MTB - M&T Bank: Conservative Bank's Valuation At GFC And COVID Lows

2023-04-03 16:24:00 ET

Summary

- Regional banks have been crushed by the Silicon Valley Bank fallout.

- M&T Bank is one of the safer choices in this space, and valuations are reasonable.

- We examine the setup, the risks, and the preferred shares.

When we covered M&T Bank ( MTB ) we suggested a defensive trade to get involved rather than chasing the stock up. We aimed to get a net price near $112.00 a share and got paid a hefty yield for the effort.

To create a rather wide level of buffer, as we always do for conservative income plays, we aim to only go long MTB if we got it at an extremely attractive price. This, to us, was somewhere near the 1.4X price to tangible book value level. With that in mind, we sold the $120 Cash Secured Puts for $740 each. This created a nice buffer and a good yield which we would get paid, just for putting in our bid.

Author's App

Source: Quality Regional With Room To Grow Its Dividend

The stock had a rather fascinating journey since then. It bottomed right around the time we sold those puts and then leaped over $180 shortly thereafter. Since it was nowhere near the $120.00 mark on options expiration, we pocketed the entire premium. Of course, we are writing about it today as it has come back down to a shade under $120, the very strike we had chosen previously.

Recent Developments

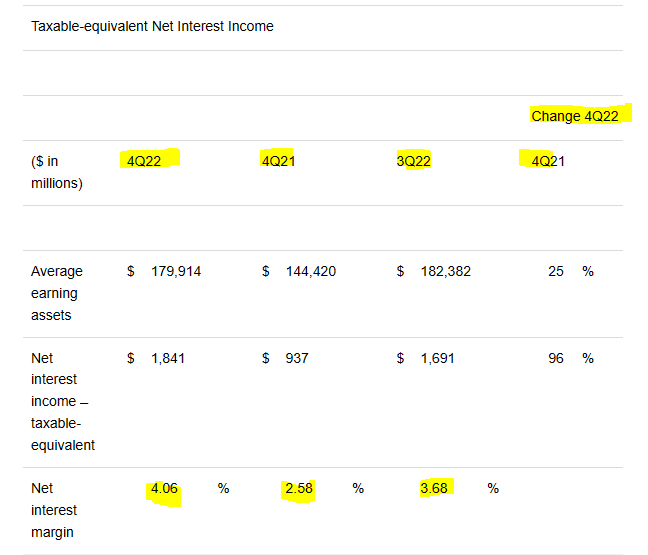

MTB's reported Q4 2022 results seem like a lifetime ago, but they are the best starting point for the analysis. The bank reported solid results and crushed estimates by 13 cents a share ($4.57 non-GAAP EPS vs $4.44 expected). The provision for credit losses was just $90 million, and the company progressed on integrating its acquisition of People's United Financial, Inc. That purchase was completed in Q2-2022 , so the year-over-year comparisons are not necessarily the best reflection of the growth, but the change from Q3-2022 was telling. Net interest margins expanded rapidly to 4.06% from 3.68%.

{kind=link}

Those are some astounding numbers, and analysts are likely extrapolating that for the year ahead.

{kind=link}

Of course, there are a few problems with that logic, as we shall see.

Outlook

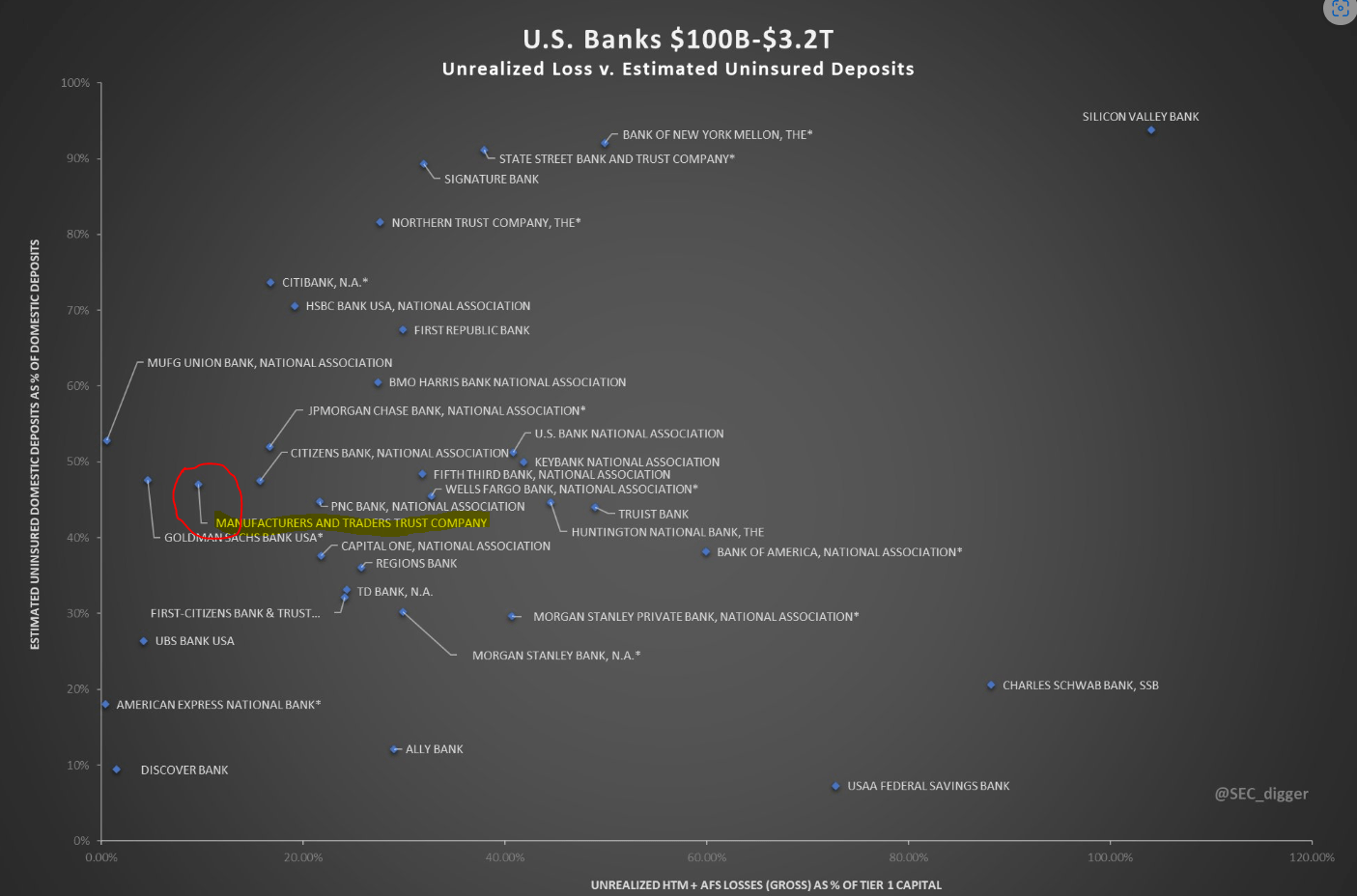

As a regional or rather a superregional bank, MTB has come under the same scrutiny on its held to maturity assets. In this regard, the bank fares better than most. You can open the image in a new tab to see where our regional banks stand relative to Silicon Valley Bank ( SIVBQ ) (top right corner).

{kind=link}

MTB's position here is about as fantastic as it can get when you weigh uninsured FDIC deposits (the gasoline, if you will) vs the losses on the held-to-maturity portfolio (the tinder). The gasoline and the tinder are the requirements for a bank run, and MTB has both in short supply. Only a few banks did better on both criteria, and they generally don't do retail banking. Let's look at that in another way. Here, the offset is how bad the tier 1 capital ratio would get if we adjusted for these mark-to-market losses.

JPM

MTB again looks fantastic, in line with JPMorgan ( JPM ) and far better than Bank of America ( BAC ) and the regional banks.

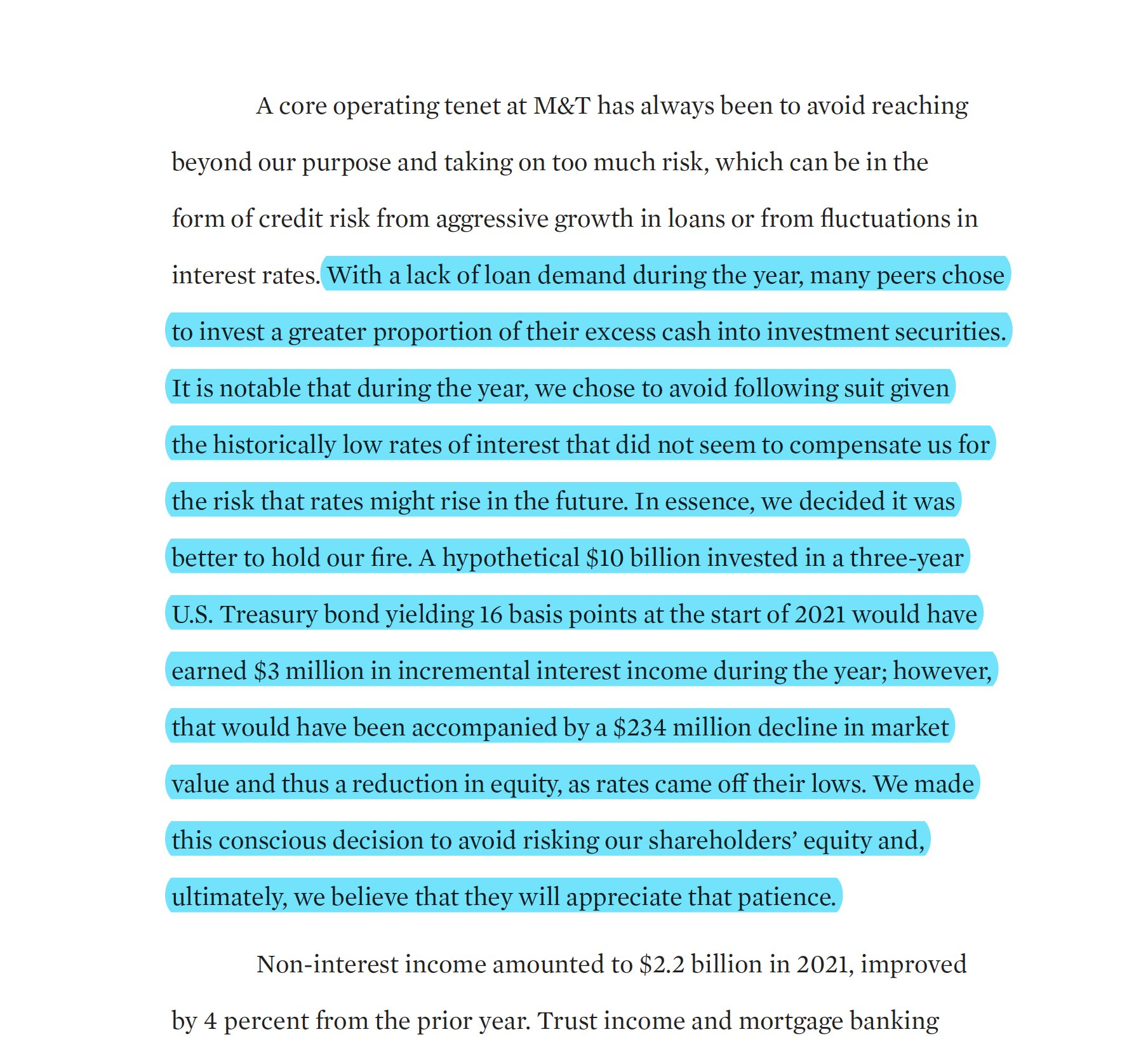

How did MTB come out so unscathed? Well, they do serve the smaller customers, so more deposits fall under the FDIC blanket. That is not something you can give them extra credit for. But they did really, really dial back the risk on the held to maturity side. Here is a snippet from their annual report. Source: Maxfield on Banks - Twitter

{kind=link}

Oh, we do certainly appreciate the patience. Just like our investment philosophy of avoiding chasing return-free risk for the fun of it, MTB dodged some major landmines. So from a bank-run and existential threat perspective, there is really nothing to worry about.

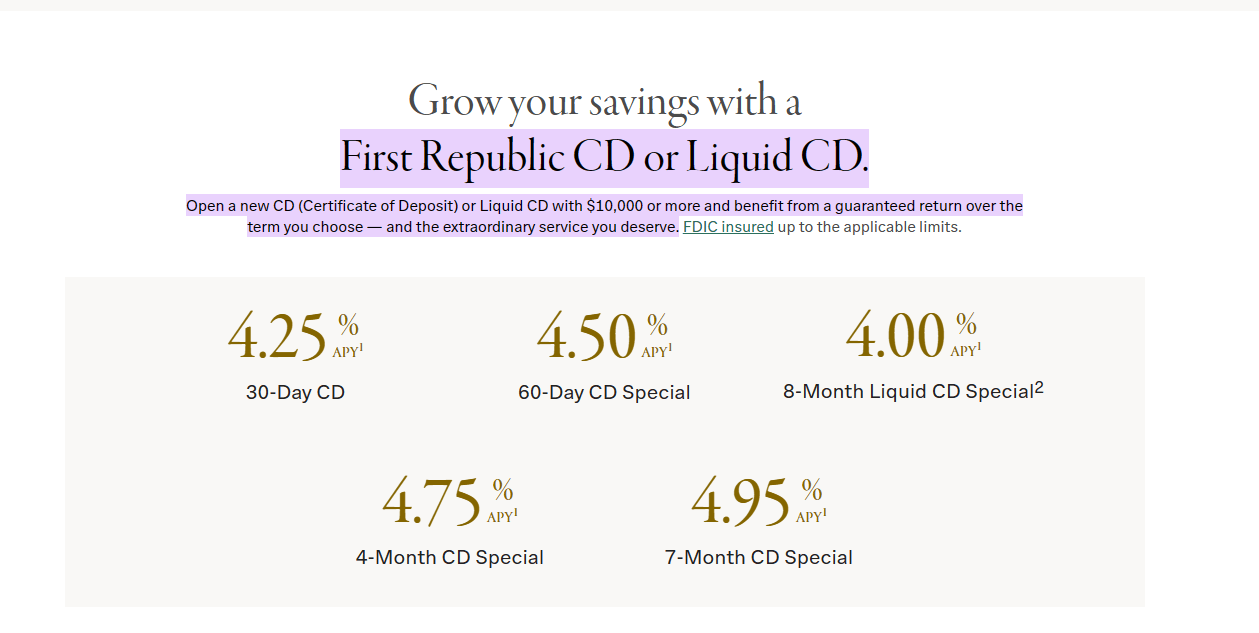

That said, they do have to find a way to retain deposits. While deposits may not run to other banks, they will run to money markets. Here is a wonderful annotated chart from Jeff Weniger making this point.

Jeff Weniger

So, this is likely to play on everyone's income statement. Even the distressed First Republic Bank ( FRC ) woke up to this realization. The 7-month special looks like it might entice a few to stay a little longer.

{kind=link}

Our take is that everyone's earnings estimates for 2023 as far as the banks go are too optimistic. We are likely to see the low-end run-rate ($3.00 per share per quarter) by Q4 2023. This is excluding write-offs from a potential recession.

Verdict

Even at $12.00 in earnings per share, you could argue that MTB is cheap. We will certainly agree if that is likely to be the trough run rate. Financials trade cheap for a reason, and that reason is that some of them frequently blow up and are forced to issue equity at bad prices. Here is a 23-year chart on Citigroup Inc. ( C ) to make our point.

But MTB is likely to dodge such a fate, and their conservative behavior helps bolster that stand. It is also extremely cheap on our favorite metric.

On a price to tangible book, it is swimming right near the global financial crisis and COVID-19 lows. We think a covered call or cash-secured put strategy makes sense for those wanting to use the volatility to their advantage.

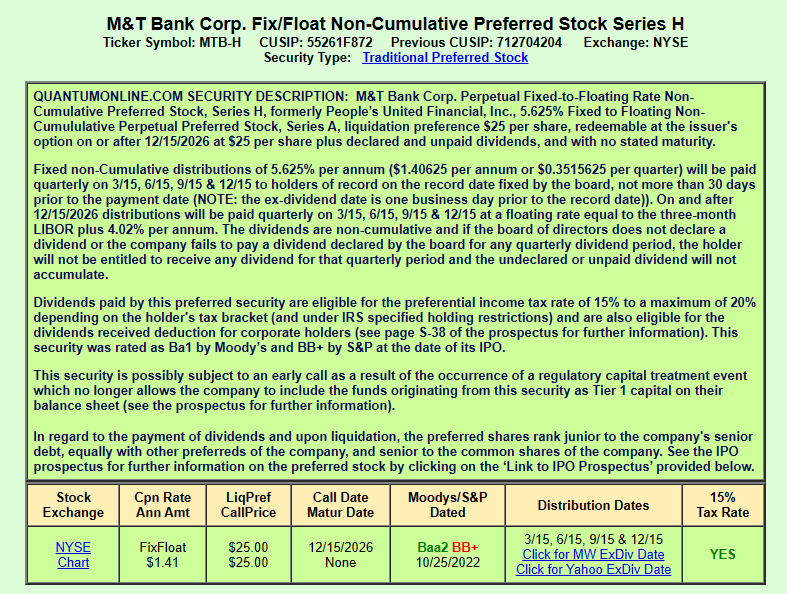

M&T Bank Corporation FIX TO FLT PFD H ( MTB.PH )

While our discussion here has been focused on the common shares, we want to also touch upon the preferred shares. MTB.PH is a fixed to float issue that is currently on the fixed portion of its journey. It pays a qualified dividend of 5.625%.

{kind=link}

The interesting aspect here is that the spread to LIBOR is quite strong at 4.02% and that might make sense for those that believe we have entered a new interest rate regime. If we never go back to ZIRP, then these preferred shares make sense. For our part, we think that option trades on the common shares should produce far higher income with equivalent risk compared to the preferred shares. We are definitely not buying these at current levels.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

M&T Bank: Conservative Bank's Valuation At GFC And COVID Lows