AEM - Macro Developments Could Send Agnico Eagle Shares Flying

2023-11-07 13:14:08 ET

Summary

- Gold prices have room to rise as investors expect the Fed to cut rates in the future.

- Agnico Eagle Mines is a strong gold company that has the potential to outperform.

- AEM's recently released earnings show strong financial results and a positive outlook for exceeding production guidance.

Introduction

It's time to talk about gold. In the current macroeconomic environment, it may be one of my favorite metals to monitor.

Why?

Because it tells us so much about what investors expect the Fed to do in the not-too-distant future.

Gold prices are not always easy to predict. While gold is a great long-term hedge against inflation, it tends to trade as if it has a mind of its own in the short term.

The (not updated) chart below shows the (negative) correlation between gold futures and the expected Fed Funds rate two years from now. As we can see, gold tends to rise when investors expect rates to come down in the future. That makes sense, as it would lower interest rates on the dollar, which competes with gold.

CME Group (Not Updated)

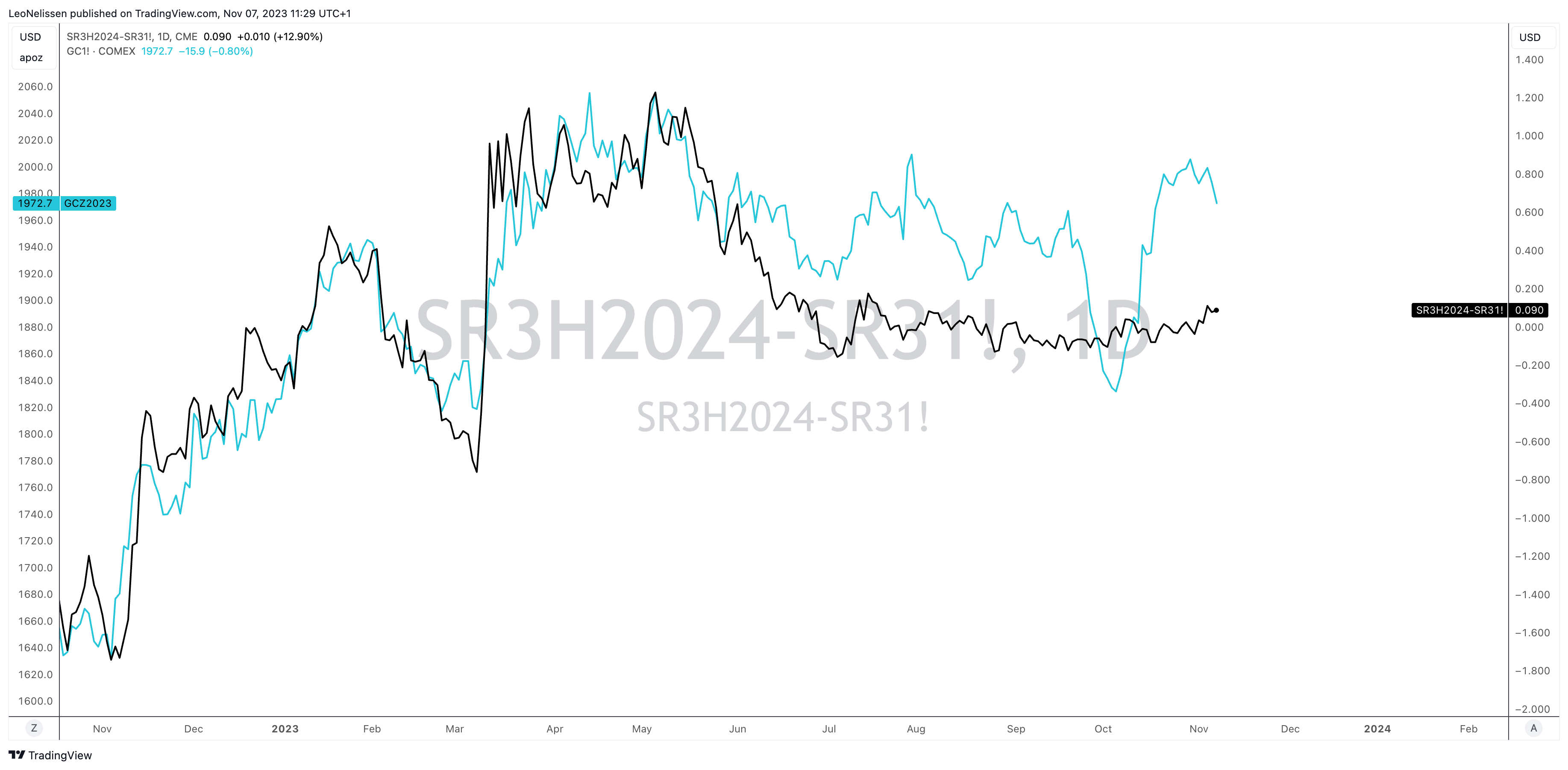

The chart below shows the difference between March 2024 SOFR futures and next month's SOFR futures. While the correlation with gold isn't perfect, we see that lower expected rates in the future tend to be very bullish for gold.

{kind=link}

TradingView (Gold, SOFT March 25 - SOFT Next Month)

This is what my gold thesis has been based on for a while.

Although I have been in the group that expects interest rates and inflation to remain higher for longer since 2020, I do believe that this creates a situation where the Fed may be forced to cut rates at some point - likely within the next four quarters.

So far, the economy is strong.

However, cracks are starting to appear.

- Unemployment is showing significant cracks (it's why gold did so well last week).

Bloomberg

- Commercial real estate deals have imploded, with a risk of accelerating defaults next year.

CBRE

- Manufacturing sentiment is falling again (already below the neutral 50 line).

Wells Fargo

- People are likely facing much higher borrowing costs on their mortgages.

Morgan Stanley

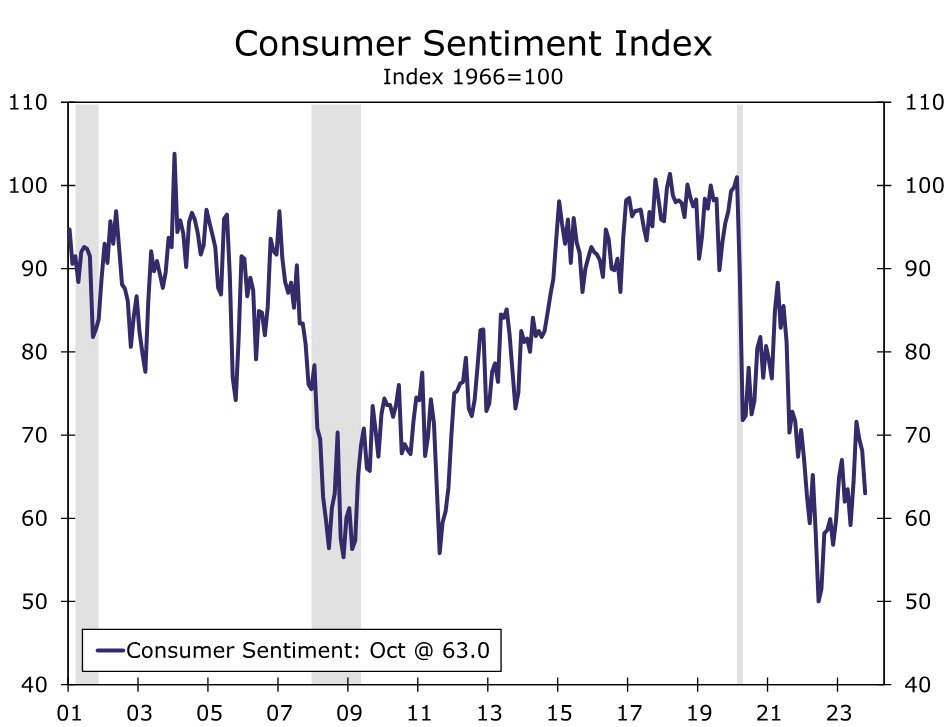

- Consumer sentiment is declining again.

{kind=link}

Wells Fargo

Don't get me wrong. I'm not making the case we're about to enter a Great Financial Crisis. I have been buying high-quality stocks on weakness, as I'm a long-term investor. I have no shorts.

However, if these developments continue, we could see a situation where the Fed may be forced to cut rates to protect financial stability. If that happens in an environment of elevated inflation, we could see a significant upswing in gold prices.

That's where Agnico Eagle Mines ( AEM ) comes in.

On August 30, I wrote an article titled Why I'm So Bullish On Agnico Eagle Mines . Now, I get to write an update based on the new macro developments (as seen above) and its recently released third-quarter earnings.

So, let's get to it!

Why I'm So Bullish On AEM

I like Agnico Eagles for at least three major reasons.

- I believe gold prices have a lot of room to run (I just discussed that)

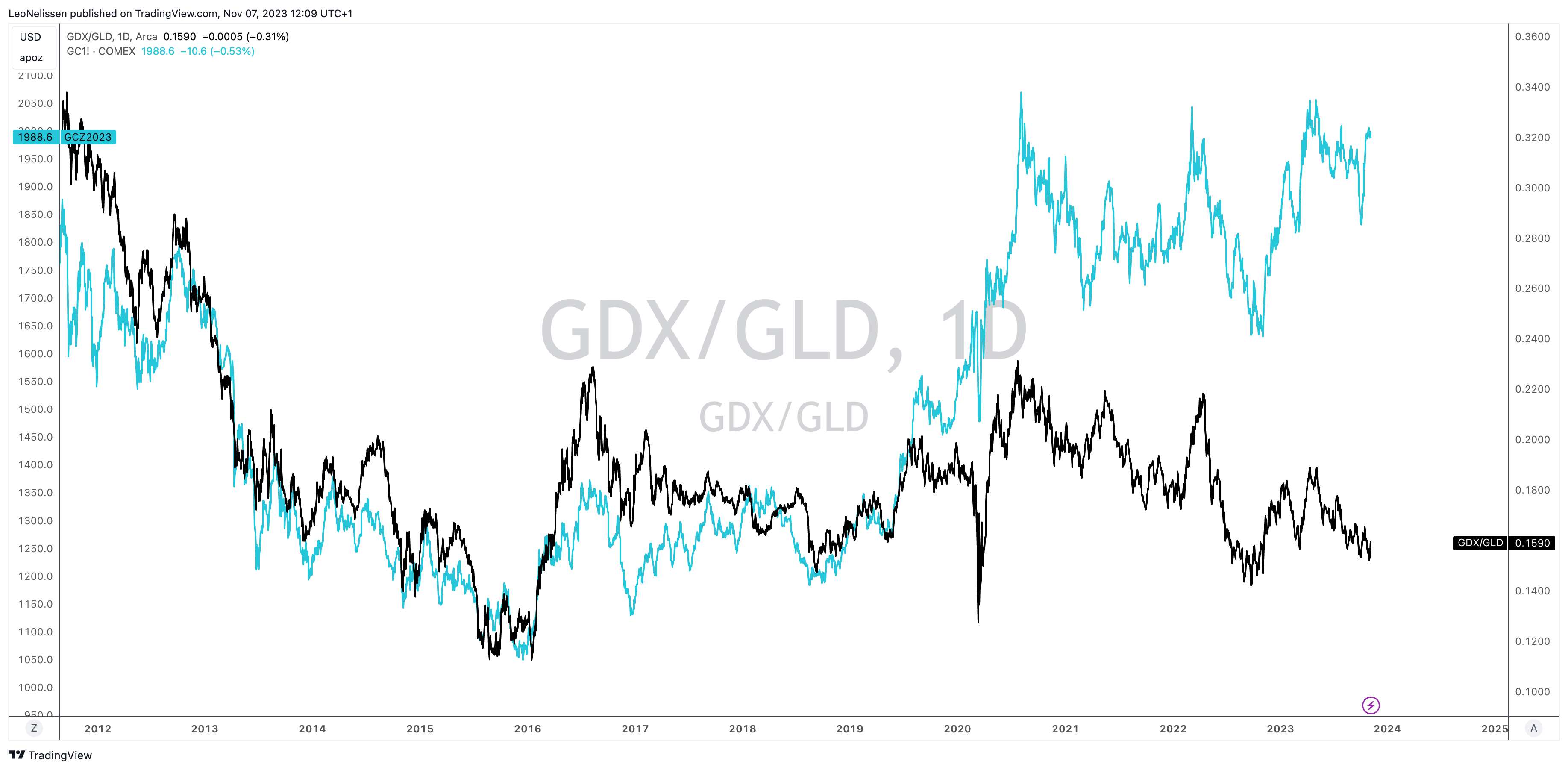

- Gold miners have significantly underperformed the price of gold. It's time to catch up. The chart below compares gold prices to the ratio between the gold miners ETF ( GDX ) and the gold ETF ( GLD ).

{kind=link}

TradingView (GDX/GLD, COMEX Gold)

- I consider AEM to be one of the best gold companies in the world. Since the inception of GDX, it has outperformed its peers. After a few years of failing to outperform, I believe AEM is poised for outperformance.

The recently released 3Q23 earnings told us a lot about AEM's potential to outperform.

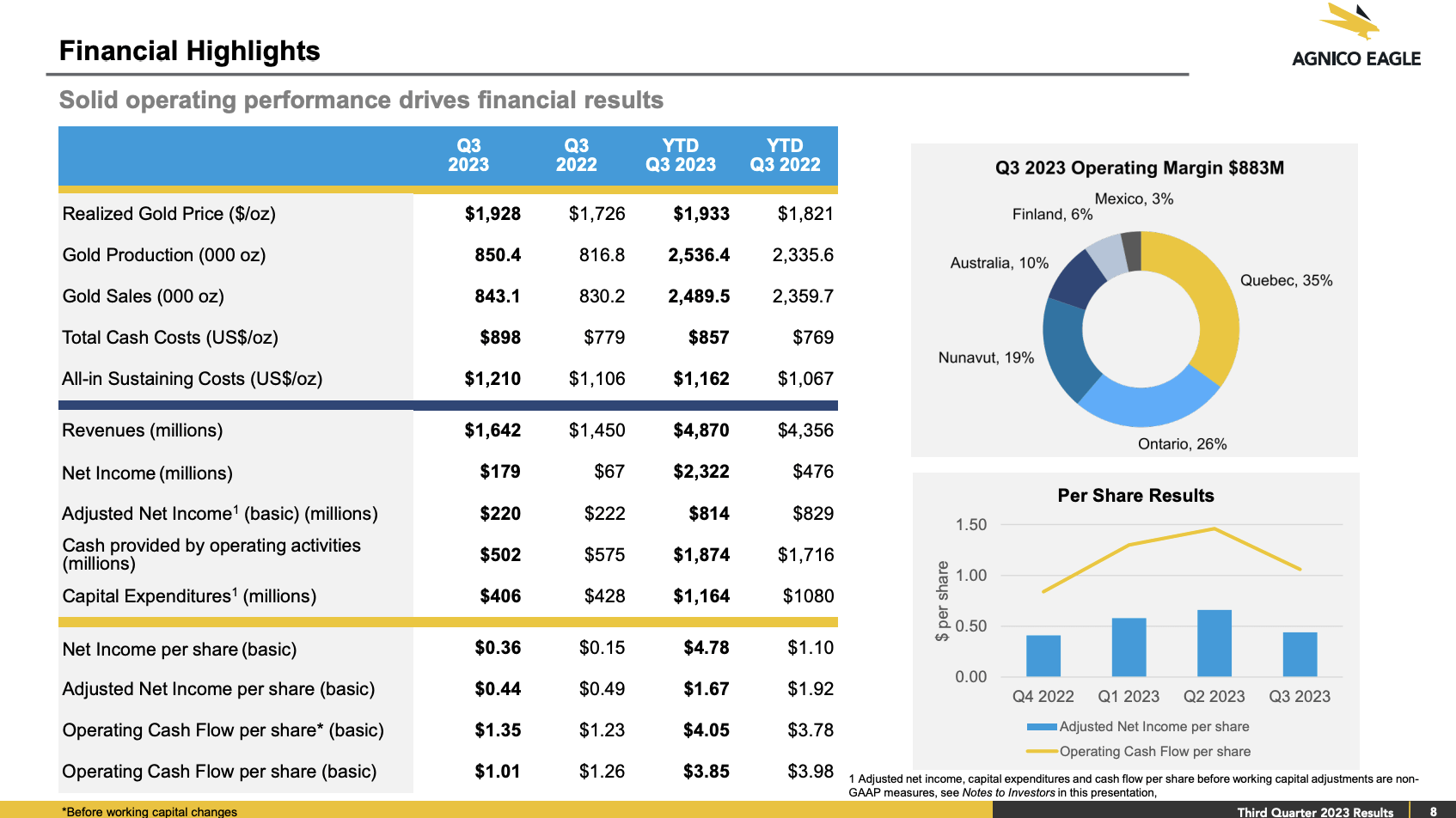

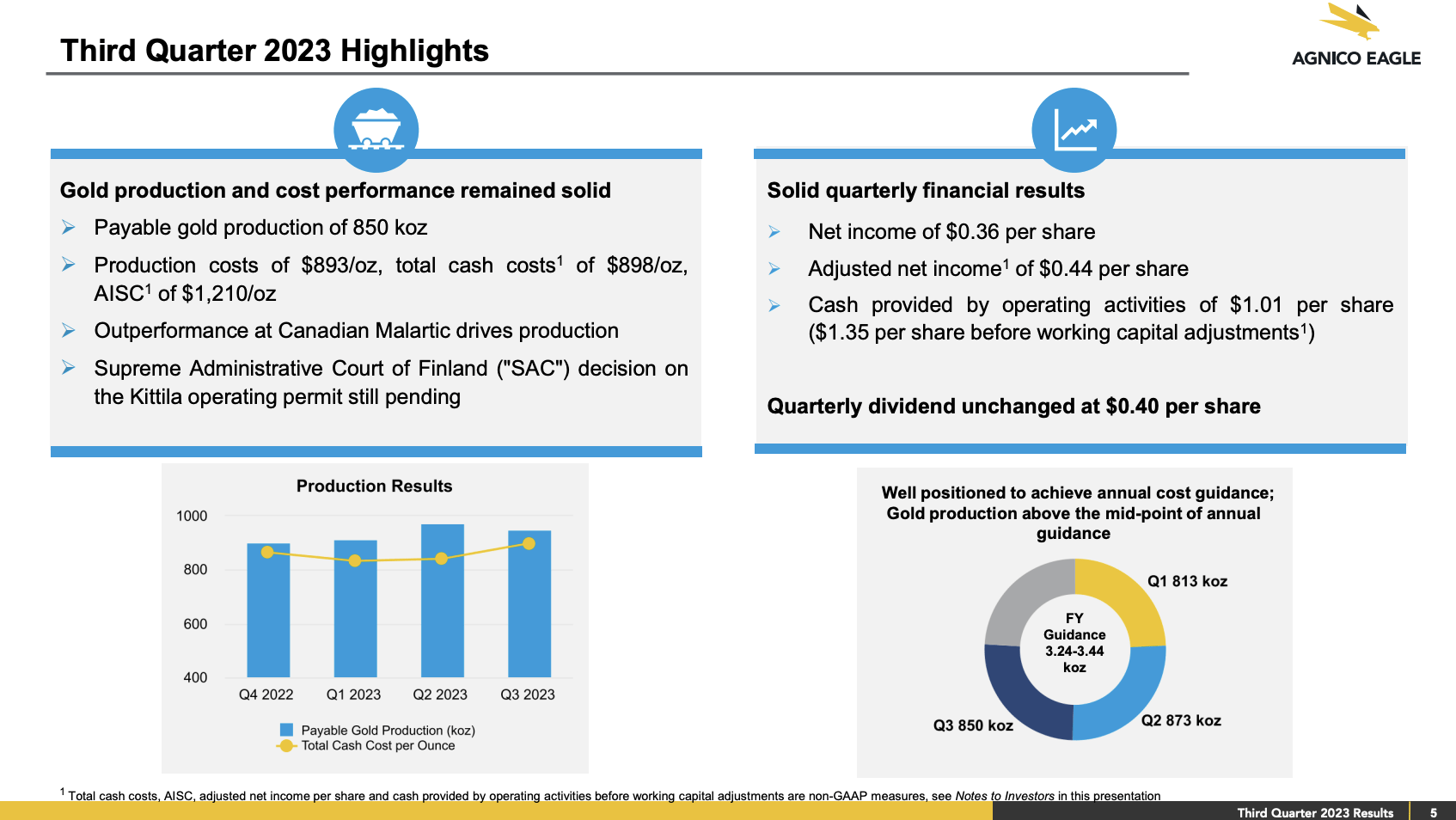

The company delivered strong financial results. The operating margin for the quarter reached $883 million, driven by outstanding performances from Canadian Malartic and Meadowbank.

Despite lower production at Detour and Fosterville, both operations maintained decent operating margins, approximately $180 million and $90 million, respectively.

The company produced 850,000 ounces of gold and sold 843,000 ounces. The average realized price was $1,928 per ounce, aligning with the fixed price.

{kind=link}

Agnico Eagle Mines

This resulted in total revenues of $1.6 billion for the quarter. For the first nine months of the year, the company produced over 2.5 million ounces of gold and is well-positioned to exceed its production guidance for 2023.

The third-quarter cash costs were $898 per ounce, slightly above the top end of the total cash cost guidance range for the year, which was set between $840 and $890 per ounce.

Year-to-date total cash costs were $857 per ounce, slightly below the midpoint of the cost guidance.

Furthermore, what matters the most is that the company remains on track to meet its cost guidance for the year.

{kind=link}

Agnico Eagle Mines

As a result, adjusted net income per share for the quarter was $0.44, a slight decline compared to the third quarter of the previous year.

This decline was attributed to higher costs due to inflation, increased amortization related to owning 100% of Canadian Malartic, and higher interest costs.

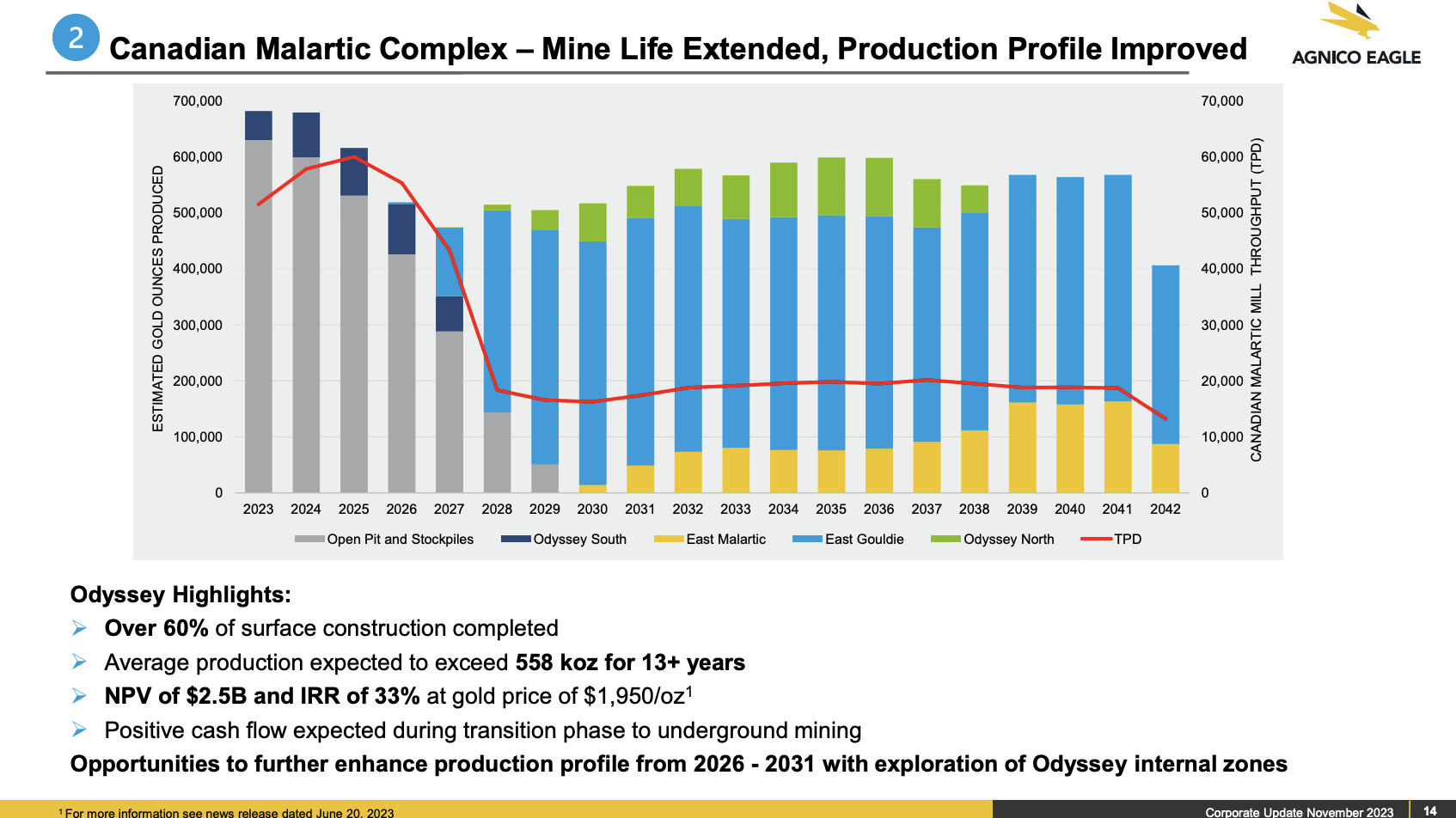

The Canadian Malartic mine is transitioning from Canada's largest open-pit mine to Canada's largest underground mine. The company has made significant progress and added 15 million ounces of resources in the last four years.

{kind=link}

Agnico Eagle Mines

This is one of the company's major projects to boost long-term output.

{kind=link}

Agnico Eagle Mines

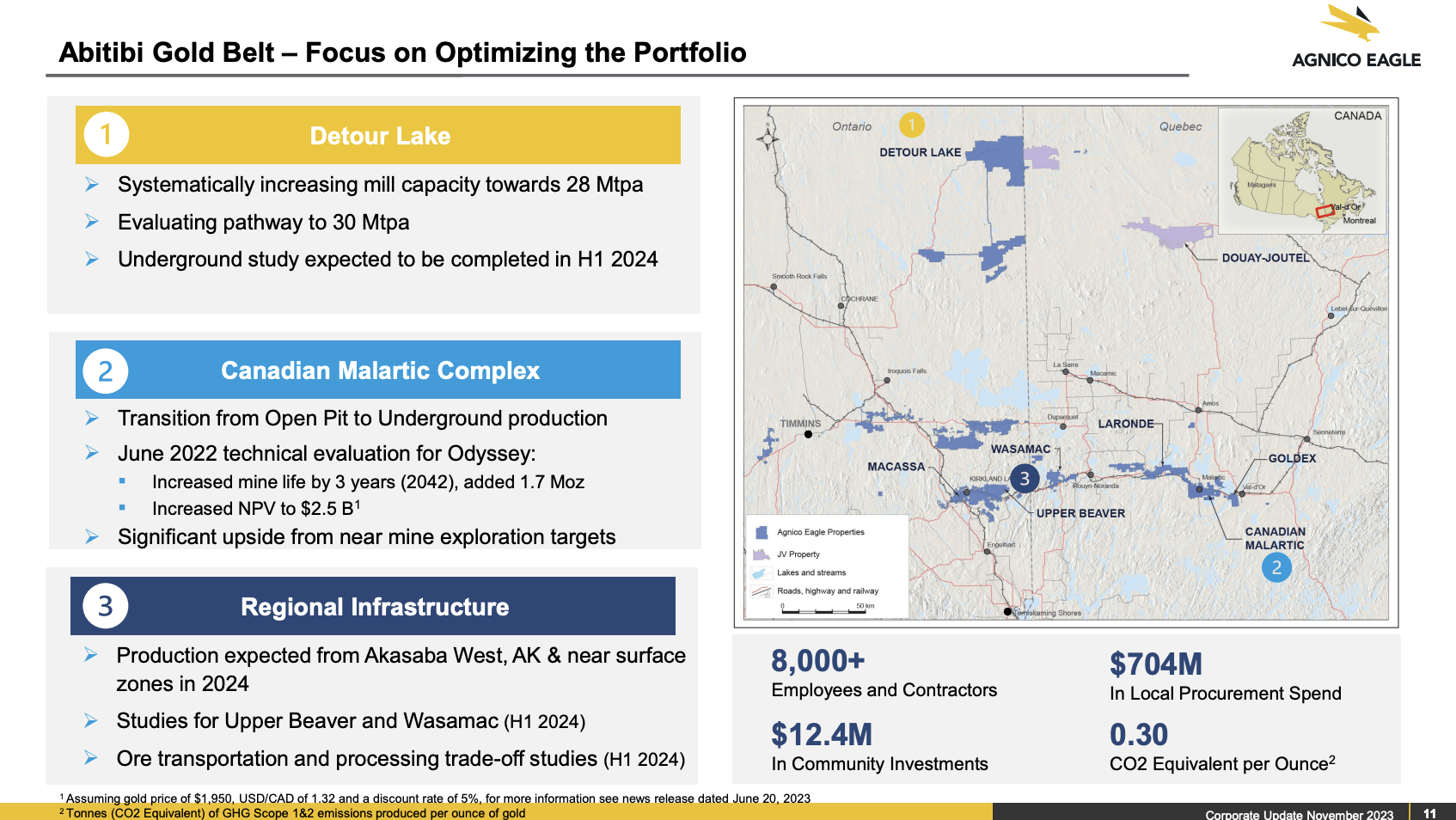

Regarding the Detour Lake expansion, Agnico Eagle is working toward its goal of reaching a million ounces a year at the Detour mine by increasing the mill capacity and raising the grade.

Despite a transformer incident impacting 3Q23 production, the focus is on achieving 28 million tonnes per year by 2025 and exploring opportunities to go beyond this target. Results from an underground study are expected in the first half of 2024.

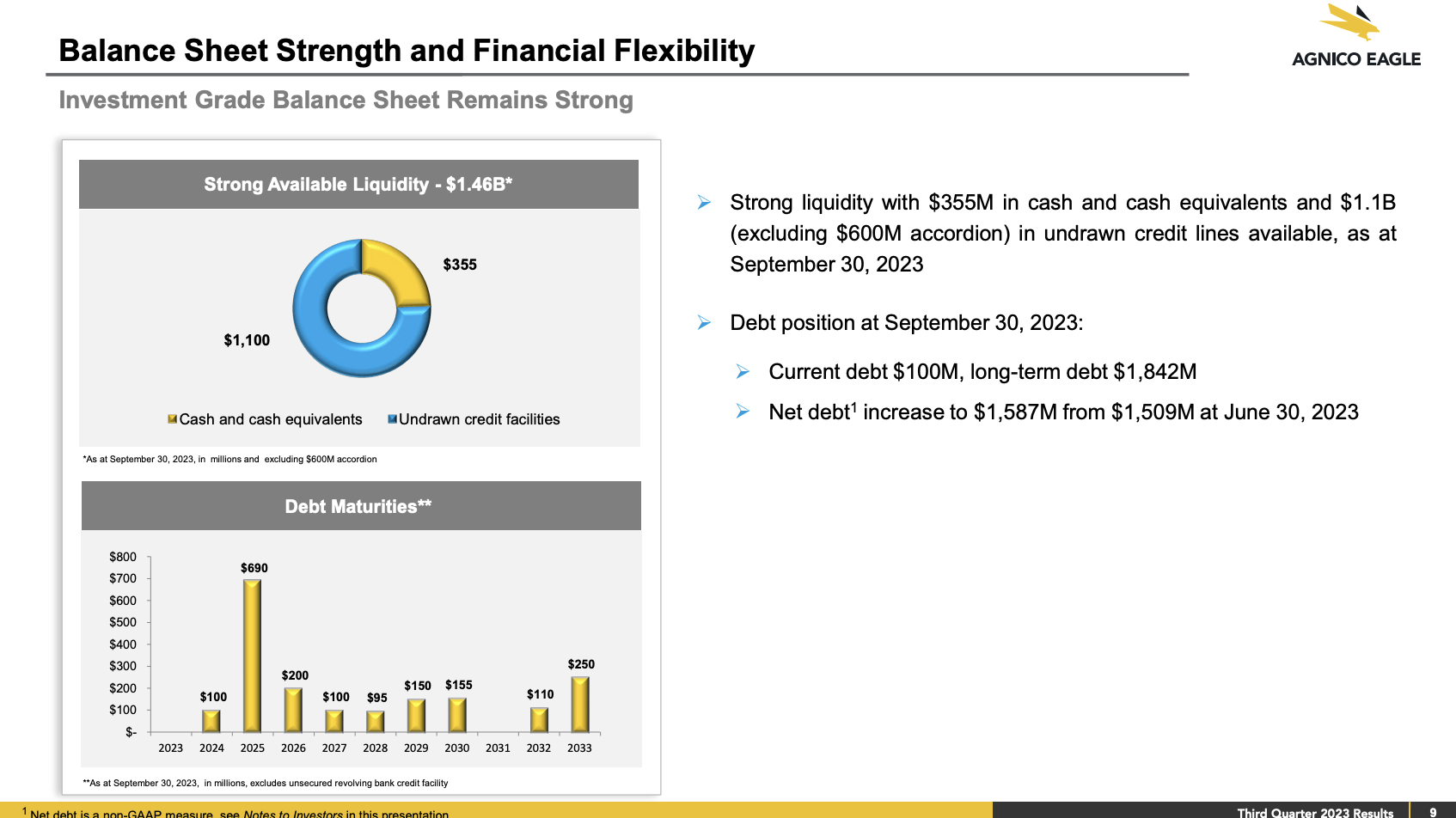

The company also maintains a very strong financial position.

AEM ended the third quarter with $355 million in cash and $1.1 billion in available liquidity under its revolving credit facility.

The net debt position increased to $1.6 billion, primarily due to increased working capital requirements associated with the seasonality of the Nunavut sealift. The net debt-to-EBITDA ratio remained low at around 0.5x, indicating a stable balance sheet position.

On top of that, AEM has no debt maturities in 2023 and just $100 million in maturing debt in 2024.

{kind=link}

Agnico Eagle Mines

It has an S&P credit rating of BBB+, which is one step below the A-range.

Going forward, the company anticipates a strong fourth quarter and expects to improve its cash and balance sheet with gold prices at current levels.

Overall, they are looking forward to a successful fourth quarter and a strong finish to the year from a financial perspective, which should be doable with gold trading close to $2,000 per troy ounce.

But wait! There's a fourth major reason why I like AEM: it has low geopolitical risks.

When it comes to mining, I am not a fan of the geopolitical risks that come with operations in nations with less stable governments and higher social risks. This includes South America, Africa, Asia, and other smaller regions.

Although most major miners have good relations with foreign governments, it needs to be seen how that changes once we enter an environment of elevated commodity prices.

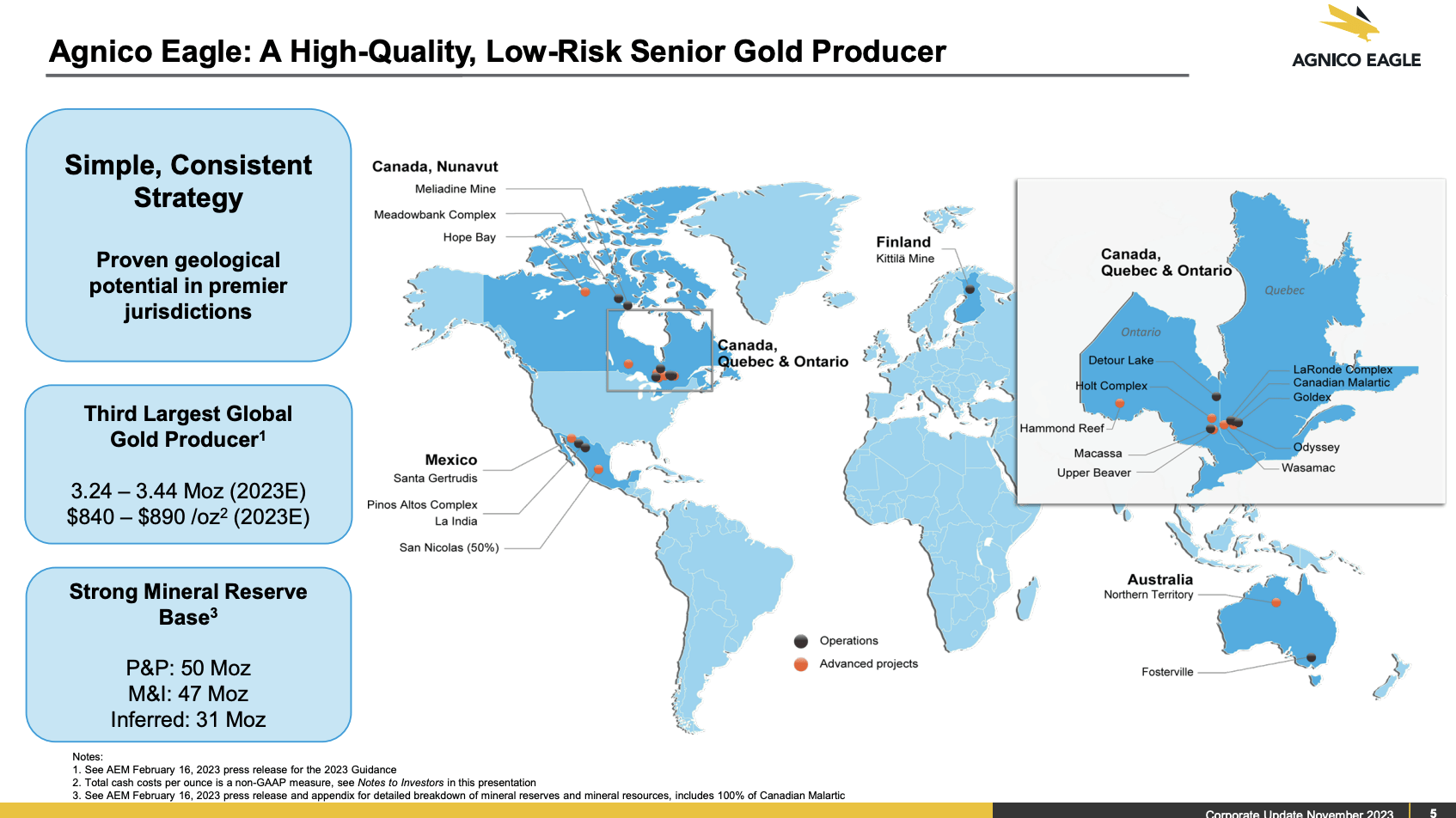

AEM mainly produces in Canada, Mexico, and Australia, which significantly lowers geopolitical risks.

{kind=link}

Agnico Eagle Mines

The company is also attractively valued.

Valuation

Putting a valuation on a company that is highly dependent on commodity prices is tough.

The company is currently trading at just 8x forward EBITDA.

This would be a fair valuation if the price of gold were to fall to $1,900 and stay at these levels.

As I'm bullish on gold, I'll stick to what I wrote in my prior article.

I believe once gold rises, AEM will have the benefit of a higher multiple and higher expected EBITDA, providing a lot of potential upside for its share price.

In my NEM article, I made the case that the stock could triple in the years ahead. I believe that this applies here as well.

I have a longer-term gold target of $3,000, which would boost EBITDA by high-double digits without incorporating higher output and production efficiencies.

However, I do not expect this to happen soon. This could take 2-3 years to unfold.

The current consensus price target of NY-listed shares is $65, which is 33% above the current price.

I think we could see $90 over the next two years, with significantly more upside on a longer-term basis.

However, please note that I see AEM as a hedge. It's not a core holding of my dividend growth portfolio. Gold miners have a very disappointing long-term performance and are volatile.

Although I will accumulate AEM shares on weakness and expect substantial long-term gains, be careful if you decide that gold miners are right for you.

For further details see:

Macro Developments Could Send Agnico Eagle Shares Flying