M - Macy's: Holding For Takeover Bid Expecting Decent Post-Holiday Sales Results

2024-01-16 01:51:38 ET

Summary

- Macy's rated Hold, agreeing with consensus from SA analysts and Wall Street.

- While Q3 revenue and earnings fell, I expect Q4 results to be in line with the usual post-holiday sales jump.

- A dividend yield of 3.5% is above the sector average, while dividend growth over 10 years has declined.

- The upside/downside risk of the recent takeover bid for M stock has been covered.

Stock & Industry Snapshot

Now that the peak holiday shopping season is behind us and a new year is well underway, we're taking a moment today to cover a major American retailer, Macy's ( M ).

Though this is my first time covering this stock, I am all too familiar with the Macy's brand as a customer, having shopped there for years, as some of my readers may have as well.

From its profile on Seeking Alpha, we can see it traces its roots back to 1830, trades on the NYSE, is known for selling apparel and accessories as well as various other consumer goods and is also the parent company behind Bloomingdale's brand.

I would call it mid-to-upper price range, with comparable peers being Nordstrom ( JWN ) and Dillard's ( DDS ), also common sights at large malls across America.

Those of us who have ever had seasonal jobs in malls know that there is seasonality in this segment, with the sales peak usually November to New Year's Day, with perhaps a smaller sales peak during the back-to-school period of late August / early September.

In a nutshell, this business model is such that it is capital intensive having to operate so many brick-and-mortar stores that sit on a lot of inventory and rely on a lot of store traffic to get the product out the door, despite also having an eCommerce presence as well. I would also say that in times of recession, consumers may be less likely to spend on non-essentials.

To gauge the sector's possible impact on this stock, from key market data , we see that the consumer discretionary sector has not done great in the last month or so far this year, however, on a 1-year basis it has climbed nearly 26%. On a 3-year basis, it barely grew 4%.

Macys - US equity sectors (Seeking Alpha)

Any earnings results for Macy's will refer to figures released on Nov. 16th, while the next results are not expected until Feb. 22nd.

Worth noting also is that several media outlets, including an article in Britain's Guardian in early December , reported an investor consortium attempting a $5.8B buyout of Macy's, however as of today I did not find any final decisions on this takeover bid.

Equities Analyzer

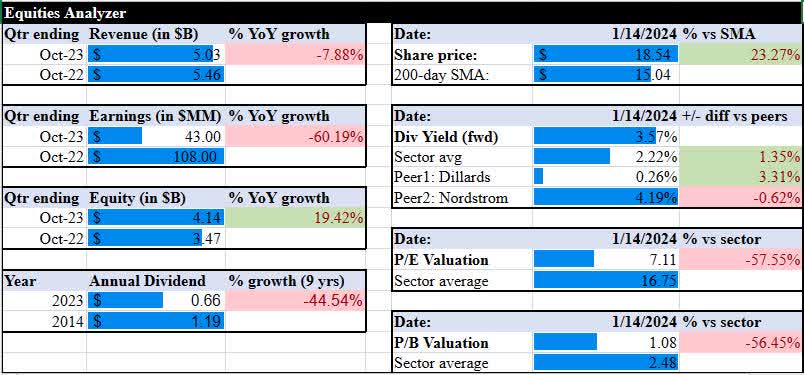

New for 2024, we introduced our Equities Analyzer , which looks at this stock across 8 metrics such as revenue and earnings growth, equity and dividend growth, dividend yield vs peers, and valuations (P/E and P/B ratios).

Here are our results for this stock:

{kind=link}

Revenue Growth

Let's start out with revenue growth. From the income statement , we know that in the quarter ending October, this stock saw a YoY revenue decline of 7.8%.

Macys - revenue growth (author analysis)

Although we will be looking back at Q3 results and comments, they could also give us some insight into forward-looking revenue sustainability.

It seems Q3 revenue took a hit both in the traditional and e-commerce channels, according to their press release : "brick-and-mortar sales decreased 7% versus the third quarter of 2022. Digital sales decreased 7% versus the third quarter of 2022."

Looking forward to the upcoming Q4 guidance, the company expects "$7.95B to $8.25B" in net sales, and a "220 basis point" YoY improvement in the gross margin rate.

We can see from the income statement that the quarter ending January usually has the highest revenue in the year, which ties back to what I said earlier about seasonal shopping peaks in retail. For instance, in both of the last January-ending quarters revenue topped +$8B, even though remaining quarters of the year could barely reach +$6B.

My sentiment for the upcoming quarter and year is that it will be a similar reflection of previous years and the seasonal cycle this company is subjected to.

One data point that supports a positive sentiment for retail would be credit card data, and just 6 days ago an article in Forbes highlighted that initial sales data point to an "OK" holiday season:

Mastercard released its initial holiday retail sales results, indicating a 3.1% increase in sales over the 2022 season.

So, my forward outlook is modestly positive about Q4 results, however, the remainder of the year I think will be similar to prior years. As I am not a huge fan of investing in a company that relies so heavily on one quarter for a large chunk of its sales, I think in this category I am more inclined to say hold rather than buy. I think the positive spending data from the holidays will be a nice tailwind, and that could help push the share price up which justifies a hold.

Earnings Growth

From the same income statement, we can see that earnings toppled by 60% on a YoY basis.

Macys - earnings growth (author)

In this case, when talking about the bottom line, I am looking also at growth trends in expenses. On a positive note, we can see that on a YoY basis, both the net interest expenses as well as total operating expenses declined, which is a good sign.

It appears to me that in this category the key impact was from declining revenue when comparing the quarter ending October with Oct. 2022.

Looking towards Q4, I expect a boost in earnings due to the expected revenue boost that happens in that quarter each year, which could send shares up temporarily at least, and this would justify a hold rather than a sell.

Equity Growth

Some positive news from the balance sheet tells us that positive equity has grown by +19.4% on a YoY basis.

Macys - equity growth (author)

Within the equity category, one item that could impact it is debt so a trend I look for is growing long-term debt. In this case, we see that debt of $2.99B was practically flat on a YoY basis, a good sign in my opinion, telling me it is not growing however I would like to see it decline.

As of Q3, according to the presentation , we also know the company had the capacity to return $135MM in dividend payments YTD as well as $25MM in share repurchases, showing a commitment to return capital to shareholders.

This equity situation presents a nice buy case, I think.

Dividend Growth

As a dividend-income investor building that type of portfolio, I care about what kind of dividend growth this stock has achieved up until now.

Macys - dividend growth (author)

From the data, this is one of few stocks I have covered lately that actually has had a decline in the dividend over the last 10 years.

As for dividend hikes in 2024, if the Q4 earnings indeed show a good result, it increases the chance of a dividend hike since the company might want to return some of that profit back to shareholders.

However, a quarterly dividend of just around 16 cents a share for a company that has been around this long and this well-established is pretty dismal, so I will pass and say the case is for a sell.

Share Price vs. Moving Average

Next, let's look at the most recent share price in relation to its 200-day simple moving average:

The data shows us that the share price has risen +23% above its 200-day moving average.

Macys - share price vs moving avg (author)

It has also gone up about +63% from its autumn lows around $11, and now hovering just above $18.

Does it make the case for a sell then?

Although there could be a revenue and earnings jump coming soon after Q4 results, and may push the stock further up, it does not seem like it would be sustainable bullishness since the seasonal effects will wear off pretty fast.

The fact that it is trading double-digit percentages to its moving average and also double-digits vs its autumn lows, yet earnings and revenue have seen YoY declines, and they have a below-4% dividend yield, does not present a strong buy case.

As for a hold, like I mentioned the share price may get a quick jump after Q4 results but then pull back since that seasonal effect will wear off. I say sell.

Dividend Yield vs. Peers

Using dividend yield data , here we are comparing Macy's forward dividend yield to that of two key peers we mentioned earlier, Dillard's and Nordstrom:

Macys - dividend yield vs peers (author)

The point of this section is to pick a stock among peers that has the best dividend return on capital invested. In this case, it would be Nordstrom at 4.19% yield, although Macy's is not too far behind at 3.57%.

In this case, it is not the best yield in this peer group but also is above the sector average, so I would say it is a hold case rather than a buy.

Now, if after the Q4 bullishness wears off and the stock price sees another dip as investors lose interest, that could present an opportunity for a spike in dividend yield, as shares will be cheaper (and assuming the company does not reduce the dividend but keeps same or increases it). So, that scenario could be better as a buy.

Valuation: P/E Ratio

Using valuation data we know the forward P/E ratio is 7.11, while the sector average is much higher at 16.75.

Macys - P/E ratio (author)

Is this valuation justified?

I say only somewhat, which makes it a hold.

On the one hand, there is a wide gap between share price growth (+23% vs its 200-day SMA) and earnings growth (-60% YoY decline). However, the P/E is far below its sector average.

Also, peers like Dillard's have a forward P/E that is higher yet also saw YoY earnings declines. Nordstrom, although seeing earnings YoY growth, has an exorbitantly high valuation of over 19x earnings.

Keep in mind that all three of them are affected by the seasonality of retail shopping trends.

So, among this peer group, Macy's has the best valuation although not a great one. I say hold on for now rather than buy.

Valuation: P/B Ratio

Also from valuation data, we can see that the forward P/B ratio is at 1.08, quite a bit lower than the sector average which is 2.48.

Macys - PB ratio (author)

Here, we can see a justified valuation because the gap between share price growth and equity growth is tight. While share price growth has happened, we know that equity (book value) has also grown +19%.

So, it is a buy because of the 1.08x forward price to book ratio, as the gap between equity growth and price growth is narrow.

Key Risks

The key risk right now to mention is the risk that the takeover bid is withdrawn. According to CNBC , the investor consortium was willing to pay $21 per share for Macy's, while as of today it is trading around $18.50, so if I have not already got in at a lower price it seems logical to buy and make a few bucks per share if the consortium buys them out.

That $21/share, however, could go higher. According to the article, the consortium:

would be willing to offer a higher bid based on due diligence, the sources said. The group would already be paying a premium for the department store, which has struggled to keep up with online competitors.

That could present an upside risk if I were overly cautious about this company right now, and potentially missing out on the share profit from a takeover.

However, there is the downside risk that the deal does not go through after all, which could also have an added effect of sending the share price down further as other investors pull out, losing interest in this stock.

Since both scenarios have a moderate probability but could have a high risk impact, I am inclined to say hold on in this case rather than buy or sell.

Summary and Rating

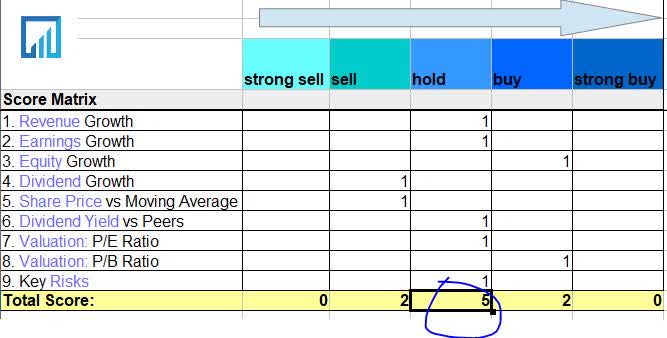

Here is a breakdown of my rating using the score matrix:

{kind=link}

The case here is for a hold.

This also agrees with today's consensus shown on Seeking Alpha from analysts and Wall Street covering this stock.

Though revenue and earnings saw declines in Q3, I expect the holiday season results to give it a boost in Q4 results coming out in February. Equity grew nicely and debt remained mostly flat. Dividend growth was dismal, although the dividend yield at +3.5% was modestly attractive.

All eyes are on the takeover bid as it could be both an upside and downside risk in 2024.

My portfolio strategy would be to hold on to this stock, and if the takeover happens I would profit from the share price premium, but if the takeover does not happen it could be a drop in share price and having to hold it longer, perhaps until next holiday season or until an even better takeover bid appears.

For further details see:

Macy's: Holding For Takeover Bid, Expecting Decent Post-Holiday Sales Results