MAC - Macerich: Downgrading To Hold After Q2 Results

2023-08-10 11:18:52 ET

Summary

- In March 2023, The Macerich Company was labeled as a buy due to its underperforming share price, improving financials and depressed P/FFO multiple.

- Since then, MAC has outperformed its closest peer, Simon Property Group, and the broader REIT market, delivering total returns close to 40%.

- Q2 2023 results show robust performance, although relatively muted compared to the significant recovery from COVID-19 in the past year.

- The recent quarterly results indicate that MAC's key issue - excessively high debt load - has increased (net debt to EBITDA reaching 10x). This year and in 2024, MAC has to refinance more than 25% of its total debt.

- Considering MAC's shallow liquidity reserves, tight lending conditions, excessive leverage, and unfavourable effects from interest rate repricing, I am downgrading MAC to a hold.

Back in late March 2023, I issued an article on The Macerich Company ( MAC ) labeling the Company as a buy - Macerich: Secure 7% Yield With A Room For Price Appreciation .

The key drivers of my thesis were a combination of the following:

- Despite a notable restructuring process in 2020, the share price was drastically underperforming its closest peers such as the Simon Property Group, Inc. ( SPG ).

- While the share price remained somewhat flat, the underlying performance was clearly improving, with growing FFO figures and the balance sheet gradually becoming less indebted.

- Price to estimated ((FWD)) FFO multiple at that time was 5.2x - considerably depressed is both in absolute and relative terms when compared to direct peers.

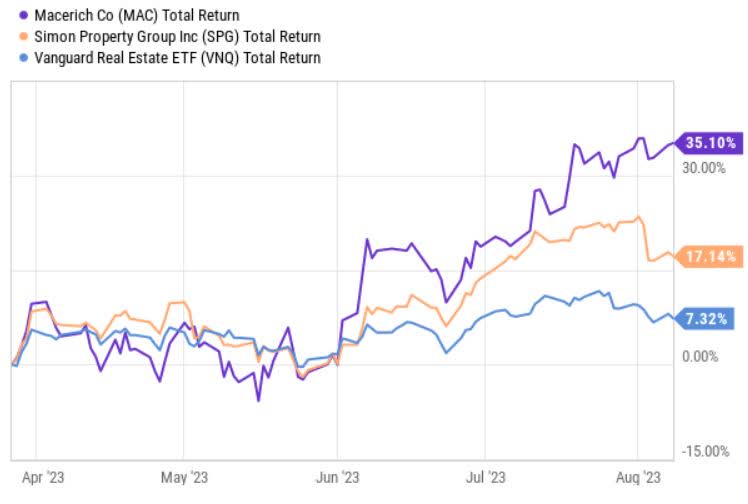

Looking at the total performance charts, the thesis has played out rather nicely.

{kind=link}

Ycharts

In a roughly 4-month period, MAC has outperformed its closest peer, SPG, and registered significantly stronger performance compared to the broader REIT market. Most of the MAC's returns have been explained by the multiple expansion in conjugation with improvements on the FFO side.

Just recently MAC circulated Q2, 2023 results , which in the context of the recent run-up in the share price make a solid case for having another detailed look at the thesis and seeing whether a "buy", in my opinion, remains intact.

Synthesis of Q2 results

The overall performance of MAC has been robust, with all of the key metrics showing resilient dynamics and structural growth. However, given that the past year and comp. quarters were characterized by a significant recovery from COVID-19, where physical retail sales came back with a vengeance, this year's results look relatively muted.

In Q2, MAC delivered FFO (excluding financing expense in relation to Chandler Freehold) of $0.40 per share, compared to $0.46 per share for the quarter ended June 30, 2022.

The like-for-like NOI, however, increased by 5.6% in Q2 compared to the second quarter of 2022, which translates to a YTD growth of a solid 5.2%. The key driver for this was rather robust spread levels on the re-leasing front. On a YTD basis, MAC managed to negotiate leases at rents, which were 11.3% greater than expiring base rents. Moreover, the fact that these juicy spread levels were achieved over a notable amount of square footage (191 leases) sends a strong message that currently the supply/demand dynamics are clearly in favor of MAC.

Some part of the overall uptick in the like-for-like NOI was attributable to the embedded rent escalators, but these are relatively minor in the context of the total growth.

Form 10-Q for Macerich

A point of caution here is the sales per square foot figure, which has assumed a declining trend since the end of 2022. There are several factors, which contribute to the decline such as tough base value, tenant recycling, and slightly deteriorating demand in certain malls. In the context of solid lease spreads and improving like-for-like performance, this is not really a concern. If the decline will still persist, then this obviously will become a problem, especially in relation to successful lease renewals.

The portfolio occupancy continued to tick higher, reaching 92.6% as of Q2, 2023 (or a 0.4% increase on a quarter-on-quarter basis).

If we look at the state of MAC's capital structure, the story is not that positive. Here the total outstanding debt has actually increased relative to both Q1, 2023, and Q2, 2022. As of now, the net debt to EBITDA stands at just over 10x and ~73% of the market total capitalization. This is extremely high - e.g., the retail REIT sector has an average net debt to EBITDA of 5.5x.

The most concerning issue is the underlying structure of MAC's debt maturities, where a significant chunk comes due in 2024 (~25%). And this is on top of $700 million that has to be still refinanced this year.

{kind=link}

Form 10-Q for Macerich

The key risk of this lies in the overall access to financing, considering the prevailing tightness in the lending markets and overall pessimism among financers to lend to interest rate-sensitive sectors. Usually, such risks are mitigated by holding ample liquidity reserves. As of Q2, MAC had ca. $565 million of liquidity, which consisted primarily of a $405 million unutilized revolver.

This is considerably below the amount of maturing debt, which in vibrant lending conditions might be acceptable. Yet, again, taking into account the size of maturing debt and the harsh lending environment, such a gap between the actual refinancing need and the available liquidity is very risky.

Another problem that is associated with the aforementioned debt rollovers is the cost of financing aspect. Namely, these loans, which are set to fall due relatively soon, are currently stipulated on fixed interest rates - on average at 4.8%. Upon the refinancing event, they will per definition become subject to the current interest rate levels and be repriced accordingly.

For context, the total interest rate for MAC's revolver was just above 9%. At this point, it is hard to estimate the exact cost of financing for MAC's resigned loans, but one thing is for sure - the weighted average interest rate will sharply increase.

The bottom line

Since the publication of my bull thesis roughly 4 months ago, MAC has delivered alpha performance exceeding the results of the broader REIT market and its closest peer, SPG. The underlying performance has remained resilient, with strong like-for-like growth.

However, considering that there is significant uncertainty and risks stemming from the massive debt maturities that are right around the corner, I am downgrading MAC to hold. In my opinion, MAC's liquidity reserves are too shallow, the maturing debt amount is excessively high in the current lending environment and the incremental uptick in the cost of financing will render a very painful effect on the FFO generation.

Lastly, the recent run-up in the share price has caused P/FFO multiple to increase accordingly, since most of the gains were explained by the multiple expansion and not improving the FFO figure. While a P/FFO of 7.2x is still somewhat low, I do not consider it attractive enough when factoring in the aforementioned risk exposures. Going short is also out of the questions because the multiple is still fairly low, and the underlying performance remains resilient.

For further details see:

Macerich: Downgrading To Hold After Q2 Results