MSGE - Madison Square Garden Entertainment: A Fairly Valued Pure Entertainment Play

2023-08-09 14:56:29 ET

Summary

- Madison Square Garden Entertainment was recently spun-off from Sphere Entertainment.

- The company holds some of the most iconic venues in NYC and Chicago and holds a solid financial position.

- However, we find the equity to be fairly valued and think there are better opportunities in the market right now.

Investment Thesis

Madison Square Garden Entertainment ( MSGE ) was recently spun off from Sphere Entertainment ( SPHR ) in a transaction that separated the MSG arena and Christmas Spectacular production from the Sphere development and MSG network. Given that spin-offs tend to generate substantial shareholder value, we decided to take a deeper look. Despite MSGE impressive portfolio of venues and financial performance, we found out that the equity is fairly valued. A rapid de-lever of the balance sheet or an accelerated share repurchase program may propel the stock higher, but we don't see an attractive risk-return ratio at current levels.

Business Overview

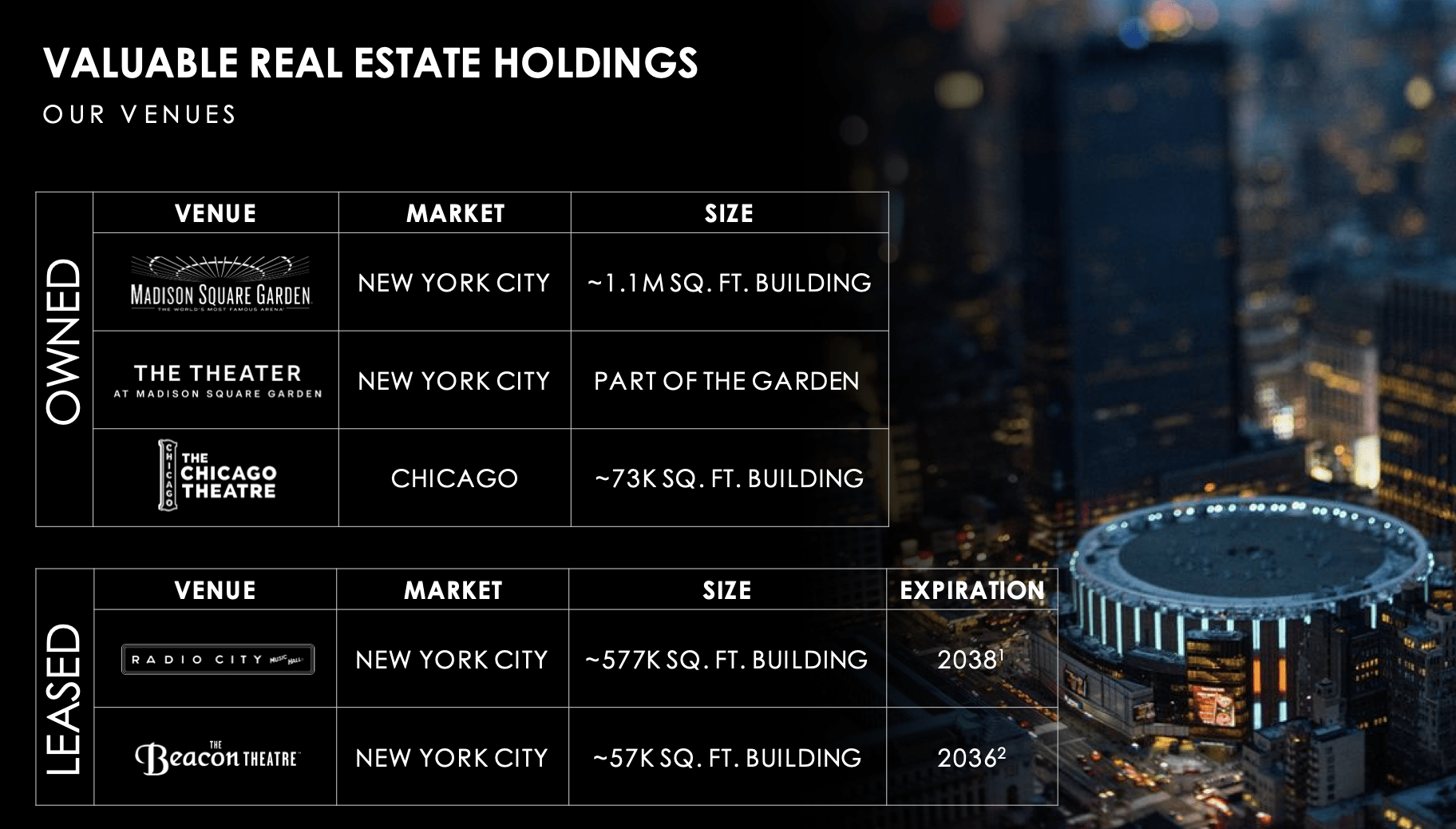

MSGE portfolio is composed of 5 iconic venues across New York City and Chicago:

- Madison Square Garden : Not only is the world's most famous arena but also the #1 grossing venue of its size in the world . It has a ~21,000 seat capacity and is home to the New York Knicks ((NBA)) and the New York Rangers ((NHL)).

- The Theater at Madison Square Garden : It is located inside the Madison Square Garden and has a ~5,600 seat capacity. Recently there were rumors that an Italian private developer was interested in acquiring it for more than $1 billion .

- Radio City Music Hall : It is the #3 grossing venue of its size in the world and has a ~6,000 seat capacity. It is an iconic theater of NYC and a national landmark where the Christmas Spectacular Starring the Radio City Rockettes show is performed for +1 million people every year.

- The Chicago Theatre : It is the #5 grossing venue of its size in the world and has a ~3,600 seat capacity.

- Beacon Theatre : It is the #6 grossing venue of its size in the world and has a ~2,800 seat capacity

{kind=link}

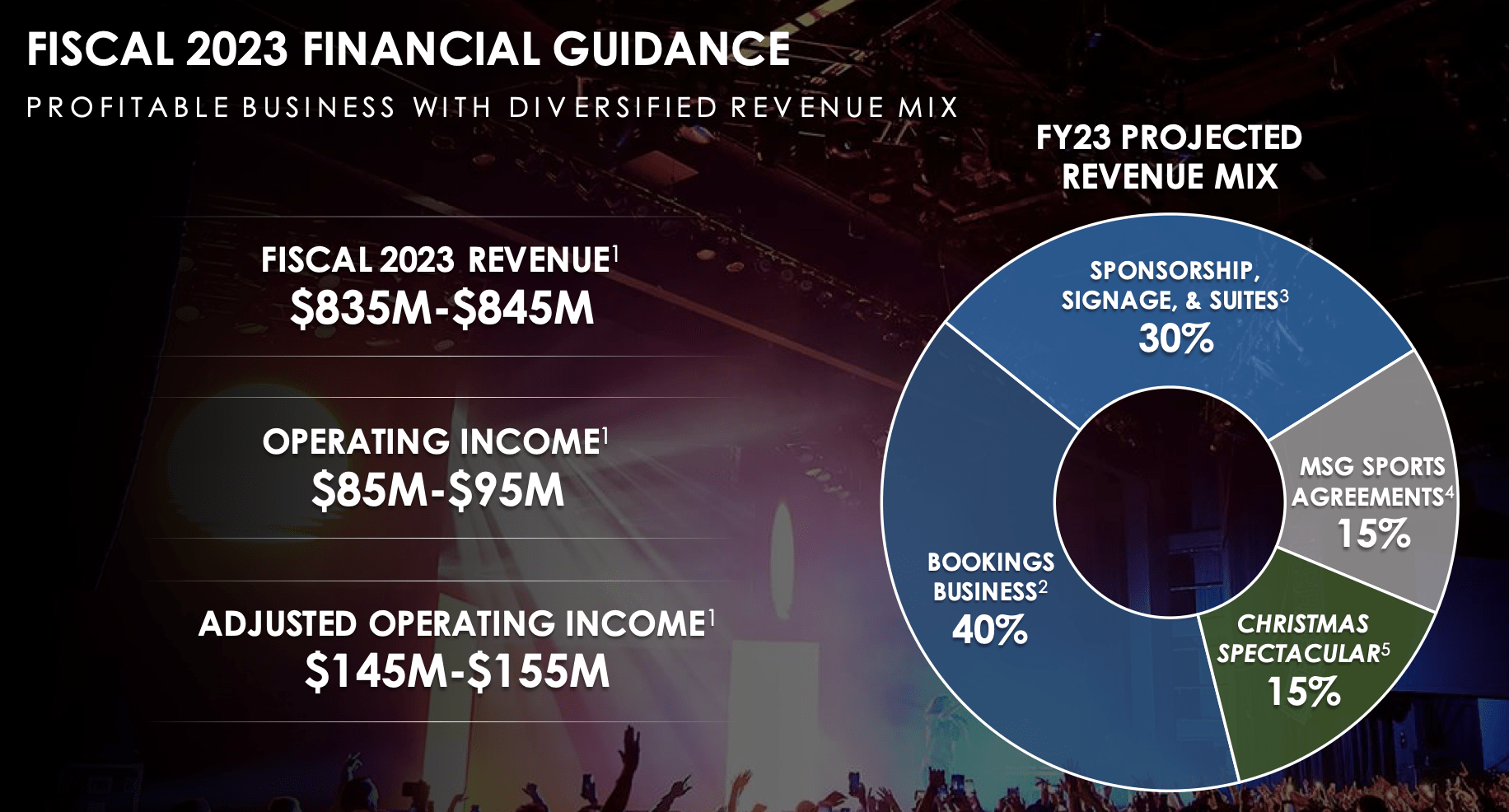

Although they don't disclose sales by venue, the company sources of revenue can be divided in 2: bookings and sponsorship, signage & suites.

The booking business includes ticketing, venue license fees, food, beverage, and merchandise sales for all events, including the ones they promote and don't. They classify them in Christmas Spectacular, Knicks, and Rangers games and all others events. This comprises ~70% of total revenue.

Sponsorships, signage, and suites are related to the sale of advertising space in the arena and the suites at The Garden, which are generally sold to corporate customers with the majority being multi-year licenses with annual escalators. They represent the remaining ~30% of sales.

Q3 FY2023 Financial Results

MSGE reported Q3 fiscal 2023 financial results on May 18. Revenue came in at $201.2 million, up 4% YoY and beating estimates by $9.2 million. Consumer and corporate demand remained very strong, while in-venue per-capita spending continues to exceed results for the prior year. In addition, suite and sponsorship revenues are on track to exceed pre-pandemic levels.

Operating income increased 55% to $24.7 million, representing 12.3% of sales vs. 8.2% a year ago. The increase was driven by higher gross profits, a 6% decrease in G&A expenses and lower restructuring costs. Adjusted operating income, on the other hand, was $38 million, 12.8% more than in Q3 fiscal 2022. Lastly, EPS was $0.42, beating estimates by $0.21 or 50%, which took Wall Street by surprise and caused the stock to jump 13%.

Outlook

The company is on track to host nearly 900 events and more than 5 million guests at its venues in fiscal 2023. As a result, they expect full-year revenue to be in the range of $835-845 million, operating income between $85-95 million and adjusted operating income around $145-155 million.

{kind=link}

Thinking further ahead, the management stated during the Q3 earnings call that they have no current plans to acquire or develop new venues nor make significant renovations. Right now they are focused on continuing to grow organically. This includes driving higher sell-through and ticket yield, as well as slowly increasing the number of shows.

However, their top priority is paying down the debt they incurred during the pandemic and returning capital to shareholders. Total debt outstanding as of Q3 was $659 million, which amounts to approximately $12 million in quarterly interest payments. Although they didn't settle a leverage target (right now is 3.6x Adj operating income), they stated that they expect to de-lever rapidly. Moreover, they also authorized a $250 million share buyback program (~15% of the share outstanding) from which they have already repurchased $25 million in shares from Sphere (Sphere still owns 25% of MSGE shares outstanding).

Valuation

Analysts estimate that full-year EPS will come in at $1.01 per share. However, we see this highly unlikely given that till Q3 MSGE gained $1.95 per share. Q4 is typically a seasonal low period, but we don't think they will lose half of what they made in the year. We think that estimating $1.3-1.4 EPS for FY 2023 is more reasonable, and even conservative. If we take this number, MSGE is currently trading at 24.4x P/E . Moreover, the stock is trading at 14.9x EV/EBIT (using the management guidance of $150 in EBIT for FY 2023). These are not exactly cheap multiples, but they are not expensive either.

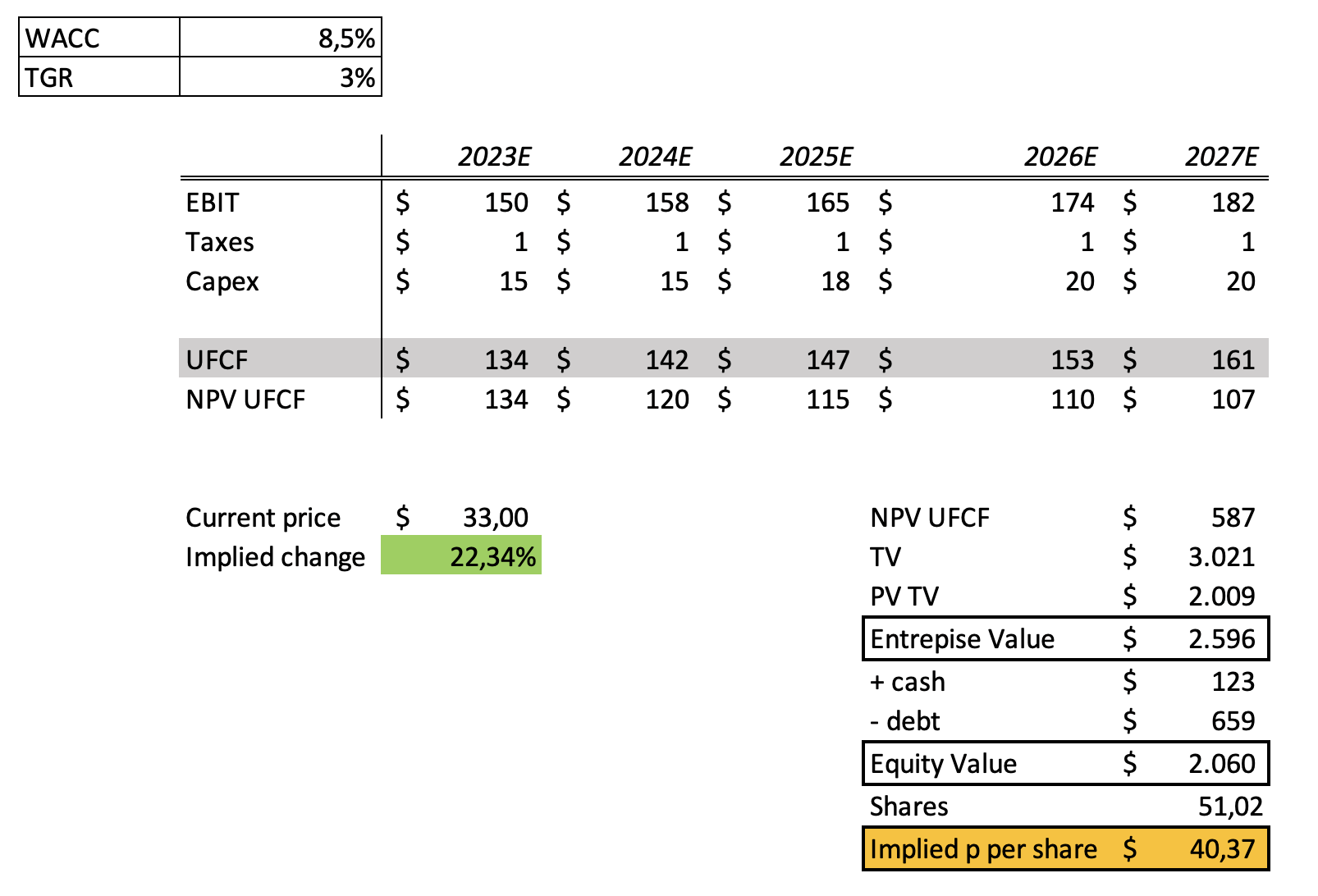

We also decided to build a DCF model. We assumed $150 million in EBIT (the adjusted EBIT figure in MSGE takes into account D&A), minimal tax expenses and maintenance capex in line with management estimates. We also assumed a WACC of 8.5% and a TGR of 3%.

{kind=link}

The implied price per share is $40.37, which represents a 22% increase from current levels. A big explanation for these results is that MSGE will be a minimal taxpayer till 2027. If we were to take a 20-30% effective tax rate, the UFCF figure would have been much lower.

Overall we don't find the equity very attractive based on its valuation, but given the amount of cash available to return to shareholders the stock may perform better than we expect.

Risks

MSGE is controlled by the Dolan family. All members of the family combined hold around 66% of the voting power, which means that they can effectively block or pass any proposal. Moreover, 9 out of the 17 board members are members of the Dolan family.

We also cannot oversee how a recession would impact MSGE. In such a scenario, spending on entertainment events and concerts could fall off a cliff, as consumers tend to prioritize essential expenses. This decline in consumer spending would result in decreased ticket sales and attendance, posing challenges for profitability and growth.

Takeaway

To sum up, MSGE is a great company that holds some of the most iconic venues in NYC and Chicago and whose financial performance has been improving year after year. However, the current price point makes us stay on the sidelines as we think there are better opportunities in the market.

For further details see:

Madison Square Garden Entertainment: A Fairly Valued Pure Entertainment Play