MAC - Macerich: U.S. Malls Are Not Dying

2023-09-20 05:24:31 ET

Summary

- Macerich has fallen by 70% over the last 5 years on a total return basis on the back of a bearish thesis that is increasingly not playing out.

- The REIT is comparatively undervalued, trading 45% lower than its peers on a price to trailing 12-month funds from operations basis.

- Record leasing volumes and rising occupancy rates indicate a strong post-pandemic rebound and a revival of US malls.

The malls are dead drum has been beaten so much over the last decade for good reason as the rise of other e-commerce and players like Amazon set up a new perpetual zeitgeist where spending flowed away from brick-and-mortar retailers to the dot coms. There have been casualties with Pennsylvania Real Estate Investment Trust ( PRET ), CBL Properties, and Washington Prime Group all filing for bankruptcy in recent years. Hence, the universe of mall REITs has slimmed dramatically with Macerich ( MAC ) and Simon Property Group ( SPG ) being the only remaining relevant public mall REITs. However, the performance dichotomy between both tickers could not be more marked with SPG down 17% over the last 5 years on a total return basis and Macerich nursing negative total returns of around 70%.

{kind=link}

Macerich is swapping hands at a 6.6x price to trailing 12-month funds from operations, around 45% lower than the median from its retail REIT peer group. There are a number of reasons for this underperformance from a dividend that's 58 cents lower than its 2019 level to a tangible book value per share that is under sustained pressure. Macerich last declared a quarterly cash dividend of $0.17 per share , in line with its prior distribution and for a 5.7% annualized forward yield. The income is the prize and Macerich's underlying operations are currently underway with a revival as leasing volumes ramp up and mall foot traffic picks up from its pandemic slump.

Record Leasing Volumes And Rising Occupancy

Foot traffic to US Class A malls, destinations with sales per square foot in excess of $500, is rising. This growth came in at 12% in 2022 versus 2019 with Macerich reporting record leasing volumes for the first half of its fiscal 2023 with 2.4 million square feet of leases signed, a 34% increase from the year-ago comp. The REIT signed 191 leases for 1.4 million square feet for its second quarter with portfolio-wide occupancy hitting 92.6%. Critically, this was an 80 basis points increase in occupancy from its year-ago quarter as re-leasing spreads grew markedly to reach 11.3%. An occupancy rate above 92% is a strong sign of good health and ranks favorably to occupancy of 94.7% at Simon Property Group's US malls and premium outlets.

{kind=link}

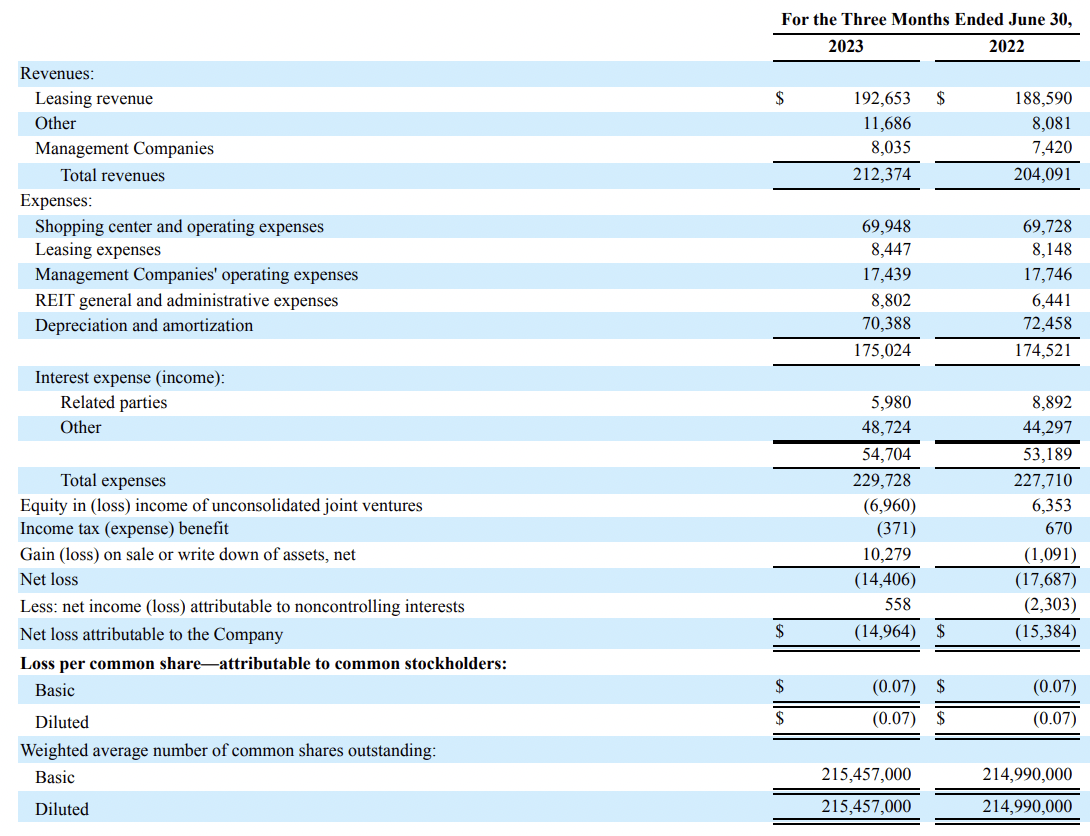

Macerich's portfolio average sales per square foot for tenants under 10,000 square feet was $853 , a slight decrease from $860 in the year-ago quarter mainly due to lower EV sales. So we've seen record leasing volume set against sales per square foot at highs with revenue for the quarter coming in at $212.37 million , a 4.1% increase from its year-ago quarter and a beat by $1.54 million on consensus estimates. Rental revenue is set for further growth on the back of 263,000 square feet of new stores opened during the second quarter and a leasing pipeline of new store openings that will drive nearly $66 million of incremental rent in the aggregate to be realized over the next two years.

What's The Outlook As FFO Expands?

The REIT did report a net loss of around $15 million, around $0.07 per share, with FFO coming in at $88.7 million or around $0.40 per share. Bears would be right to flag that FFO dipped by around $0.06 per share year-over-year and that higher interest expenses drove most of this decline like most other REITs on the back of a Fed funds rate currently sitting at 22-year highs of 5.25% to 5.50%. However, Macerich's pace of interest expense increase was relatively modest $54.7 million of interest expenses realized during the second quarter only rising by 2.85% from its year-ago comp. The REIT also had $565 million of liquidity as of the date of filing its second-quarter earnings report with around $405 million of this being constituted by available capacity on its $525 million revolving line of credit. This bore interest at SOFR plus a spread of 2.36% and matures on April 14, 2024.

Second quarter FFO covered the dividend by around 235% with Macerich guiding for its full year FFO, also excluding Chandler Freehold financing expense, to come in at $1.77 to $1.83 per share. The bull case now rests on the marked difference Macerich is trading at against its historical trading multiples. The REIT's price to free cash flow multiple has dropped to its second lowest-ever level, only surpassed by the early pandemic crash when stay-at-home orders catalyzed a collapse of brick-and-mortar retail foot traffic and Macerich's dividend. This relative undervaluation comes against continued leasing strength and double-digit re-leasing spreads. I'd like to initiate a position once FFO is no longer clearly dipping on a year-over-year basis and the Fed's interest rate hikes move into the rearview mirror.

For further details see:

Macerich: U.S. Malls Are Not Dying