ITUB - Magazine Luiza: Best To Avoid This Brazilian Retailer

2024-01-05 19:43:43 ET

Summary

- Magalu's stock surged 93,000% (2015-2020) but faced a downturn, dropping 71%, 62%, and 20% in 2021, 2022, and 2023 in Ibovespa.

- Accounting issues in Q3 2023 impacted shareholder equity, raising concerns about undisclosed irregularities.

- Financially, Magalu grapples with increasing debt, equity dilution, and liquidity challenges, with a quick ratio of 0.64.

- While valuations align with reality, high leverage, accounting concerns, and short-term pressures warrant a neutral recommendation.

Magazine Luiza ( OTCPK:MGLUY ), also known as "Magalu," has undergone a significant transformation in its performance over the past several years. Between 2015 and 2020, the company's stock soared by an impressive 93,000%, reaching a valuation of R$160 billion, equivalent to around $32 billion.

However, in the subsequent three years, the stock experienced a downturn: a decline of 71% in 2021, followed by a 62% drop in 2022 and a further 41% decrease in 2023.

{kind=link}

TradingView

Despite the challenging economic environment for the retail sector, Magazine Luiza's shares have shown resilience. Factors such as accounting inconsistencies in the third quarter and struggles among its Brazilian retail peers have not significantly shaken confidence in Magalu's future. Notably, in December 2023, coinciding with Brazil's fourth interest rate cut (Selic), the shares surged by 29.21%, despite relatively high-interest rates at 11.25% and a decline in consumer spending.

While specific indicators of the company's operations have shown improvement, the recent revelation of accounting inconsistencies in this quarter adds a layer of increased risk to the investment thesis.

Magazine Luiza is traded on pink sheet markets outside Brazil through an unsponsored ADR, with a ratio of 4:1. Investors should be cautious about potential illiquidity issues and limited information.

Magazine Luiza's Business Model Overview

Magazine Luiza, one of Brazil's leading retailers, has undergone various development cycles, including expanding into the interior, entering the São Paulo market, and embracing digital transformation. In 2019, the company shifted its focus to positioning itself as a digital retail platform and ecosystem.

Five pillars support this strategy: (1) exponential growth, (2) faster delivery, (3) the Superapp, (4) offering new product categories through the marketplace, and (5) "Magalu at your Service" (or Magalu as a Service).

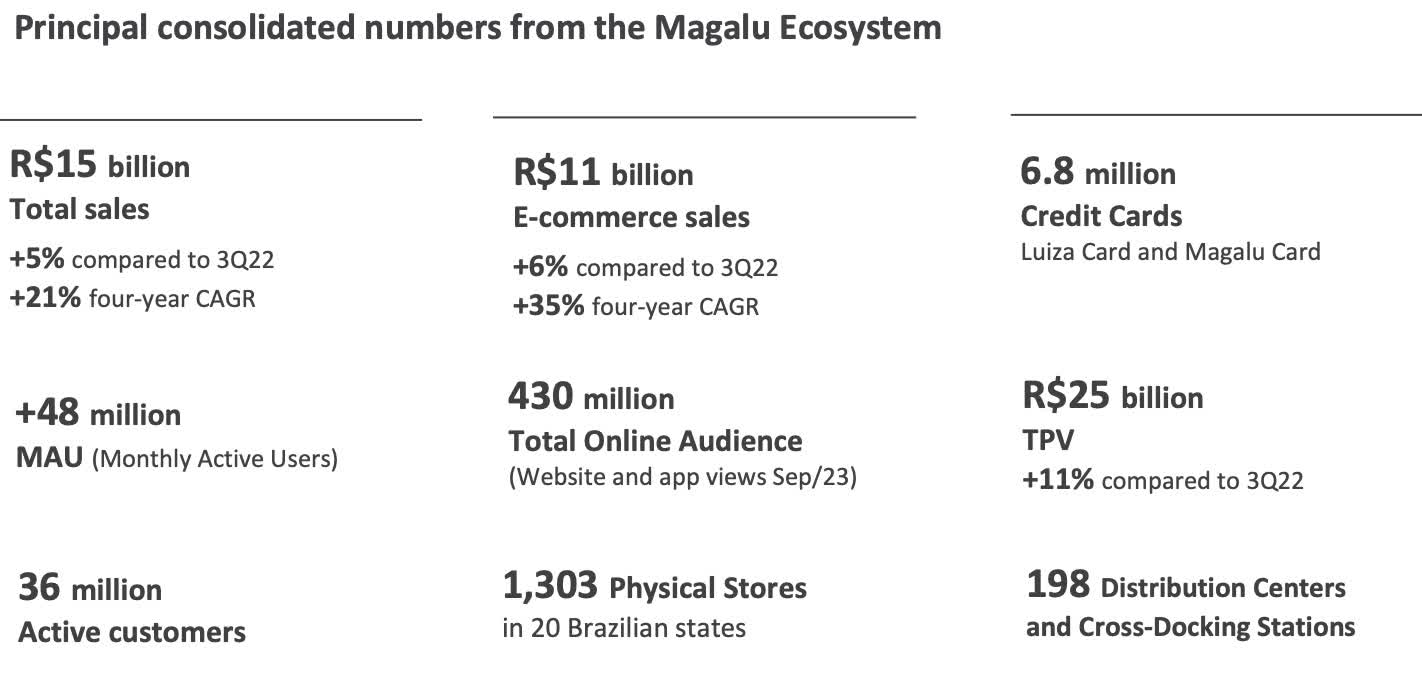

With over 35,000 employees, the company operates over 1,100 physical stores across 819 cities and 21 states in Brazil. It has 17 distribution centers and utilizes Malha Luiza, comprising around 2,500 truck drivers, for logistics. The acquisition of Logbee, a logistics technology company, was a crucial milestone that significantly improved the user experience by enhancing parcel delivery efficiency. In 2020, more than 50% of light deliveries were handled by Logbee, reducing dependence on the Post Office and minimizing the risk of delayed deliveries.

Magalu also operates Luizacred, a joint venture with Itaú Unibanco ( ITUB ) since 2001. Luizacred, a 50/50 partnership, is vital in building customer loyalty, improving sales performance, and enhancing profitability. It offers products such as the Luiza Card (credit card), personal loans, and payroll loans, contributing to increased customer purchases and overall profitability.

The integrated nature of Magazine Luiza, with its logistics and credit segments, has positively impacted the profitability of its sales, solidifying its position as a key retailer in Brazil. Over the past four years, the company's initiatives have diluted operating expenses, substantial EBITDA and Net Profit growth, and powerful operating cash generation.

The Rise and Fall and Liquidity Concerns

The period from late 2015 to the peak in 2020 marked a remarkable journey for Magazine Luiza. During this challenging period, which included the difficult years of 2015 and 2016, the retail sector in Brazil faced increased competition from several domestic retailers. Today, the market is strongly represented by global players such as MercadoLibre ( MELI ) and Amazon ( AMZN ).

Magalu, focusing mainly on products like stoves, fridges, smartphones, and televisions, survived and thrived while other companies struggled. Established brands like Ricardo Eletro, Lojas do Baú, and even Grupo Casas Bahia ( OTCPK:VIAYY ) lost market share to Magalu. Through strategic partnerships, including one with an insurance company for debt management, Magalu emerged stronger.

Since then, the company has undergone significant changes. Capitalizing on falling interest rates and a more favorable credit environment, Magalu invested in digitalization and business diversification. CEO Fred Trajano played a crucial role in leading this transformation, bringing a digital focus to the company. The establishment of Luiza Labs, a think tank dedicated to keeping the company technologically advanced, proved pioneering, positioning Magalu ahead of many traditional retailers during the transition to the digital environment.

Despite experiencing solid and euphoric initial revenue growth and net income, the pandemic further accelerated the company's positive trajectory. In the "new normal," where people sought products to enhance their home experiences, Magalu stood out with its well-established online service. The pandemic, initially seen as a potential setback, turned out to be an opportunity for companies with a robust online presence.

However, the optimistic phase of online retail was followed by a hangover. Overly optimistic expectations for the future of e-commerce and retail have been shattered. This underscores the complexity and dynamics of the market, where adaptability and continuous innovation are essential to sustain success.

The predominant factor, in my opinion, was the interest rate. In 2020, Brazil had an interest rate of 2%. In this scenario, there are inherent risks, and investors are willing to pay a premium for retailers and the potential future profits they can deliver.

Banco Central do Brasil

However, this interest rate rose to almost 14% in 2022 and persisted until 2023. Even though it is now in an interest rate cut scenario in Brazil, it is anticipated to remain above 9% for 2024, which should continue to make investors more selective. Companies that require intensive investment and heavily rely on capital may begin to suffer if they lack solid financial management, and this has been the case with Magazine Luiza since 2020.

It is crucial to note that several companies are starting to feel the impacts of this abrupt change in interest rates in Brazil. This phenomenon has affected one company and several others within the sector.

Due to the characteristics of the retail sector, which demands a significant amount of working capital, Magazine Luiza's debt has been steadily growing since 2021. EBITDA has been oscillating downwards, with slight improvements throughout this year, but still at levels much lower than those seen in 2020.

This situation has placed Magazine Luiza in a precarious position. To sustain its growth, the company requires investments, and if it cannot generate sufficient cash, it is compelled to take on increasing levels of debt. Consequently, the company has made equity offerings to fortify its balance sheet. However, this approach comes at a cost – it dilutes its shareholders and significantly impacts the company's share price.

Since 2017, the company has issued approximately 270 million new shares, resulting in a sharp decline in Magazine Luiza's share price. Presently, its ADR trades at just over $1 per share.

For Magazine Luiza, a quick ratio of 0.64 suggests that the company may encounter challenges in fulfilling its short-term obligations with its most liquid assets. Having $0.64 in highly liquid assets available for every $1 of current liabilities, the ratio indicates a potential liquidity concern. However, the company also maintains a current ratio of 1.14.

The fact that the quick ratio is lower than the current ratio suggests that a significant portion of the existing assets may consist of less liquid items, such as inventories. This implies that the company may need to rely on selling these less liquid assets to meet its short-term obligations.

There's a cautionary signal in case there is no significant recovery in the Brazilian retail sector, resulting in improved cash generation for Magazine Luiza. The future might not be promising for the company.

Magazine Luiza's Latest Results: Making Progress

In the third quarter of 2023, total sales amounted to R$14.8 billion, representing a 4.8% year-over-year (YoY) increase. Physical stores maintained nearly the same sales level YoY (+2.3% YoY), while online sales with own stock (1P) declined by 4.2% YoY, and marketplace sales (3P) increased by 24.8% YoY.

{kind=link}

Magalu's IR

Although the growth in Gross Merchandise Volume (GMV) was driven by marketplace sales, which impact revenue by recognizing only the commission charged to the seller (take rate), net revenue experienced a 2.6% YoY decline.

Adjusted EBITDA mirrored the decline in net revenue, falling 2.7% YoY. The increase in selling, general, and administrative expenses as a percentage of net revenue by 3.1 p.p. YoY was offset by the increase in gross margin, maintaining the Adjusted EBITDA margin at 5.3% YoY.

The net result for the quarter benefited from the recognition of tax credits amounting to R$523.8 million. This non-recurring event led to a net profit of R$331 million in 3Q23, compared to a loss of R$191 million in the same period the previous year.

Excluding this event, Magazine Luiza would have reported a loss of R$143 million, emphasizing the reduction in the negative impact of the net financial result as a percentage of net revenue by 1.0 p.p. YoY.

Regarding financial leverage, there was an increase of R$255.3 million in gross debt YoY but a reduction of R$923.4 million in net debt. Consequently, the company ended the quarter with R$4.1 billion in net debt, equivalent to 2.1x Adjusted EBITDA over the last 12 months, with 40.6% of the debt maturing in the short term.

Notably, there was a positive generation of R$926 million in free cash flow in the quarter, with the highlight being the generation of R$1 billion in operating activity. In the first nine months of 2023, free cash flow totaled R$2.4 billion, a significant improvement compared to the consumption of R$754 million in the same period of 2022.

Accounting Practices and Tax Credits Raise a Yellow Flag

Magazine Luiza issued a material fact after releasing its third-quarter results, revealing identified inaccuracies in accounting entries related to bonuses in specific commercial transactions. These inaccuracies stemmed from recording sales campaign launches on balance sheets before the conclusion of these campaigns.

To rectify this error, the company adjusted the corresponding accounting entries, leading to a reduction in shareholders' equity of R$829.5 million as of June 30, 2013. Notably, this adjustment did not impact cash flow and was net of taxes.

Simultaneously, the company reported the recognition of tax credits amounting to R$507.4 million (net of taxes). This recognition was based on a recent ruling by the Brazilian Superior Court of Justice ("STJ"), which clarified that PIS/COFINS should not be levied on suppliers' discounts, bonuses, and rebates. Considering these adjustments, the net shareholder equity reduction amounted to R$322.1 million.

This negative development indicates accounting inconsistencies within Magazine Luiza's practices. These inconsistencies were identified after an investigation triggered by an anonymous complaint.

While the complaint was ultimately deemed unfounded, the necessity to revise accounting entries and implement measures to enhance internal control mechanisms introduces uncertainties regarding the presence of undisclosed inconsistencies. This, coupled with concerns about the company's corporate governance, adds risk to the investment thesis, reminiscent of Brazilian retailers' challenges, exemplified by the Americanas case.

Magazine Luiza, controlled by the Trajano and Garcia family (58%), has its shares on Ibovespa (MGLU3) listed on the Novo Mercado , representing the highest standard of corporate governance in the Brazilian market. An encouraging aspect is Magalu's Board of Directors, which boasts an independent majority with four out of seven members, aligning with positive aspects of the Environmental, Social, and Governance ("ESG") framework.

Another crucial aspect to consider is that, from Magazine Luiza's perspective, the accounts receivable from installment sales (a common practice in Brazil) – though not debts in the traditional sense – represent a significant aspect of financing for the company. These receivables reflect extending credit to customers and deferring the receipt of installment sales.

While they do not incur direct financial costs, accounts receivable impact Magalu's cash flow, as they tie up capital temporarily until these receivables are converted into liquid resources. This underscores the importance of effective cash cycle management and the necessity for working capital to sustain operations while the company awaits payment for these installment sales.

Magalu reports a total debt of $2.18 billion but has $1.22 billion in accounts receivables. In practice, if significant default problems occur in its accounts receivable, these could represent a similar magnitude of debt. Defaults could threaten operating cash flow, necessitating loss provisions and harming the company's net income and overall financial health.

Valuation: Cheap or "Value Trap"?

Undoubtedly, Magazine Luiza is trading at valuations that align more with its business's reality than the last two years.

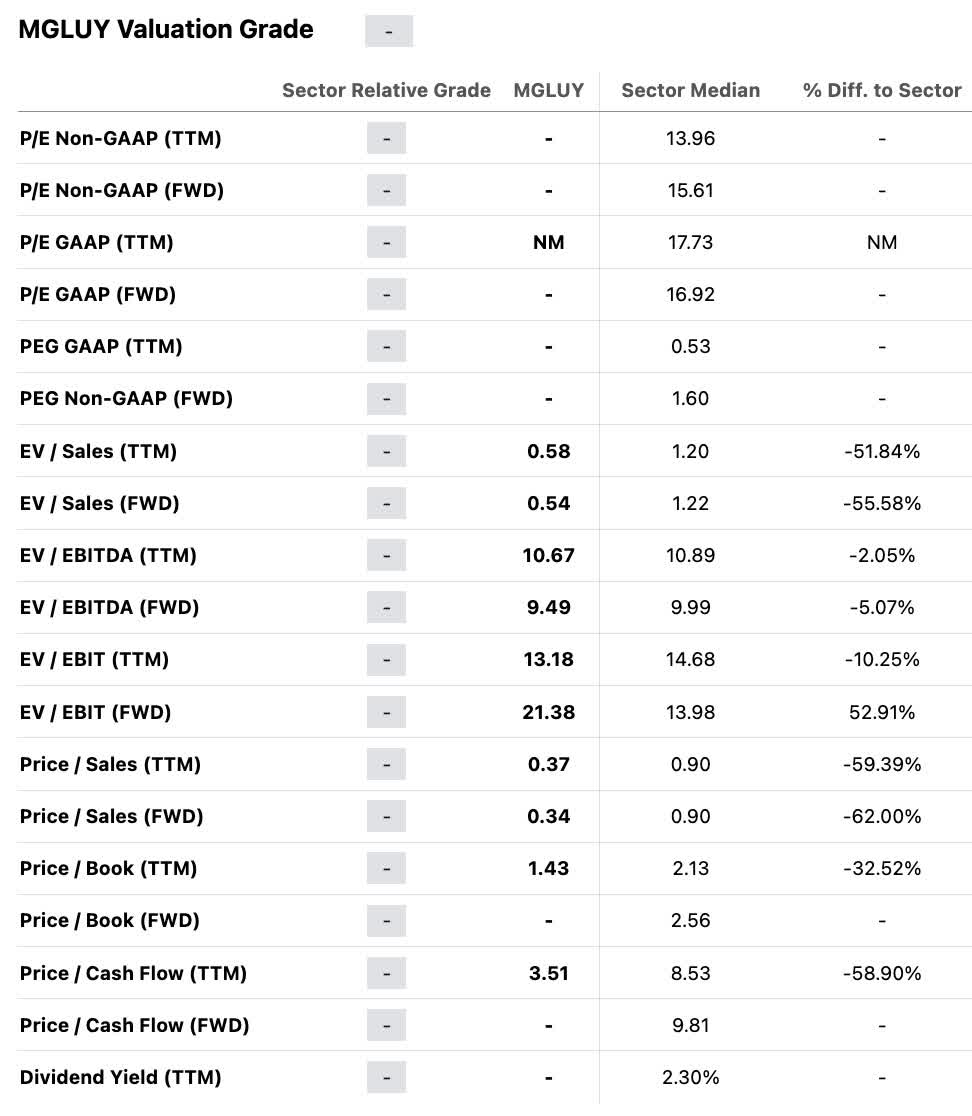

Magazine Luiza trades at a price-to-book ratio of 1.43, 75% below its historical average over the last decade. Additionally, it has a forward EV/EBITDA of 9.49x, which is 55% below its historical average over the same period. These valuations are very much in line with the retail sector average.

{kind=link}

Seeking Alpha

However, is Magazine Luiza, along with the retail sector in Brazil, genuinely inexpensive?

With year-to-date declines of almost 80% for major companies in the sector—especially Grupo Casas Bahia—reaching the status of penny stocks, taking a position in these assets might be falling into a "value trap" (i.e., when a stock appears to be at a discount but is actually undervalued because it's a bad deal).

As depicted in the chart below, Ibovespa currently exhibits a substantial short interest in the retail sector, with a 12.2% short interest in Magazine Luiza's shares. This reflects the prevailing pessimism towards the industry, particularly following the accounting scandal involving Americanas.

{kind=link}

XP Inc.

Despite having a short interest of 12.2%, Magazine Luiza's lending rate is 8%. This suggests that the availability of shares to borrow is not very high, especially compared to Americanas. This could be attributed to Magazine Luiza's already extensively diluted float. Theoretically, this factor makes the thesis less susceptible to a turnaround or a short squeeze.

The Bottom Line

Magazine Luiza should continue strengthening its online presence as the company solidifies a higher level of maturity in the digital channel and an increasingly robust ecosystem regarding product variety and infrastructure to support sales.

With a more developed digital channel contributing to the company's operating leverage and the end of the interest rate hike cycle alleviating pressure on financial expenses, Magazine Luiza's outlook for the future appears more positive in the coming months.

I foresee more positive signals for the e-commerce sector in anticipation of economic improvement. Following a challenging period with high-interest rates and inflation impacting consumer purchasing power, I believe the population will gradually return to consumption patterns in 2024, providing the e-commerce sector more momentum.

Therefore, Magazine Luiza is well-positioned to capitalize on this improved scenario. The ecosystem created by the company is expected to continue driving the growth of digital operations, enabling the company to gain market share further despite the heavy presence of MercadoLibre in Brazil.

Moreover, the conclusion of the interest rate hike cycle should benefit Magalu, facilitating a gradual reduction in financial expenses and alleviating pressure on the company's profit.

While acknowledging the company's growth potential, I recognize that Magalu may face short-term pressures due to its high leverage, with nearly $600 million in debt due in the short term, and the potential repercussions of the accounting inconsistencies disclosed in the press release. It wouldn't be surprising to see an announcement of a Magazine Luiza follow-on in the coming months to reduce leverage and address liquidity to facilitate the company's growth in the coming years. However, despite the company's hint that, after the gross margin recovery in the third quarter of 2023, the plan is to settle operations with its own cash, I remain pretty skeptical.

Until Magazine Luiza addresses these issues, I maintain my neutral recommendation for the company.

For further details see:

Magazine Luiza: Best To Avoid This Brazilian Retailer