MHO - M/I Homes: Still Building Value

Summary

- M/I Homes has done well recently, but investors are likely concerned about questionable market conditions and weaknesses the firm has pointed out.

- Short term, it is likely to see some pain, and that could result in near-term downside for shares.

- But given how cheap the stock is, both on an absolute basis and relative to other firms, now might be a good time to consider a stake in the business.

One lesson that I have learned over the years being invested in the market is that it can often make sense to buy into spaces that are the most unpopular at the time. Industries that come under pressure due to broader market conditions after experiencing pain from investors that is greater than what is often warranted. A great example of this that has played out nicely can be seen by looking at the home building space. And when it comes to one company, in particular, I would like to point out M/I Homes ( MHO ) as my example. Driven by attractive revenue growth and profit growth, not to mention robust cash flows, shares of the company have outperformed the broader market in recent months. Having said that, we are now still seeing signs of weakness that could impact the company in a negative way. I do believe that investors would be wise to keep a close eye on these changes. But given how cheap shares of the company are, I would still make the case that it warrants further upside moving forward. And because of that, I have decided to keep the 'buy' rating I assigned to the company previously.

Great results, but pain on the horizon

The last time I wrote an article about M/I Homes was back in early August of 2022. In that article, I talked about how cheap shares of the company were and I expressed amazement at the excellent operating history of the firm. I mentioned that strength for the enterprise was likely to continue through the rest of the year. But even back then, I mentioned that there were signs of pain for investors. Despite that pain though, I felt as though the upside potential outweighed the risk, resulting in my decision to rate the enterprise a 'buy' to reflect my view that it should outperform the broader market over time. Since then, the company has behaved in a manner that conformed with my own expectations. While the S&P 500 dropped 7.9%, shares of the home builder generated a return of 8.5%.

{kind=link}

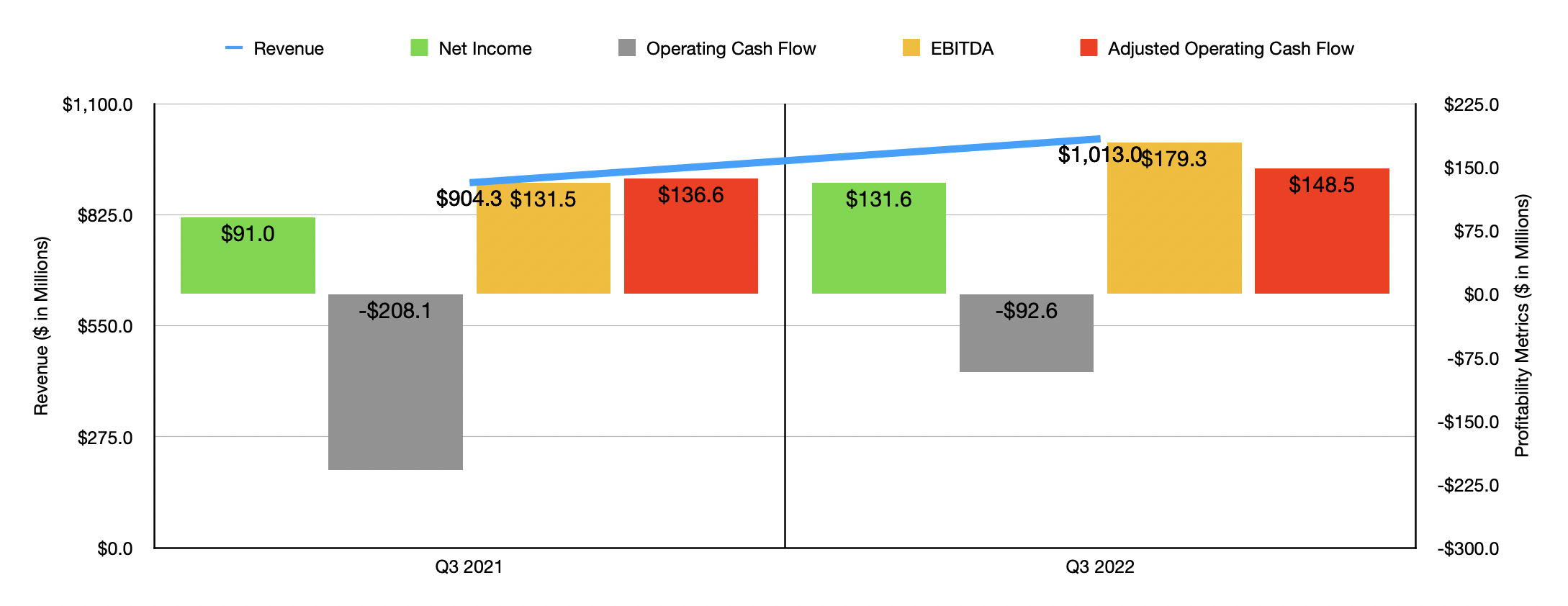

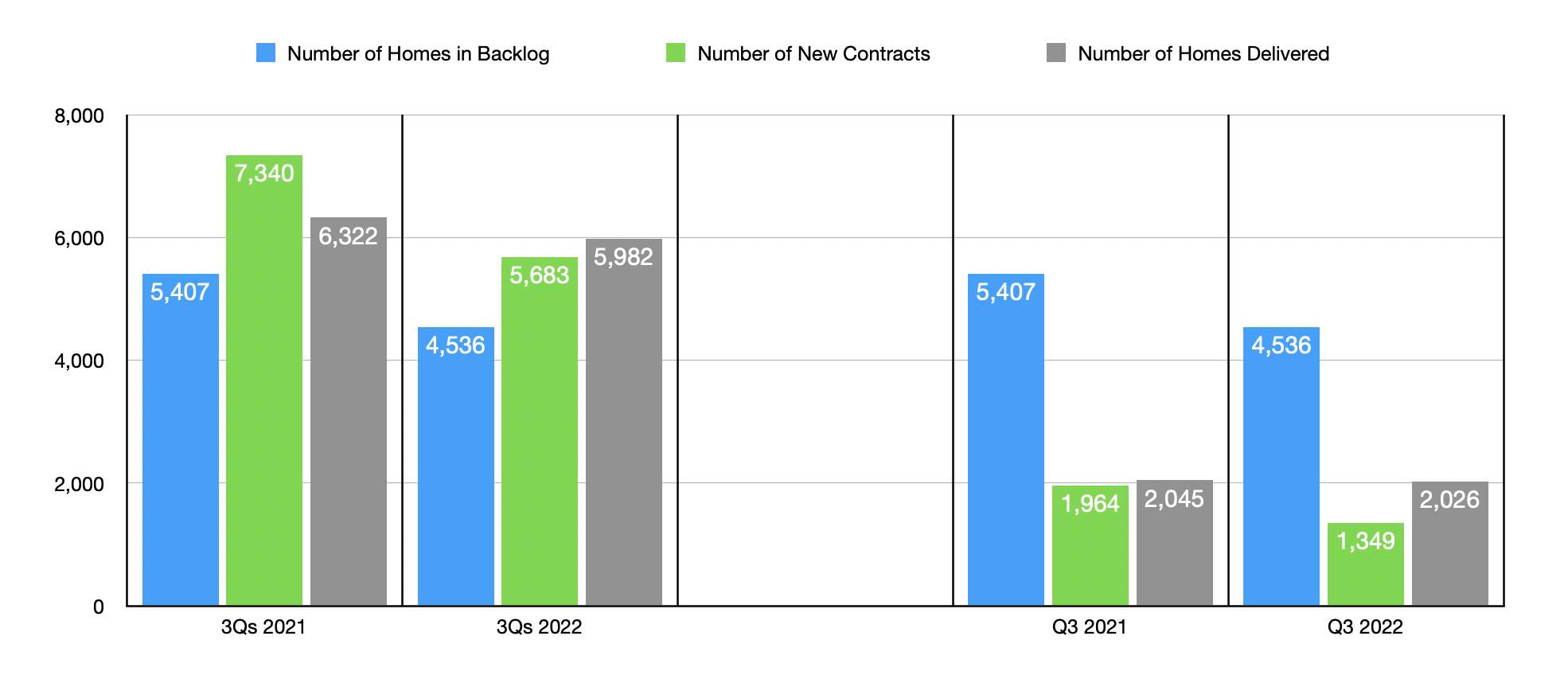

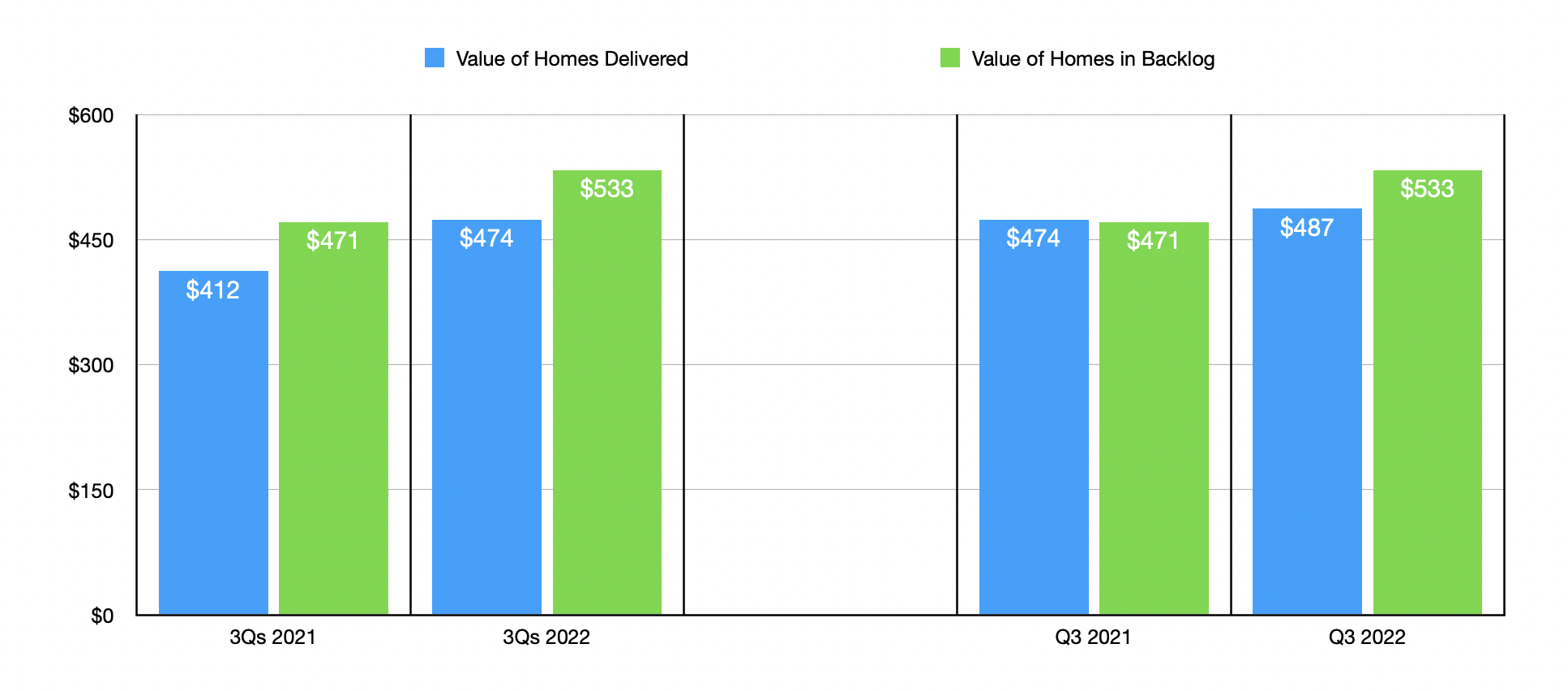

This return disparity has been driven by two facts. The first is that the company's fundamental performance has been robust. And the second is that shares look remarkably cheap right now. To see what I mean when it comes to fundamental performance, we need only look at data for the third quarter of the company's 2022 fiscal year. This is the most recent quarter for which data is available and it was not available when I last wrote about the enterprise. Sales then came in at $1.01 billion. That represented an increase of 12% over the $904.3 million generated the same time one year earlier. Even though the number of homes delivered for the company dropped year over year, falling from 2,045 to 2,026, the average price of homes delivered jumped from $474,000 to $487,000.

{kind=link}

{kind=link}

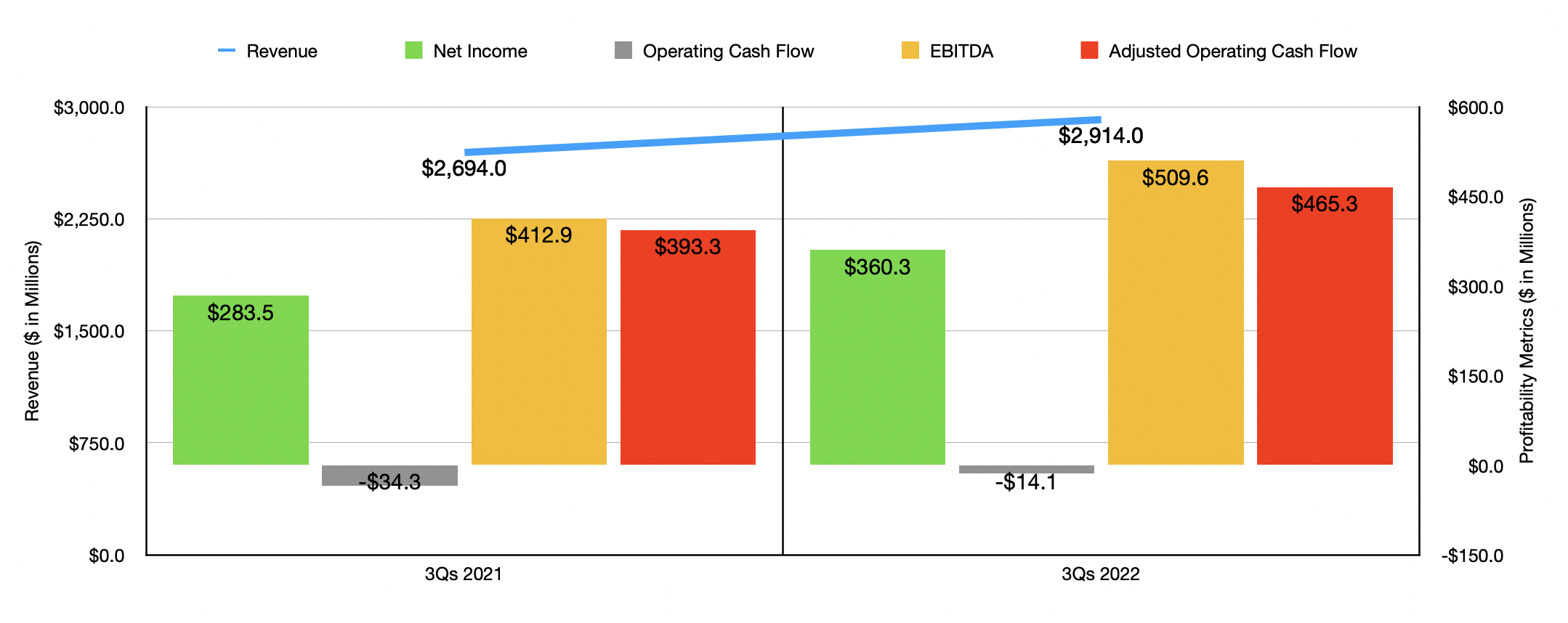

On the bottom line, the picture has also been favorable. Net income of $131.6 million dwarfed the $91 million reported the same time one year earlier. It is true that operating cash flow worsened, going from negative $208.1 million to negative $92.6 million. But if we adjust for changes in working capital, it would have risen from $136.6 million to $148.5 million. And over that same window of time, EBITDA also improved, rising from $131.5 million to $179.3 million. It's worth noting that fundamental performance in the third quarter followed a trend that existed for the first nine months of 2022 as a whole. Revenue of $2.91 billion beat out the $2.69 billion reported in the first nine months of 2021. Yes, the number of homes delivered fell during this time, dropping from 6,322 to 5,982. But the average price of homes delivered more than made up for this, soaring from $412,000 to $474,000. In response, net income shot up from $283.5 million to $360.3 million. In this case, operating cash flow did improve, turning from negative $34.3 million to negative $14.1 million. If we adjust for changes in working capital, however, it would have shot up even more from $393.3 million to $465.3 million. And over that same window of time, EBITDA also improved, jumping from $412.9 million to $509.6 million.

{kind=link}

All of this looks great. But there are signs of weakness building. In addition to the number of homes delivered falling, we have also seen a significant reduction in the number of new homes contracted to the company. In the latest quarter, that number came in at 1,349. That's down considerably compared to the 1,964 contracted one year earlier. For the first nine months as a whole, the number dropped from 7,340 to 5,683. What this shows is that, as time goes on, the number of new homes contracted on a year-over-year basis is worsening. That's an acceleration of pain. This has been instrumental in pushing the number of homes in the company's backlog down from 5,407 to 4,536. Perhaps the only positive here is that the average value of a home in the company's backlog is still up, totaling $533,000 compared to the $471,000 reported one year earlier. But given these other numbers, it's only a matter of time before this number starts to decline.

{kind=link}

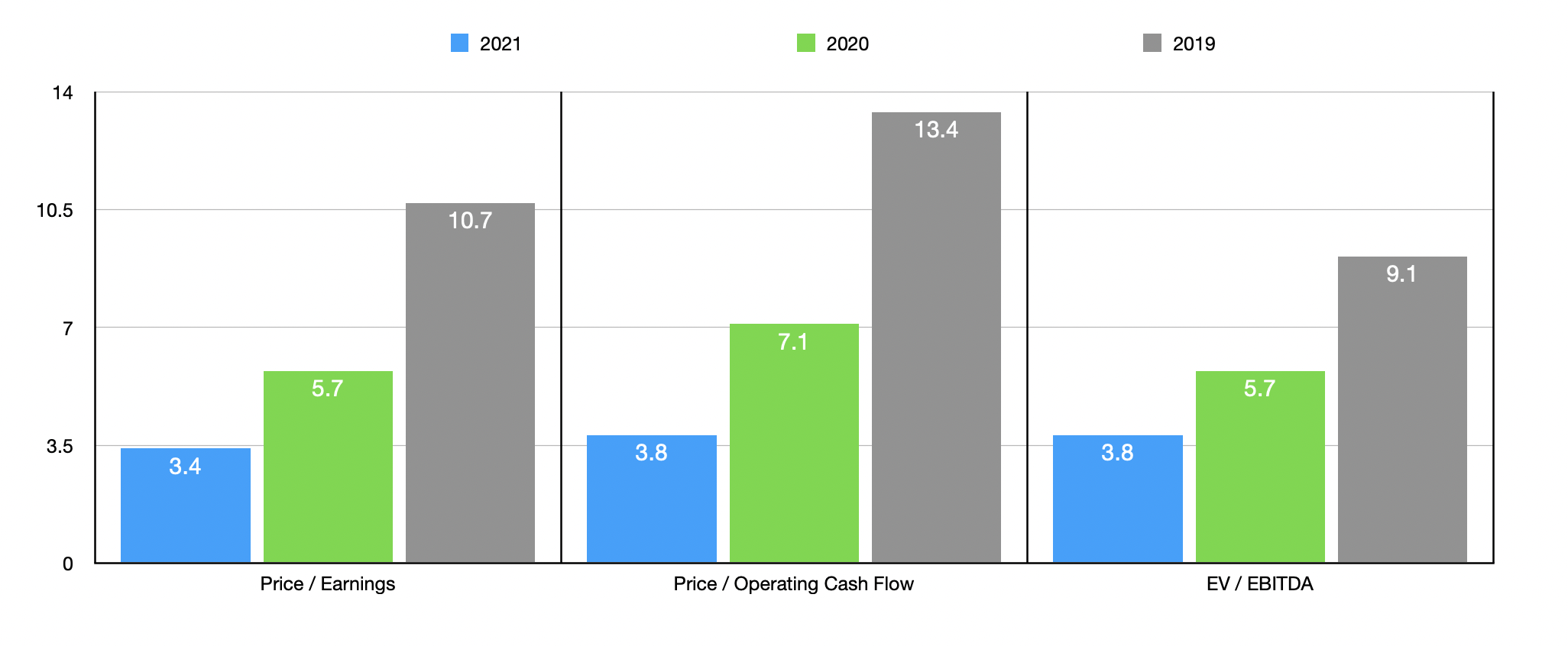

Clearly, the rise in interest rates that we are seeing, as well as other uncertain economic conditions, are playing a role in this pain. To many investors, this would be a sign to sell and go look for returns elsewhere. But the fact of the matter is that shares of the company look incredibly cheap even if the business deteriorates to some degree. As you can see in the chart above, the stock looks very cheap if we price it based on data from 2021. I didn't do a 2022 analysis because I know that current conditions will worsen from here. But if we were to have done that, then the stock would look even cheaper still. Even if you look back to 2019, however, shares were not unrealistically priced on an absolute basis. Not only are shares cheap on an absolute basis. They are also cheap relative to similar firms. As you can see in the table below, where I compared the company to five similar firms, the enterprise is the cheapest of the group when it comes to the price-to-earnings approach to valuing the business, the price to operating cash flow approach, and the EV to EBITDA approach.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| M/I Homes |

| 3.4 |

| 3.8 |

| 3.8 |

| Green Brick Partners ( GRBK ) |

| 8.2 |

| 44.3 |

| 8.2 |

| Dream Finders Homes ( DFH ) |

| 15.7 |

| 28.5 |

| 14.6 |

| Century Communities ( CCS ) |

| 5.6 |

| 25.7 |

| 5.6 |

| Tri Pointe Homes ( TPH ) |

| 6.8 |

| 7.6 |

| 5.8 |

| Beazer Homes USA ( BZH ) |

| 4.9 |

| 25.0 |

| 8.9 |

Takeaway

I would be in the wrong if I told you I didn't think that industry conditions for companies like M/I Homes will only worsen before they get better. It would take a miracle to change that. Having said that, the company does look cheap even if operations worsen from here. Obviously, if it goes into a multi-year spiral, that could be a different matter entirely. But given how cheap shares are relative to other firms in the space, I would say that it makes for a solid prospect for those who feel confident about the home-building market for the long haul. For that reason, I've decided to keep the 'buy' rating on the firm for now.

For further details see:

M/I Homes: Still Building Value