AMKBY - Maersk Q3: A Long-Term Winner With A Short-Term Downward Potential

2023-11-30 13:15:20 ET

Summary

- Maersk reported 3Q23 results with group revenue of $12.1B and an EBIT margin of 4.4%.

- The company is taking efficiency and restructuring measures, including reducing the workforce by 7,000 people.

- Maersk expects lower-end realized underlying EBITDA for the year and is considering options to preserve cash.

Dear readers/followers,

There has been discussion about Maersk ( AMKBY ) and its future prospects. I've been following the company with articles for going on two years now, initially being neutral but later going to a positive stance that I have maintained going on a few months now. This is an updated article for Maersk, with my latest article for the ticker being published in mid-August , a few months back, with a Buy rating. Since that time, the company has declined but has also reported 3Q23 results.

Valuation for the company during the past 10 months has not been in a favorable trend - then again, the same is true for many companies I cover. The entire market has not been in a positive trend for much of that time, and I don't believe the market challenges in the near term are in any way done.

In this company, I'll include 3Q23 results and see what we can expect from Maersk going forward.

Maersk - After 3Q23, there's still optimism for the long-term

The 3Q23 quarter wasn't necessarily a bad one as such. The company reported group revenue of $12.1B with an EBIT margin of 4.4%. Despite a solid recovery in company shipping volumes, the overall impact of lower freight rates resulted in an overall negative view for the quarter, and more negative trends are to be expected going forward.

There's an overall volatile environment in shipping, which I have highlighted not only when writing about Maersk, but also about other companies in the shipping sector, such as Hapag-Lloyd ( HPGLY ). As of this quarter, the company does maintain overall operating guidance and financial expectations but also expects the results to come towards the lower end of the previously communicated EBIT and EBITDA ranges.

To combat these effects, the company is taking efficiency and restructuring measures.

- Maersk is reducing the workforce by 7,000 people, with a long-term target of reducing it by even more than 100,000 people.

- The company now expects savings of over/around $600M for 2024.

- Restructuring costs meanwhile are expected to run at around $350M.

The obvious focus for the company is a continued high target of cost measures and efficient asset utilization. Given the current market environment and market expectations, Maersk is also lowering its CapEx targets and considering options to preserve cash, including the potential of halting the buyback program for the company's shares despite an overall relatively low share price here.

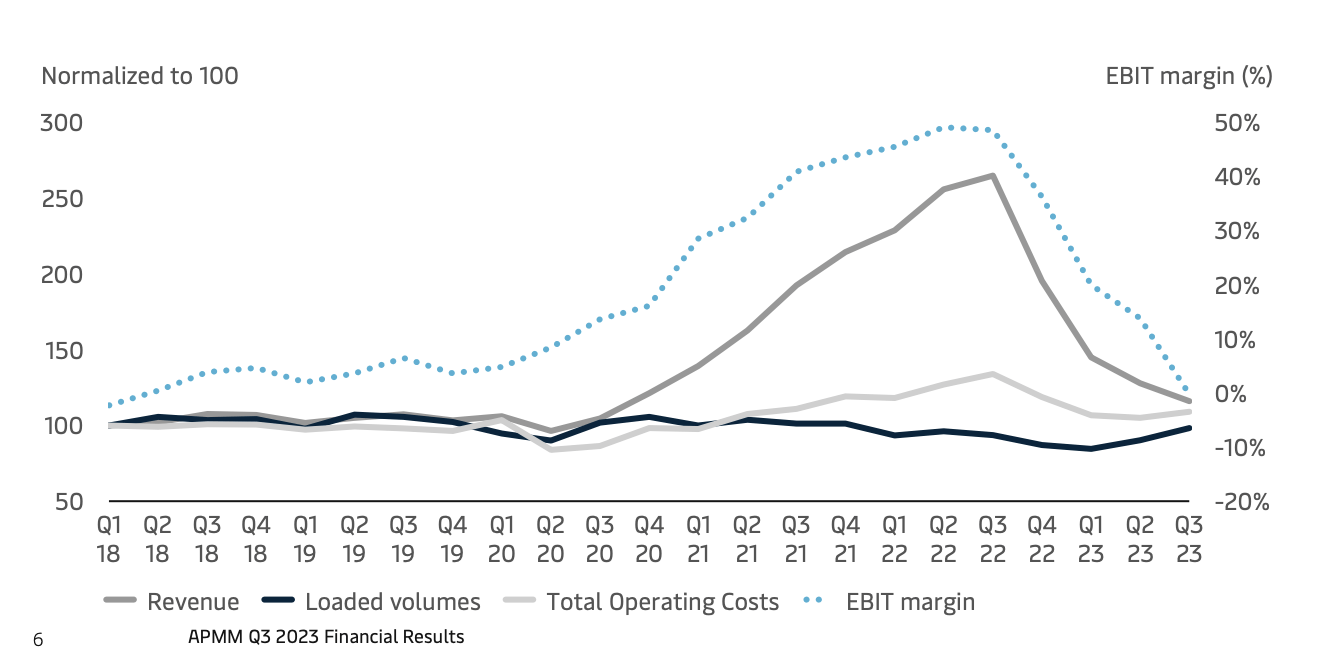

To look at the company's results on a more granular level, the volumes in the Ocean segment were the positive result and trend here. We have supply-side advantages and positives, but severe impacts on the negative side, with rates now at a break-even level. We also have high levels of additional supply coming online in 4Q and next year's idling and scrapping numbers which normally weigh up new supply, being at low levels.

In essence, we've almost come "full circle" here.

{kind=link}

In the logistics & services segment, meanwhile, we're seeing good volume recovery despite lower rates, with air and landside transportation being chief among the negatives here. E-commerce verticals remain very challenged at this time, especially in core areas like NA - but overall increased cost management has led to a segment-wide EBIT margin stabilization, and Maersk is expecting progressive margin recovery in the Logistics and service segment. Its only negative is that the segment is comparatively smaller than Ocean.

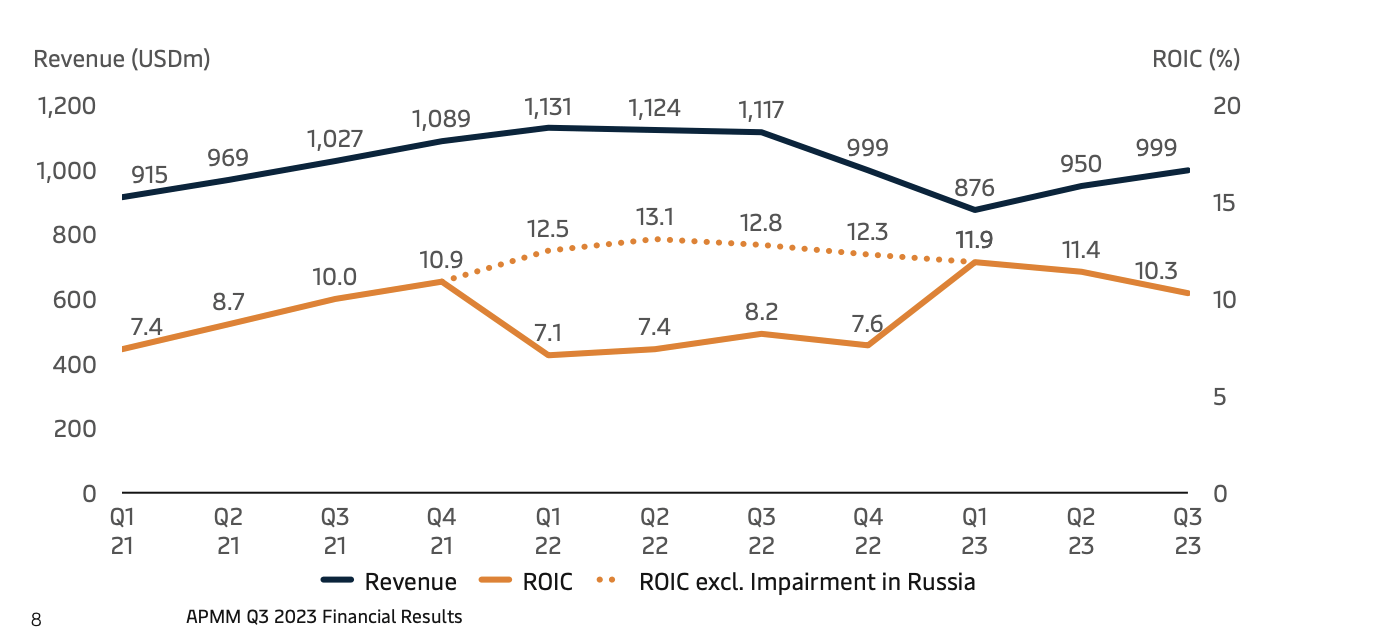

We also have the company's budding Terminals quarter, part of what the company and similar businesses have been focusing on to improve its mix. The company reports good margins and attractive returns, improvements since the trough seen in 1Q23, even with volumes in a negative trend - which given the current inflationary and macro environment is very impressive.

{kind=link}

Again, the negative here is that the segment isn't that big a portion of the company's overall revenues. The overall expected downturn in the ocean segment calls for a continued focus on transformation for the company - and this is currently ongoing.

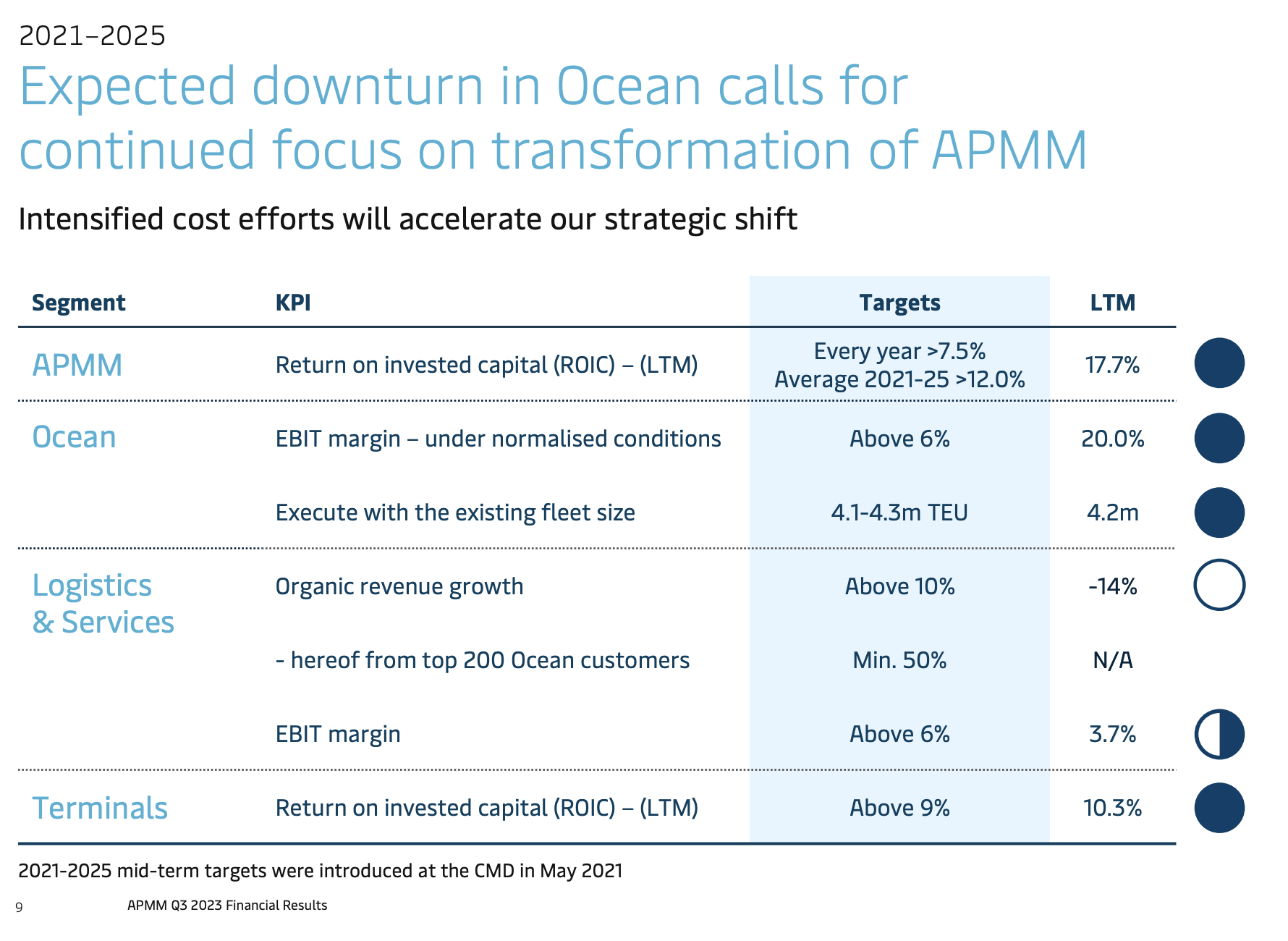

Here is how the company is currently meeting its stated overall targets.

{kind=link}

The company's near-term future and financials are tricky - not because they are complex as such, but because they include a potential range of quite negative results at this time. We're seeing the potential for negative global container volume growth, though the assumption of negativity here is abating.

The company currently maintains its financial outlook for the year, but expects a lower-end realized underlying EBITDA, below the double digits in billions in the range, coming in at around $9.5B. CapEx meanwhile is expected at $8B, and restructuring costs are raised to now be closer to $350M compared to $150M previously, with the majority recognized not next year, but this year. This is part of the reason why the results are going to be lower, and I believe, why things are down in general.

The problem for shipping companies in general continues to be the overall erosion of the shipping rates across the entirety of the industry. Volumes can only do so much to make up for this, and in this case, it's not enough. Results during the quarter were impacted to the degree that Free cash flow actually went negative , to around $100M on the negative side due to that lower profitability.

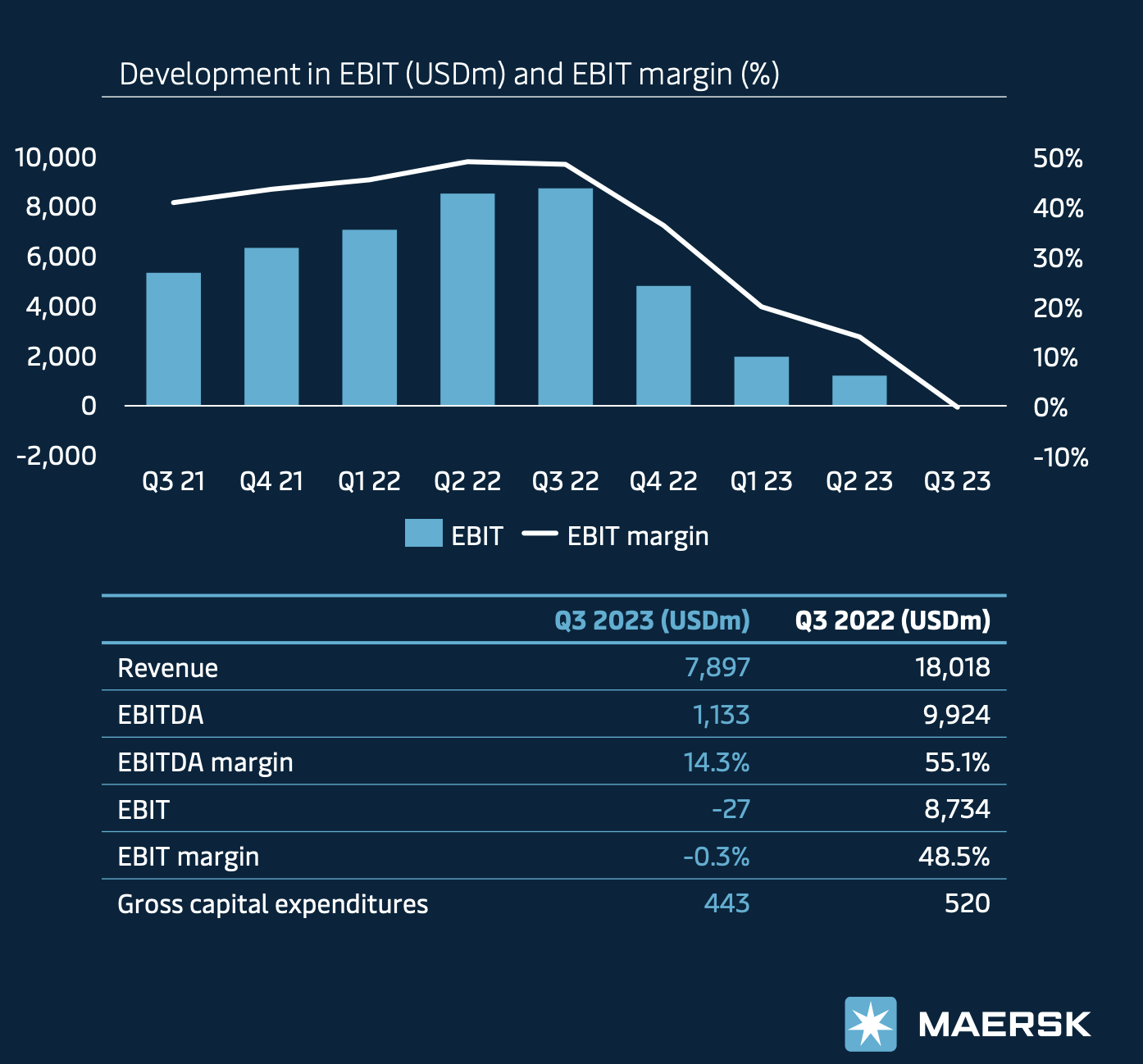

Still, on the housekeeping and fundamental side, Maersk remains very attractive, with almost $22B in cash and deposits and an overall net cash of $6.8B at the end of 3Q. So a small quarter of negatives isn't even close to enough to impact the company from a wide sort of perspective here. The issue with FCF was lower cash conversion from the operational side, now at 74%. We can illustrate the sheer drop in the ocean segment by looking at this graphic.

{kind=link}

Risks & Upside

The risk to Maersk is obviously that the erosion of freight rates continues at or even above the level we're seeing here. Given the new supply coming online this and next year coupled with lower-than-usual scrapping trends, this is something an investor could expect. At the same time, there is a "bottom" for these trends, and historical levels are a fairly good proxy for an expectation here. The freight rate effect, meaning the bridge impact on freight rates for 3Q was a massive $9.4B, unable to be weighted up by bunker prices, handling cost increase, efficiencies, and volume effects. With the other two segments either too small or also in a negative trend, the primary short-to medium-term risk both to the company and share price is this, which could result in short-term negative developments.

The upside meanwhile dictates that when we reach a bottom in freight rates and when scrapping and volume trends turn around, so will Maersk's trends and results. With as much cash as the company has on hand and on its books, Maersk is not in any danger of any sort of fundamental decline, as I see it. This means that once things turn around, there is a valuation-related upside to the company, and that's why investors who are bullish would be interested in this.

Valuation

The estimates for Maersk have worsened over the past few months. What was once a low expectation for the company's 2024E result has gone into negative estimates from FactSet analysts, now expecting adjusted negative EPS of 441 DKK for the native share for the 2024E fiscal. Of course, this is then expected to reverse in 2025E with a 200%+ increase in adjusted EPS.

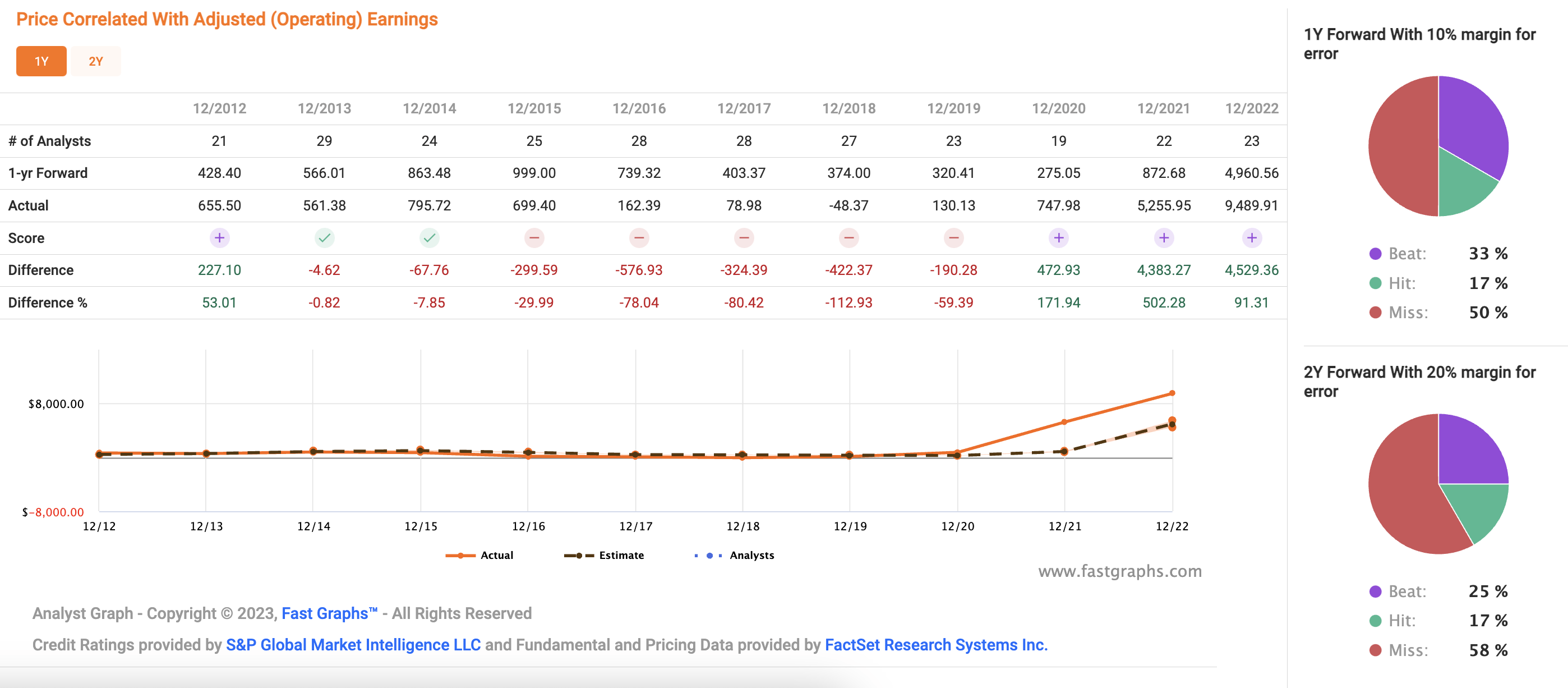

The lack of forecast accuracy here is something to be aware of.

Maersk forecast Accuracy (F.A.S.T Graphs)

{kind=link}

In order for a Maersk investment to be successful, it should be viewed as a long-term play. I believe that for the shorter term, Maersk is unlikely to move significantly upward, and because of that, I'm also impairing my share price target here, now expecting a 13,500 DKK PT compared to the company's current 10,700 DKK/share native price. It still makes the company a "BUY" but comparing the company to other investments available on the market today, it's a stretch to say that this is one of the first investments one should consider in today's macro. The company has very good fundamentals, including a BBB+ rating, good leverage, and a theoretically strong eventual upside in the case of normalization, though it may indeed take a few years to get there.

My own position in Maersk is mixed. I bought some cheap, some at more expensive levels. Some of my negative expectations for the Ocean segment have actually materialized. In my previous article, I guided you to be on the lookout for this, and this is also the reason for the overall lowering of my target here. I also still maintain that the fourth quarter for the company is likely to be weak. The company is still doing a good job at containing overall costs, but unfortunately, the way the market and the sector look, I don't expect a quick recovery here.

I would put a recovery to the 15-17,000 DKK level perhaps in 2025E or thereabout, which for many investors may be a long time to wait.

Overall, this means that I'm taking a more conservative stance on Maersk, without for that reason changing my stance in terms of "BUY" or "HOLD" - I'm still at a "BUY" here, it's just that the buy now is with a more conservative PT, and my new expectation for recovery is farther away in the future.

The company cannot rightly, based on the expected normalization, be called "cheap" any longer. But cheap has never been a deal breaker for me with this business. I just want a good valuation - and we still have that here.

I update my thesis on Maersk after 3Q with the following.

Thesis

- This is one of the world's most important shipping companies. At a good valuation, this company is, to me, a no-nonsense "BUY" with no looking back. The flow of goods dictates the state of our national economies, which makes the company a major player in macro.

- I view the company currently as fairly or even slightly undervalued in the face of what is an unprecedented logistic crisis.

- It's a "BUY" here to me - and I view it with a target of 13,500 DKK/share updated for late November of 2023.

- I recently bought more in the company.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them:

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company, therefore, fulfills all of my investment criteria here except it no longer really being "cheap" here.

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Maersk Q3: A Long-Term Winner With A Short-Term Downward Potential