MDGL - Madrigal Pharmaceuticals Setting The Standard

Summary

- Madrigal's lead drug candidate was already expected to be successful in its pivotal trial.

- FDA approval would then be earned by a positive on one of the trial’s dual endpoints.

- Because both endpoints were met, something not seen in Phase 3, Madrigal will rule the market for years.

Madrigal (MDGL) grew 272% to a $4.9 billion market cap biotech since my earlier coverage. The magnitude of the rally was likely because there was doubt with management's confidence that MAESTRO-NASH, a Phase 3 study currently assessing the safety and efficacy of resmetirom for the treatment of nonalcoholic steatohepatitis ("NASH"), would hit its dual primary endpoints (PEPs), a doubt this author shared. But trial did it (see Table 1), and now resmetirom is in a unique position. The predicted financing of $300 million also came to pass. So the big question for investors is, can share prices go higher?

Table 1. Key Endpoints of MAESTRO-NASH

| Primary Endpoint |

| Resmetirom 80 mg |

| p-value |

| Resmetirom 100 mg |

| p-value |

| Placebo |

| NASH resolution (ballooning 0, inflammation 0,1) with ?2-point reduction in NAS and no worsening of fibrosis |

| 26% |

| <0.0001 |

| 30% |

| <0.0001 |

| 10% |

| ?1-stage improvement in fibrosis with no worsening of NAS |

| 24% |

| 0.0002 |

| 26% |

| <0.0001 |

| 14% |

| Key Secondary Endpoint |

| LDL-C lowering (24 weeks) |

| -12% |

| <0.0001 |

| -16% |

| <0.0001 |

| 1% |

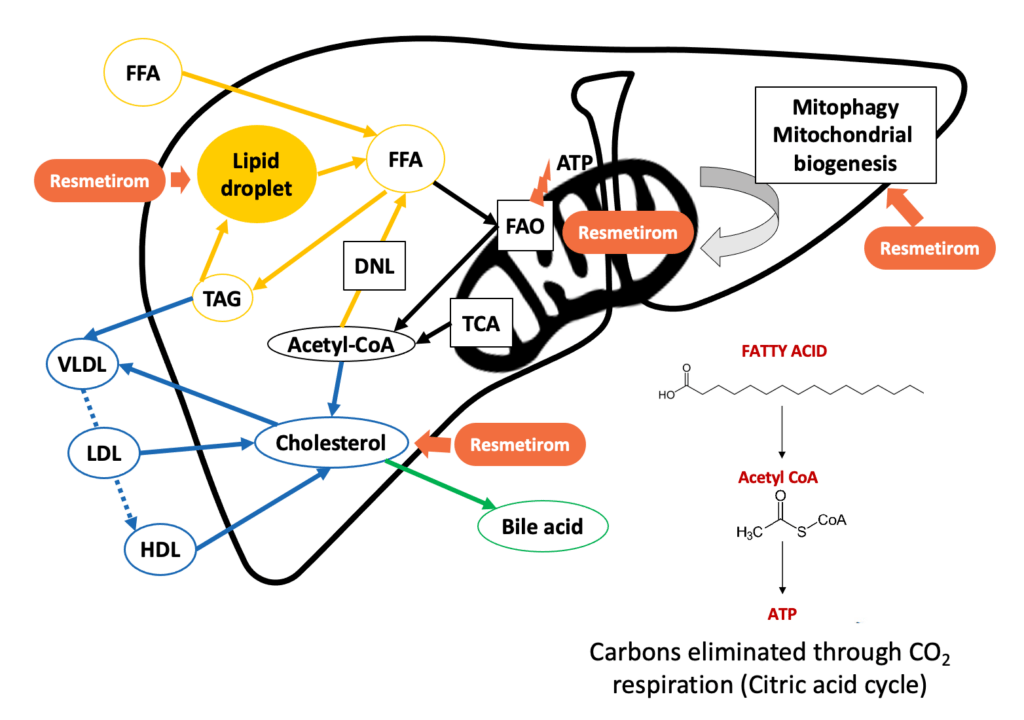

Resmetirom, Madrigal's sole clinical candidate, is an oral thyroid hormone receptor ("THR") ?-selective agonist that helps regulate mitochondrial activity such liver fat metabolism (Figure 1). This was important because a non-selective THR agonist would also activate not just the THR-? receptors found mainly in hepatocytes, but also THR-? receptors in bone and cardiac cells. The selectivity was confirmed by the similarity of serious adverse events in the study's treatment and placebo groups. Furthermore, the results have now clinically validated the concept that liver fat reduction also assists in resolving fibrosis.

Figure 1. Resmetirom's Mechanism of Action

{kind=link}

By the FDA's standards , resmetirom has the requisite supportive evidence for efficacy, so barring some miraculous disaster, such as, say, a safety signal not yet disclosed that caused discontinuation at the higher dose, approval is a foregone conclusion. By the time resmetirom's New Drug Application ("NDA") is filed, the Agency will already be well-versed in evaluating Phase 3 data due to its experience with Intercept Pharmaceuticals ( ICPT ), which resubmitted the NDA for obeticholic acid ("OCA") on the 23rd. The target review action date is in 6 months.

As discussed in my previous coverage of Intercept , OCA will also likely be granted commercial authorization, if not outright, at least after an Advisory Committee meeting; thus, OCA is expected to have first-mover advantage but would eventually share the market. However, the previous thesis was based on resmetirom being more of an anti-NASH drug, while OCA was more of an antifibrotic with a much longer safety record after being approved for another indication in 2016. Now that resmetirom resembles an ideal NASH agent with antifibrotic activity seemingly on par with OCA but with no pruritus issues or negative impact on cholesterol, the dynamic changes.

The previous Madrigal article included this passage:

The prevalence of NAFLD in the U.S. was modeled to be 26.3% in 2016 , or 85.2 million, of whom, 20% would have NASH, but only 20% of those classified as at least F3 on the fibrosis score. That makes 3.4 million the total addressable market of high-risk patients based on the population tested in NASH clinical trials. If sold at $50/pill, it would be a blockbuster if 55,000 patients are on it annually.

Fifty-five thousand represents 1.6% penetration of the NASH market. There is little point to prescribe OCA over resmetirom, and fewer reasons to believe Madrigal can't corner at least 10% share.

One of those uncertainties is who Madrigal will partner with, because the company has no sales infrastructure. They now have enough cash (more than $450 million) to finance at least another year while waiting for a partnership or buyout. Given the $80 million third quarter loss , operational expenses for the next 12 months should be >$350 million. If they decide to go it alone, their manufacturing source will need capacity to produce at minimum 600,000 30-count bottles to supply 50,000 patients. Of course, if they GIA, they don't have to share profits, and 10% penetration using the model means $6.2 billion in sales annually, and all this is just from the U.S.

Risks and Takeaways

To conclude, Madrigal isn't the typical go-to defensive healthcare stock in a bear market based on having consistent earnings, as they have no commercial products. Dealings with the FDA are never guaranteed. There may be unknown deficiencies in the NDA, or things outside Madrigal's control, such as from inspections of manufacturing facilities. The Agency could also delay the decision date by holding an AdComm first. There may even be biased committee members with hidden connections to competitors.

In the end, longs should be confident in resmetirom and the upside that will come with eventual approval in late 2023, developments regarding the launch, and the subsequent cornering of the NASH market for a significant time. Interested investors may wait to buy with better price targets if the general market declines due to economic recession and inflation worries. Swing traders could also profit from the volatility. However, they and option traders may run the risk of missing out on a potentially bigger catalyst, because it will be very difficult to time.

The median price/sales ratio for the Healthcare sector is 3.91 according to Seeking Alpha, which is similar to the 3.64 average from Zacks ' Medical-Drugs industry that includes 195 biopharmaceutical as well as specialty pharmaceutical companies. The lower P/S suggests a $22.6 billion cap; dividing this by the total of 17,103,395 common shares at Q3 end plus the 1,183,344 generated by the secondary gives over $1,200 per share, or 4.5 times the current price. Again, relying only on U.S. revenues. Someone in Big Pharma looking for value acquisitions will likely come to a conclusion that anything approaching that figure will be too high a price to pay for later.

Editor's Note : This article was submitted as part of Seeking Alpha’s Top 2023 Pick competition, which runs through December 25. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Madrigal Pharmaceuticals Setting The Standard