M - Macy's: Still Being Dumped On

2023-10-16 07:28:45 ET

Summary

- Macy's is undervalued and trading as if the company is going out of business.

- The department store retailer has made significant changes to its business model, but weak sales and recession fears are impacting its stock price.

- Macy's owns a valuable real estate portfolio, but the market is not giving the stock much benefit for these assets.

- The stock trades below 4x FY23 EPS targets, though the numbers could get cut.

A lot of the department store stocks now trade as if the companies are going out of business while a retailer like Macy's ( M ) continues to guide towards strong profits. The market often extrapolates current weakness into future results similar to after the Covid pull forwards. My investment thesis is ultra Bullish on the department store stock heading into the holidays, though the lingering recession fears could lead to a depressed price for an extended period.

Source: Finviz

Extrapolating Too Much

Macy's continues to slip along with the current sales trends despite knowledge the numbers are impacted by short-term issues, such as an inventory overhang in apparel. The stock collapsed during the initial Covid sales dip followed by a rebound to $30 when sales jumped and profits expanded with the shift to online sales and lower in-store costs.

The problem now is that Macy's has fallen back lower than pre-Covid levels of $15 due to recently reporting weak results. The department store faces a giveback on online sales while International travelers haven't fully replaced the tourist sales from the flagship Hudson Square store in NYC.

The end result is a very confusing financial outlook for Macy's and investor fears the department store has returned to the pre-Covid sales drip. In reality, the department store has completely altered the business with a focus on better shipping options and a shift towards beauty sales and smaller store formats.

The business would appear far better positioned than pre-Covid, but the company isn't getting any benefit from this position currently due to the reported sales dip. Macy's still forecasts a $3 EPS for FY23, yet the stock has fallen below $11.

The market is clearly fearful sales and profits will deteriorate in the future quarter due to a recession and consumers under pressure from higher interest rates, inflation and the restart of student debt repayments. The company definitely faces a precarious position towards the end of 2023, but the market should normalize in 2024. By 2024, any recession will likely have ended, Asian tourists will return and any apparel inventory overhang will end.

Macy's earned a similarly $3 in FY19 prior to Covid and numbers surged to $5+ in FY21 from the Covid boost along with contained costs. Note though, the big FQ4'21 EPS of $2.45 was only produced on $8.67 billion in sales, up fractionally from the $8.34 billion produced during FQ4'20.

Macy's didn't report strong EPS results during Covid from substantially higher sales. The clear opportunity here is to normalize back at a $3 EPS and target higher profits similar to during Covid due to the improved options of the department store from improved design setup, better shipping options and new store formats.

Real Estate

Not that it has mattered much to the stock value, Macy's has fallen to a market cap of $3 billion while the company owns a massive real estate portfolio. Back in early 2022, we backed up estimates for a $7 billion valuation for their real estate based on an analysis by Evercore ISI.

The stock never obtains any valuation from these assets, but ultimately the department store retailer has from $6 to $8 billion worth of assets based on the current analysis from Cowen and up to $21 billion by Starboard. The investment firm pegged the 700+ physical locations worth a gigantic value, including the Herald Square Manhattan property worth nearly $4 billion alone. The real estate would have a valuation far in excess of the stock valuation for the whole company.

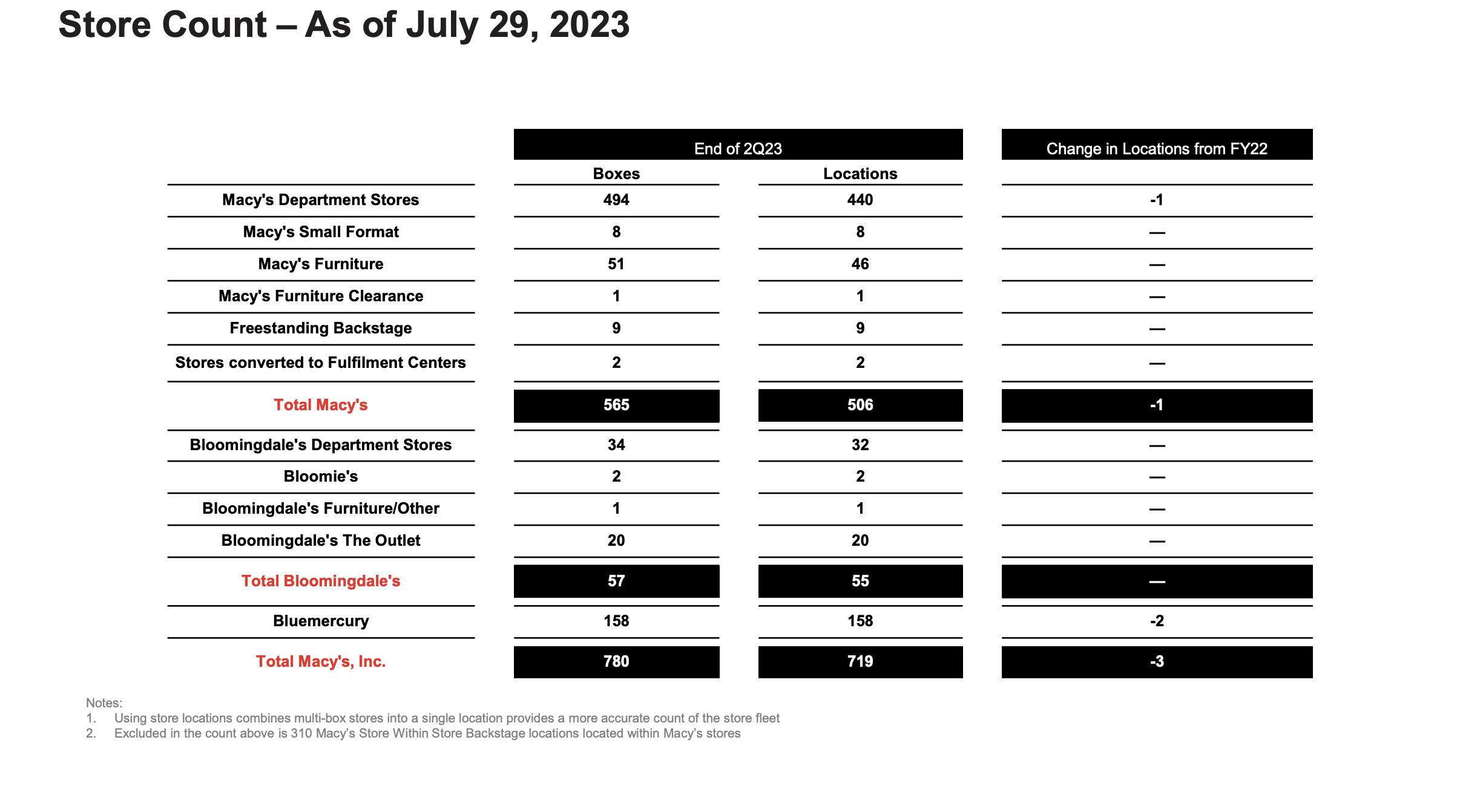

Macy's lists 719 store locations as of July 29, down slightly from the 726 listed at the end of 2021. The company owns the majority of these locations, especially the Macy's and Bloomingdale's locations, in high-quality A malls.

{kind=link}

The stock only has a market cap of $3 billion following the massive sell-off this year. The real estate assets don't drive a lot of value for the stock in the short term, as the market focuses almost entirely on the operations of the business.

Takeaway

The key investor takeaway is that Macy's is absurdly cheap trading below 4x EPS targets while the department store retailer has multiple investment firms and analysts valuing the real estate assets at prices of at least double the current market cap. The stock isn't likely to turn higher until the sales quit dipping and analysts forecast a small dip in sales next FY. Ultimately though, Macy's has strong EPS potential in the $3 to $4 range and real estate assets worth far in excess of the current market making the stock at $10 an absurd bargain.

For further details see:

Macy's: Still Being Dumped On