MAG - MAG Silver: Quality For A Good Price

2023-04-03 06:23:51 ET

Summary

- MAG Silver has underperformed in 2023, likely due to the recently announced bought deals.

- MAG stock trades with a very attractive earnings multiple, which is rare for a low-cost silver miner that often trades at a premium.

- I do think the trust in management has taken a turn as the bought deals did not feel like optimal capital allocation decisions.

Investment Thesis

MAG Silver ( MAG ) is a silver developer with its core asset in Mexico and is in the process of transitioning to a producer. I have covered the company in the past, where my last article on the stock can be found here . I was skeptical then due to an elevated valuation, but the valuation has become much more attractive compared to a couple of years ago.

The stock price has so far this year underperformed most silver mining companies, even if it has been on par with the industry over the last year. The recent underperformance is primarily due to two very poorly received bought deals that were announced a couple of months ago, when most investor likely thought the share dilution would be in the rear-view mirror, as Juanicipio is ramping up its production this year.

The impact of the recent bought deals is relatively minimal, which means the recent share price underperformance could be an opportunity for anyone that has trust in the management team.

Figure 1 - Source: YCharts

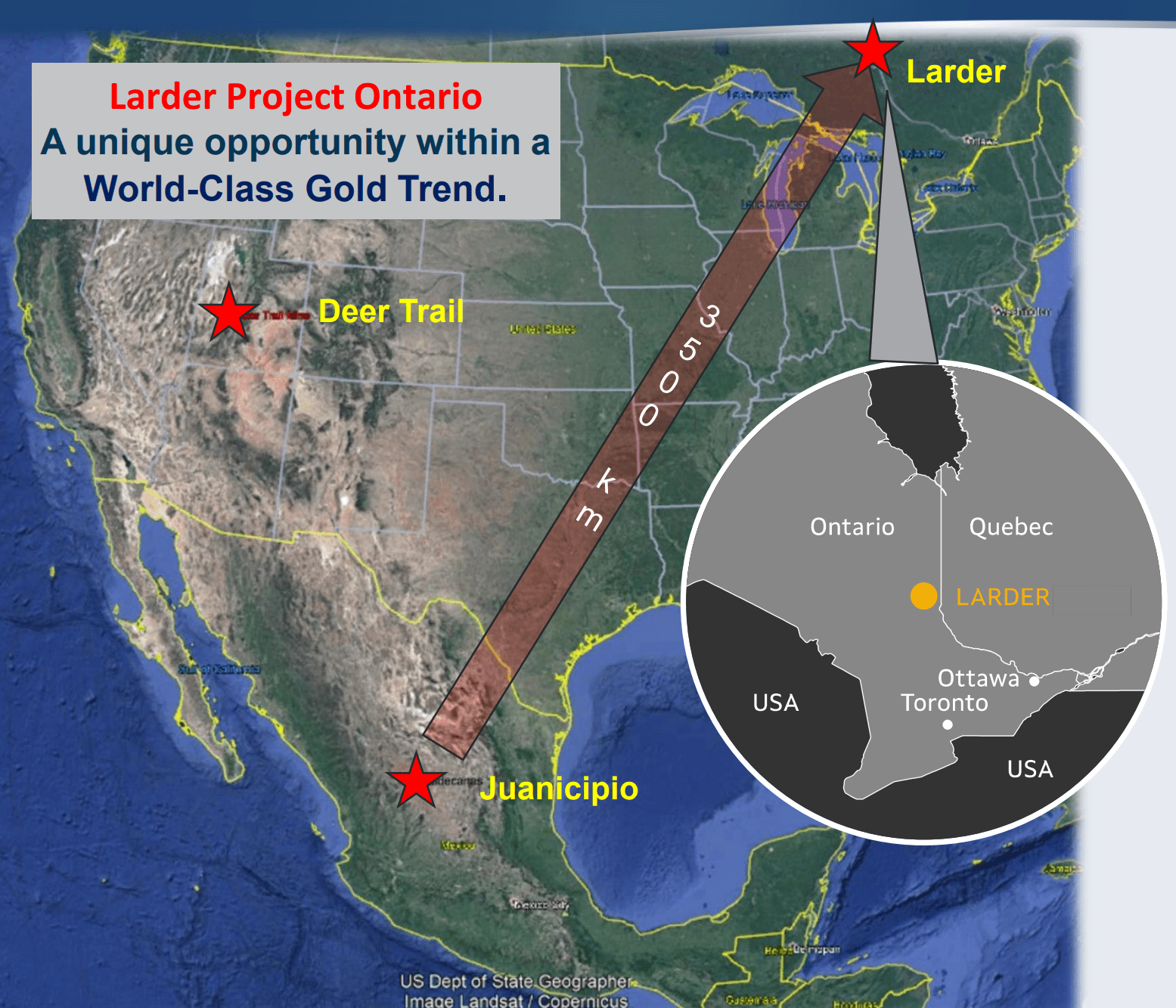

Deer Trail & Larder

MAG Silver does apart from its core Juanicipio project in Mexico have two early exploration projects: Deer Trail in Utah, United States and Larder in Ontario, Canada.

{kind=link}

Figure 2 - Source: MAG Silver Corporate Presentation

Both exploration projects are in very prospective mining areas, which if successful, could turn out to deliver substantial value to shareholders.

Having said that, we are talking about early exploration projects, where only some drilling has been done so far. So, I would prescribe very little value for that potential today. Exploration potential is not something I like to pay for, it is something you often get for free when investing in producers or later stage developers. So, I will primarily focus on Juanicipio in this article.

Juanicipio

Just about all the value of MAG Silver does in my view come from the 44% ownership interest in high-grade Juanicipio project, where Fresnillo ( OTCPK:FNLPF ) owns 56% and is the operator.

{kind=link}

Figure 3 - Source: Older MAG Silver Presentation

The project has over the last couple of years experienced delays getting to production, where the primary reason was due to a delay in getting the plant connected to the electricity grid, which was finally achieved in late December 2022.

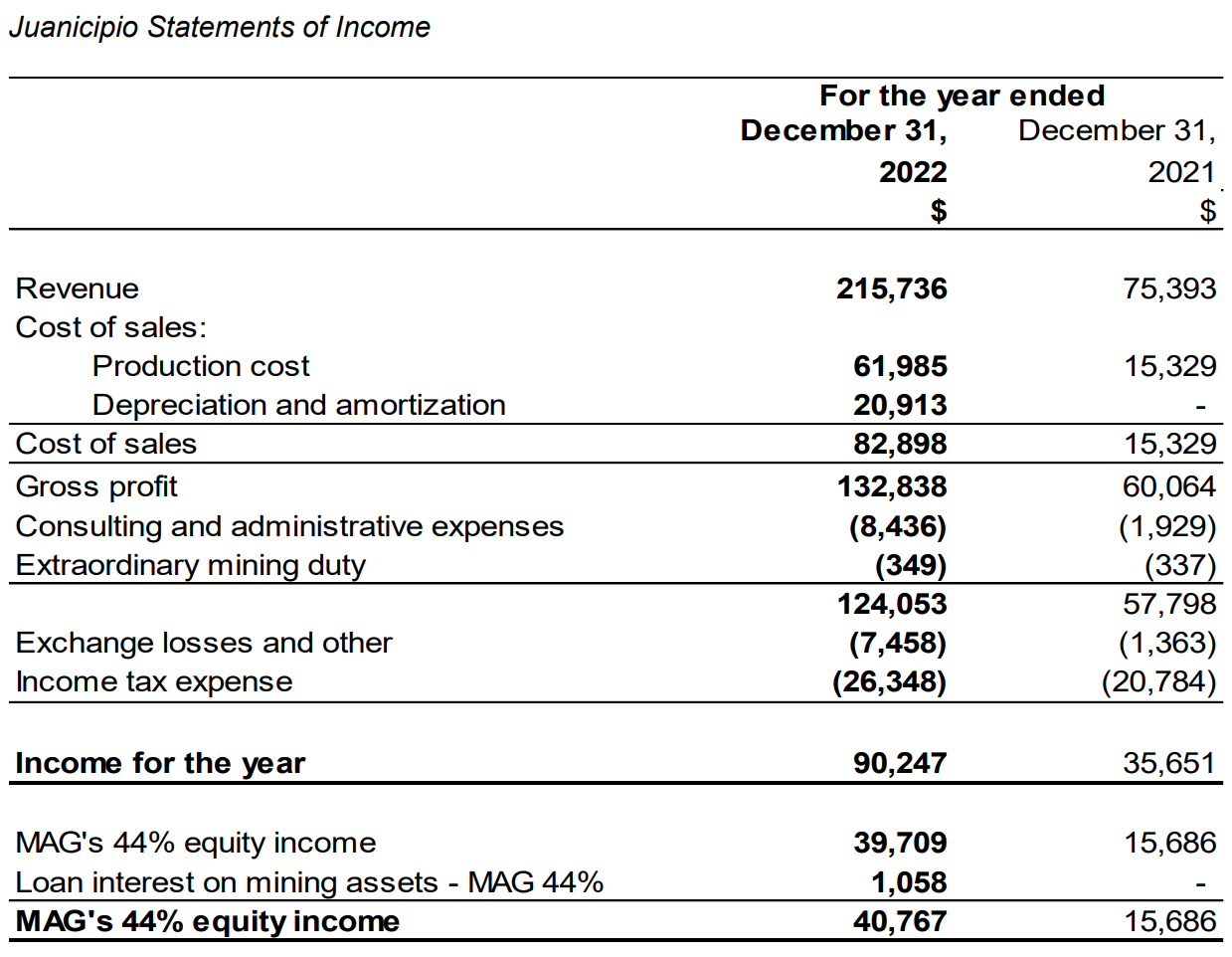

The material from the Juanicipio project has in the meantime been processed at the nearby Saucito and Fresnillo plants. That has generated revenues and a very healthy income for MAG during last year.

{kind=link}

Figure 4 - Source: MAG Q4-22 Financial Statement

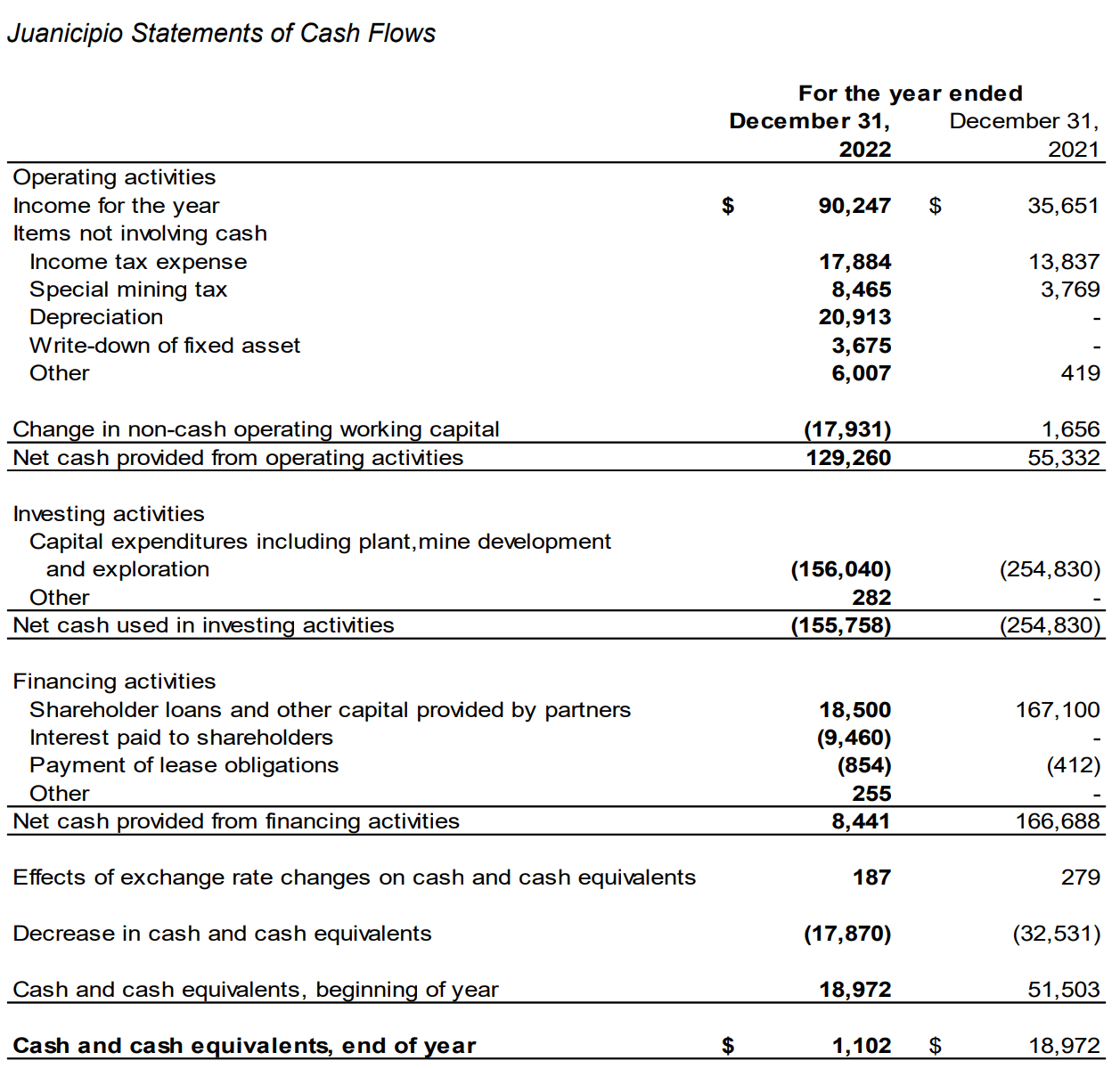

{kind=link}

Figure 5 - Source: MAG Q4-22 Financial Statement

It is important to remember that income does not automatically translate to free cash flow though. Even if Juanicipio is likely to generate very healthy cash flows soon, more capital investments could be required in the ramp up process, which will be ongoing during 2023. The company expects Juanicipio to reach nameplate capacity of 4,000 t/d in Q3-23.

{kind=link}

Figure 6 - Source: MAG Q4-22 MDA

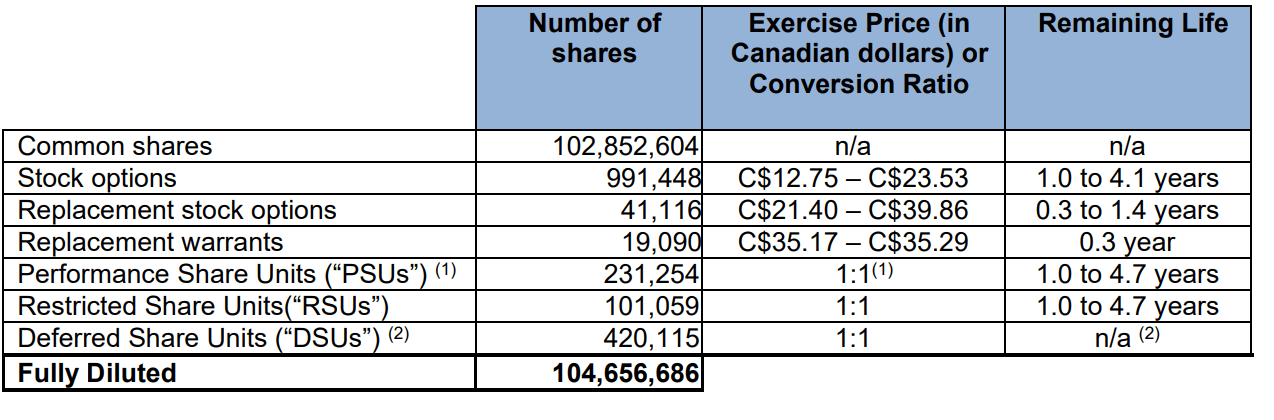

Using the fully diluted number of shares as of the 27th of March 2023 from the Q4-22 MDA, the company currently trades with a $1.30B market cap and has an enterprise value of $1.21B.

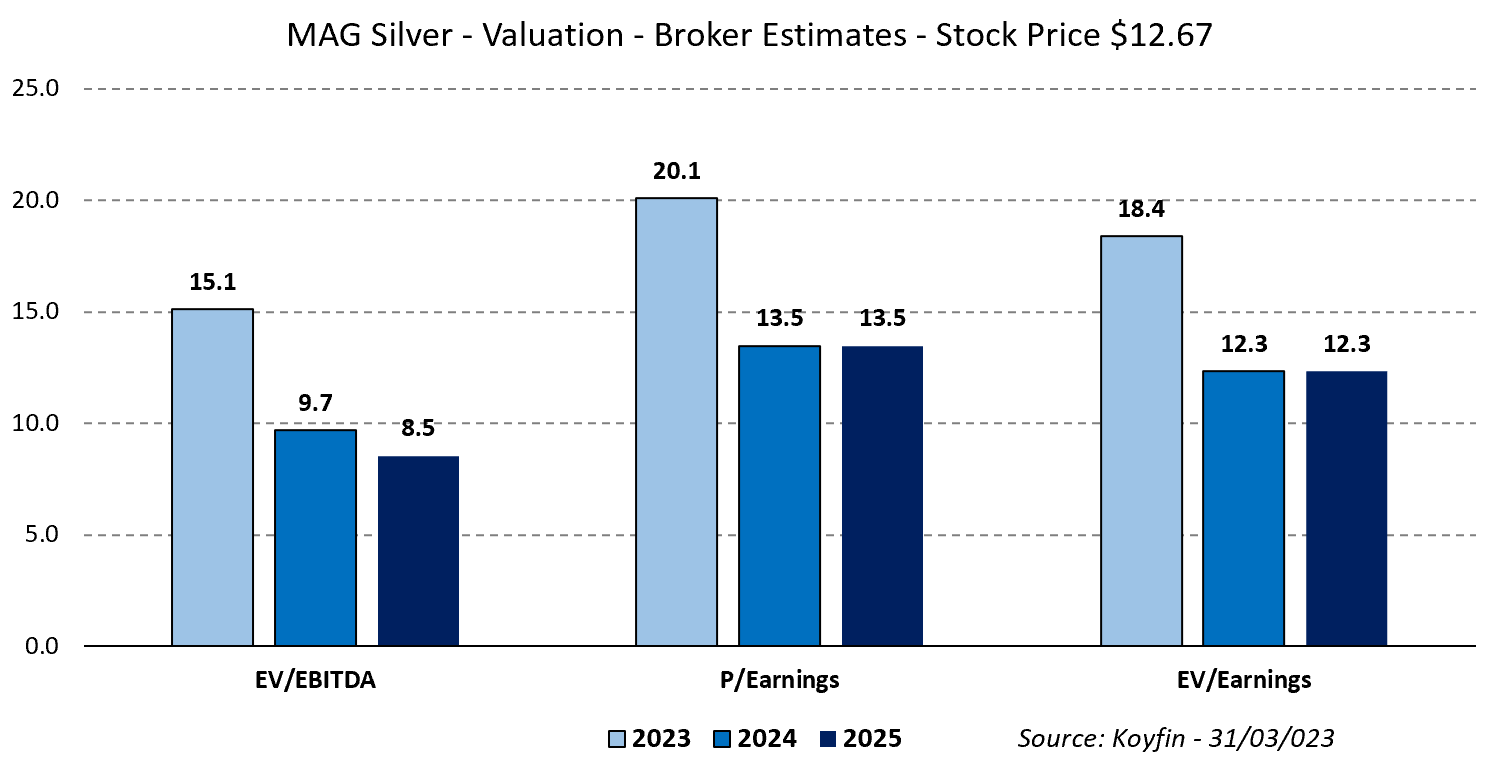

Earnings are likely to be slightly lower in 2023 given the ramp up process, but we are looking at a price to earnings ratio of 13-14 for 2024-2025, which is very attractive for silver miners. That would by my calculations roughly translate to a FCF yield around 10% for an asset that can have 15+ years of production.

{kind=link}

Figure 7 - Source: Estimates from Koyfin

Recent Bought Deals

MAG Silver did earlier this year announce two bought deals for a combined $60M. This was partly done to cover exploration in Canada and United States, where at least the money earmarked for Canada was done in a relatively tax-efficient way using flow-through shares. Another reason was as a precaution to make sure the company had sufficient capital to cover the ramp up period of Juanicipio.

While I understand the rational, I think this was far from an optional capital allocation decision. There are likely shareholders that have waited 5-10 years for Juanicipio to get into production, and this is not a good way to reward those shareholders.

The delays of getting Juanicipio to nameplate capacity would have been difficult to predict, together with all the accompanying capital requirements. However, surely getting a debt financing sorted would have been a more prudent financing option for money which might not be needed and if needed, likely can be paid back relatively quickly once Juanicipio is up and running. With regards to the exploration capital, that could have been curtailed or delayed until such time Juanicipio would have been able to fund that.

Conclusion

There is no doubt MAG Silver is cheap compared to its recent history and in relation to projected earnings. The process of ramping up production is not a massive concern in my view given the fallback option of processing material in Fresnillo's nearby plants.

If silver prices continue to climb, I suspect the poorly timed bought deals will soon be forgotten, and MAG Silver has a good chance of outperforming as the stock recovers from the recent oversold levels.

However, I will remain on the sideline and would need an even more depressed share price to invest in MAG. I really don't like the recent bought deals, which were poor capital allocation decisions in my view. If you want to be treated like a producer, and receive a premium valuation, this is exactly the kind of behavior which should be avoided. If silver has more of a sideways price action, there is a good chance it will take more time until investors overlook the bought deals, and MAG Silver might continue to underperform.

Just to be clear, it is not the impact of the bought deals which is the major concern, it is rather the trust in management. If management thought this was a good decision, rather than relying on debt financing or curtailing exploration. It is clear that management does not align with my views on how capital allocation decisions should be made, and more disappointments in the future might be likely.

For further details see:

MAG Silver: Quality For A Good Price