AMKAF - Maersk: Still A 'Buy' Even After Double-Digit Market-Beating Returns

2023-03-17 12:10:32 ET

Summary

- I've been reviewing Maersk pretty much on a 2-3 month basis since fall of 2022, due to the company's attractiveness as an overall investment (As I see it).

- Maersk is a global-leading shipping company - and with the ongoing political and supply chain situation, this becomes more and more important.

- Despite the volatility in the market, Maesrsk has been holding its own, and for the time being, I believe that the company can be bought at a good valuation.

- Maersk remains a "BUY" for me - and here is why.

Dear readers/followers,

You should never underestimate A.P. Møller - Mærsk A/S ( OTCPK:AMKAF ). Those that do, might end up underperforming the market. I believe those who, like myself, err on the side of the potential upside during cheapness, can see some outperformance - like this recent case:

Maersk Article (Seeking Alpha)

I've been very slowly expanding my Maersk position because the share price for the company on a native basis is fairly massive - over 10,000 DKK per share or $1,000+ per share. Also, and this is a crucial point that I want to reiterate, Shipping and logistics are far from the easiest sort of segment to cover with only limited time - but I believe it's one of the more crucial sectors to actually stay invested in and to invest in when we're in a downturn for the long term.

Because Ocean Freight, and freight overall, obviously isn't going anywhere.

Let's review Maersk for 2023, and what we can expect from the company in this volatile situation over the coming 12 months.

Maersk for 2023 - An upside is still there

So, Maersk. Last time I wrote about the company we had 2Q22 and 3Q22, and we were going heavily into forecasting for the full year and the coming 2023 fiscal and what could drive the company.

Now, chaos and global ups and downs are oftentimes an advantage to shipping. Over the past few years, we've seen shipping prices pretty much spiral completely out of control - a development I myself find interesting and welcoming, both for what it does to the company and also what it does to the market as a whole. Before this development, prices for an LCL or a Reefer were so low as not really to make sense long-term.

Well, that situation's changed. In my last article, Maersk confirmed the FY22 outlook, and this is despite the global deterioration of macro and the overall outlook (a recession in this case).

I'm a believer that we are headed for a recession. There is nothing we can do to stop it, and large parts of Scandinavia, with a particular focus on Sweden, are definitely going into a recession in the near term future in my view - perhaps as early as 2023, but I would say definitely in 2024. The combination of a mortgage market with people leveraged to the gills on the basis of mostly-floating or short-term fixed rates that are expiring this year will likely cause a domino effect, and what remains to be seen is how bad it's going to be. Europe and the global economy in the larger sense though, I believe will do better.

We have 4Q22 results and FY results from Maersk as I am writing this article. And those results mostly confirm the positive thesis I gave in my last article - also part of the reason for the positive performance we've seen.

In fact, things are even better than expected.

Full-year revenue is over $80B, with an EBITDA of $36.8B, and despite ongoing normalization of the Ocean segment, all segments saw good contributions to the record EBITDA. This also led Maersk to declare a 4,300 DKK dividend for the year.

That's a yield of 27%.

Together with ongoing company buybacks, this implies a shareholder return of no less than $14B for 2023.

The company sees trend changes going on in the shipping industry - and Maersk is at the forefront of being able to deliver those.

What trends do I mean, and does the company refer to?

Resilience in Supply Chains. While price is obviously a factor, the ongoing situation means that participants and customers can't really be choosy about pricing. Instead, they're demanding that the owners and facilitators of the supply chains deliver predictability and quality above all, in a chaotic world.

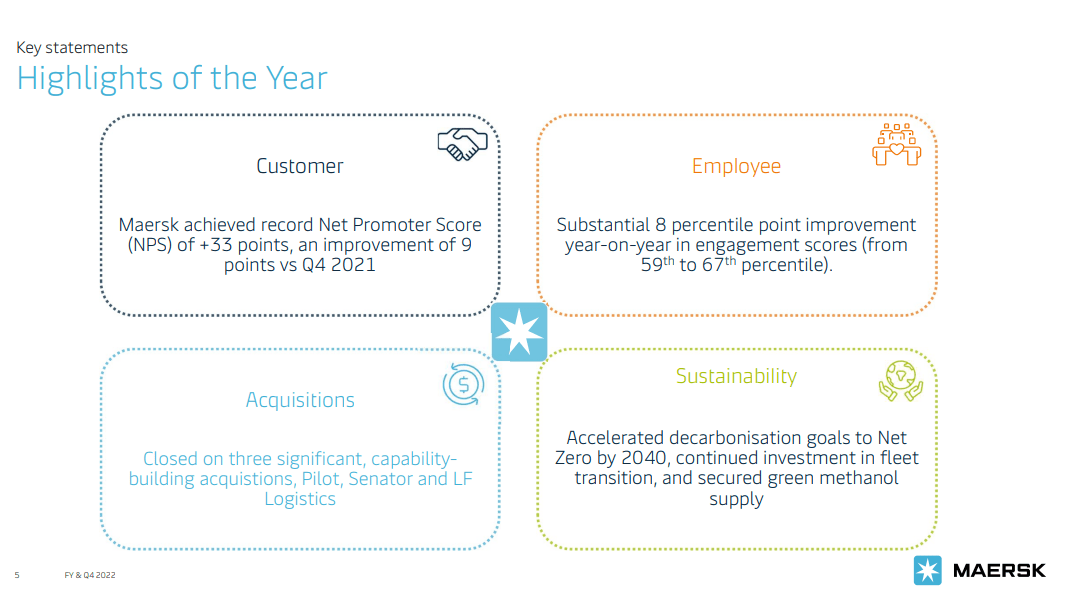

It was a great year for Maersk, both in terms of soft and hard targets.

{kind=link}

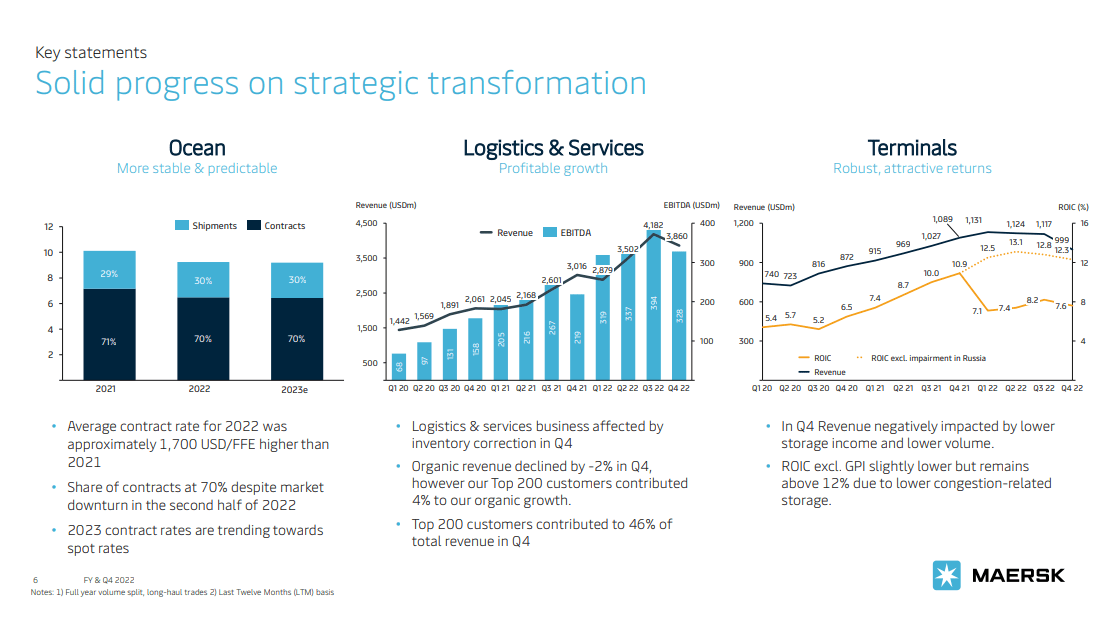

Maersk is in the midst of a strategic transformation in its shipping, logistics, and terminals businesses. All of these transformations are currently going according to plan, for the most part. The company's share of contracts in Ocean has been far more stable than initially expected, more in accordance with my own expectations for how well market volume and market share is going to be holding up.

{kind=link}

For the first time perhaps there's also a positive in the fact that there have been lower shipped volumes than before because it enabled Maersk to focus on releasing and working the global port congestion, which now is dropping not only in the UK, US, and US East coast but is starting to abate somewhat in China as well. European imports are up, but NA imports remain down.

The company's roadmap until 2025E is being delivered on, with a 12% target for ROIC (60.4% in 2022), above 6% EBIT (45.3% in 2022), and over 10% organic revenue growth in Logistics and service growth (21% in 2022). The company is working with the expected normalization in Ocean and the APMM segment while focusing on driving the terminals and service businesses up, both of which have room to grow relatively substantially going forward. The target for Terminals, for instance, is a 9% ROIC - that's currently at 7.6%.

So these quarterly trends going into 2023 is what we want to be looking at.

The company has given us up-to-date guidance for the 2023 period. This includes:

- Negative container market growth, possibly as much as -2.5%, and on the bullish side up 0.5%, due to significantly muted GDP growth on a global basis.

- Underlying EBITDA of around $11B on the high end and $8B on the low end, with FCF of at least $2B for the year.

- $9-$10B worth of Capex During the year, with investments in decarbonization, strategy, technology, and other things.

- A small restructuring charge of $450M in 1Q22.

Here are some basic assumptions and expectations for the various segments for the coming year as well, that I will be keeping a close eye on.

Maersk IR (Maersk IR)

The highlights from this year are nothing to be underplayed. The company delivered record results in basically every segment and across every single metric. We're talking 53% EBITDA growth, 32% revenue Growth, 56.9% EBIT growth, and almost 65% growth in FCF, with a 63% net profit growth. All of this was possible due to a massively impacted shipping market. It's a performance that is very unlikely to see repetition in any way here.

Maersk is "flush" with cash, increasing its net cash position to $12.6B, and posted a cash conversion of 125%.

Combining acceleration in the company's transformational strategy, as well as retaining a top-graded balance sheet and credit rating when looking at the broader industry, Maersk is the sort of business I'd say you want to be investing in at a good price.

And you know, today is a good price for Maersk.

Maersk Valuation - Why the company is appealing here

As I mentioned starting out, not all contributors or analysts following the company have a positive view of Maersk at this time. Me, I have a position that's firmly in the green here, and I'm very clear on why despite a double-digit RoR since my last piece, I'm also still at a "BUY" here.

Is Maersk "cheap"?

I wouldn't say that's the case.

But we can't expect this company to turn dirt-cheap during a time when costs for reefers and containers are still closer to very high than very low. Taking current data and trends into account, our estimates are for the normalization of company sales as freight costs normalize somewhat. This now brings us to an implied EV of between 18,200 DKK and 19,000 DKK, or thereabouts, for the DCF valuation.

I've mentioned the cadence of the company's income before - it's a complex part of the thesis here. Maersk currently trades at a native share price of 16,000 DKK. My own cost basis is around 14,900 DKK overall, which means I'm in the green here, but I'm also seeing the potential for a decline when things normalize somewhat.

15 analysts follow Maersk. Based on those analysts, we find PT ranges starting at around 14,000 and going all the way up to 40,000. It's completely insane and reflects the current state of shipping. The average PT for the analysts here comes to around 24,500 DKK, which by the way I consider too high.

The analysts are split between 6 at "BUY", 5 at "HOLD" and 4 at "Underperform" or "SELL". It's one of the most split analyst groups I've ever followed on a stock, with an upside of around 9% to today's share price.

The important thing to understand is how much of an outlier the results were that we saw not only in 2021 but in 2022. Because they have never really been at this point, nor are they likely to get there again as we move forward. Maersk is, aside from the situation we've seen here, usually a pretty "boring" company, all things considered.

{kind=link}

So, as you can see, we're unlikely to see a repeat of these years. My own forecasts lie somewhere in the ranges of what S&P Global analysts are seeing here, given that it's a fairly accurate range of forecasts, going by where the company has been from a historical context. A very similar forecast case to my previous one is still the one relevant here - no surprise given that there isn't that much that has changed over the past few months.

We still know that earnings for the 2023 period are going to be significantly lower than they were in 2022. Some are forecasting a 2023E earnings decline of over 80%, along with a massive, 60%+ cut in the dividend, given that no earnings range that the company itself seems to expect can support a dividend of 4,500 DKK per year - so such a forecast makes complete sense.

On a normalized forecast, this company still comes to a 10-15% annual upside, but there's also the realistic case for a downside movement as well. Maersk, during bad times, has been as cheap as 6,000 DKK, and that's less than half the current share price. I don't see that we'll easily reach these levels again, but it's not unlikely that the company may, when things normalize, go down below 13-14,000 DKK for the native share price. Of course, I don't believe that quality shipping as a whole will see a massive sort of decline at this time given global macro trends.

As I've said before, Peers for the company do exist - we actually have plenty of them. We have companies like Hapag-Lloyd ( OTCPK:HPGLY ), Kuehne + Nagel ( OTCPK:KHNGF ), Cosco, Nippon Yusen ( OTCPK:NPNYY ), and various other global transport and logistics companies. Yet few of these, or none, are even close to as large or as relevant as Maersk is. The valuations here are still very mixed, and Maersk remains relatively cheap on a peer valuation model as well.

My last PT for the company was 21,000 DKK. Usually, I'd stick to that given the company's improvements in terms of performance. However, because I see some more risk in terms of rates, in terms of macro, and in terms of how the earnings might normalize in the long-term, I'm lowering it to 20,000 DKK/share here. This is still below the analyst PT, but it better reflects my long-term expectations and thesis for Maersk.

Thesis

- This is one of the world's most important shipping companies. At a good valuation, this company is, to me, a no-nonsense "BUY" with no looking back. The flow of goods dictates the state of our national economies, which makes the company a major player in macro.

- I view the company currently as fairly or even slightly undervalued in the face of what is an unprecedented logistics crisis.

- It's a "BUY" here to me - and I view it with a target of 20,000 DKK/share, updated as of the latest few days.

- I recently bought more in the company, and my stake in Maersk is actually growing quite rapidly, now over 0.6%.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them:

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I won't call it "cheap" here, but aside from that, you can definitely "BUY" Maersk.

For further details see:

Maersk: Still A 'Buy' Even After Double-Digit, Market-Beating Returns