SBLK - Maersk Doesn't Need A Soft Landing To Be A Great Investment

2023-09-19 16:02:17 ET

Summary

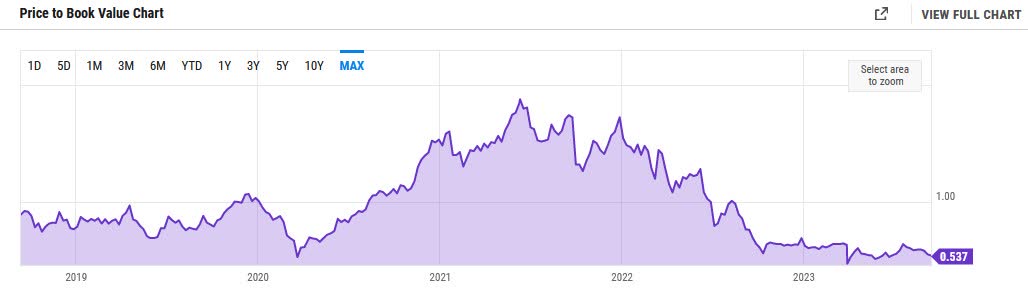

- Maersk is currently trading at nearly half of book value, representing a margin of safety for value investors.

- The company has a robust cash position, with low debt-to-equity and strong potential for outsized returns from stock buybacks in future years.

- Dividend yield is uncertain for the next 1-2 years, but will likely help to offset some of the near-term downside which stems from cyclicality.

- Overall, Maersk seems like a relatively safe way to make a macro bet on the economy, with or without a soft landing contributing to returns.

Investment Thesis

A.P. Møller – Mærsk A/S, ( AMKBY ) or more commonly known as just Maersk, is one of the largest container shipping companies in the world and has its hand in nearly 1/6 of global trade with a market share close to 17%. The stock is depressed currently due to cyclical factors as well as other issues, and now trades at a cheap valuation at nearly half of book value. Reversion to the mean of around 1x book value would indicate significant upside for the stock, however, potential returns also stem from sizeable dividends and stock buybacks over the next several years. This combination of factors could end up being the real reason for investing in Maersk in my view, as I believe the longer-term buyback potential is being underestimated by the market. Future dividend yield is a little uncertain, but it is likely to be significant for returns going forward. An economic soft landing would certainly change the valuation and narrative surrounding Maersk stock, but this is not entirely necessary for a favorable outcome in the long run for shareholders.

Introduction - Michael Burry Enters Shipping

One thing that catches my attention every now and then is Michael Burry's portfolio , and his adoption of bulk shipping companies from time to time.

No, Michael Burry did not buy Maersk, but this past quarter, he did start small positions in several shipping companies - Safe Bulkers ( SB ), Euronav ( EURN ), Costamare ( CMRE ) and Star Bulk Carriers ( SBLK ). This basket of shipping companies reminds me a lot of his old trade in Golden Ocean ( GOGL ) from a couple of years ago, which was highly successful. After I decided to start a recent position in Maersk, I noticed the 13-F filings were starting to come out, so I took a look at Burry's recent changes to his portfolio. I noticed he was also buying shipping companies during the quarter, which was a welcome surprise, but also most likely just a random coincidence of market timing.

Burry's trading style is a bit hard to follow because usually his holdings turn over every quarter or two, and he trades at a fast pace which can be hard to draw any conclusions from. Earlier this year, he bought a bunch of US bank stocks and was out of them by the very next quarter. Michael Burry is not a Warren Buffett, "buy-and-hold" forever type of investor, but what can value investors learn from his portfolio? What can be useful to investors from watching Burry's portfolio over time is learning patterns and seeing when he enters into a trade and what industries he chooses to focus on, and come back to time and time again. Could it be the right time to buy into the shipping cycle now? Or is Burry simply making a macro bet on a soft landing with a basket of shipping companies?

Just recently, on September 18th, 2023, J .P. Morgan upgraded Zim Integrated Shipping ( ZIM ) citing margin declines as temporary, with a rebound being likely as COVID-era charters get re-chartered or redelivered at cheaper rates. If an economic soft landing is perhaps in the cards after all, shipping stocks such as Maersk are sure not trading like it.

Whatever the case may be, I see Maersk as somewhat the opposite of what Michael Burry would typically buy in the industry. The market capitalization and sheer size of the company is not like him at all; Burry typically trades small caps or even borderline micro-cap shipping companies with a short time horizon, but I intend to do the opposite. My goal is to not trade the stock in the short term, but hold Maersk for much longer, reinvesting the dividends along the way.

I like Maersk simply because it is a massive company in its industry with a competitive advantage, trading at a large discount to book value, with potential for outsized returns from stock buybacks over time. It is unusual to find a company with such a huge market presence that trades at nearly half of book value (even if this is the shipping industry we are talking about here). The potential returns from just buybacks in future years are significant, but combined with dividend reinvestment over time, I think the stock could be a worthy compounder.

In this article, I will outline the basic thesis for investing in Maersk stock, and explain why buying at nearly half of book value makes sense given the buyback strategy.

The Valuation Is Incredibly Low

Maersk trades at roughly 0.5x book value and also at historically low levels when isolating for this variable, even slightly below the COVID crash levels of March 2020.

{kind=link}

Most of the valuation metrics seem very low, but the recent P/E ratio of the stock is somewhat misleading, due to cyclical reasons and the recent years of earnings being abnormally good for the company. I would not go from just the recent earnings of the prior two years, but use other variables to determine if the stock really is as cheap as it currently appears to be.

A P/E multiple for 2023 is estimated to be around 7x, which seems more in-line with a fair valuation, but earnings could be better than expected next year, even if a soft landing for the economy is not in the cards. The most recent earnings call shed light on this, as management stated that while a slowdown is still weighing on the industry, earnings guidance would be better than expected for the full year. Sort of contradictory statements, but better earnings for the full year would translate to possibly better dividends than expected as well. Recent declining financial results since 2022 and a big crash earlier this year have both pushed the stock from near record highs back to test a support level (near $8.00 for the ADR, which trades as AMKBY). I like the stock here around this price, as the discount to book value should not be viewed as a weakness, but rather as a support level and buying opportunity for those with a longer-term mindset.

{kind=link}

For me, Maersk seems like a relatively safe way to make a macro bet on the economy and collect dividends along the way. When I look at companies like this, I always try to screen for low valuations, a competitive advantage, nice margin of safety, and if possible, potential for reinvestment of dividends each year. Shipping companies can be tricky because they are cyclical, with highly variable earnings and dividends which are usually not consistent. This makes valuing the company difficult based off of EPS alone.

Maersk paid a whopping dividend in March, which will likely not stay high again next year. Even with a big drop in the dividend yield being priced-in, the recent action in the stock does not worry me. I would rather see management prioritize stock buybacks over dividends anyway at this time, as the discount to book means that more value likely can be created from these buybacks over the next few years, rather than paid out as dividends to shareholders.

The future dividend yield is somewhat uncertain, but nevertheless, it helps in terms of offsetting the downside that may be apparent in the next 6 months. Could the stock get even cheaper and trade for under 0.5x book given a hard landing for the economy? Yes, I believe that anything is possible, but this could be a necessary outcome to create future value from buybacks at rock bottom prices before the cycle inevitably turns positive once more.

Making macro bets directly via complicated strategies and hedging is not my style as an investor. However, investing in Maersk seems like a good way to have some protection against the downside while making a largely macro bet on the economy.

Excellent Balance Sheet

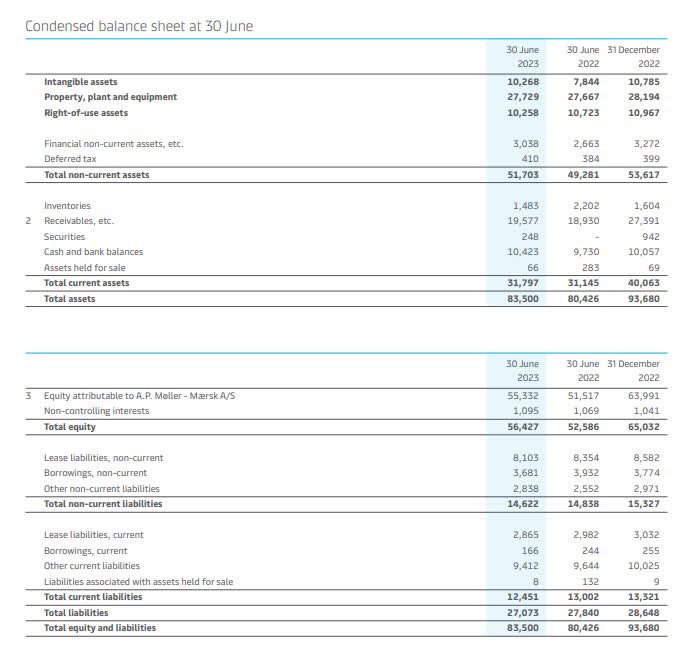

The thing that stood out to me right away in my research into the company was how surprisingly good the balance sheet was. Maersk does not have too much debt, and the company has tons of cash which can be used to buy back stock at discounted prices to book value.

This alone will create value for shareholders over time in my opinion, but there is some risk that management may prioritize dividends over buybacks in the next couple years, make acquisitions, or change the capital allocation strategy in some other way which could hinder performance.

{kind=link}

Shown above is the company's balance sheet from the most recent quarter . Maersk has over $10 billion in cash and around $14 billion in total non-current liabilities. Compare the debt with the total equity, at $56 billion, and the debt-to-equity ratio is close to 0.25.

Comparing the cash position to the market cap, at around $29 billion, and it becomes clear just how much buyback potential there is over the next several years. Buybacks have already been aggressive, and management seems committed to this strategy as the stock price has declined in recent months.

Where Could The Return Come From?

When considering certain stocks like Maersk as an investment, one should ask themselves, how am I going to get to my desired return? For some stocks, it is clear that growth in some capacity is going to be a main factor, while in other stocks, a lot of the return comes from dividends. What if the company is not growing at all? Are multiples expanding or contracting? In many cases, returns will come from four things - dividends, multiple expansion, earnings growth, and stock buybacks. Reversion to the mean is always something that must be considered, especially with cyclical companies like Maersk. Timing the cycles can be difficult, and so a longer-term approach is necessary to produce favorable results. Trading these stocks in the short term is possible, but it is risky and does not always guarantee that dividends will contribute to the return.

One possible place the return could come from would be simply from a reversion to the mean in terms of book value. In my opinion, it is somewhat more likely that Maersk could become loved by the market once more in the next cycle and trade closer to 1x book value, rather than the stock getting punished even further to trade in a range near 0.25x book value from 0.5x book value. A risk is that given a bad enough recession, today's prices could be too high compared to future earnings potential.

Another place the return could come from would be the combination of two factors - one being dividends reinvested over each year of the holding period, and management's commitment to stock repurchases going even higher over the next several years. The results of the buyback program are already exceptional, as the number of shares outstanding has decreased from 21 million as of 2019 to almost 17 million as of this year. Aggressive buybacks are one thing, but buying back stock at major discounts to book value is an overlooked mechanism that could supercharge future returns. Dividends will likely not be very large next year, but reinvesting the dividends at opportune moments in future years will be important to the longer-term strategy of holding the stock through various parts of the cycle.

The last place the return could come from could be the most overlooked of them all - actual unexpected economic growth in future years and Maersk being re-rated with a higher multiple compared to similar players in the industry. The company has an excellent balance sheet, so it would not be a shock to see the stock trade at a premium to book value at some point in the future when the cycle inevitably reverts.

Further Risks - The Nature Of The Cycle

Shipping companies are widely known for their cyclicality. In good times, the earnings and dividends will be astronomical, but in bad times, shipping rates decline and the company struggles to make any profits at all. Similar to the semiconductor cycle, the market goes through ups and downs as conditions with pricing change. One year, a certain company in a cyclical industry has high margins and earns record profits; the next year, the margins are terrible and the company barely makes any money at all. This can be a problem for many shipping companies that use excessive leverage to build their fleets, as the downturns can be worse than expected, causing financial difficulty and instability. In my opinion, Maersk does not use excessive leverage, but this is still a risk which should be considered before making an investment in the company.

It is also important for investors to realize that Maersk's earnings potential and dividends in a given year are closely tied to shipping rates, which are highly volatile. In terms of recent years, the post-pandemic environment caused demand to skyrocket, and many bulk shipping companies looked dirt cheap compared to what they were trading for in the middle of 2020. Now that this post-pandemic rush has subsided, for the most part, supply and demand are beginning to look more balanced. Investing in shipping companies is notoriously tricky, as timing the cycles becomes more important than other aspects of the business itself, and being on the right side of the cycle is easier said than done.

Conclusion

A.P. Møller – Mærsk A/S, or simply just Maersk, is a relatively safe way to make a macro bet on global trade, with a further advantage given due to a margin of safety with shares trading at nearly half of book value. This relative safety stems from managing downside risk with high dividends and the potential for future returns stemming from sizeable stock buybacks over time. The company has an excellent balance sheet, and a commanding market position with a market share of around 17%, giving a competitive advantage in the shipping industry. The valuation is extremely favorable, with a low P/E multiple and shares at nearly 0.5x book value, which makes management's buyback strategy even more enticing for longer-term investors. A soft landing for the economy would be an amazing outcome, but this is not entirely necessary for Maersk stock to produce favorable returns in future years. I currently view shares of Maersk as a Buy at this time, and will be watching the stock closely for continued buying opportunities in the $8.00-$9.00 range for the ADR.

For further details see:

Maersk Doesn't Need A Soft Landing To Be A Great Investment