MSGS - Madison Square Garden Sports: A Potential Value Trap

Summary

- At first glance, the company appears undervalued.

- But the sale of the Knicks and Rangers is highly unlikely.

- On closer inspection, applying alternative valuation methods reveals that the stock does not seem undervalued anymore.

Thesis

Today, Madison Square Garden Sports Corp. (MSGS) held its earnings call and released its latest earnings report. With eager anticipation, individuals likely hoped to gain insights into how the company intends to bridge the gap between the estimated value of the Knicks and Rangers and the market capitalization. It should be widely known that there is a discrepancy between the two values. But what is the likelihood of achieving a market-beating return without a sale? I believe that over a 5-year period, this investment is unlikely to outperform the S&P 500. This is due to the following reasons: The valuation of the company in relation to its earnings is excessively high, and the return on equity and return on capital metrics are disappointing and fall well below expectations.

Short Introduction

MSG Sports boasts a roster of renowned professional sports teams, including the New York Knicks of the NBA and the New York Rangers of the NHL. Its properties also encompass two developmental teams - the Westchester Knicks, the official G-League affiliate of the Knicks, and the Hartford Wolf Pack, serving as the player development team for the Rangers in the American Hockey League.

The company has made its mark in the rapidly growing esports industry through its ownership of Counter Logic Gaming, a leading North American esports organization, and its participation in Knicks Gaming, a franchise in the NBA 2K League.

Analysis

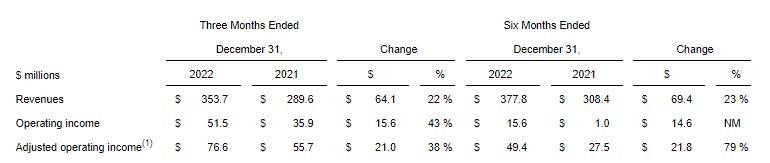

Let us begin by examining the latest quarterly figures that have just been published. The results are quite promising. The revenue has seen a significant increase of 22% compared to the previous year, and the operating income has skyrocketed by 38%. This growth was widespread, as total revenues and per-game revenues for tickets, suites, sponsorship, food and beverage, and merchandise all saw a year-over-year increase in comparison to the second quarter of fiscal 2022.

{kind=link}

Furthermore, a vast majority (over 90%) of the season ticket holders have opted to renew their tickets, while new season ticket packages experienced robust demand. Additionally, the run rate impact of deals with sports gaming companies can be felt since the start of the NHL and NBA seasons. Additionally, a special dividend of $7.00 per share, amounting to roughly $173 million, and a $75 million accelerated share repurchase program were carried out, returning close to $250 million to shareholders , representing approximately 5% of the market cap. Information about whether a dividend will be issued in 2023 is not yet known. However, during the current earnings call, it was stated that excess cash flows will be used first to pay down debts. However, it was also noted that they are aware of the difference between intrinsic value and the current market cap, and they appear confident in their ability to generate shareholder value in the future.

Intrinsic Value

I think everyone following this stock should be aware that the estimated market values of the Knicks and Rangers are probably higher than the current market cap of the stock. A recent evaluation by Sportico assessed the Knicks at $6.6 billion and the Rangers at $2.2 billion , as reported by Forbes, bringing the total to $8.8 billion or ~$360 per share. When compared to the $8.8 billion, the $4.37 billion market cap represents an undervaluation of almost 100%. The challenge lies in the fact that this value can only be realized through a sale, and there are currently no signs that this will occur in the near future. However, there is a glimmer of hope as the NBA has allowed private equity and sovereign wealth funds to enter the marketplace, and during today's earnings call, they stated that they would not rule out the possibility of selling a minority stake. The question now arises as to whether the sale of a minority stake would be sufficient to align the stock price with the intrinsic value.

Metrics

Given that the intrinsic value, as determined by the brand values, is currently only theoretical, I suggest examining the company's fundamental data. A sale of minority stakes, in my opinion, is insufficient as the value lies in being in control of the franchise, not just being a minority shareholder. It must be noted that an EV/EBIT of ~60 and an FCF yield of ~2% are indicative of the company's high valuation relative to its earnings. The company is not considered a good value, and it is likely overpriced.

{kind=link}

The underlying ROC and ROE values also indicate that capital has not been used efficiently. I personally prefer values in the 20% range, which the company is currently far from achieving. But there's always room for improvement.

Opportunities

The current NBA TV agreement is set to end in 2025, which presents the opportunity for a new, highly lucrative TV deal that could drive up revenues. Additionally, there is a remote chance (as of now) that the Knicks could become NBA champions. I believe that winning a championship could boost the share price significantly.

Should the management decide to pay an annual dividend and continuously reduce outstanding shares, it would likely have a positive effect on shareholder value.

Conclusion

Given that the sale of the Knicks and Rangers is highly unlikely, it is advisable to examine metrics like EV/EBIT to determine whether there is an undervaluation. Upon closer inspection, it appears that some of the theoretical sale values may already be reflected in the stock price, as an EV/EBIT of ~60 is not considered to be favorable. Considering the absence of factors that could drive the share price higher, Madison Square Garden Sports Corp. is not a suitable investment for me. Despite its appearance of being undervalued, the likelihood of a sale occurring is extremely low, making it a potential trap for value investors. As a result, I anticipate that Madison Square Garden Sports Corp. will underperform the S&P 500 over the next 5 years.

For further details see:

Madison Square Garden Sports: A Potential Value Trap