AMKAF - Maersk: At The Mercy Of The Cycle

2023-08-22 02:23:42 ET

Summary

- Maersk’s resilient Q2 and upward guidance revisions have given investors hope.

- But with headwinds from China only worsening in recent weeks and the supply-side overhang still a key unknown, I wouldn’t underwrite a turnaround just yet.

- Maersk stock is cheap but justified by a lack of positive catalysts and the prospect of lower for longer ROEs.

The lower volume outlook from containership major A.P. Møller - Mærsk A/S ( AMKBF ) ( AMKAF ) was a key negative coming out of an otherwise positive quarter, signaling a longer-than-expected destocking cycle from here. The pessimism was largely consistent with commentary from global freight forwarders like Kuehne + Nagel (KHNGF), discounting hopes of a prolonged recovery following consecutive weeks of Shanghai Containerized Freight Index (SCFI) rate resilience.

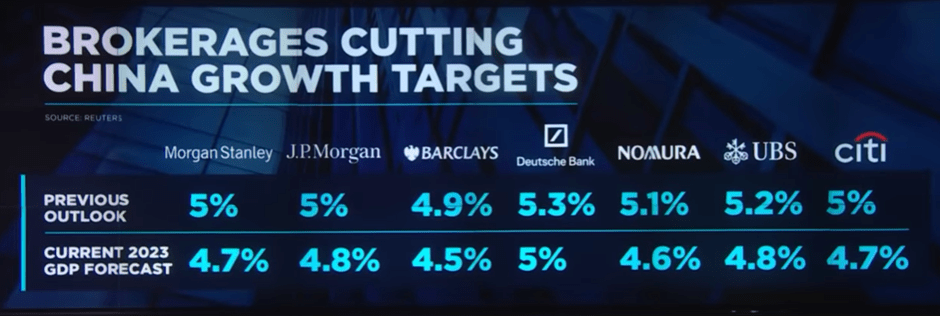

Even balanced against some compelling secular themes, including Maersk’s ambition to transition into a diversified and less cyclical integrated logistics company, the cyclical shipping headwinds are concerning. So is the prospect of an even more pronounced China slowdown (now potentially even short of its +5% GDP target), as well as the increased competitive intensity in key Maersk routes following the announced breakup of the 2M mega alliance (comprising Maersk and MSC (MSM)). Plus, it’s not clear to what extent (if at all) slow or ‘super slow’ steaming will offset the major capacity backlog set to come on stream over the coming months.

So while management raised the guidance bar this quarter, I’m not prepared to underwrite a recovery just yet. The stock rightly trades at a ~40% discount to its book value given its low-single-digit % ROE expectations through 2024/2025; net, the risk/reward seems balanced here.

P&L Deterioration Continues but at a Slower Pace

Maersk’s Q2 headline profitability was still down YoY but much better than expected. EBIT at its ocean segment (i.e., the core containership business) was one positive highlight at $1.2bn (vs. ~$2.0bn last year), though the implied ~610bps of operating margin compression QoQ underlined the challenging operating backdrop. Digging deeper, tailwinds from volume growth (up high-single-digits % sequentially) and ex-bunker unit costs (down high-single-digits % sequentially) were key positive drivers, while continued mid-teens % freight rate normalization (in line with the containerized freight index declines out of China) was the key negative drag. Freight rates (proxied by the SCFI) have since ticked higher post-Q2, but after accounting for the recent series of (potentially unsustainable) General Rate Increases and seasonality, I don’t see too many silver linings for the near-term rate path.

{kind=link}

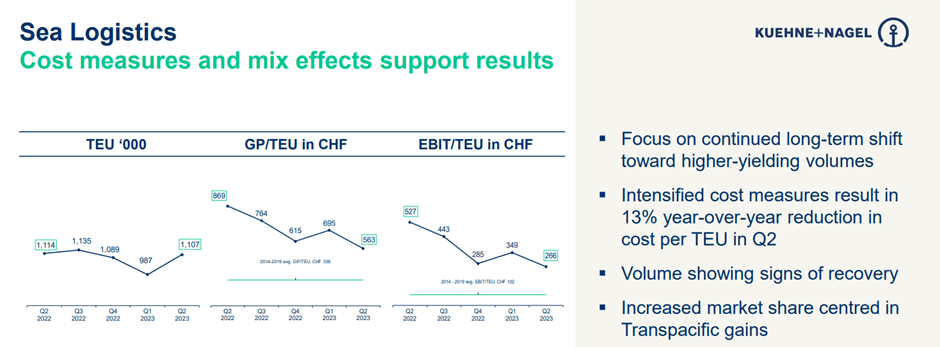

The read-through from key peer Hapag-Lloyd ( HPGLY ) isn’t great either. While bookings have rebounded YoY, the sustainability of this trend remains uncertain, particularly given management’s caveat that freight rates are only up from prior unsustainably low levels (i.e., sub-costs) in certain routes. Freight forwarder Kuehne + Nagel also posted better-than-expected operating profitability (up >90% from pre-COVID levels but still >50% down YoY), yet appears to be struggling with rate pressures in the sea logistics segment. That said, Kuehne + Nagel also pointed to encouraging signs that customers are willing to give up some margin in return for stable transportation, which bodes well for large-scale operators like Maersk. For Maersk management, leveraging its economies of scale advantage into more favorable contract terms and building out its adjacent high-value-added services side will be key to outperforming this industry downturn.

{kind=link}

Guidance Revised Higher But Emerging Risks Weigh on the Near-Term Outlook

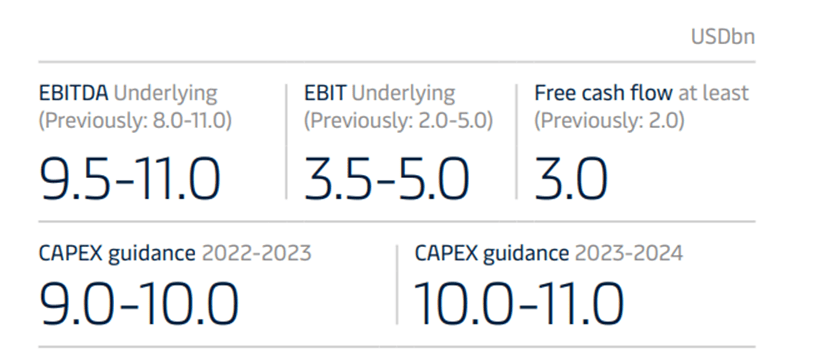

Following a more resilient quarter, management has raised full-year adj EBITDA guidance to $9.5-11bn (vs. $8-11bn prior), with adj underlying EBIT also raised at the lower end to $3.5-5bn (vs. US$2-5bn prior). While positive at first glance, this revision still implies a >70% decline YoY at the mid-point. Importantly, it also embeds reduced ocean volume assumptions, implying a more downbeat expectation for global trade going forward. This might seem conservative, but given the similarly bearish sentiment echoed by freight forwarders like K+N, an extended destocking cycle seems more like a base case, in my view.

{kind=link}

Plus, this guidance was set before the recent slew of China downgrades (now moving below the +5% growth target) and heightened property sector contagion risks following Evergrande’s ( EGRNF ) bankruptcy filing . The knock-on impact of a China slowdown for commodity imports is also worth considering, posing incremental downside risks to a containership volume recovery. In line with these developments and the prospect for freight rate underperformance as we end Q3, I don’t think Maersk is quite out of the woods yet.

{kind=link}

Beyond the macro, there are also industry-specific risks, particularly from the supply side. Maersk management isn’t sure how much overhang there’s going to be themselves, though the lowered capex outlook (lower end of $9.0-10.0bn for 2022-23 and $10.0-11.0bn for 2023-24) indicates they’re adding buffer against more freight rate pressure ahead. FCF has also been raised to >$3bn (up from >$2bn prior), which potentially leaves room for downward revisions depending on the freight rate path from here. Over the mid-term, the key positive is that Maersk still generates enough cash to make good on its capital return promises (up to 30% of its current market cap). Should a prolonged industry downturn materialize, however, it’s not entirely clear how management will balance its dividend/buyback commitment with its planned transition into a less cyclical integrated logistics company.

{kind=link}

At the Mercy of the Cycle

Maersk stock has risen on the back of a positive Q2 (relative to a very low bar), though the downbeat volume outlook should warrant more caution, in my view. Yes, management is being conservative with its expectations, but perhaps not that conservative, given global freight forwarders have cited similar views on a prolonged destocking cycle post-Q3. So while the Maersk story has its positives, including a long-term plan to de-risk its income stream and a massive capital return plan through 2025 (up to 30% of its current market cap), it’s hard to look past the cyclical negatives. Adding to peak cycle concerns are the supply-side headwinds, which are unlikely to be mitigated by any amount of slow steaming.

And over the mid to long-term, Maersk could see its rates pressured substantially as the 2M mega alliance breakup runs its course. The stock might seem cheap at the current ~0.6x P/B, but with Maersk poised to sustain ROEs well below its cost of capital for a few years, I won’t be rushing to buy anytime soon.

For further details see:

Maersk: At The Mercy Of The Cycle