M - Macy's Stock Q2 Earnings Ahead: Trends Tactics And Takeaways

2023-08-21 09:00:00 ET

Summary

- Macy's upcoming earnings report offers an opportunity to evaluate its strategy and assess its growth measures.

- Real wage growth has emerged as a key macro factor, but concerns about inflation, energy costs, and student loans remain.

- Macy's has implemented measures such as focusing on private brands, small format stores, the marketplace, the luxury segment, and personalized offers to enhance its business.

Introduction

It's time to talk about Macy's, Inc. ( M ) . Founded in 1830, the company isn't just one of America's oldest stock-listed companies, but it is also a fascinating macro proxy, as its sales are driven by economic trends - on top of company measures to enhance traffic and margins.

The company is set to report its earnings on August 22, before the market opens, which makes this the perfect opportunity to:

- Assess the macroeconomic environment.

- Look into the company's growth measures.

- Assess the risk/reward of Macy shares.

So, without further ado, let's dive right in!

All Eyes Are On Potential Macro Tailwinds

In general, I prefer to avoid consumer-focused stocks. The only consumer-focused stock I own is Home Depot ( HD ), which is mainly dependent on demand for DIY and construction projects and its ability to remain competitive.

Macy's is different, as it is dependent on more consumer trends, fierce competition, and related economic developments.

Over the past ten years, Macy's shares haven't been a great place to be. Investors who bought shares exactly ten years ago have lost more than 60% on their investment, excluding dividends.

The most recent upswing was the massive consumer bull market after the first wave of lockdowns in 2020. Since then, shares have resumed their long-term downtrend, pressured by macro headwinds.

For example, in the first quarter, the company acknowledged the challenging macro environment and the impact on demand trends.

CEO Jeff Gennette noted that the company expected intensified pressure in 2023 compared to the previous year and highlighted the worsening demand trends in mid-March and April (the company reported on June 1).

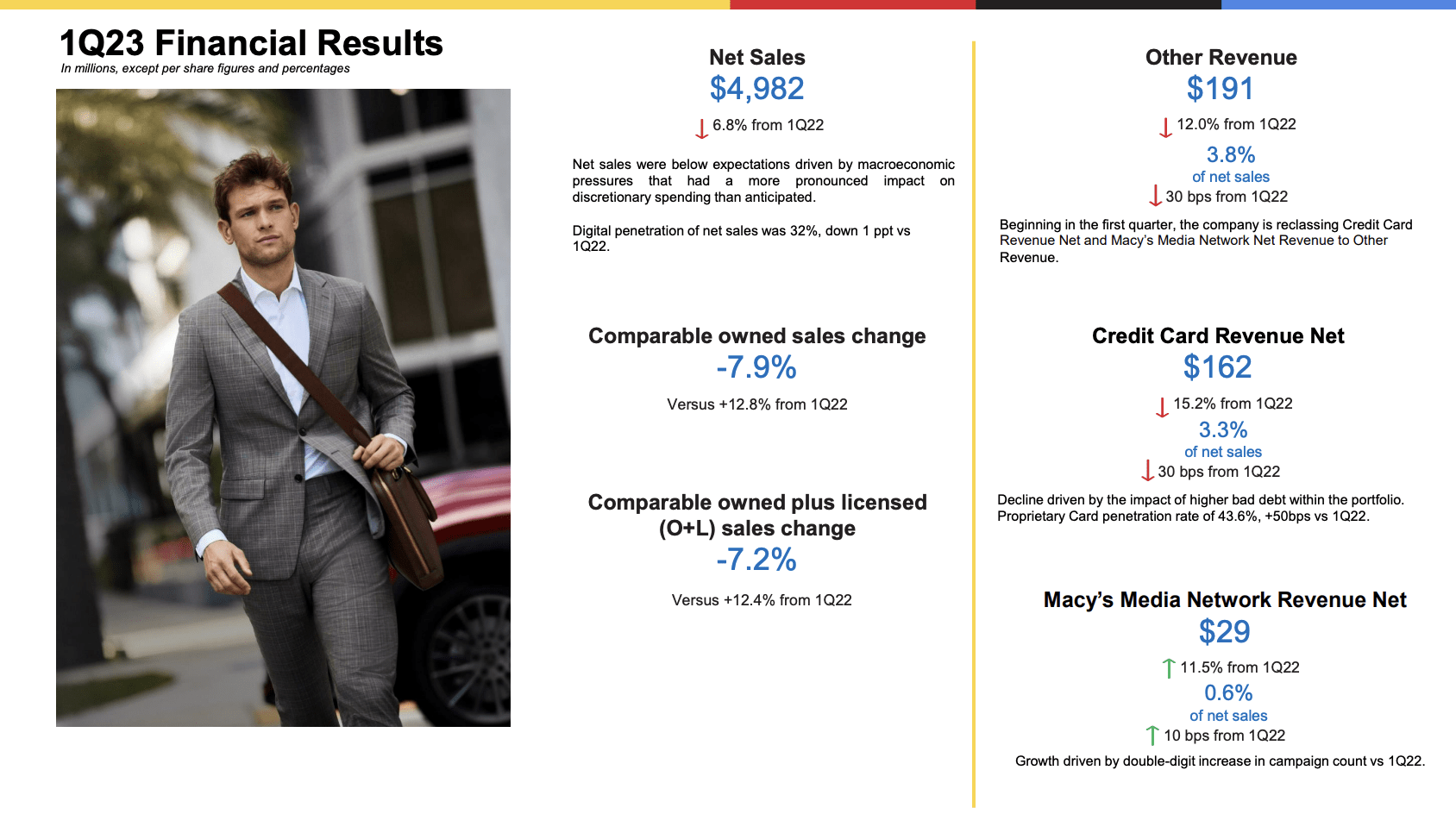

As we can see in the overview below, the results were far from great.

{kind=link}

- Net sales declined by 6.8%.

Net sales were below expectations driven by macroeconomic pressures that had a more pronounced impact on discretionary spending than anticipated . - M 1Q23 Earnings Presentation

- Comparable sales declined by 7.9% after growing by 12.8% in the prior-year quarter.

Now, hopes are that we could get a return of 2020/2021 market conditions - at least when it comes to one major macro factor: outperforming wage growth.

The single-best thing for consumers is when their wages outperform inflation. After all, that results in higher spending power.

Earlier this month, Bloomberg reported that Yellen is increasingly focusing on communicating the benefits of Bidenomics , a term coined by the administration to promote its economic success (in certain areas).

The key focus was on the fact that workers are experiencing improved conditions compared to the previous year, with real average hourly earnings surpassing inflation, indicating real wage growth.

With subdued unemployment, labor markets remain tight. Year-on-year wage growth is currently at 4.4%, which is below its peak close to 6%, but without a meaningful downtrend.

Consumer prices, on the other hand, have been in a steady downtrend, falling to 3.2% in July.

The result is positive real wage growth for three consecutive months.

Bloomberg

Using the chart below, we see that these favorable developments have led to the outperformance of retail stocks, using the SPDR S&P Retail ETF ( XRT ) as a benchmark. This ETF has gained 9% over the past three months, excluding dividends.

Unfortunately, both Macy's and the Invesco S&P 500 Equal Weight Consumer Discretionary ETF ( RSPD ) have failed to outperform the market. They didn't underperform by much, but it's still an interesting development.

This clearly shows distrust among market participants when it comes to favorable macro developments.

Based on that context, Walmart ( WMT ) recently reported its earnings, which showed interesting developments.

As reported by the Wall Street Journal, the company announced an increase in sales and profit for the latest quarter. In Walmart's case, it indicates sustained consumer spending on essentials like food and bargains.

The company's US comparable sales rose by 6.4% in the three months ending July 28. This growth, slightly slower than previous quarters, exceeded analysts' expectations of 4.1% growth.

{kind=link}

The rise in sales was driven by groceries and health products, supporting a trend of consumers prioritizing necessities amid rising prices.

Walmart also gained market share in the grocery segment.

In other words, the company did very well, just not for the reasons we discussed in the first part of this article.

Consumers continue to hunt for deals, prioritizing essentials over discretionary items: must-have versus nice-to-have.

However, in light of rising real wages, Walmart noted that the consumer outlook appears positive as unemployment remains low and wages remain strong.

Nonetheless, Chief Executive Officer Doug McMillon highlighted budget pressures from increasing energy costs, the resurgence of federal student-loan payments, higher borrowing expenses, and reduced savings.

Or, to put it differently, while consumers are benefiting from higher real wages, new troubles seem to be brewing on the horizon.

As most of my readers may know, I agree with these concerns.

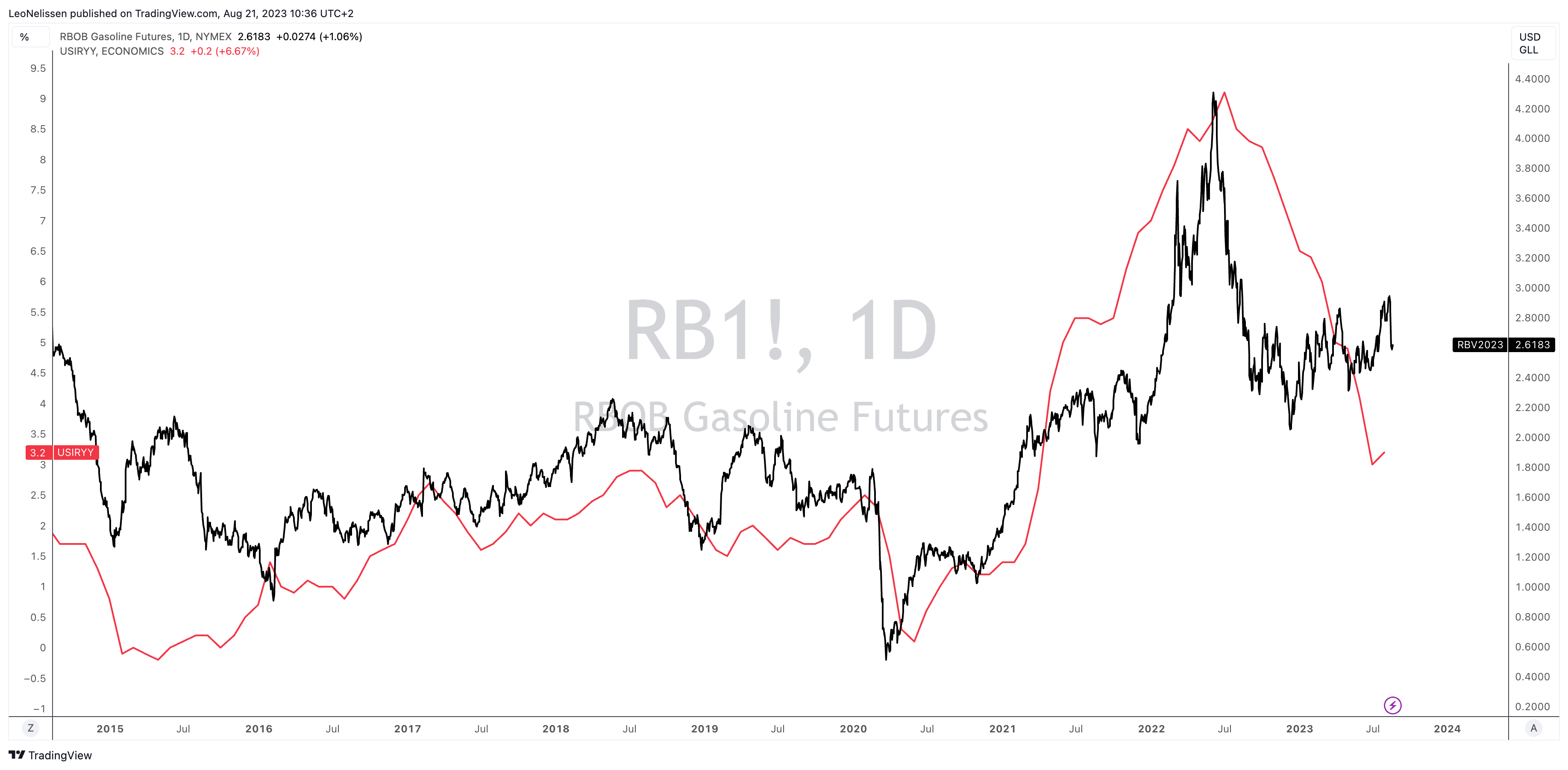

Energy prices are rising again, making further upside momentum in inflation likely.

TradingView (RBOB Gasoline, CPI Y/Y)

{kind=link}

On top of that, the returning student loan payments will be a big issue. CNBC reported that 56% of borrowers say they'll have to choose between their debt and buying groceries.

This will add a whole new layer of problems to consumer discretionaries, especially if inflation increases again.

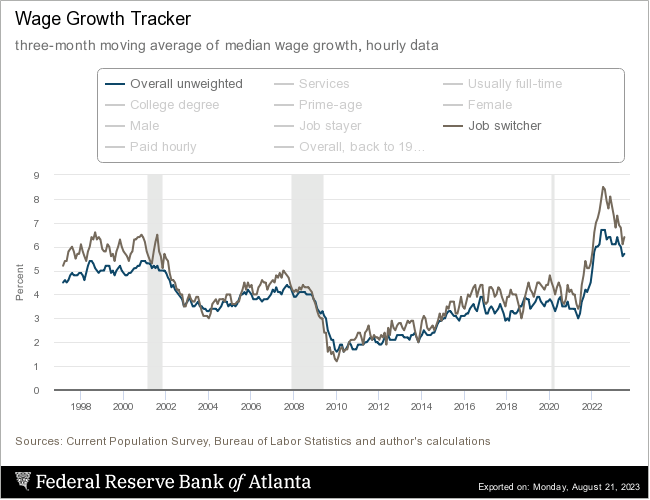

To add to the list of problems, economic growth is starting to slow, which could hurt wage growth.

While Atlanta Fed data shows that wage growth is slightly improving (from already elevated levels), with outperforming job-switcher wage growth to highlight a tight labor market, I do not expect real wages to improve.

Federal Reserve Bank of Atlanta

{kind=link}

So, what does this mean for Macy's?

Macy's Is Improving Its Business

While Macy's is unable to impact the macro environment, the company operating Macy's, Bloomingdale's, and Bluemercury is working on measures to take its business to the next level.

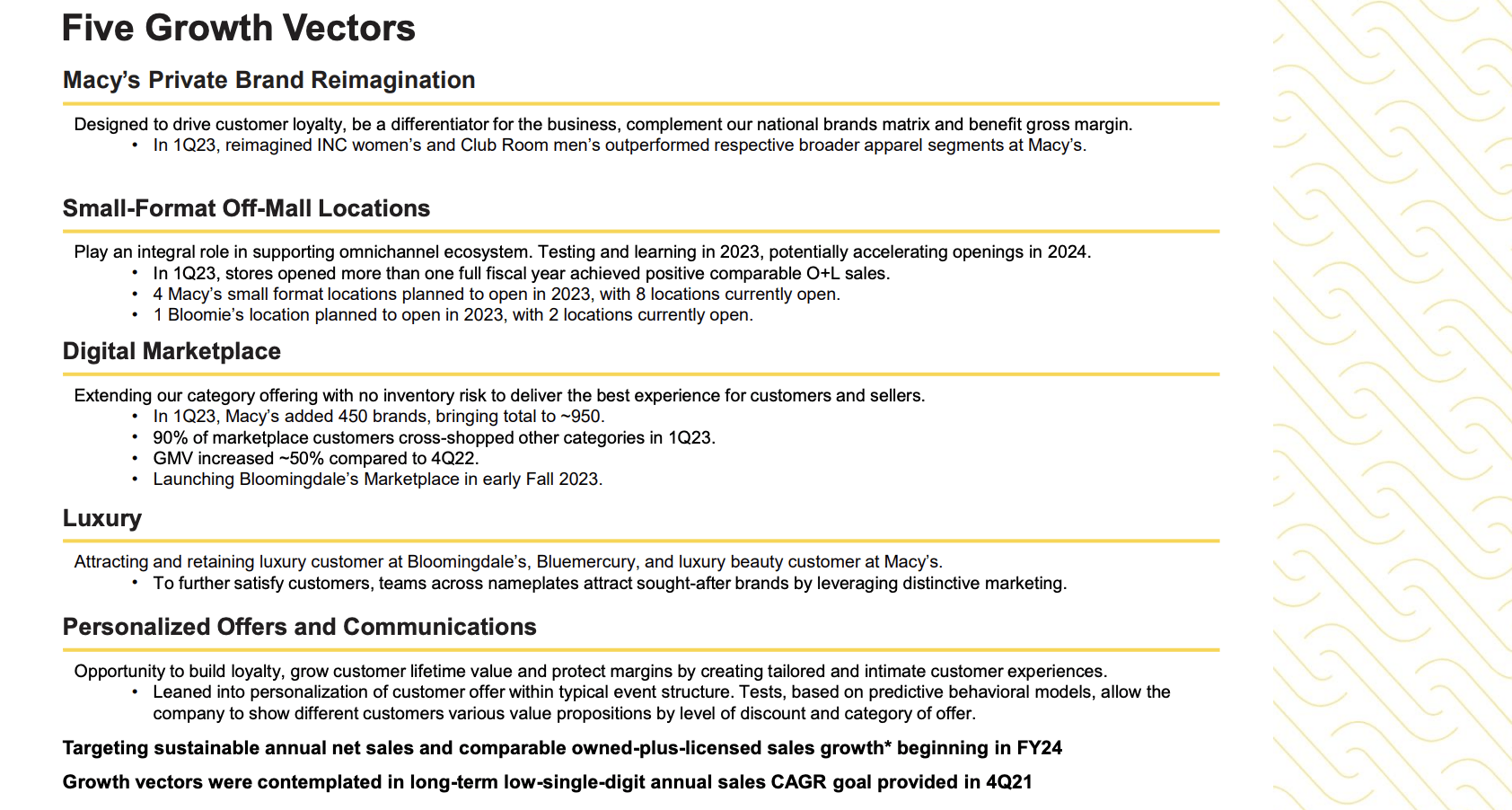

On top of acknowledging that it focused on the wrong merchandise in the first quarter, leading to markdowns, it introduced a Five Growth Vectors strategy.

{kind=link}

1. Macy's Private Brands

During its 1Q23 earnings call, the company emphasized the significance of compelling private brands alongside national and unique brands to cater to target customers.

Bloomingdale's and Bluemercury have successfully applied this formula.

The company also sees progress in the strong performance of reimagined brands like INC Women's and Club Room Men's, which outperformed their respective apparel segments in the first quarter.

Macy's also hinted at the launch of a new women's apparel and accessories brand later in the summer.

While I agree with this strategy, it emphasizes the company's dependence on bringing the right products to market at the right time with the right price tag. That's challenging and one of the reasons why I like to own consumer stocks further up the supply chain.

2. Small Format Stores

The company also saw success when it came to optimizing the store portfolio for both Macy's and Bloomingdale's. Small format stores provide a localized off-mall experience, resulting in positive comparable sales and high customer experience scores.

Macy's noted that these stores don't cannibalize existing markets and instead drive additional shopping trips.

As a result, the company will expand its small-store portfolio.

3. Macy's Marketplace

The company was also highly satisfied with Macy's marketplace, which saw an increase in the number of brands and categories. New and younger customers are responding positively, leading to larger basket sizes.

{kind=link}

Furthermore, gross merchandise value increased by over 50% compared to the previous quarter, and average order value and units per order were also higher for marketplace customers.

4. Luxury Segment

With record sales at Bloomingdale's and Bluemercury in fiscal 2022. The company sees opportunities for growth in stores, digital, and marketplace channels for both luxury-focused nameplates.

During its earnings call, the company noted new efforts to elevate the beauty business by offering a larger luxury assortment, which has shown limited price resistance and potential for more partnerships.

In the upcoming earnings call, I'm eager to hear if the company is successful in offsetting weakness in the cheaper segments with higher-margin luxury items.

5. Personalized Offers and Communications

Macy's sees the potential of personalized offers and communications, with the ability to reach over 40 million consumers with tailored offers.

So far, tests based on predictive behavioral models are showing different customers various value propositions.

As one can imagine, personalized offers can drive sales growth, margin expansion, and customer engagement.

The company has, therefore, accelerated analytics-powered campaigns in the second quarter to inform opportunities at Bloomingdale's and Bluemercury.

Needless to say, we'll hear how well this is going in the next earnings call.

Preparing For Macy's 2Q23 (+ Valuation)

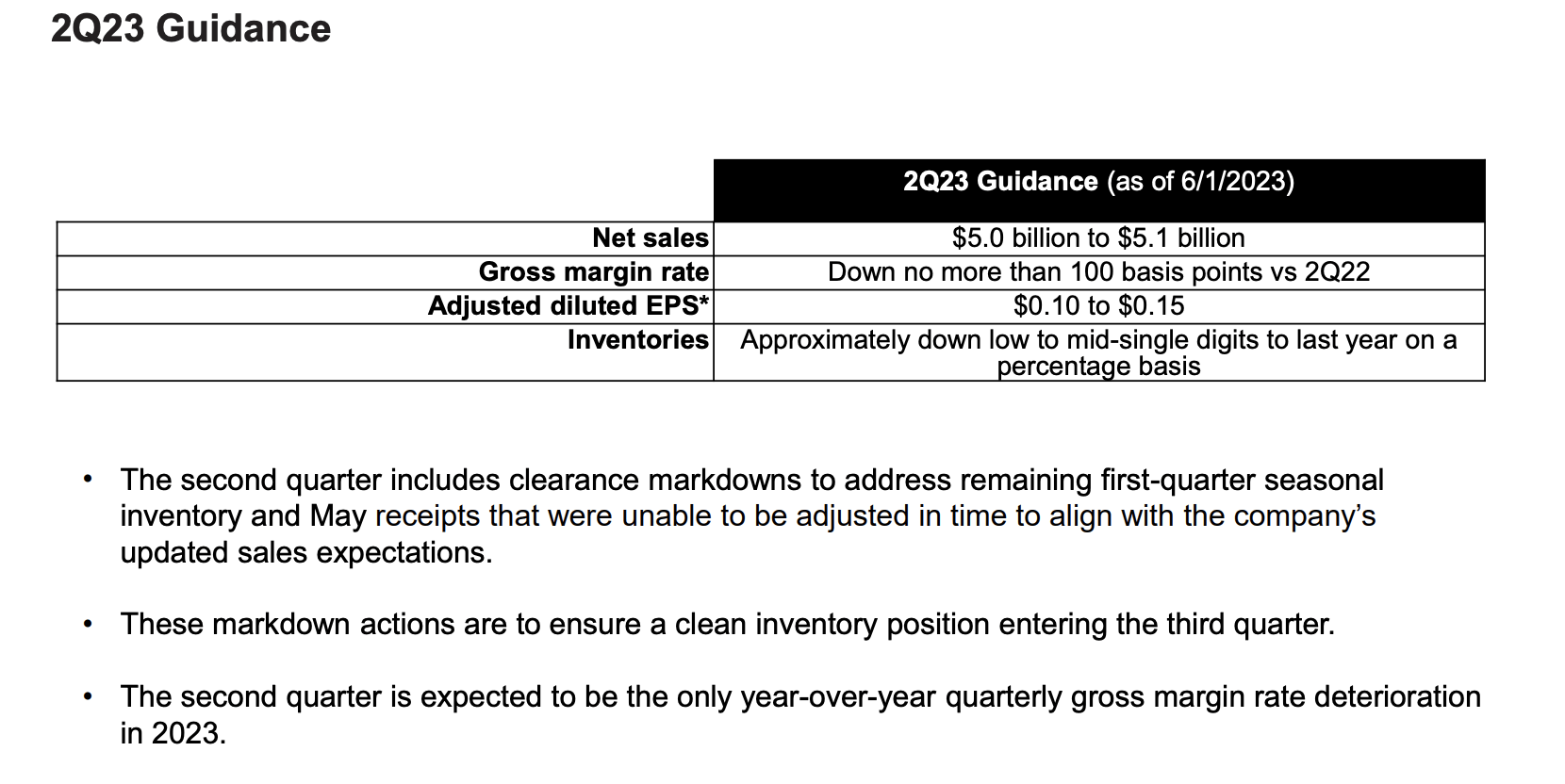

For the second quarter, Macy's expects sales to come in between $5.0 and $5.1 billion. Adjusted diluted EPS is expected to be between $0.10 and $0.15, which does not include potential buybacks.

{kind=link}

This is what the company is incorporating in its guidance (emphasis added):

The high end of our second quarter and full year guidance ranges assume heightened macro pressures experienced in mid-March through April that they persist , while the low end of both contemplates potential deterioration as the year progresses.

If demand improves, we will use our ample inventory receipt reserve, which is above last year's levels to chase into areas of strength as they materialize . Availability of goods remains robust, and we are confident that with our strong liquidity position, we will be able to secure the right product to support demand curves, if justified. - M 1Q23 Earnings Call

What's interesting is that analysts believe this range is still valid.

Using Nasdaq data, analysts expect the company to generate quarterly EPS between $0.11 and $0.17 with a consensus of $0.13. This is based on eight estimates. The company's EPS received one downgrade in the past four weeks and one upgrade.

{kind=link}

Besides the EPS numbers, I'll be looking for comments and developments regarding the company's five growth vectors, organic growth in light of improved real wages, and forward-looking statements that may confirm my view on sticky inflation and the potential deterioration in consumer spending down the road.

With regard to its valuation, we're dealing with a 2.7x LTM EBITDA multiple and a 3.1x NTM EBITDA multiple.

Prior to 2016, M shares were trading close to 8x EBITDA. That number has gradually dropped, as investors simply weren't interested in applying a higher multiple to a company with incredibly inconsistent revenue growth.

On top of that, the alternatives are just better.

As I already said, I prefer to buy stocks like Home Depot with better track records and fewer (but different) risks.

On top of that, investors can buy warehouse operators like Prologis ( PLD ), e-commerce giants like Amazon ( AMZN ), and companies with strong secular growth, like AutoZone ( AZO ).

I'm not trying to get anyone to bail on Macy's. I'm just making the case for a gradual decline in its valuation multiple.

The current consensus price target is $17.80, which is 18% above the current price.

That's a fair target and easy to achieve if the company reports success in its business improvements and better-than-expected sales volumes.

However, I will maintain a Hold rating, as I do not like the risks of a potential inflation rebound and additional uncertainties in light of Macy's fragile recovery.

I will turn bullish the moment we get a high likelihood of a longer-term recovery in consumer sentiment. If that happens, along with successful business improvements, we could get a very strong bull case at some point.

Takeaway

The outlook for Macy's is complex, marked by its sensitivity to economic trends and competitive challenges.

The upcoming earnings report offers a chance to evaluate its strategy.

Real wage growth has emerged as a key macro factor, but concerns about inflation, energy costs, and student loans loom.

Macy's has taken steps to enhance its business, focusing on private brands, small format stores, the marketplace, the luxury segment, and personalized offers.

While a strong recovery (likely) remains a distant prospect, successful execution of strategies could lead to upward momentum.

For now, I maintain a cautious Hold rating, awaiting a stronger consumer sentiment to drive a potential bullish scenario at some point in the future.

For further details see:

Macy's Stock Q2 Earnings Ahead: Trends, Tactics, And Takeaways