:12 ET

Summary

- M.D.C. Holdings shares rallied 18% after the acquisition announcement by Sekisui, nearing the purchase price.

- Sekisui aims to achieve its goal of building 10,000 homes in the US by 2025 with the acquisition of MDC.

- It is unlikely for the deal to be blocked due to low market share and no antitrust or foreign investment concerns.

- At 12x earnings and 1.4x book value, no other bidders are likely to emerge.

Sekisui to Acquire M.D.C. Holdings

Shares of M.D.C. Holdings ( MDC ) have been a strong performer over the past year, and shareholders received another boost Thursday, thanks to an acquisition that sparked an 18% rally. Under the terms of the deal, Sekisui ( SKHSY ) will pay $63 per share in cash . Shares are already within 0.5% of that price. Given I view a deal as likely to close but no superior offers likely to materialize, I would sell shares and lock in the profit.

{kind=link}

Rationale for the Deal

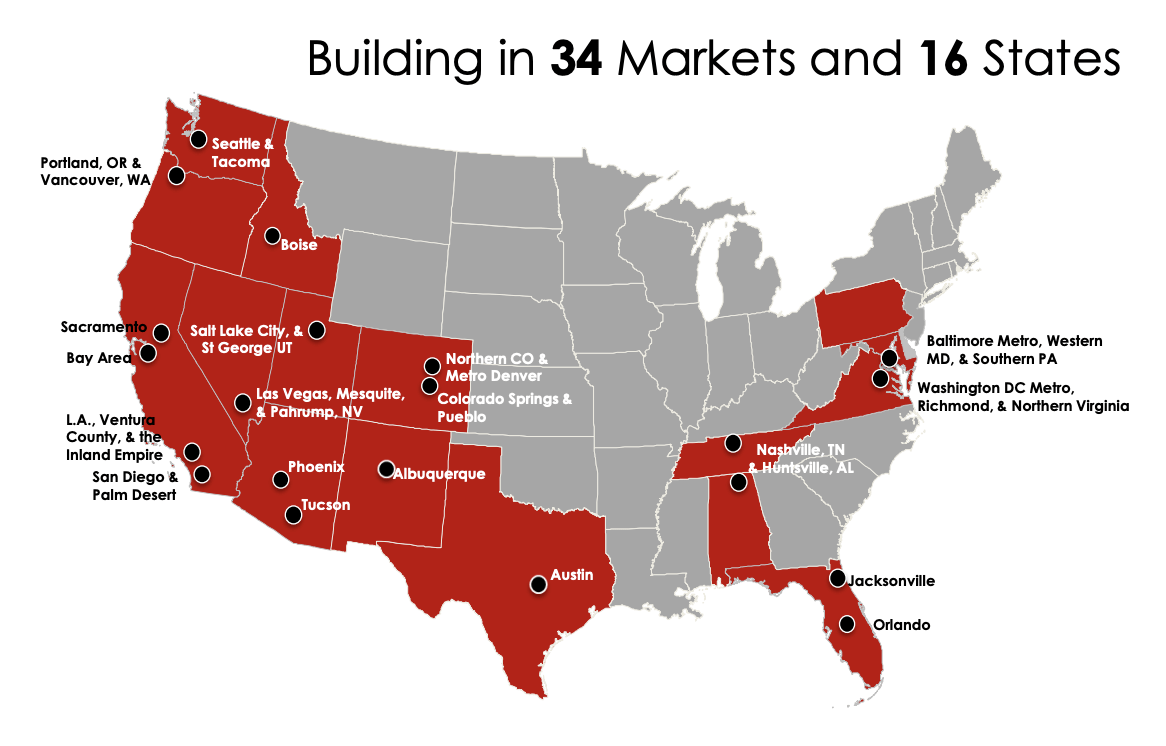

M.D.C. Holdings is a mid-sized US homebuilder with a focus on first-time homebuyers given its average selling price of about $550k as of the third quarter . Over the past year, MDC has delivered nearly 8,400 homes, and it has 235 active subdivisions. As you can see below, MDC operates primarily across the Western United States, with additional exposure in the Sun Belt.

{kind=link}

The deal logic is clear when we look at Sekisui’s US business because it operates across a very similar footprint, similarly focusing on the middle and lower-end of the new housing market in the US.

{kind=link}

With MDC, Sekisui is operating in markets it already knows, and this increased scale should help the company find synergies to reduce costs and support margins. While Sekisui is primarily a Japanese builder, it has sought expansion in the US to diversify revenue. This purchase will help Sekisui achieve its goal of building 10,000 homes in the United States by 2025.

Sekisui in June 2022 announced an acquisition of Chesmar, which built just over 2,000 homes. That added to its Woodside and Holt Group brands, which together build over 3,000 homes, giving the company about 5,000 units of capacity. With the ~8,400 units from MDC, the company will vault past its 10k unit goal. MDC was the 11 th largest US homebuilder by volumes, and together they should be about the 5 th .

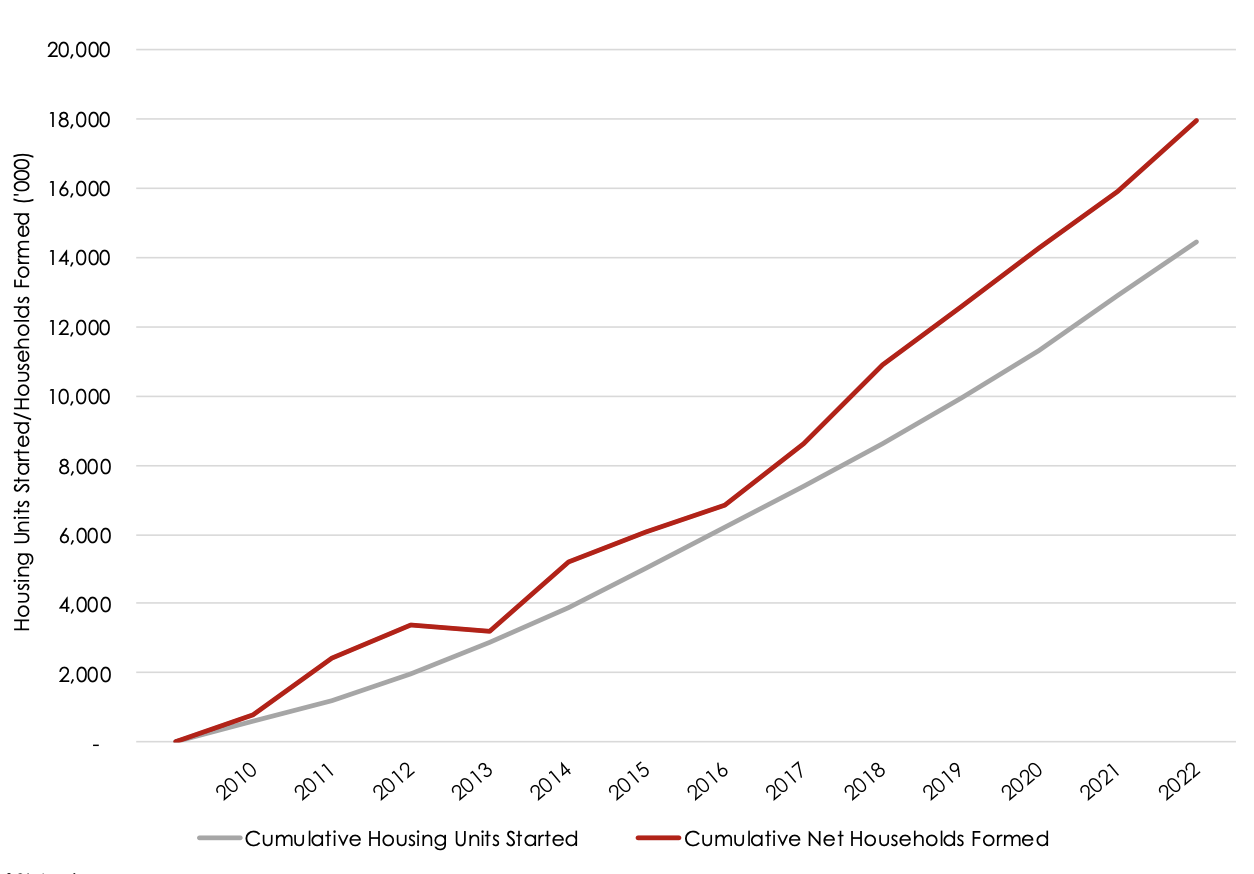

To be clear, Sekisui is not diversifying for the sake of diversity; the US housing market is very attractive, which is why I have rated many housing-related stocks a buy over the past year and a half. As I wrote about in 2022 , the US housing market is deeply undersupplied because of low construction levels last decade, and I have estimated a ~4 million unit shortfall. MDC’s analysis is similar, at about 3.7 million units.

{kind=link}

I believe Sekisui likely agrees with this analysis. Under-supplied markets give sellers more pricing power, which is why I have viewed homebuilders favorably, expecting this dynamic to keep prices up and housing more resilient to higher rates than many expected, which has largely played out. With the Federal Reserve potentially cutting rates, the market could face renewed demand, further assisting builders.

Could the deal be blocked?

In M&A, there are two risks: on the downside, that the deal is blocked, or on the upside that another suitor comes in and starts a bidding war. Beginning with the downside risk, with shares nearly at $63, the market views completion as highly likely. I agree with this.

There certainly has been increased antitrust scrutiny - as Spirit Airlines ( SAVE ) and JetBlue ( JBLU ) investors have learned recently - of all deals over the past few years. I see no antitrust issues here. The US housing market sees about 1.5 million homes built per year. It is very fragmented with many local builders. Together, Sekisui and MDC will have only about 1% market share. They remain a very small player. With still 4 builders larger than them, and such a small market share, it is difficult to see any plausible antitrust argument in my opinion.

{kind=link}

The other risk here is that this is a foreign company buying a US firm, which can create some additional scrutiny. However, Sekisui did close its acquisition last year with no issue, and I view that likely here. Particularly with Japan being a close US ally, I would normally see no issue with foreign buyer risk. However, it would be remiss not to note that Nippon Steel’s proposed acquisition of US Steel ( X ) has become politically controversial with some calling for a review by CFIUS, the Committee on Foreign Investment in the United States.

This push does suggest increased skepticism of foreign buyers of US assets, even from less-controversial companies like Japan. That said, I do not expect a similar response here. MDC is much smaller and less of an “iconic/legacy” brand as US Steel. Moreover, as I have discussed in write-ups of the steel sector , that industry has benefitted from a much more consistently protectionist spirit, across both sides of the aisle. For instance, President Biden has largely kept President Trump’s steel tariffs in place—a rare point of agreement.

Given MDC’s relatively small size and the small combined market share, I do not see regulatory challenges for this deal from either an antitrust or foreign investment perspective. Further, there are not financing conditions, and so Sekisui should have no issue closing by 6/30/24, if not sooner.

Could another bidder emerge?

While I do not see downside from the $63 purchase, with shares so close to $63, there would likely need to be another bidder to materialize to justify owning shares. I do not see this as likely. First, Larry Mizel and David Mandarich the founder/Chairman and CEO respectively have each agreed to vote in favor of this deal, giving 21% shareholder support already. With that key support, Sekisui should have a relatively easy path getting the necessary majority support. While this is not a founder-controlled company, with that ownership stake, MDC is heavily “founder-influenced.” Presumably if it had another interested party to sell to, it would have, and so appear happy to sell to Sekisui.

On top of this, MDC is getting a fair price in this transaction in my view. In the company’s third quarter , MDC earned $1.40 as revenue fell from $1.4 billion to $1.1 billion. Deliveries were down 17.5% to 1,968. Through 9 months, it has earned $3.73. Based on Q4 guidance of 18-19.5% gross margins on about 2,300 deliveries at a roughly stable sales price of $550k, MDC should earn about $5.25 this year.

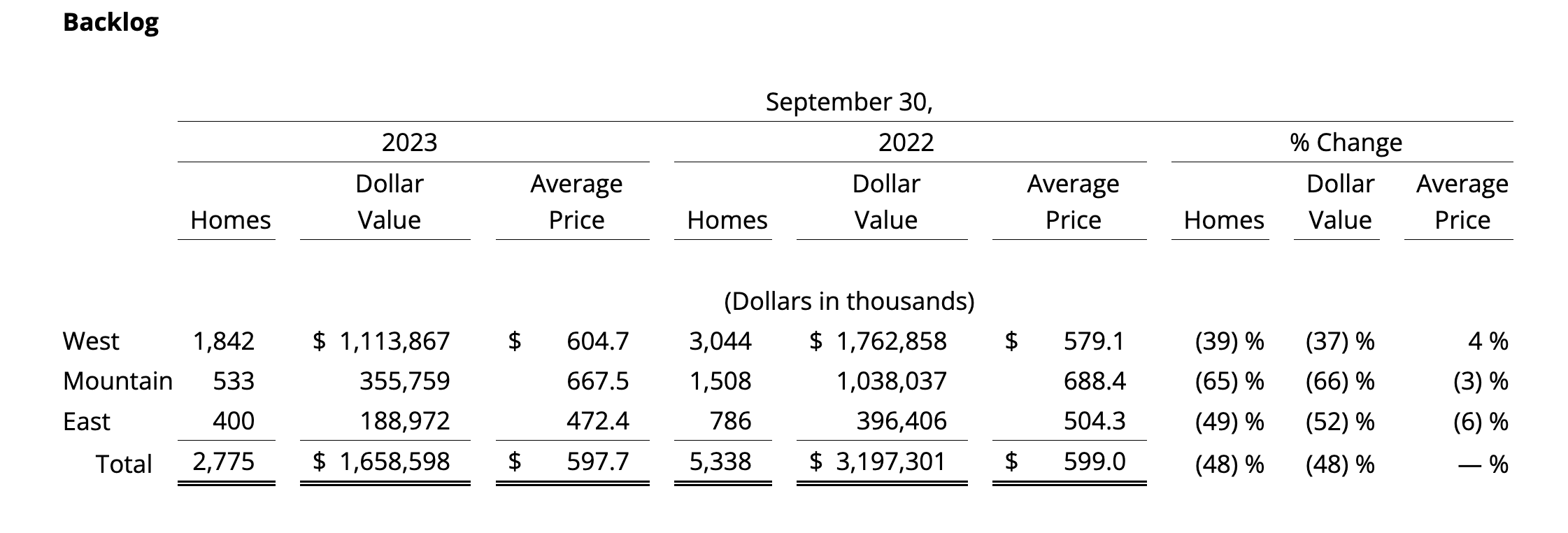

At this purchase price, MDC is selling for 12x 2023 earnings and about 1.4x book value (this was $44 in Q3 and likely ended the year in Q4 at ~$45). That is a solid multiple. Now, at this price, Sekisui immediately gets MDC’s added scale with 235 active communities. MDC also owns 17,800 lots with a further 4,600 optioned. The company has a backlog of 2,775 units, which while down by 48% from last year, provides a solid base of revenue for 2024.

{kind=link}

Importantly, MDC has seen improving activity lately. In Q3, there were 1,695 in new orders, well up from 299 last year with the West accounting for 60% of deliveries. Additionally, with building costs declining, gross margins improved by 280bp sequentially, though they are expected to decline slightly in Q4 from the 19.7% in Q3. Sekisui likely sees room for margin improvement as it combines operations and builds scale.

By buying MDC, Sekisui gets to pull forward its US expansion and add exposure to a secularly strong market. Additionally, MDC adds balance sheet strength as it has $1.8 billion in cash and securities vs just $1.5 billion of debt, leaving it with a net cash position.

12x earnings and 1.4x book value is a good price to sell at. For comparison, KB Home (KBH), which I recently downgraded to hold , is trading just below 9x 2023 earnings and about 1.2x book value. Now, it does carry about $1 billion in net debt, which likely suppresses its P/E vs MDC. Given where KB trades, it would be difficult for it to top the bid and still be accretive to its shareholders without adding significant debt, which US homebuilders have been loath to do.

With most homebuilders trading at ~10x earnings, they are likely to continue to direct their cash flow to repurchasing more of their own shares than seek M&A, particularly at this multiple. Indeed, some might argue I was too cautious in moving KBH to a hold, given its lower valuation. Typically though, publicly traded companies trade below M&A premium prices. Sekisui also had a unique rationale (scale up small US operations) that can justify its decision to pay a premium above potential stand-alone value. As such, I would not expect KBH to reach MDC’s multiple.

Concluding thoughts

Ultimately, this has been a great year for MDC holders. With this deal highly likely to close but no clear reason for shares to move above $63, this trade is now played out. Assuming a ~3 month close, investors have an annualized return of ~5%, assuming one more dividend payment. For that yield, investors can own a treasury bill. With essentially no premium to the risk-free interest rate, markets are correctly, in my view, assuming this deal is likely to be completed. As such, with no equity risk premium left, I would sell shares, lock in strong profits, and look to allocate elsewhere.

For further details see:

M.D.C. Sells To Sekisui At An Attractive Price; Further Upside Is Unlikely