M - Macy's: Now Fairly Valued

2023-06-20 11:27:36 ET

Summary

- Macy's stock has been upgraded to "Hold" as it is now fairly valued after its price fell below $16 per share.

- The company's stock price has declined more than 20% year-to-date, significantly underperforming the market.

- The stock is vulnerable to broader economic weakness and a potential recession, which could lead to decreased consumer spending on discretionary items.

Investment thesis

My two previous bearish articles about Macy's (M) stock faced much criticism from the bulls. But, both calls aged well, since the stock substantially declined in its price. The company still faces severe headwinds and its quarterly sales have been declining for multiple quarters in a row. However, as the stock price went below $16 per share, now I believe it is very close to its fair value. Therefore, I upgrade my rating for Macy's stock to "Hold".

Financials update

The company announced its latest quarterly earnings on June 1, missing again on revenue. It was the third quarter in a row when Macy's missed revenue consensus estimates. On the other hand, the bottom line was better than expected by analysts. On a YoY basis, the top line declined about 6.8%, and the revenue decline is accelerating.

{kind=link}

The gross margin improved sequentially and YoY, which is a good sign. The slight improvement in the gross margin was thanks to controlling inventories and costs, which is crucial in the current harsh environment. At the same time, I still have plenty of room for improvement in terms of cost of revenue. On the other hand, the operating margin almost halved because of increasing SG&A expenses. As a result, quarterly levered free cash flow [FCF] decreased more than two times YoY. The company's SG&A to revenue ratio has been consistently above 30% for several periods and I think there is not much room for improvement here. Macy's needs to spend heavily on marketing to sustain its sales. The company's comparable sales dropped 8% in the first quarter, which reflects both temporary and secular headwinds for the company.

The upcoming quarterly earnings are scheduled on August 18 and revenue is expected to demonstrate a YoY decline again. Quarterly sales are expected at $5.1 billion, about 9% lower than a year ago. The bottom line is also expected to suffer with adjusted EPS expected to decline from $1 to $0.14. The company is in a substantial net debt position meaning that a couple of quarters of negative FCF might become a big problem. Moreover, I also want to underline that the quick ratio is very low, meaning elevated inventory levels.

From a consumer spending perspective, U.S. retail sales improved in May. But, clothing sales dynamics were almost flat , meaning there are few near term drivers to fuel Macy's revenue growth.

Valuation update

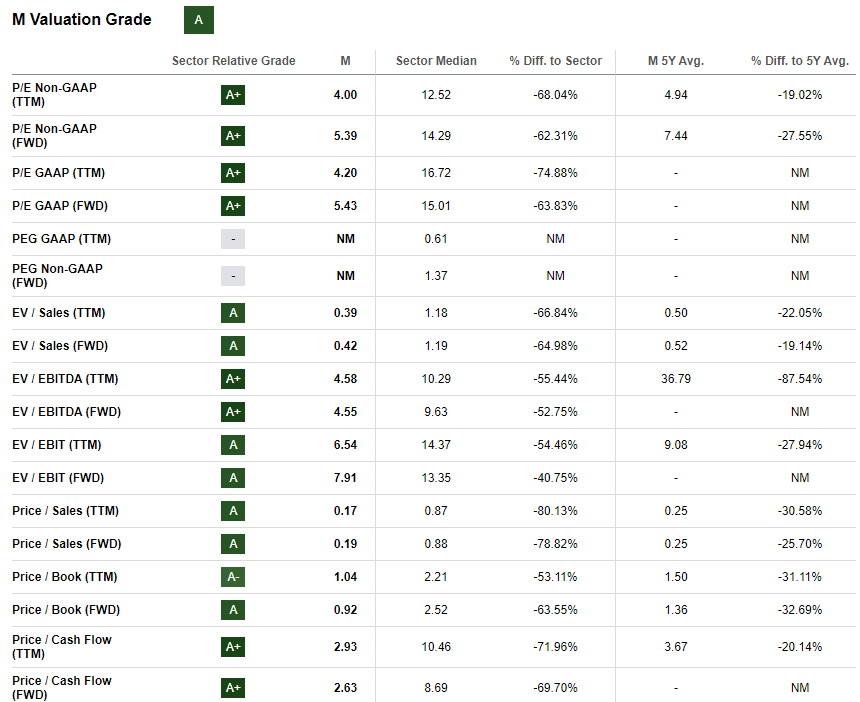

Macy's stock price declined over twenty percent year-to-date, while the broad market demonstrated double-digit growth. The stock significantly underperformed the market. Valuation multiples of Macy's are very low, and it is most likely the reason why the Seeking Alpha Quant assigned the stock an "A" grade. I'm afraid I have to disagree here, because as discussed in my first article about M, the company's financials are in a secular decline and margins are deteriorating.

{kind=link}

Yes, multiples look attractive. But I think that the discount is fair due to the secular headwinds the company is facing. Moreover, the management's initiatives do not seem to work, based on the recent financial performance dynamic.

Let me update my discount dividend model [DDM] valuation analysis. I use the same 8% discount rate as I did before. Consensus estimates forecast FY 2024 dividend at $0.68. The company has a shallow dividend growth rate grade from Seeking Alpha Quant because recent years' dividend dynamics were poor. To be conservative, I divide a 10-year dividend growth CAGR by two, which would be about 3.7%.

Author's calculations

Based on these assumptions, we can see that the stock's fair value is very close to the current share price level. It means the stock is currently fairly valued. But I would also like to underline that my DDM analysis is very vulnerable to the dividend growth rate. For example, if I implement a 3% dividend growth rate, the stock's fair value decreases to $13.6, meaning a substantial downside potential.

But, since the company's payout ratio is relatively low, flying just slightly above 15%. Therefore, I believe that the company will be able to sustain long-term dividend growth, and a 3.7% pace looks conservative.

Risks update

The major risk for a retailer like Macy's is the broader economy's weakness. Recently, Deutsche Bank shared the opinion that recession is inevitable for the U.S. When the economy weakens, it decreases consumer spending as people become more cautious with personal finance. In these circumstances, consumers are highly likely to cut spending on discretionary items like clothing, accessories, and other things that Macy's sells.

At the same time, M faces fierce competition from traditional retailers like Walmart ( WMT ), e-commerce giants like Amazon ( AMZN ), and discounters like Ross ( ROST ). Such a highly competitive landscape poses significant challenges for Macy's. The company recognizes the need to adapt to the changing retail landscape and actively pursues new approaches to appeal to customers. Its Polaris and Omnichannel plans aim to enhance the shopping experience by integrating online and in-store experiences. However, the effectiveness of these strategies in acquiring customers and driving higher spending remains highly uncertain.

Macy's relies on a complex global supply chain to source its products. Supply chain disruptions, such as delays, quality issues, or rising input costs, can affect the availability and cost of merchandise, which can adversely affect Macy's financial performance. Moreover, the company can suffer significantly because of escalating tensions between China and the U.S. Clothing represents a lion's part of the company's sales, and China accounts for 35% of worldwide apparel exports, according to Morningstar Premium. That is why a trade war between the U.S. and China can disrupt Macy's operations and is highly likely to adversely affect the company's financials.

Bottom line

Overall, I believe that headwinds are not over for Macy's. On the other hand, the stock suffered a substantial selloff year-to-date. According to my latest valuation update, now the stock is fairly priced by the market. Also, at the current stock price level, Macy's offers a decent 4.17% forward dividend yield. Based on these updates, I revised my rating for Macy's stock and upgraded it to "Hold".

For further details see:

Macy's: Now Fairly Valued