MGPUF - M&G: Better Start Thinking About Private Credit And Selling

2023-09-01 14:33:23 ET

Summary

- M&G Plc is facing challenges from inflation in its fixed costs, commodification of asset management, and the high interest rate environment.

- The company has a strong presence in fixed income and institutional clients, so there is a decent way forward for them despite the end of TINA compared to other asset managers.

- One could speculate, as markets already have in M&G's case, on it being potentially acquired. But while there is a case, it is speculative.

- Otherwise, the industry and company isn't that well positioned, and we don't like the diseconomy from seeing a rapidly devaluing fixed income portfolio.

M&G plc ( MGPUF ) is not a clear story. Inflation is against them. Asset management commodification is against them. The high interest rate environment is also somewhat against them, although less so than other asset management companies. We want to hear about a private credit growth push, which we think M&G could actually manage well given its focused presence so far on fixed income. It is probably this factor that makes a speculated acquisition somewhat possible by an advisory company or a full-service bank. Indeed, while only speculated, maybe it will be Macquarie ( MCQEF ). In the end, there is a decent case for M&G getting folded into another operation. However, an exit like that is speculative considering the current, risk-averse M&A environment, and without acquisitions there's not much impressively propelling M&G forward into higher earnings.

FY and Q1 Trading Update

It's useful to get right to why M&G isn't a relatively weak pick in the AM space, even in spite of the headwinds that have been secularly pressuring the industry.

{kind=link}

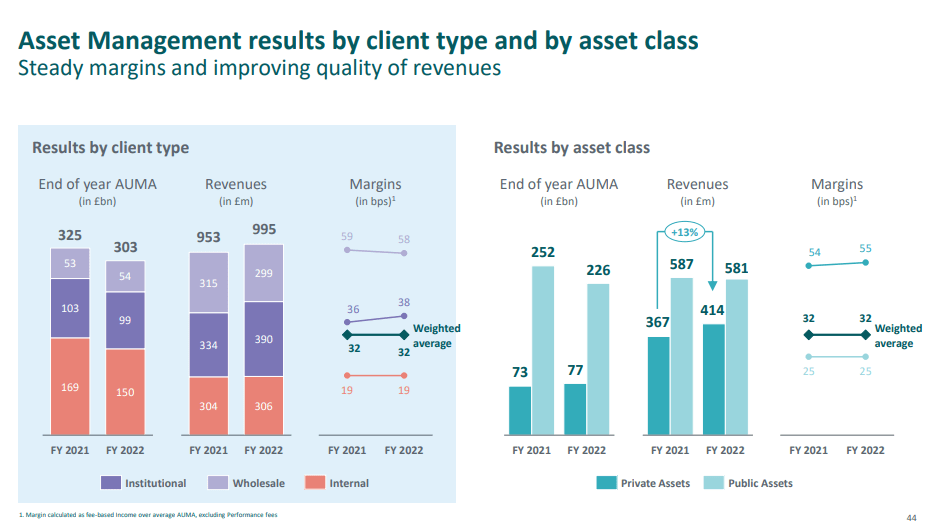

Firstly, there are quite a lot of institutional clients. These guys are less flighty when it comes to competition with deposit institutions and base rates on deposited cash at banks. This is important as interest rates rise and TINA takes effect. However, they are losing price value on bonds big time from long-dated maturities in the portfolio, just look at how it hits the very bottom line.

{kind=link}

Similarly, they have a pronounced public fixed income business, actually bigger than equities. Again, good considering the end of the TINA environment.

{kind=link}

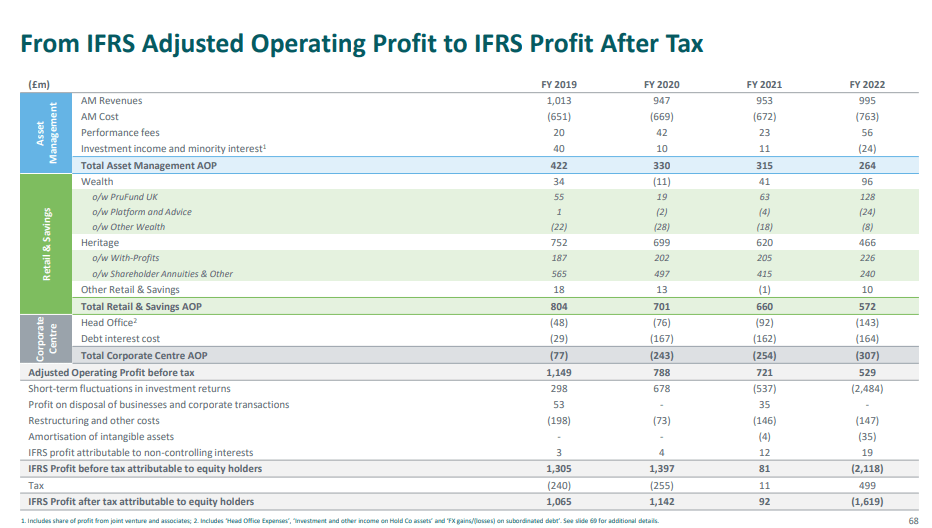

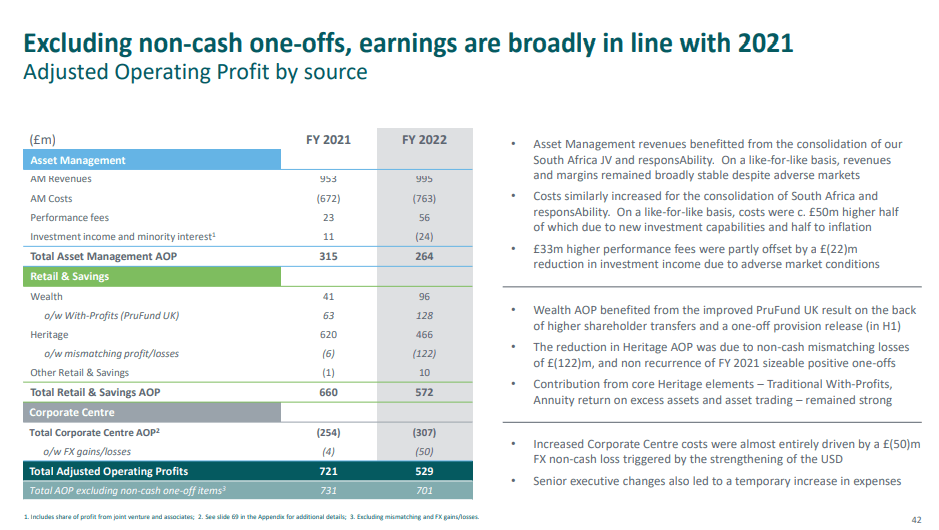

The problems for them that are less mitigated is inflation in the fixed cost base. These businesses are being attacked from all sides by other savings solutions and AM is becoming more commodified. With not much pricing power at all, inflation in the fixed cost base meaningfully crimps income.

{kind=link}

With the interim trading update (UK companies don't usually do full-on quarterly reporting), things haven't gotten much better either in terms of AUM, with the fundamental KPIs still going flat as of March 2023 . That may be improving now, but the inflation without pricing power looks to indicate basically a permanent hit to the bottom line. Cost reduction will have to be pursued.

Acquisition is the Only Investment Case

There has been speculation around an acquisition of M&G by an advisory firm. Management has obviously not commented on it, and it's all just rumours , but the notion does make some sense. Firstly, there is a private-fixed income business, but it should grow considering the secular shift we are seeing from public to private credit. Originating private credit deals is a little more involved, and combining it with an advisory firm could make some sense, especially as they try to grow their franchises in providing private credit intermediation services.

It helps also that the M&G price has stagnated since separatin g from Prudential ( PUK ), and an acquisition could be a good opportunity to make some cost reductions and improve margins. Joining with a more appropriate financial institution than Prudential could make sense, with a particular eye on full-service banks and advisors, especially as UBS's ( UBS ) grip on the wealth management market tightens as well after the CS collapse.

Sharing backend and other low-hanging fruit synergies could also be important for improving run-rate bottom lines after margin pressure, although some AM functions likely have to be conducted separately due to compliance reasons, depending on the acquirer.

M&G isn't that expensive as a multiple of adjusted operating earnings, a little over 10x in PE excluding some pre-maturity bond devaluations. They probably make sense to pick up. However, playing that speculative case is the only way to get a good return on M&G, in our opinion. Otherwise, there are better shares out there on other markets that are being despondently sold at lower multiples and with better business models than M&G. Overall, we rate it a hold.

For further details see:

M&G: Better Start Thinking About Private Credit And Selling