M - Macy's Stock Pops Higher Yet I Doubt It Will Last

2023-11-16 13:06:02 ET

Summary

- Macy's stock has rebounded by roughly 30% from its lows, driven by better-than-expected inflation numbers and 3Q23 earnings.

- The company's strategic focus on private brands, small format stores, digital marketplaces, luxury segments, and personalized offers positions it well amid economic challenges.

- While inventory improvements and strong sales results are positive, caution remains due to lingering consumer uncertainties, and a sustainable consumer recovery is crucial for long-term success.

Introduction

It's time to talk about the consumer. In this case, the consumer that shops at Macy's ( M ) . Three months ago, I wrote an article titled Macy's Stock Q2 Earnings Ahead: Trends, Tactics, And Takeaways . In that article, I discussed the impact of macroeconomic headwinds on the company and its methods to mitigate risks.

Real wage growth has emerged as a key macro factor, but concerns about inflation, energy costs, and student loans loom.

Macy's has taken steps to enhance its business, focusing on private brands, small format stores, the marketplace, the luxury segment, and personalized offers.

While a strong recovery (likely) remains a distant prospect, successful execution of strategies could lead to upward momentum.

For now, I maintain a cautious Hold rating, awaiting a stronger consumer sentiment to drive a potential bullish scenario at some point in the future.

After publication, Macy's stock dropped more than 30%.

Now, it's up roughly 30% from its lows, fueled by two things:

- Better than expected inflation numbers - this started the rally

- Better than expected 3Q23 earnings

In this article, we'll discuss both these drivers as we assess the risk/reward of buying a stock that is still trading close to 70% below its five-year highs.

So, let's get to it!

The Macy's Recovery

The third quarter of the 2023 fiscal year could have been a whole lot worse.

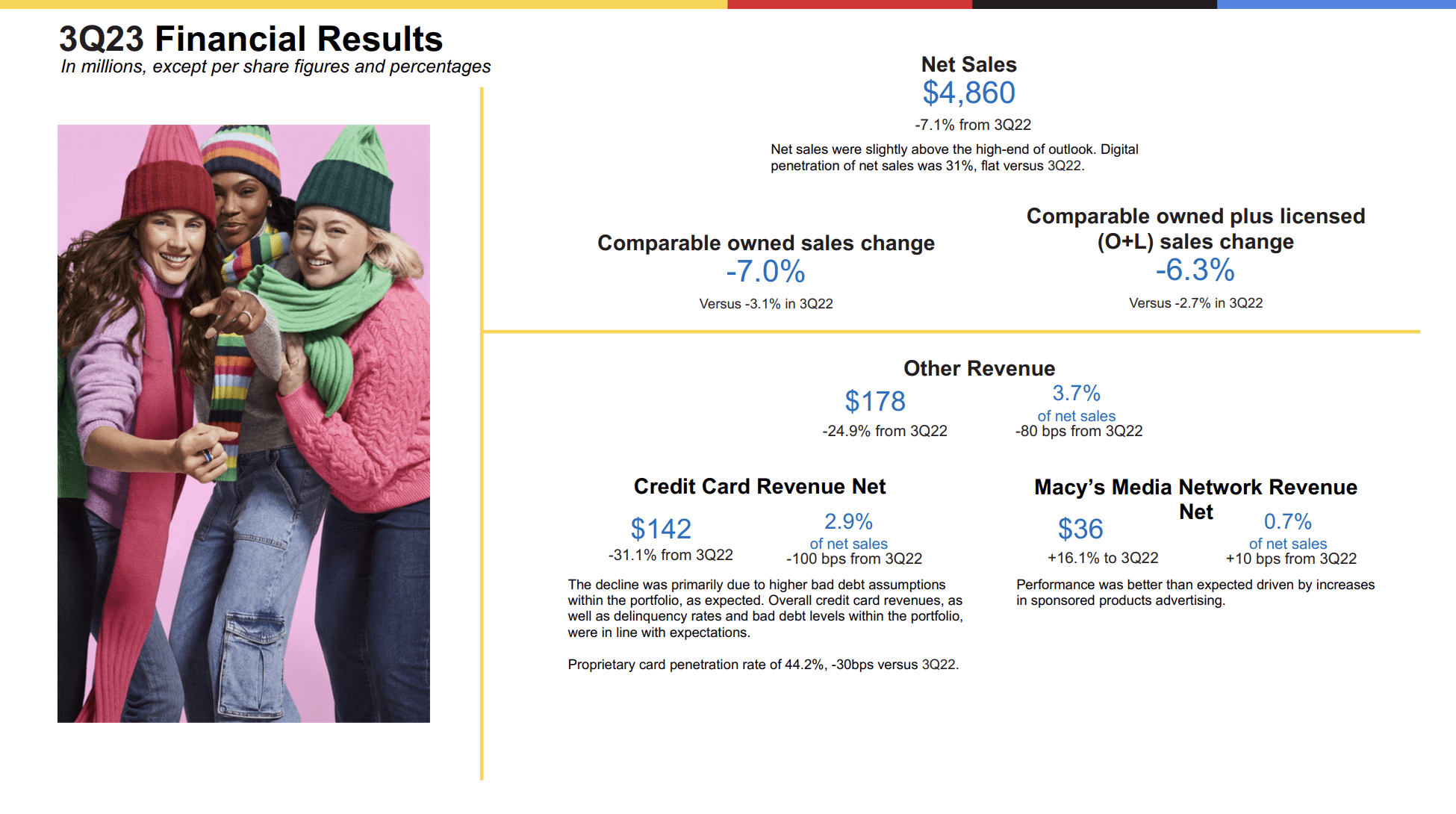

Sales results at Macy's exceeded expectations, with notable strength in beauty, fragrances, prestige cosmetics, women's sportswear, and men's tailored clothing, while challenges were observed in women's casual sportswear, big-ticket items, and handbags.

As a result, revenue declined by 7.1% to $4.86 billion ($30 million higher than expected), and comparable sales declined by 6.7%.

Bloomingdale's net sales declined 2.6%, with beauty, women's contemporary apparel, and shoes as top-performing categories.

{kind=link}

Owned AUR (Average Unit Retail) rose by 5.2%, driven by changes in product and category mix.

Other revenues, including Macy's Media Network revenue, grew by $5 million or 16%.

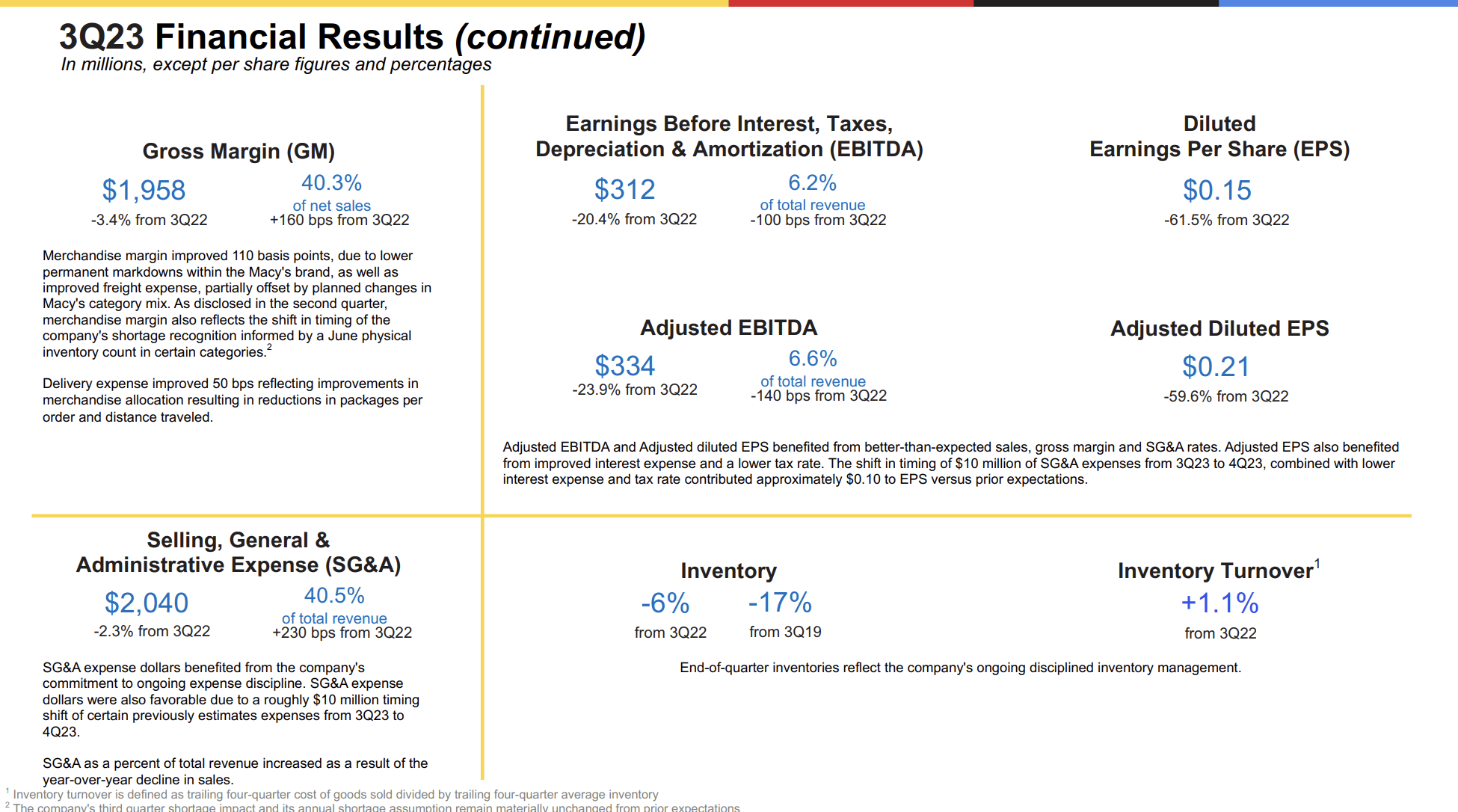

The gross margin rate was 40.3%, a 160 basis point improvement from the previous year. Merchandise margin improved by 110 basis points, attributed to lower permanent markdowns. Improved freight expense also benefited merchandise margin.

These developments are very important, as retailers had to mark down products very consistently since 2021/2022 when most had too much inventory.

Speaking of inventory, end-of-quarter inventory was down 6% year-over-year and down 17% versus 2019. Trailing 12-month inventory turn increased by 1% compared to last year, reflecting improved inventory productivity.

{kind=link}

As a result, third-quarter adjusted diluted EPS was $0.21 versus $0.52 last year, benefiting from the aforementioned better-than-expected sales, gross margin, and SG&A rates.

Analysts expected $0.01 in EPS, which makes this a very significant beat.

Now What?

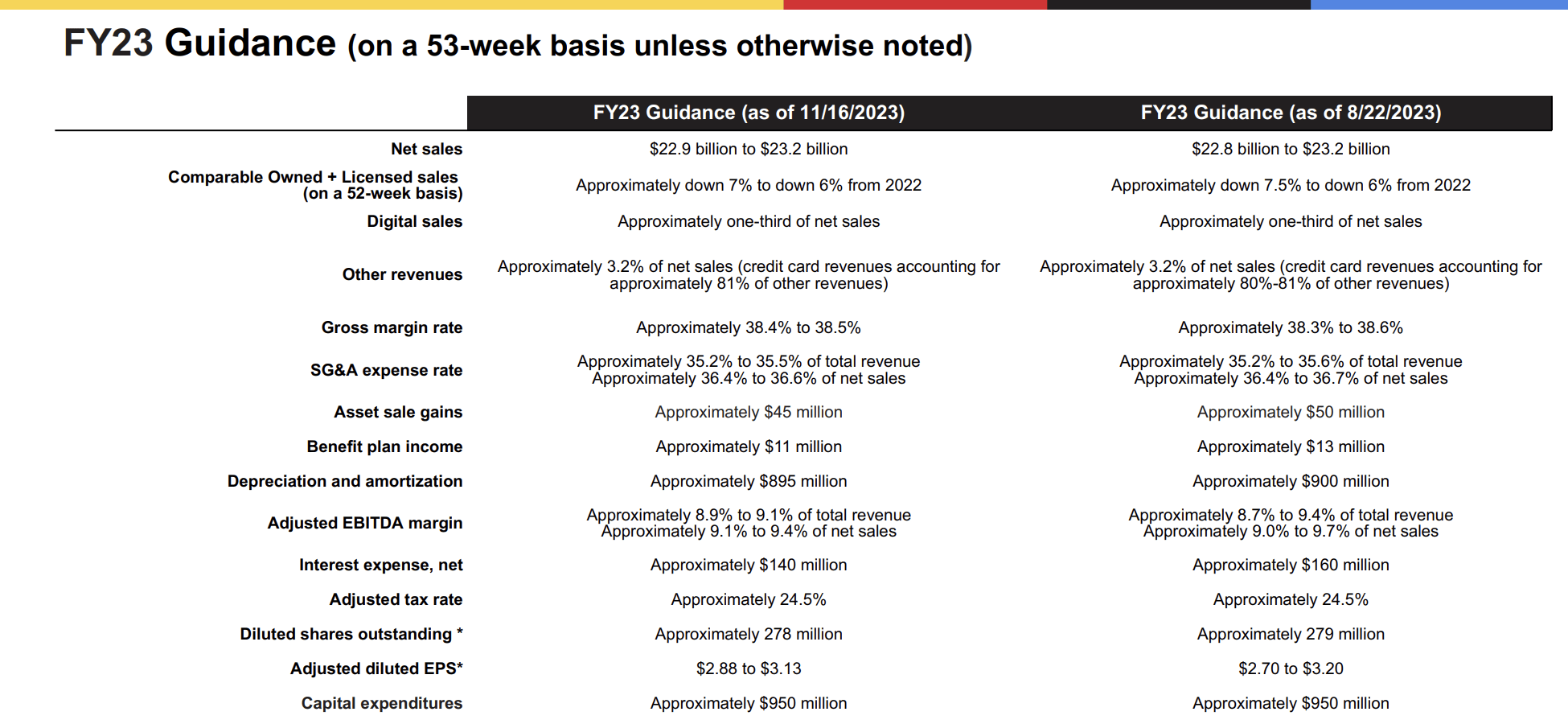

Looking forward, Macy's expects fourth-quarter net sales to be $7.95-$8.25 billion, with a gross margin rate at least 220 basis points better than the fourth quarter of 2022.

Adjusted diluted EPS is projected at $1.85-$2.10, including a $10 million shift in SG&A expenses and $15 million in combined investments.

Full-year expectations include net sales of $22.9-$23.2 billion, a comparable sales decline of 6% to 7%, and an adjusted diluted EPS outlook of $2.88-$3.13.

As we can see below, all full-year guidance numbers I just mentioned have been hiked. Needless to say, this, too, is great news in light of economic challenges.

{kind=link}

While Macy's cannot influence macro developments, the company is embracing a balanced portfolio of nameplates, leveraging data science tools, AI, and machine learning for decision-making.

This includes the five major growth factors that have served the company well so far.

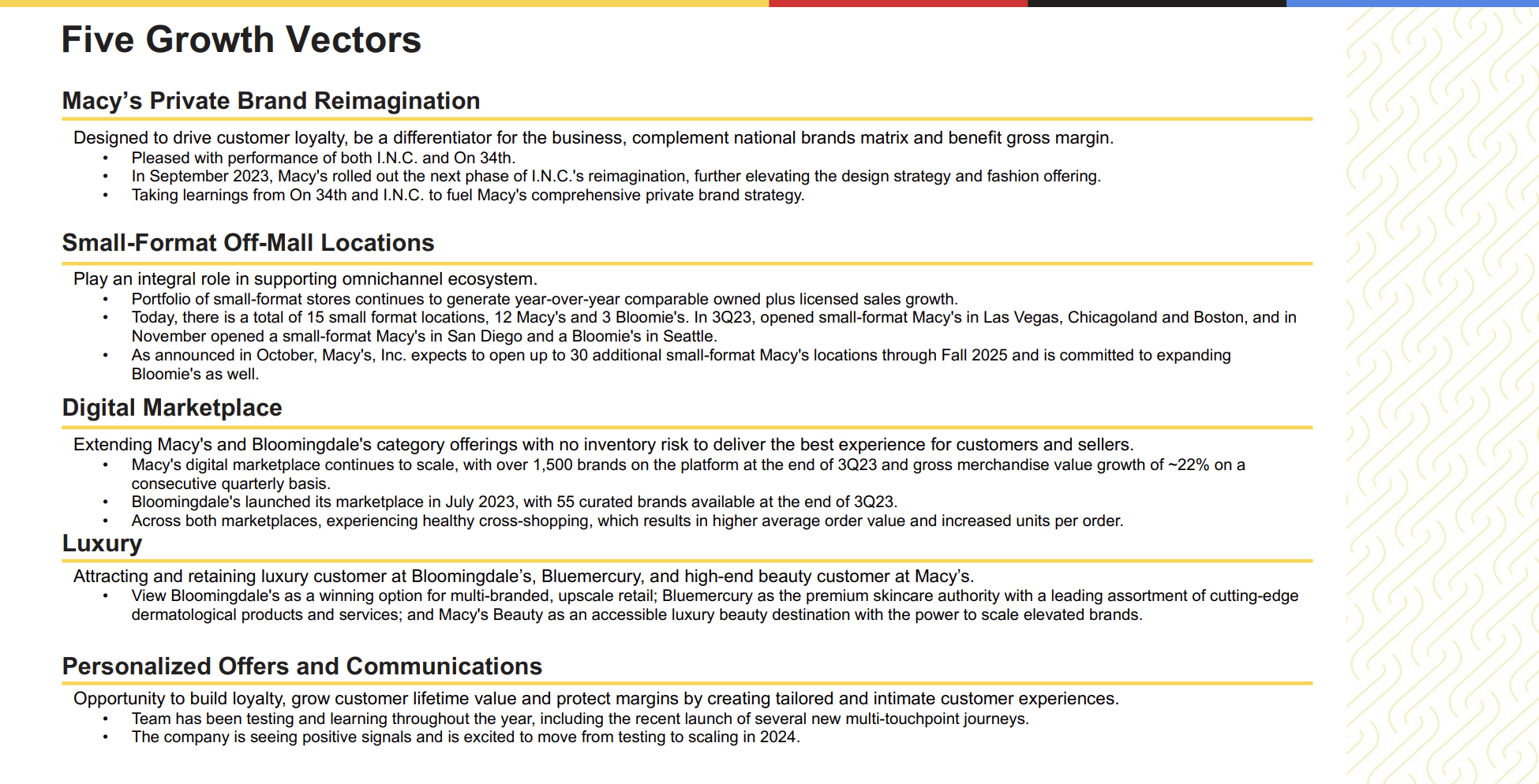

- Private Brand Reimagination: Macy's launched a new private brand on 34th Street and is pleased with the performance as it is fueling a comprehensive private brand strategy.

- Small Format Stores: The company opened new Macy's and Bloomingdale's small-format locations, generating positive customer feedback.

- Digital Marketplace: Macy's digital marketplace, with over 1,500 brands, is growing gross merchandise value by approximately 22%. Bloomingdale's introduced its own marketplace.

- Luxury: Bloomingdale's positioned as a winning option for upscale retail, Bluemercury establishing itself as a skincare authority, and Macy's beauty as an accessible luxury beauty destination.

- Personalized Offers and Communications: Macy's is testing new multi-touch journeys, which are working out well so far and are likely to be accelerated in 2024.

{kind=link}

Based on this context, the company introduced Nike in 75 stores and UgHome in 200 stores. Bloomingdale's added new brands like Veronica Beard, Hatch, and Alex Mill.

Meanwhile, Bluemercury had its 11th consecutive quarter of growth, unveiling a redesigned luxury store and spa experience in Connecticut.

Nonetheless, as part of its outlook, the company anticipates continued pressure on customer spending during the holiday season, which makes sense, as consumer sentiment took another hit.

{kind=link}

A part of this slump is a fear of inflation, as consumers expect inflation to remain sticky. Long-term inflation expectations have hit a 12-year high.

Wells Fargo

While stocks rebounded thanks to a favorable inflation print, I believe that this won't be so bullish, as a big part of the inflation decline seems to be economic weakness pressuring prices.

For example, we're starting to see cracks in employment numbers.

Jobless claims just hit a new high, which is likely to continue and a possible further drag on consumer spending.

Bloomberg

So, what do we make of this?

Valuation

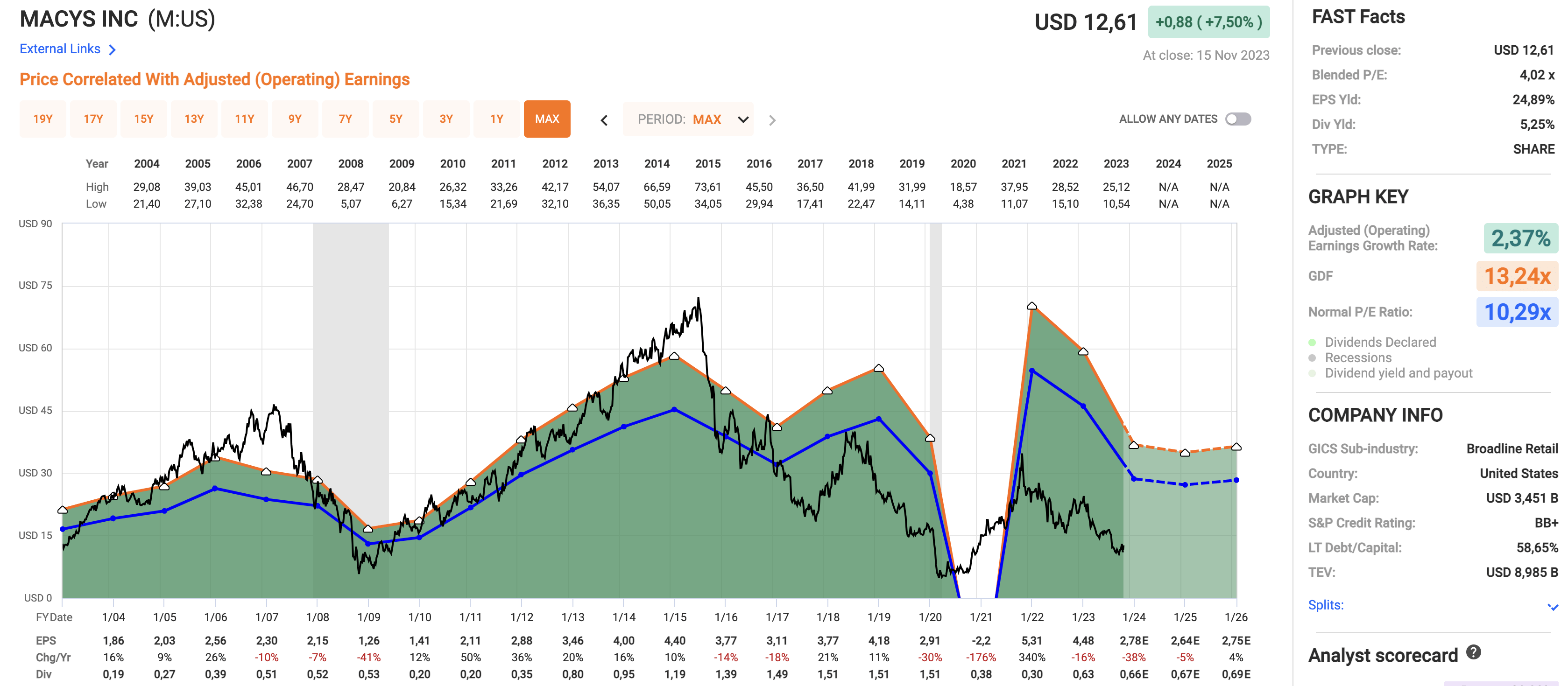

Macy's is cheap. Very cheap. The stock is trading at a blended P/E ratio of 4x. The long-term normalized multiple (going back two decades) is 10.3x.

This year, EPS is expected to decline by 38%, followed by a decline of 5% in 2024. The 2025 calendar year is expected to see a rebound in the low-single-digit range.

If the company is able to achieve this and return to 10.3x earnings, it could see a stock price of roughly $30. That's more than 100% above its current price.

{kind=link}

While the company deserves credit for a strong 3Q23, it is not out of the woods yet.

- The economic trend will make it very unlikely that the company can return to growth soon.

- Although inventory developments are promising, that's not a basis for a sustained recovery.

- A return to 10x earnings will not happen unless the market sees a sustainable recovery for the U.S. consumer.

I agree with the post-earnings jump in the company's stock price.

However, I cannot say that I'm tempted to join investors in buying M stock.

I will remain cautious until I see a more sustainable recovery for the consumer.

Until that happens, I remain Neutral on this company.

Takeaway

Macy's recent surge, driven by robust 3Q23 earnings and better-than-expected inflation numbers, reveals resilience.

Strategic emphasis on private brands, small format stores, digital marketplaces, luxury segments, and personalized offers positions the retailer strategically amid economic challenges.

While inventory improvements and a strong sales beat are commendable, caution prevails due to lingering consumer uncertainties.

The stock, currently trading at a significant discount, holds the potential for a rebound if long-term normalized earnings return.

Although a post-earnings stock price surge occurred, a sustainable consumer recovery is key for a cautious investor like me, which is why I am maintaining a Neutral stance on Macy's.

For further details see:

Macy's Stock Pops Higher, Yet I Doubt It Will Last