MHO - M/I Homes: Cheap Homebuilder Primed For Growth

2024-01-18 22:39:11 ET

Summary

- M/I Homes revenue has grown at a CAGR of +16% while EBITDA is at +26%, as the demand/supply imbalance in the housing industry has widened.

- MHO has an attractive business model, underpinned by geographical diversification, expertise in the segment, and a healthy portfolio of land.

- We see numerous tailwinds that should drive demand for newly built homes in the coming years.

- The current economic conditions are concerning, but we see evidence to suggest strength in the housing market, which suggests a return to healthy growth will likely come soon after rates decline.

- MHO is performing well relative to its peers yet is trading at a ~40-50% discount, suggesting further upside.

Investment thesis

Our current investment thesis is:

- Primarily centered around the demand for homes in the coming years, which we suspect will be elevated due to a lack of supply. The housing market is struggling currently but property prices remain flat, suggesting the expected sell-off has not occurred. The current period of lower housing starts will only act to compound this issue in the medium term.

- Underpinning this thesis is a quality business that appears to be run well. It has exposure to affordable housing, is innovating to remain ahead, and has a swelling cash balance that can be used to acquire land and distribute the excess to shareholders.

Company description

M/I Homes ( MHO ) is a leading homebuilding company in the United States, founded in 1976. Headquartered in Columbus, Ohio, the company operates in various regions, providing a range of residential properties. M/I Homes is known for its commitment to quality construction, innovative design, and customer satisfaction.

Share price

MHO's shares have returned over 400% during the last decade, much of which has come during the last year. This share price volatility is a reflection of the current environment, as investors seek to understand how homebuilders are impacted by the increase in rates.

Financial analysis

{kind=link}

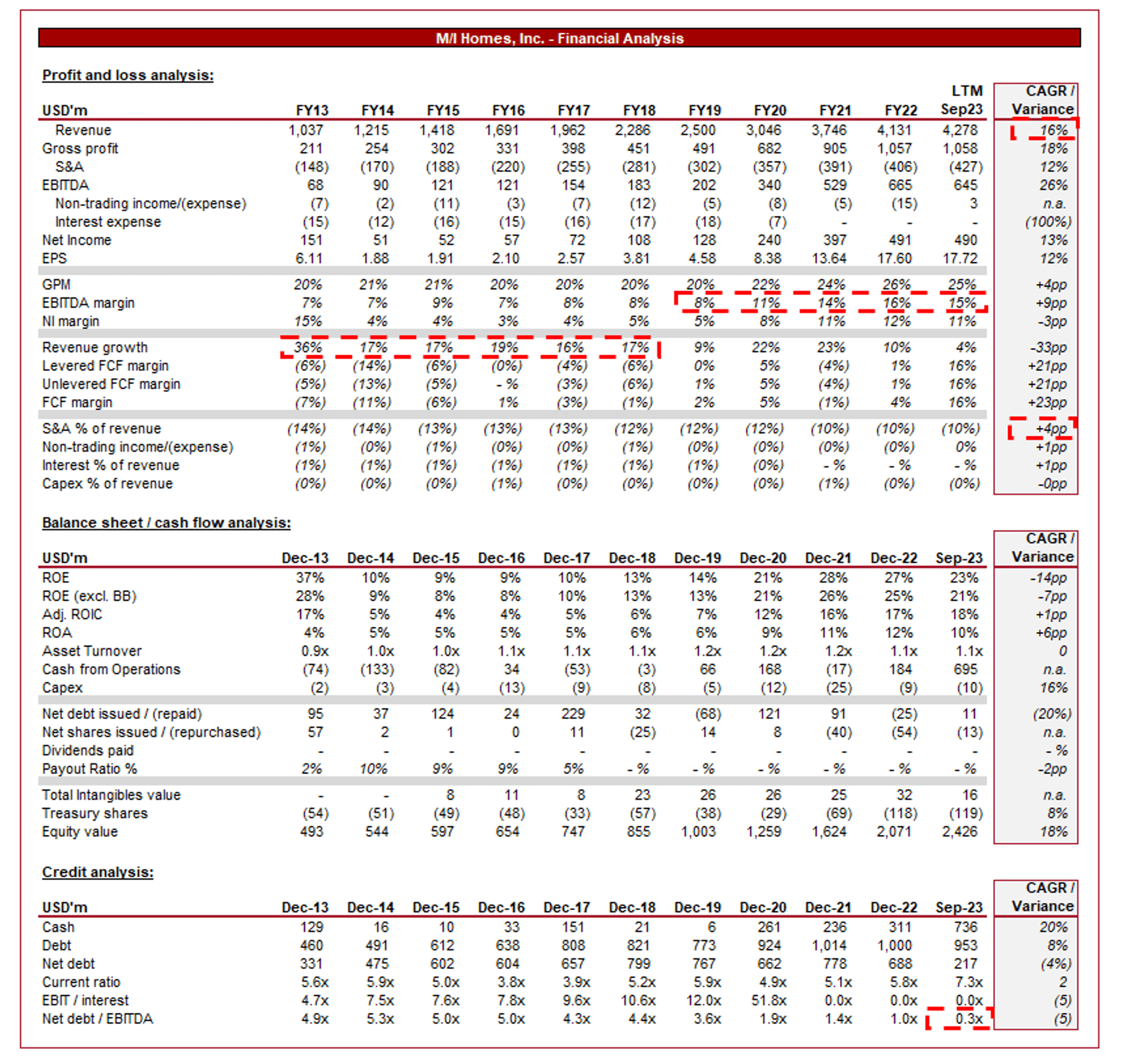

Presented above are MHO's financial results.

Revenue & Commercial Factors

MHO's revenue has grown well during the last decade at a CAGR of +16%, while EBITDA has exceeded this at +26%.

Business Model

MHO primarily engages in the construction of residential properties, including single-family homes and townhomes.

MHO offers a range of home designs and floor plans to cater to different preferences and market segments, with an ASP of $481k in 3M Sept. 23. This diversification allows the company to appeal to a broader customer base.

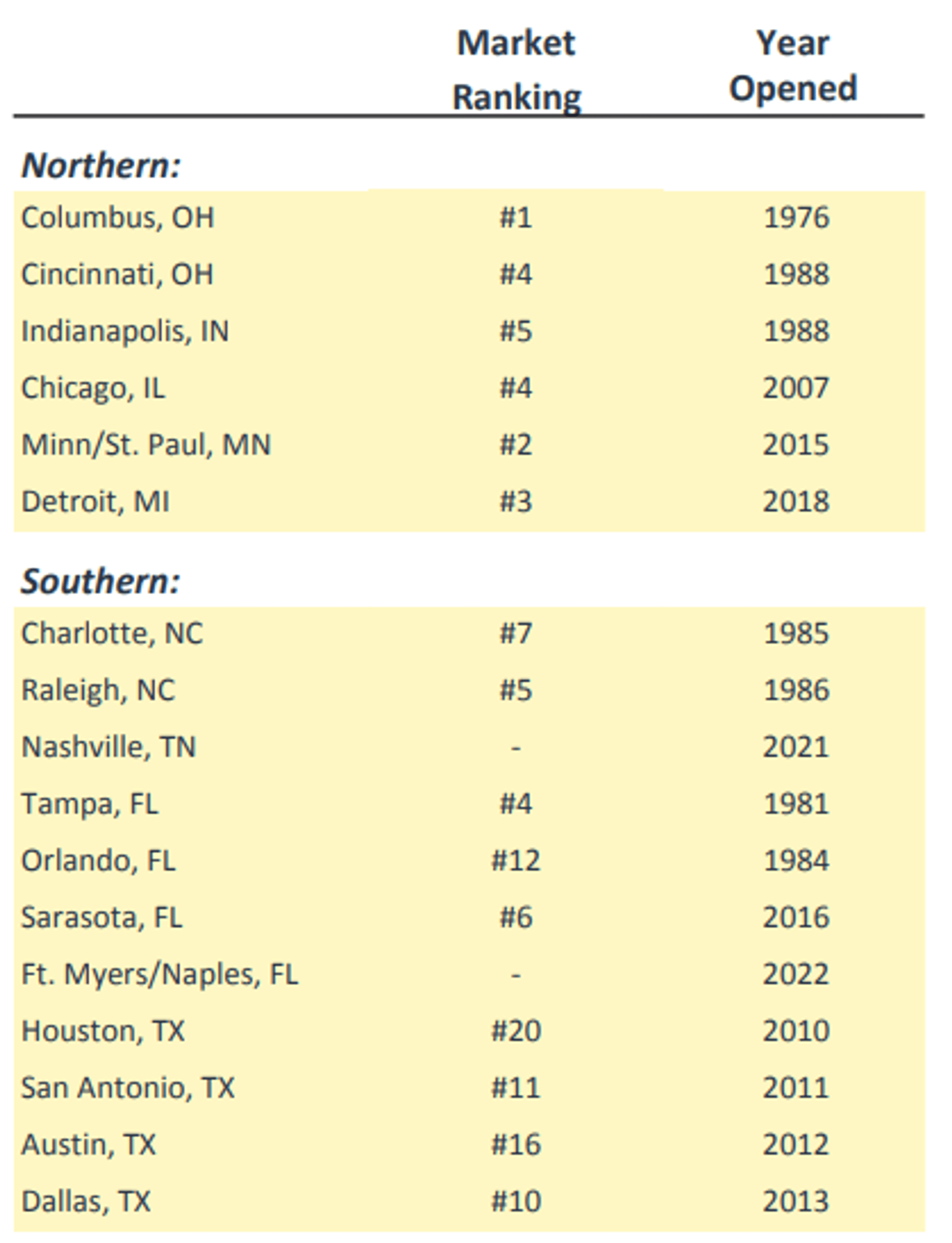

The company strategically operates in multiple geographic regions, targeting areas with strong housing demand. This geographic diversification helps MHO capitalize on regional market trends and economic conditions. The company is a market leader in the majority of its key geographies, allowing for brand development, which is critical for consumer trust.

{kind=link}

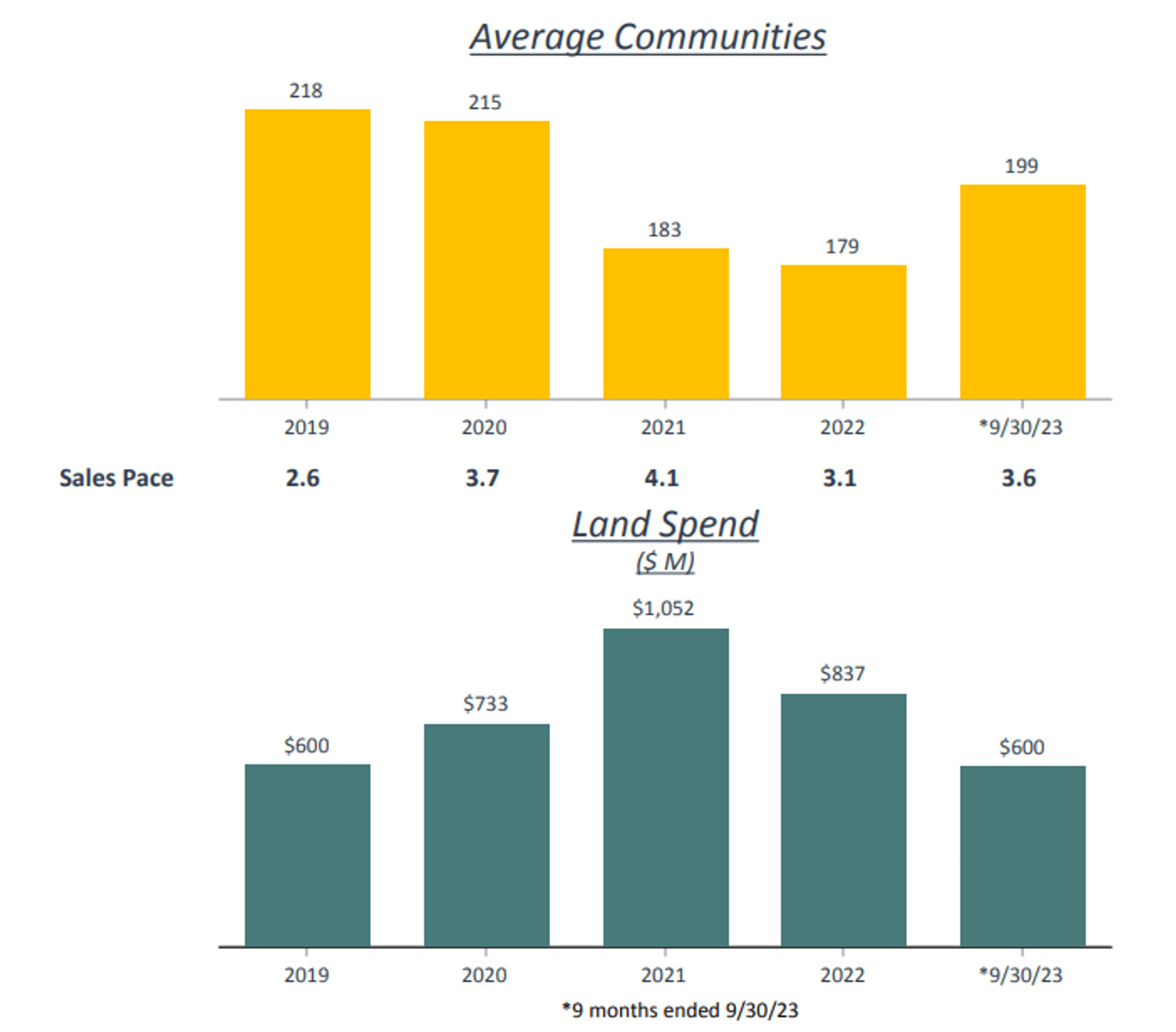

MHO engages in land acquisition and development to secure the necessary resources for building homes. Strategic land planning and development are crucial components of the business model to ensure a steady pipeline of construction projects. The company's size and expertise in core markets position it well to persistently acquire prime assets.

{kind=link}

In some cases, MHO offers mortgage and title services, streamlining the homebuying process for customers reducing key barriers to the home-buying process and differentiating itself. The company currently has a capture rate of ~86%, a strong buyer profile with an average credit score of 748, an average down payment of ~17%, and an EBT margin for the segment of 46%.

Competitive Positioning

We consider the following factors to be key to MHO's growth trajectory:

- Customization - MHO often provides customization options, allowing homebuyers to personalize certain aspects of their homes. This customization feature enhances customer satisfaction and sets MHO apart in the competitive homebuilding market and is a key advantage compared to the traditional real estate market.

- Quality - MHO has focused on quality construction and modern design aesthetics. The company generally boasts strong customer satisfaction and positive brand perception based on our research, although noting there are always cases of "horror stories" and so much of its success is based on selling the customer on-site.

- Housing Demand and Market Trends - MHO has strategically positioned itself in regions with high housing demand. The company's ability to identify and respond to market trends has contributed to its growth.

- Innovation in Design and Technology - The incorporation of innovative design elements and technology, such as smart home features, resonates with modern homebuyers and differentiates new builds from existing properties.

- Effective Land Management - Efficient land acquisition and management are critical to the homebuilding business.

- Adaptation to Sustainability Trends - The focus on energy-efficient and environmentally friendly homes aligns with the growing emphasis on sustainability. Similarly to a number of points above, this differentiates new builds from existing properties.

- Financial Services Integration - As discussed, this reduces barriers to purchase.

Homebuilding Industry

MHO faces competition from leading (multi)national firms and local builders in specific states. Its listed peers include, but are not limited to: PulteGroup ( PHM ), D.R. Horton ( DHI ), Lennar Corporation ( LEN ), TopBuild ( BLD ), Toll Brothers ( TOL ), and NVR ( NVR ).

The competitive dynamics within the industry center around:

- Pricing strategies and affordability.

- Quality of land acquired.

- Innovation in home design and construction techniques.

- Geographic presence and market share.

- Sales approach and ability to limit barriers to purchase.

Opportunities

We see the following factors as key growth drivers going forward:

- Lack of home availability - The US, similarly to the rest of the West, is experiencing a housing shortage. This is a reflection of chronic infrastructure underspending, restrictive zoning laws, and an influx in immigration. This is not an issue that will be solved in the medium term, allowing for a natural appreciation in property prices and an imbalance between supply and demand.

- Affordable Housing - Addressing the demand for affordable homes in key markets. ~55% of its Q3'23 sales were from its Smart Series, with a lower ASP of ~$418k.

- Technology Integration in the sales process- Embracing digital tools for virtual tours and home customization.

- Expanding Market Reach - Entering new markets (target market) and geographies (states) with growth potential.

- Energy-Efficient and Smart Homes - This aligns with market trends and addresses the growing demand for homes that are environmentally friendly and technologically advanced.

Notable threats

- Market Volatility - Sensitivity to economic downturns affecting housing demand. More long-term, how rates develop, and what the "new normal" level will be.

- Regulatory Changes - Adapting to evolving building codes and regulations.

- Labor Shortages - Impact on construction timelines and costs.

Economic & External Consideration

Homebuilders enjoyed a decade of expansion, owing to favorable economic conditions, namely low interest rates and a growing economy. This has changed during the post-pandemic period, as contractionary monetary policy has been initiated, with rates rising persistently for over 18 months.

This has contributed to a cost of living crisis alongside the impact of inflation, alongside a rapid increase in the cost of debt. As the following illustrates, the US affordability index has declined to a record low level and importantly, sits below 100, suggesting a strong restriction on the ability to finance a home.

Further, In the US, consumers are usually locked into long-term mortgages, a difference from many other nations such as the UK, meaning many are locked into record rates at a time when the 15Y mortgage rate has reached ~6%. This discourages moving home as consumers would potentially see a significant increase in their living costs.

Finally, the industry is experiencing a natural supply/demand shift, namely the costs associated with home ownership have increased, and thus demand has declined.

These factors are clearly not good for homebuilders. The number of Housing starts has flat-lined in recent quarters, while Home sales have persistently declined. We are not as concerned as some appear to be, however. The House price index remains positive, although admittedly has slowed, suggesting the bottom is not falling out of the market. It remains strong. Consumers are responding to these market conditions by holding onto their homes, suggesting an ability to withstand the pain (attributable likely to wage inflation). Further, we consider this a characteristic of the Home shortage, with consumers understanding the value of keeping their home.

With equity value maintained, Housing starts flatlining but not declining, and valuations remaining healthy, we believe the demand for homes will remain on an upward trajectory in the coming years. We do not see any fundamental damage caused by this downturn (such as post-GFC), and we expect there to be resilience in the market during 2024. Consumers may not be buying properties in droves in line with the last decade, but those who are willing to pay more, and the rest are sidelined awaiting a decline in rates.

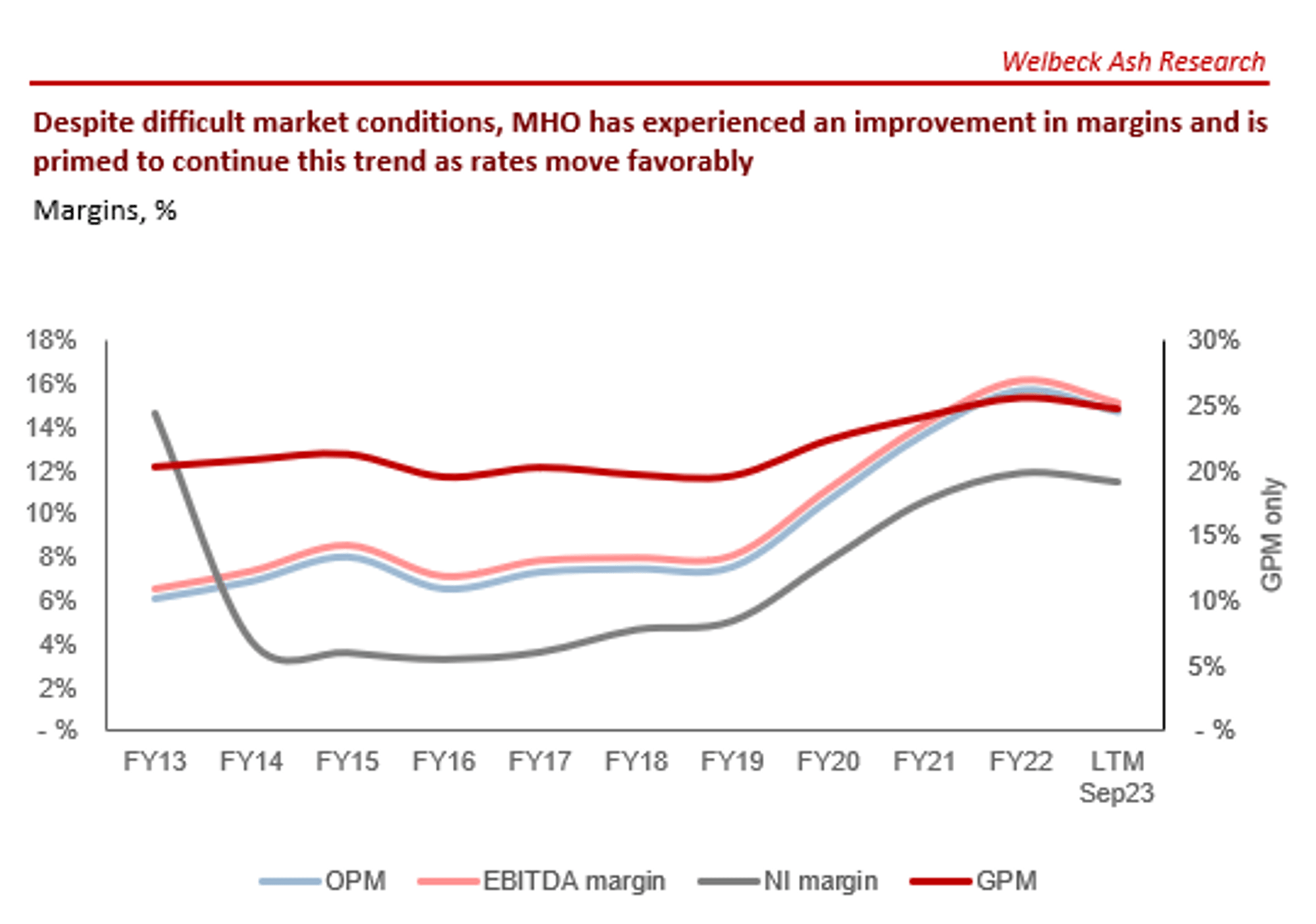

Margins

{kind=link}

MHO's margins have trended up during the last decade, with EBITDA-M more than doubling to 15% (+9ppts). This is a reflection of industry tailwinds contributing to superior unit economics on the revenue side (GM% +4ppts), alongside economics of scale from an operational perspective (S&A% of revenue +4ppts).

We suspect this trend will continue in the coming years, as the benefits of the tailwind accelerate. The gains may not necessarily be as aggressive, owing to competition and a natural equilibrium, however.

Quarterly results

MHO's top-line revenue growth was +15.7%, +16.2%, (2.6)%, and +3.3% in its last four quarters, reflecting healthy growth despite the wider conditions. In conjunction with this, margins have softened from their peak in FY22.

Average sales price declined only (1)% in its most recent quarter, while new contracts are up +50% (lower comparable period) and higher than Q3'21. The company appears to be increasingly experiencing a slowdown but continues to see resilience softening the impact.

Balance sheet & Cash Flows

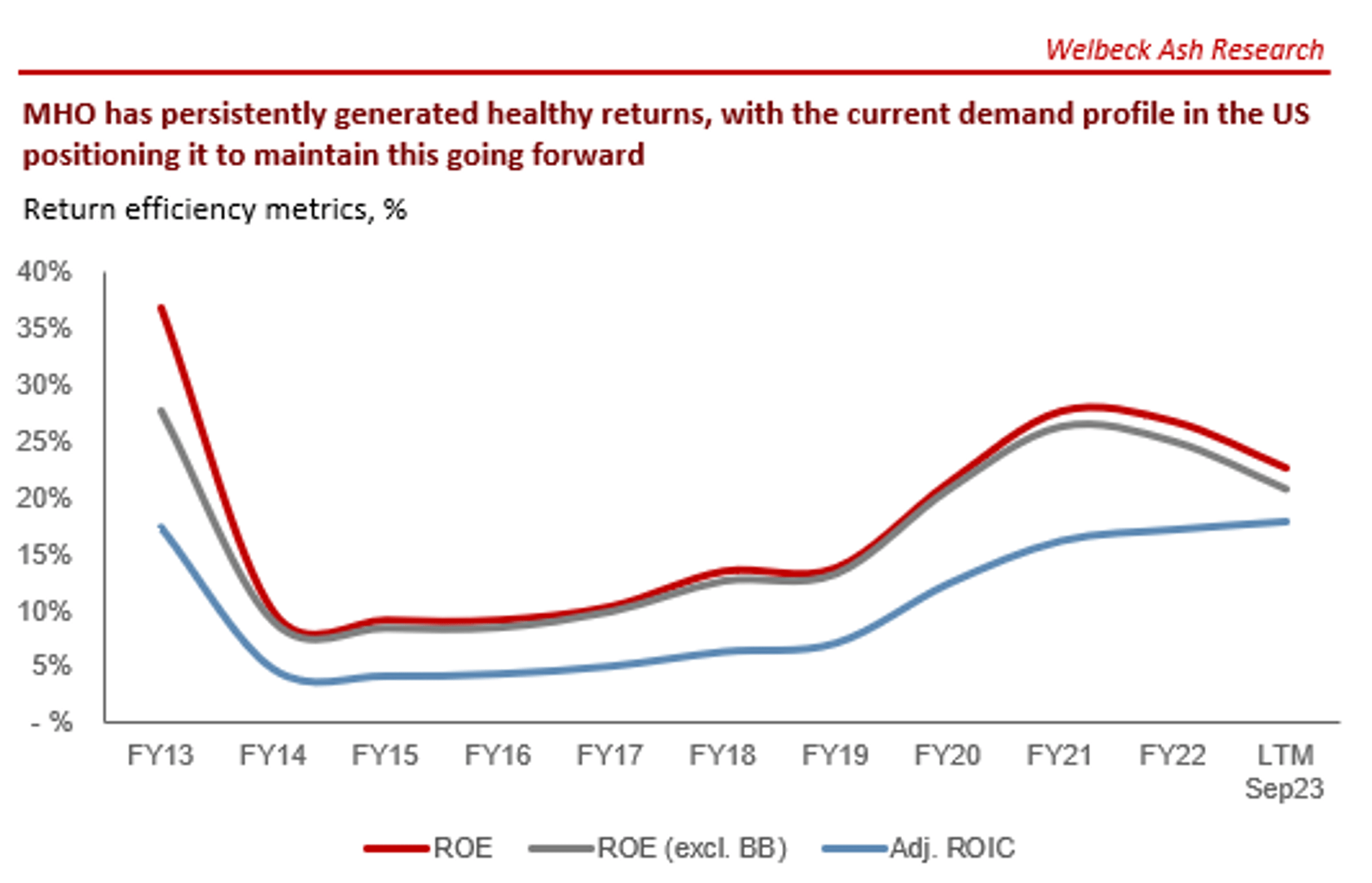

Growing margins and a conservative capital allocation approach have allowed MHO to grow its ROE, without the need for debt. The company has accumulated a significant amount of cash in the most recent period, as land acquisition has reduced. Assuming our expectation of a soft landing in 2024 is correct, investors may see some of this cash as a special one-off payment.

{kind=link}

Industry analysis

{kind=link}

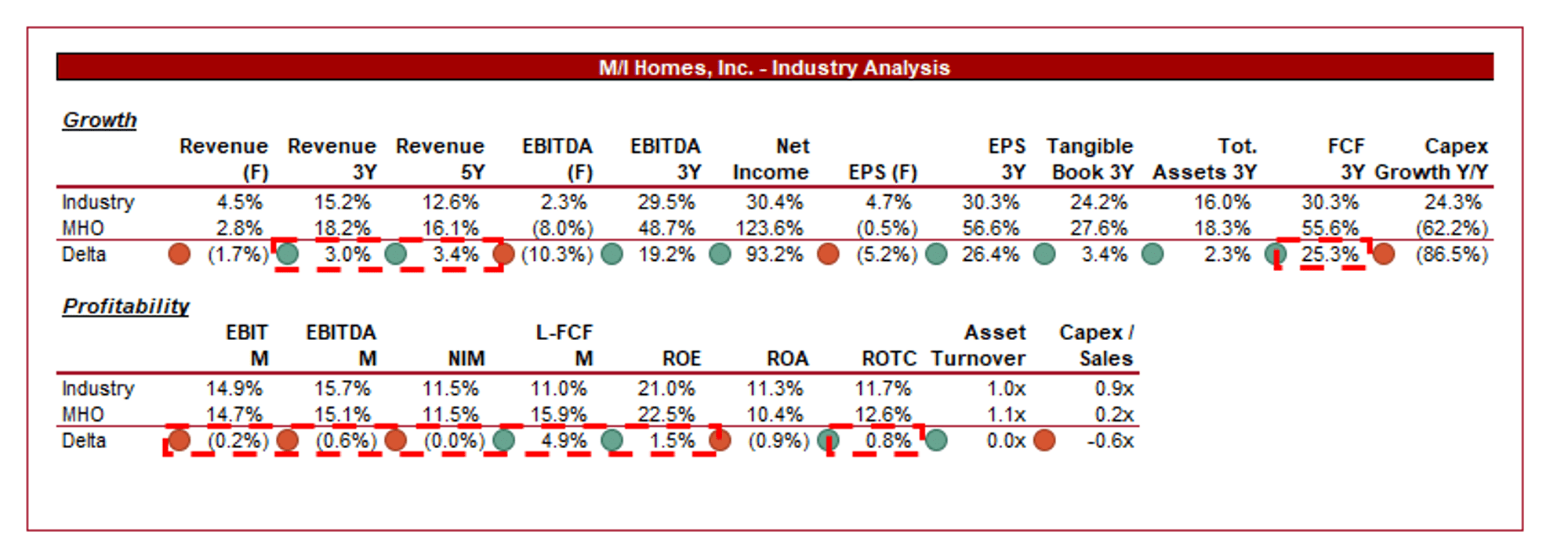

Presented above is a comparison of MHO's growth and profitability to the average of its industry, as defined by Seeking Alpha (23 companies).

MHO is performing well relative to its peers, with superior revenue and profitability growth across a 3Y and 5Y period, alongside similar margins. This has translated to a better ROTC/ROE.

Valuation

{kind=link}

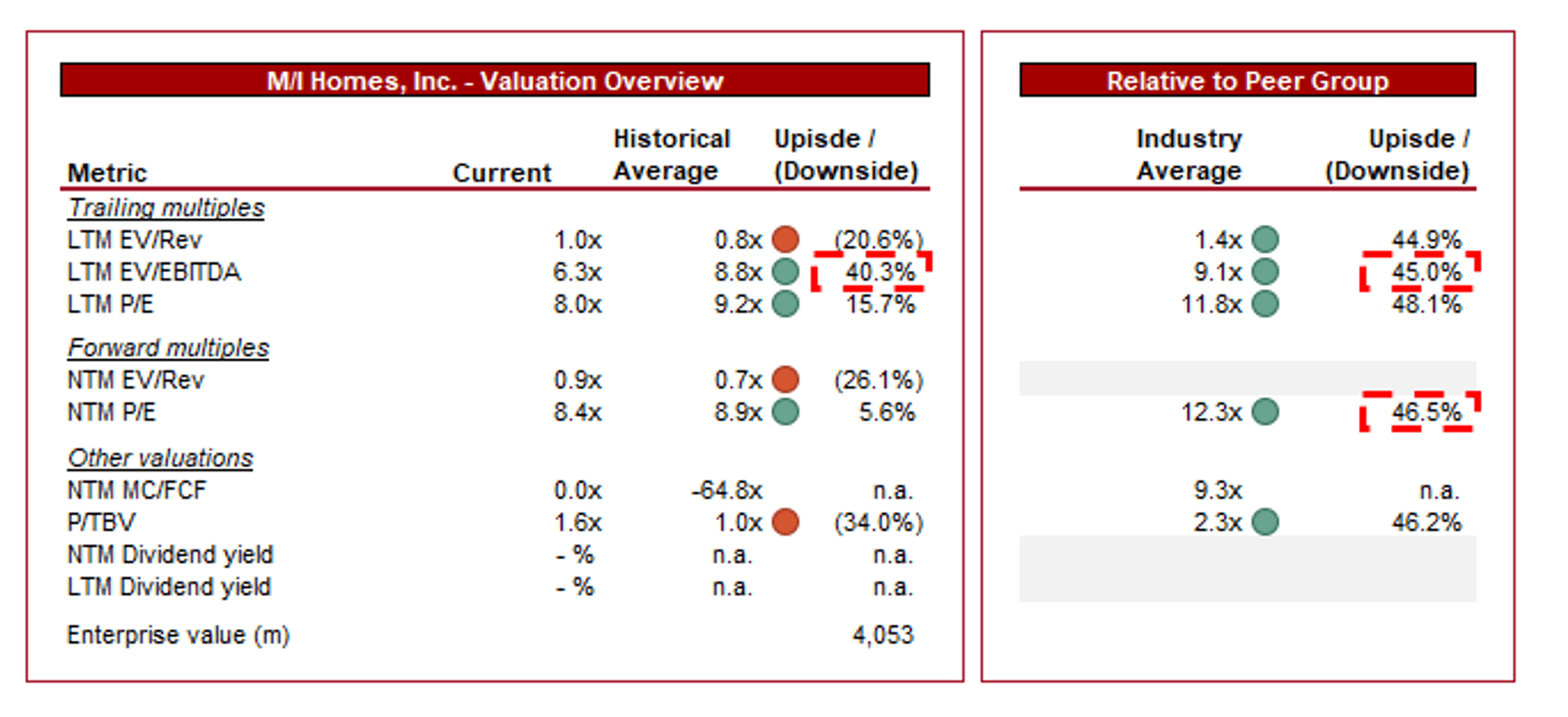

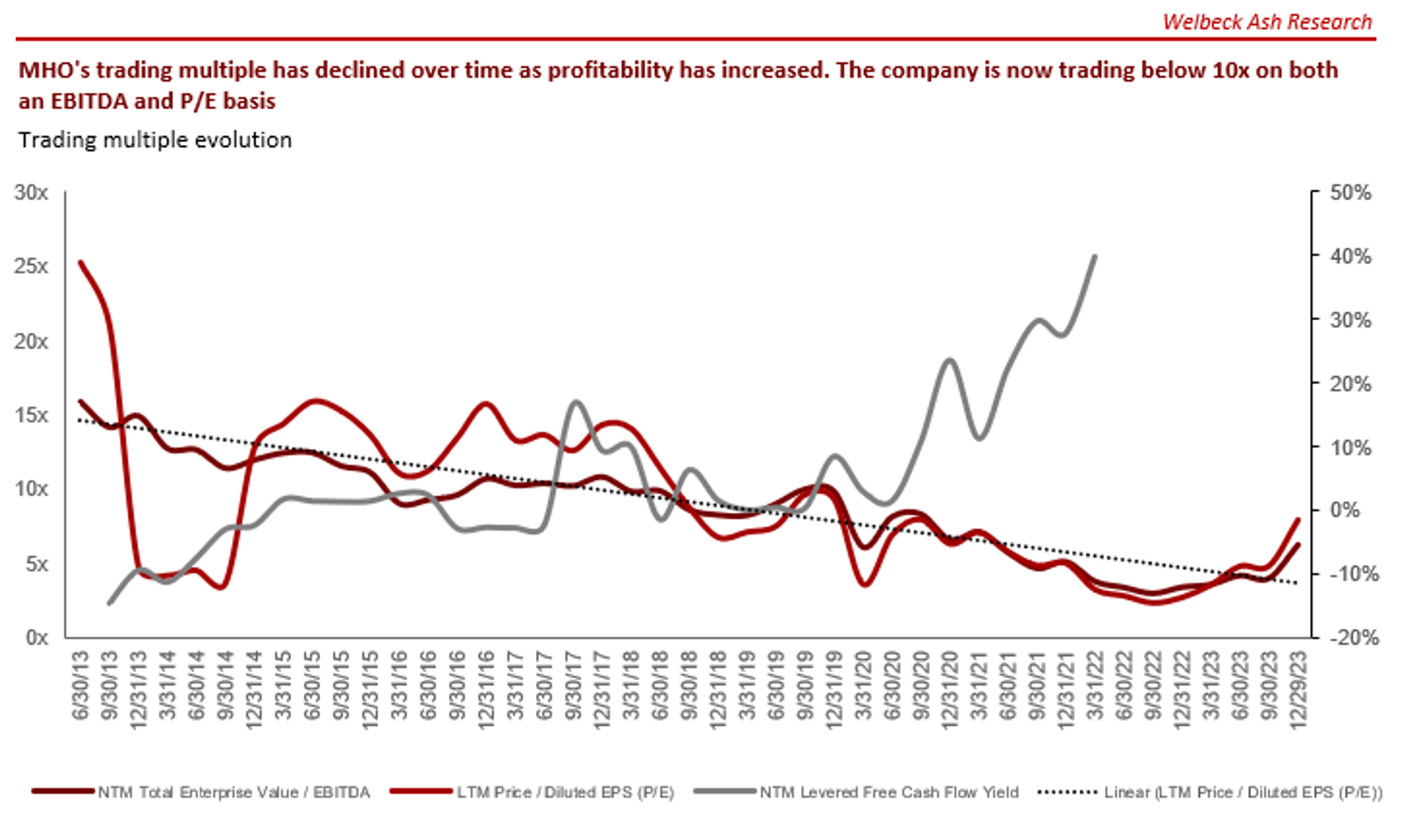

MHO is currently trading at 6x LTM EBITDA and 8x NTM P/E. This is a discount to its historical average.

A discount to its historical average is warranted in our view, primarily due to the uncertainty of long-term interest rates and developments in 2024. Beyond this, however, we believe the benefits of tailwinds, primarily the shortage of homes, appear to be a greater growth driver relative to historical levels. For this reason, we would only suggest a small discount, which does not appear to be the case.

Further, MHO is trading at a larger discount to its peers, in the region of 40-50% across all metrics. This is despite its strong financial performance and shared scope for further growth. We believe this discount is unjustified.

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- Greater than expected economic downturn affecting homebuyer confidence.

- Inability to reduce rates, restricting an expansion in demand.

- Supply chain disruptions lead to project delays.

Final thoughts

MHO is a high-quality business in our view, reflected in its strong growth and margin appreciation. The US housing industry is currently in a multi-decade shift, with prices soaring and supply falling behind. This is an issue that will drive value for MHO in our view.

The stock appears considerably undervalued relative to its peers and historical average while showing signs of a soft decline in 2024.

For further details see:

M/I Homes: Cheap Homebuilder Primed For Growth