M - Macy's: Navigating Modern Retail Challenges With Legacy Strengths

2023-10-13 09:55:41 ET

Summary

- Department stores like Macy's once symbolized shopping luxury. However, the rise of online shopping and DTC models has challenged their dominance, prompting strategic shifts.

- Macy's "On 34th" initiative counters the DTC trend but faces challenges from established brands.

- Macy's valuable real estate assets offer potential shareholder returns, contrasting with Sears' liquidation strategy.

- Macy's faces competition but real estate value and stable FCF suggests potential for a decent return.

Investment Thesis

Historically, department stores, such as Macy’s Inc. ( M ), represented the pinnacle of retail luxury and convenience. Yet, the evolving retail dynamics, driven by the proliferation of online shopping and the emergence of direct-to-consumer ((DTC)) strategies, have posed significant challenges to their dominance. To navigate this shift, Macy's launched its "On 34th" initiative, seeking to carve a distinct niche amidst the DTC trend. However, this endeavor faces hurdles, particularly when compared against legacy brands. One of Macy's notable strengths, and a potential value proposition for its investors, lies in its expansive real estate holdings. Given its prized properties and consistent free cash flow, Macy's appears poised to offer potential upside, even as it grapples with the intense competition of the contemporary retail scene.

Company Overview

Macy's Inc. is a renowned omnichannel retail organization that operates under three primary brands: Macy's, Bloomingdale's, and Bluemercury. These brands offer a diverse range of merchandise, including apparel for men, women, and children, cosmetics, home furnishings, and other consumer goods. Macy's has a strong presence with stores in 43 states, the District of Columbia, Puerto Rico, and Guam. The company has been focusing on expanding its digital footprint, launching Macy's digital Marketplace in 2022, which features a collection of new brands and products from third-party sellers. This move aims to introduce customers to new merchandise options in the ever-evolving retail landscape and gain an edge over their numerous competitors, ranging from traditional department stores such as Kohl's Corporation ( KSS ) to global e-commerce giants such as Amazon ( AMZN ) and eBay ( EBAY ).

Challenges in Adjusting to the Changing Consumer

In my opinion, department stores like Macy's were once the epitome of shopping convenience and variety. Their vast product range, combined with in-store events, and personalized customer service, made them more than just shopping hubs; they were entertainment centers.

In recent years, however, we've observed a pronounced shift in consumer behavior, further accelerated by the COVID-19 pandemic. This shift has been driven by the significant shifts towards online shopping and DTC models which have threatened and seemingly ended the dominance of the department stores.

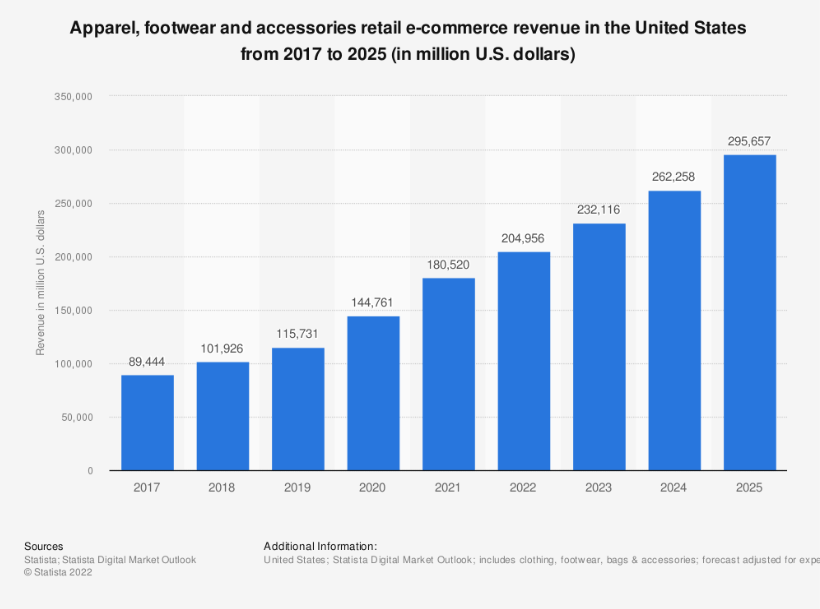

Firstly, the shift towards online shopping has been profound and has seen a consistent rise in recent times. The e-commerce fashion sector in the U.S. is projected to grow at a compound annual growth rate ((CAGR)) of 14.2% from 2017 to 2025 , achieving a market value of $1 trillion by 2024 and far outpacing the much slower growth rate of the overall U.S. fashion sector.

Retail E-commerce Growth from 2017 to 2025 (Statista)

{kind=link}

This has resulted in online sales now making up 20.8% of total retail sales, which is also expected to continue to rise and tipped to total 24% of the fashion retail market by 2026. Department stores, such as Macy’s and Kohl’s have recognized this and have shifted their business models to better address the changing market and meet consumer demands. For Macy’s this meant they have had to massively expand their online presence to the point it now accounts for approximately 30% of total sales, a number which is down from the COVID peak of 44% but still higher than the pre-COVID share of 25%. Additionally, the company acquired brands such as Bluemercury, a specialty beauty retailer, which operates in an industry segment which is dominated by offline sales. While these initiatives have been important and diversify the company’s offerings, they have ultimately failed to stop the slow decline in recent years, as the core businesses have continued to contract.

Partner Brands Continue to Switch to DTC Approach

While I do not believe that online shopping will completely shift consumers away from traditional brick-and-mortar stores, I believe it will continue to consume a larger share of the retail market, ultimately requiring further digitalization of Macy’s. This results in the company operating in an space where they do not have a strong competitive advantage and will be competing with other businesses including the brands the Macy’s stocks within its stores, most of which have been trending towards more DTC models. Some of the biggest brands sold by Macy’s such as Ralph Lauren, Calvin Klein and Levi Strauss have all seen the share of their of revenue from DTC sales increase over recent years with plans to continue to expand their DTC network. For example, over the next three years, Ralph Lauren plans to launch 250 new stores , emphasizing its DTC approach. This move indicates the brand's strategic pivot from department stores and wholesale channels, with most companies citing improved control and cost reductions as reasons for the switch.

In my view, new initiatives by Macy's such as "On 34th” clothing appear to be calculated moves in response to the shifting dynamics of the retail industry. As numerous major partner brands pivot to DTC models, traditional retailers, including Macy's, are undoubtedly under pressure. The appeal of DTC for brands is clear: direct engagement with customers, potentially higher profit margins, and greater control over their brand narrative. In this context, Macy's decision to roll out "On 34th" private label seems like an attempt to counteract the DTC trend by offering something proprietary and distinct.

Introducing "On 34th" is more than just adding another product line to their portfolio; it's Macy's way of signaling their adaptability in a rapidly changing market. However, the success of this initiative is far from guaranteed. While the intent behind "On 34th" is commendable, its actual impact will depend on execution, market reception, and how it differentiates itself in a saturated market. The initiative underscores Macy's recognition of industry challenges, but whether it will be the solution they need in the face of the DTC wave remains to be seen.

In my opinion, Macy's "On 34th" faces an uphill battle in matching the stature of established brands they've traditionally stocked. These legacy brands come with decades of consumer trust, recognition, and a loyal customer base. They've carved out distinct niches, backed by extensive marketing campaigns and global reach. For "On 34th" to gain similar traction, it must not only offer exceptional quality and value but also differentiate itself in a crowded market. While Macy's has retail expertise, building a brand's reputation and loyalty takes time and consistent effort, and I believe that stocking their lesser-known brands as opposed to more established partner brands may reduce the attraction of shopping at Macy’s for many consumers.

Impressive Portfolio of Valuable Real Estate

While I do believe that all department stores will continue to face headwinds thanks to shifting consumer behavior and a change in strategy for many apparel companies, Macy’s still holds an impressive portfolio of valuable real estate in some of the most desirable locations on the planet and I believe this is one of the most valuable aspects of the business that would have the potential to return significant value to shareholders. Over the past few years, several department stores and retail chains have opted to liquidate or monetize their real estate assets, either as a strategy to raise capital or as a response to declining sales and the challenges posed by the rise of e-commerce. Perhaps the most prominent example is Sears which has been selling off its real estate assets for years. In 2015, the company formed Seritage Growth Properties, a real estate investment trust, which has been liquidating many former Sears properties since Sears filed for bankruptcy. While I recognize that Sears shareholders ultimately received none of the returns resulting from the sale of the properties, it is worth noting that the company was burning substantial cash during the last years of operation which is notably different to current situation of Macy’s, which is currently generating solid free cash flow ((FCF)).

Macy's boasts more than 700 locations, and for value-focused investors, the real estate alone is estimated to be worth between $6 billion and $8 billion , with some estimates suggesting value is closer to $10 billion. With a market capitalization of $3.03 billion and an enterprise value of $8.56 billion, the company appears undervalued relative to the value of its real estate. Macy's has the flexibility to leverage or divest parts of its real estate assets to generate funds, reduce its $5.97 billion in total debt, buy back shares or pay back shareholders in the form of a dividend, all of which would be of benefit to the shareholders.

Financial Analysis

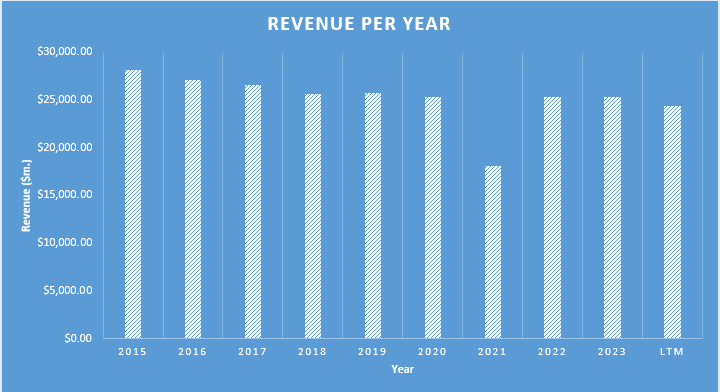

In the last five years, Macy's revenue has seen little growth, and is down from $25.7 billion in 2019 to $24.36 billion in the last 12 months ((LTM)). Macy’s Inc. experienced a decline in its earnings per share ((EPS)) from a record $4.55 in 2022 to $2.70 In the last 12 months.

M's Revenue per Year (DJTF Investments)

{kind=link}

In terms of cash flow, Macy's generated an LTM FCF of $683 million, a number that is down considerably from $2.36 billion a little over a year ago, although this was an exceptional year for the company.

The intrinsic value of the company, as reflected by its book value per share ((BVPS)), is down since 2019. It went from $20.91 in 2019 to $15.39. This indicates that the company has had its core value reduce over this timeframe although much of this decline came during the COVID pandemic where foot-traffic numbers were down considerably. Since then, the company has been slowly building up its intrinsic value from the low of $8.22.

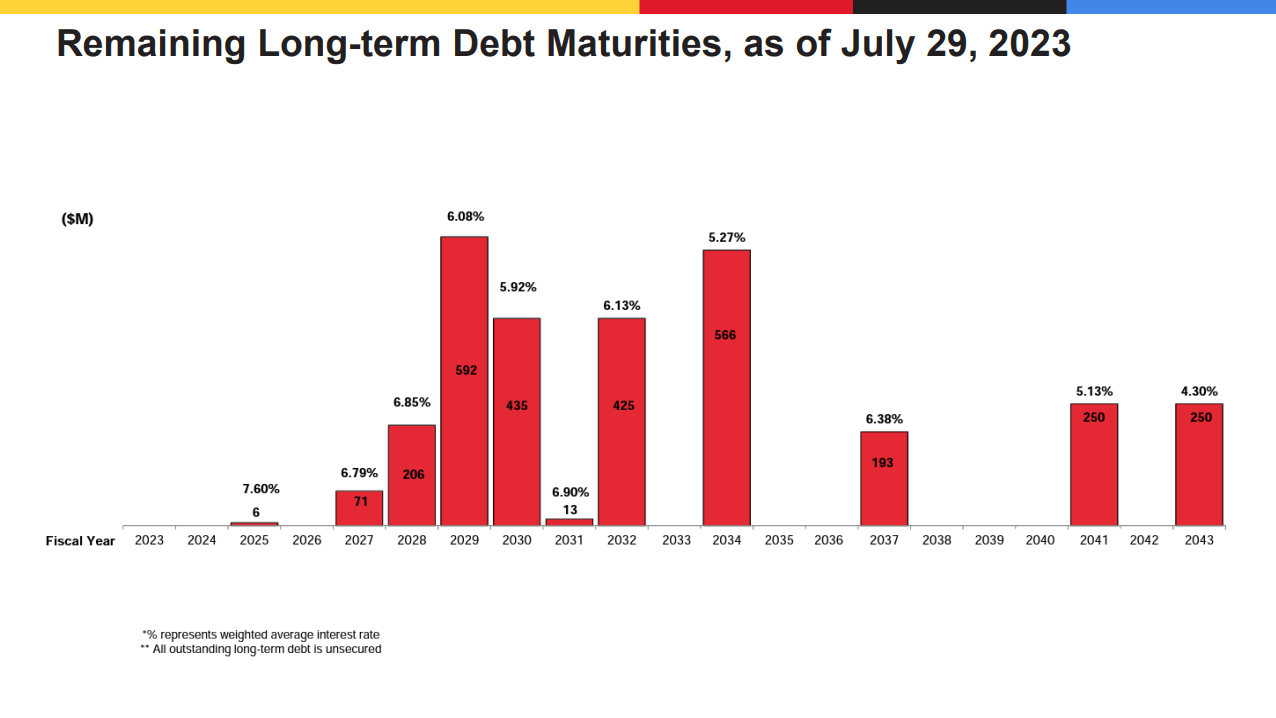

As of the most recent quarter, the company reported having cash and cash equivalents of $438 million with the company’s total debt standing at $5.97 billion. While the company does have a significant amount of debt, it's important to consider that the management team in the past few years have been prudent in actively repaying debt, with the total debt down considerably from the 2021 level of $8.24 billion. Additionally, much of this debt does not mature until the late 2020s, so as long as the company can continue to generate FCF, I am not too concerned about the debt levels.

Remaining Long-term Debt Maturities (Macy's Inc.)

{kind=link}

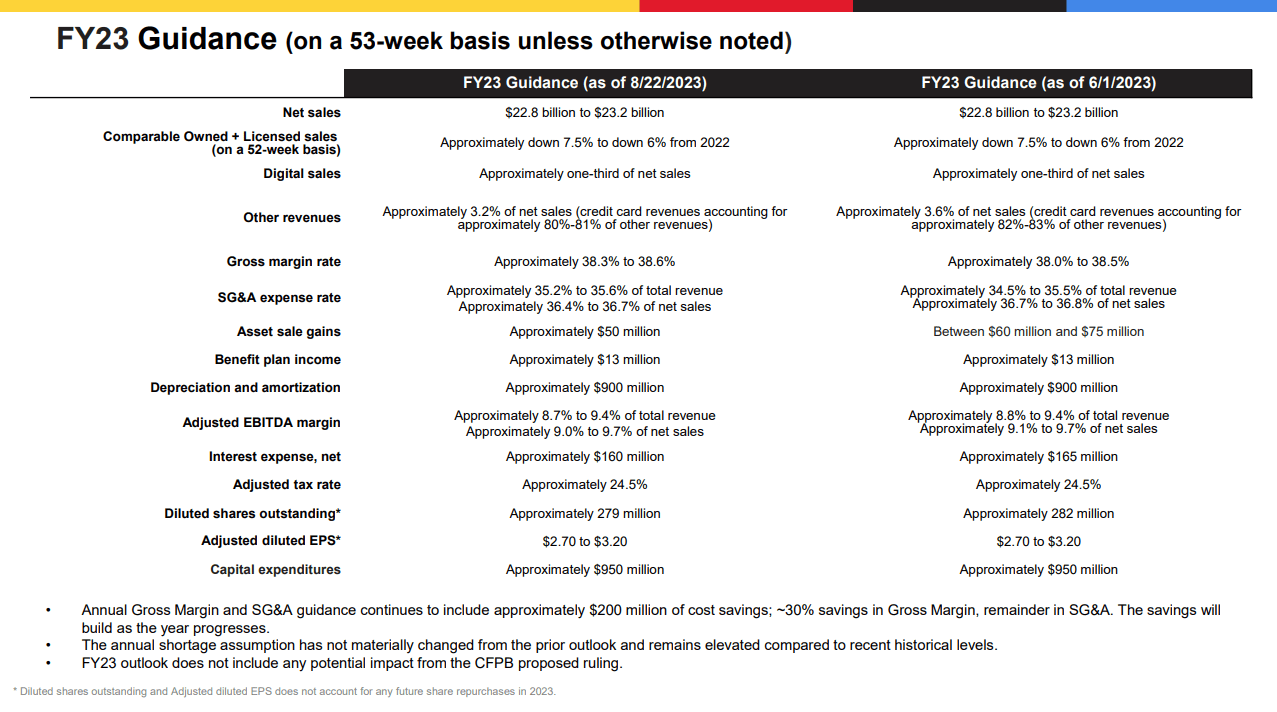

For fiscal year 2023, Macy’s has provided detailed guidance in which they anticipate revenue to fall to between $22.8 and $23.2 billion while EPS is expected to remain flat at $2.70 up to an increase of 18% to $3.2. Additionally, the company expects to gain from the sale of assets and expects Earnings Before Interest, Taxes, Depreciation, and Amortization ((EBITDA)) margins of 8.7% to 9.4% of total sales. I don’t anticipate this slow decline changing in the short term as I do not foresee the macroeconomic situation improving much in the coming months. In the longer term I could see the company return to slow, low single digit growth, however, I anticipate the company will still be subject to the same consumer headwinds.

{kind=link}

Valuation

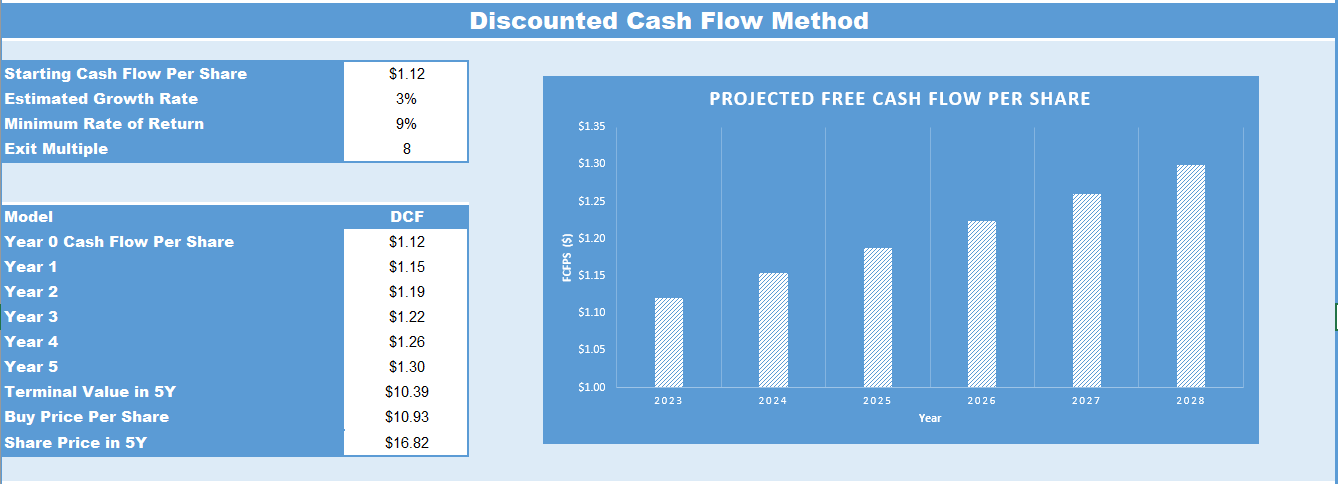

In my assessment of Macy’s, I see the company’s core business continuing to struggle as it must compete with online and DTC brands. I do, however, believe the company will continue to streamline operations, reducing their overall store count and keeping the stores which have high foot traffic and robust consumption. Because I do not foresee Macy’s ceasing operations or selling some of their most valuable real estate, I have opted to utilize a discounted cash flow ((DCF)) method for the valuation. For my valuation I have assumed that FCF generated from Macy’s overall in-store and online sales remain flat as the company slowly sells off its underperforming stores, offset by the slow growth of their remaining stores. FCF generated from the incremental sale of real estate is why I have assigned a 5-year growth rate for the company of 3%. Projecting the LTM FCF per share of $1.12 at 3% CAGR results in a 2028 FCF per share of $1.30.

Using an exit multiple of 8, derived from Macy's average price to FCF ratio over the past decade, I project a five-year price target of $16.82. Hence, if one were to invest in Macy’s at its current share price of $10.93, it could potentially yield a CAGR of 9% for the upcoming five years. Despite this seemingly positive upside, I have designated Macy’s as a 'hold' rather than a 'buy'. This stance primarily stems from my skepticism towards any significant augmentation in the company's Free Cash Flow over the next 5 years, as I do not anticipate the sale of its most prized real estate assets which would ultimately result in improved returns for shareholders. Additionally, in adherence to my personal investment philosophy, I target a minimum expected rate of return of 15%. This benchmark is significant as it renders the inherent risks associated with investing in individual stocks more palatable when compared with the broader market exposure afforded by index investments.

DCF Valuation for M (DJTF Investments)

{kind=link}

Conclusion

Department stores, epitomized by giants like Macy's, were once the pinnacle of shopping luxury and convenience. However, the modern retail landscape, shaped by the surge in online shopping and the rise of DTC models, has significantly challenged their traditional dominance. In response, Macy's introduced the "On 34th" initiative, aiming to offer a unique proposition in the face of the DTC wave. Yet, this move is not without its challenges, especially when competing against well-established brands. A silver lining for Macy's, and a potential boon for its shareholders, is its substantial real estate portfolio. With valuable properties and a stable free cash flow, Macy's could hold promise for potential returns, even amidst the competitive pressures of today's retail environment.

For further details see:

Macy's: Navigating Modern Retail Challenges With Legacy Strengths