MGTA - Magenta Therapeutics: Potential Upside In The Merger Wait To Buy More

2023-07-28 10:36:08 ET

Summary

- Magenta Therapeutics, a previously promising biotech firm, halted operations following a clinical trial tragedy, but its merger with Dianthus Therapeutics provides opportunities and a potential brighter future.

- Dianthus Therapeutics, focused on developing antibody complement therapeutics, shows impressive growth potential, especially with its lead drug DNTH103, which aims to treat serious autoimmune diseases like CAD (Cold Agglutinin Disease).

- The merger, expected to close in Q3 2023, may offer significant potential returns for current Magenta shareholders despite their reduced stake in the combined company.

Introduction

After going on 3 years without any analyst coverage, I thought it was time this company was due for another set of eyes. Magenta Therapeutics ( MGTA ) is a clinical-stage biotech company out of Cambridge, Massachusetts, specializing in stem cell biology aiming to transform stem cell transplantation (or bone marrow transplantation) for patients with immune and blood-based diseases. This procedure treats damaged and destroyed bone marrow and replace them with healthy stem cells. The company announced in May of its plan to merge with Dianthus Therapeutics. Throughout this analysis, I will be assessing the merged company value for Magenta investors, which includes Dianthus' existing assets and prospects.

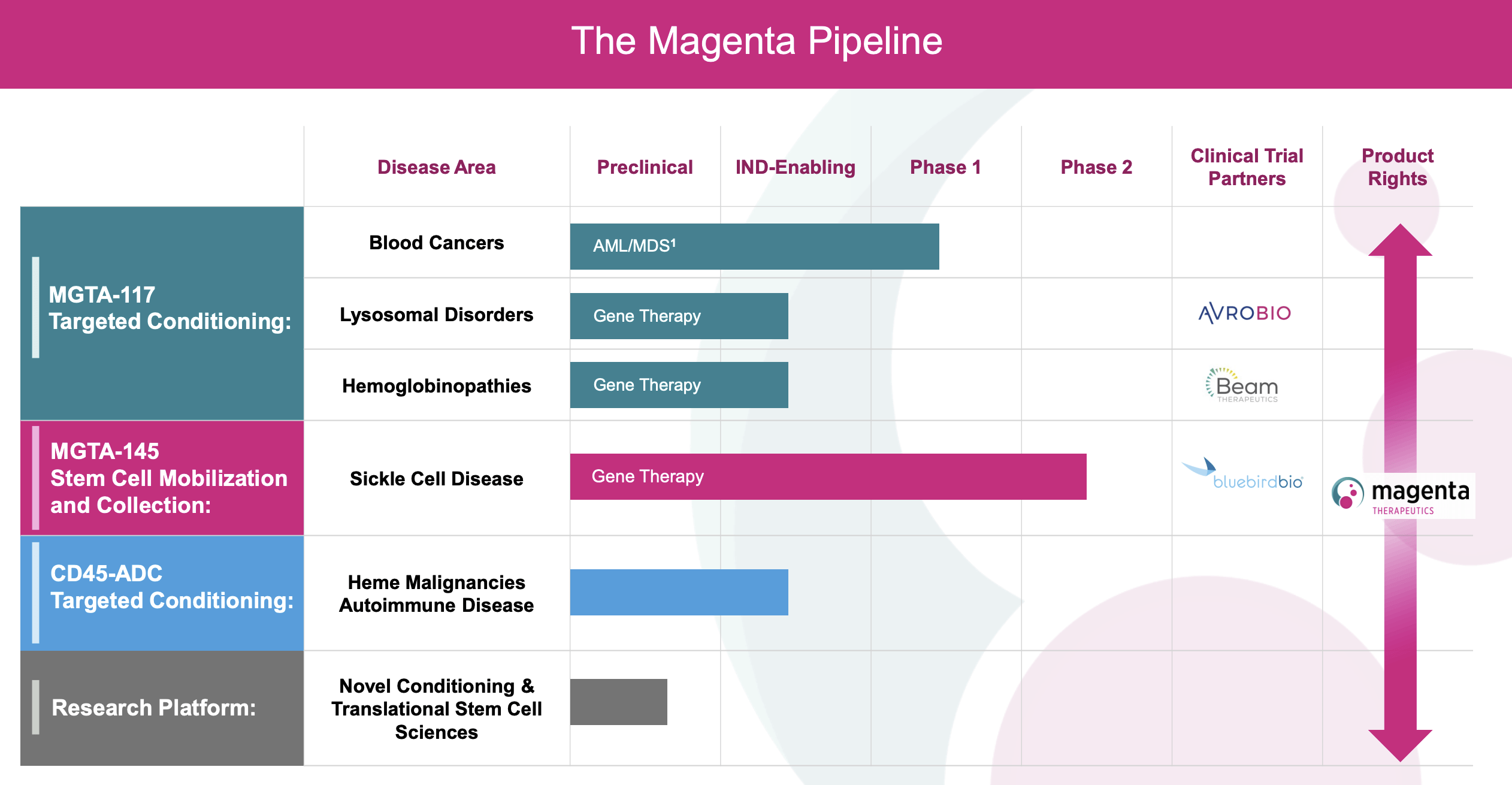

Prior to the company's end to operations in February 2023, Magenta was primarily focused on the development of two drugs:

MGTA-145 - a drug aiming to mobilize large amounts of hematopoietic stem cells so that they can be used for stem cell transport to treat conditions like leukemia, lymphoma, and multiple melanoma. MGTA-145 is the drug closest to FDA approval at Phase 2 of clinical trials. In December of 2020, the company also partnered with bluebird bio to evaluate the drug for its Phase 2 clinical trial.

MGTA-117 - an antibody drug conjugate targeting CD117 to be used independently to condition the body for HSCT, or stem cell transplant. In its most recent clinical trial in December, the trials had to halt dosing for Cohort 4 because two out of three patients experienced severe respiratory side effects, including respiratory problems and alterations in liver enzymes. At a lower dosage level, the drug proved effectiveness in reducing cancer cells, leading the company to deem the drug as both safe and potentially beneficial.

{kind=link}

Magenta Therapeutics

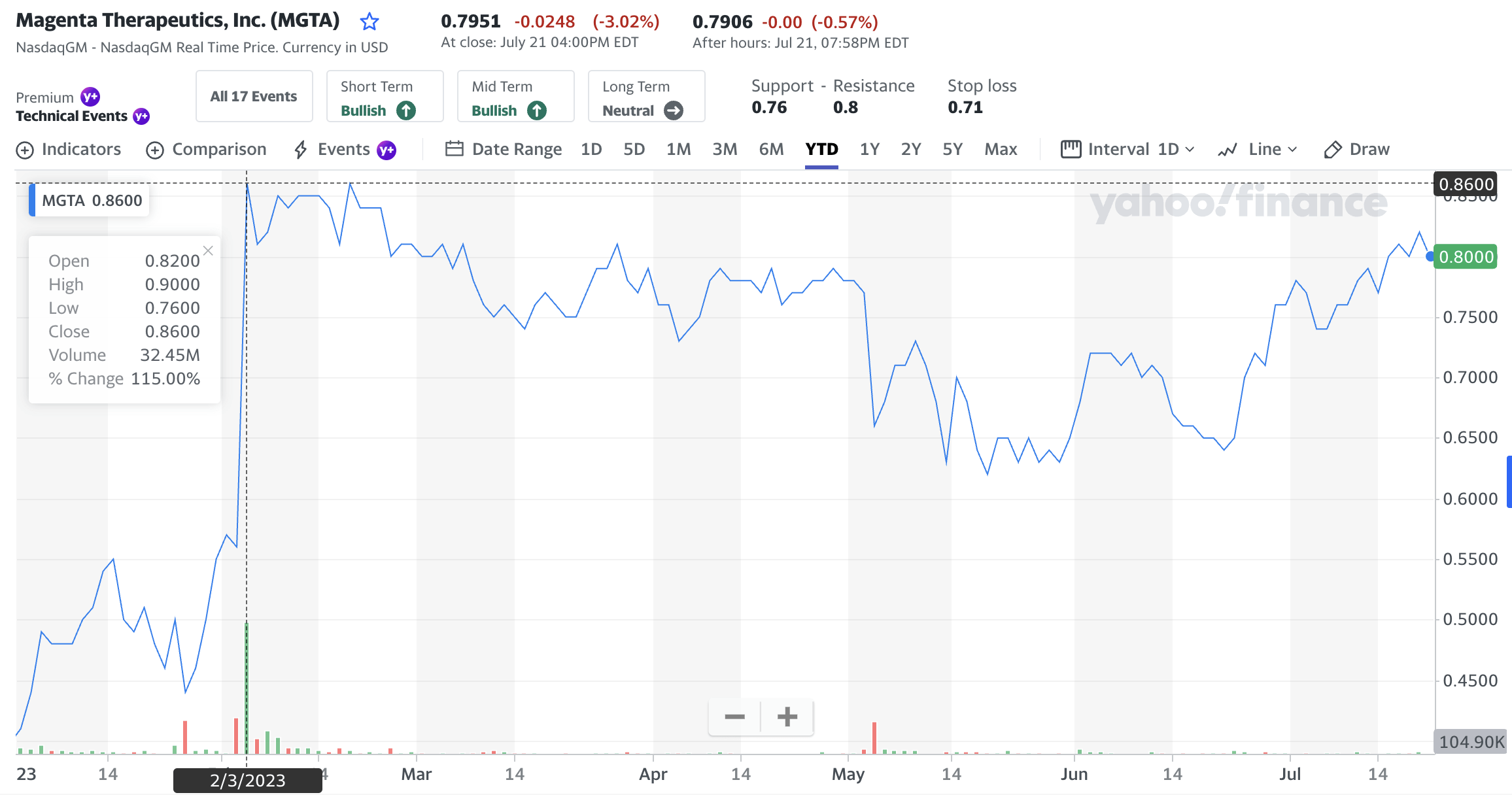

However, in January this year, the company had to pause its Phase 1/2 trial for MGTA-117 as a result of the death of a clinical participant from respiratory failure and cardiac arrest. The company had to then halt operations entirely and decided instead to pursue either a merger or an acquisition . The CEO promptly resigned, alongside other top executives. In a surprising turn of events, the stock price promptly surged 95% in the matter of a week following the death of the patient and 47% the day the company announced its plans to pursue strategic alternatives. Its price has fallen slightly since, but has relatively maintained stability. As of July 24, 2023, Magenta has a market cap of slightly over $48 million, trading at 79 cents a share.

{kind=link}

Yahoo Finance

In May, the company announced its agreement to merge with private biotech company, Dianthus Therapeutics. The merger is expected to be completed in the third quarter of 2023 and Magenta will operate under the name Dianthus Therapeutics to be traded on the Nasdaq under the ticker "DNTH". Magenta stockholders prior to the merger are expected to own about 21.3% of the combined company following the merger, and the percentage is subject to change based on the Magenta's net cash at the date of closing. Despite this smaller percentage, Magenta stockholders will also receive contingent value rights that give them future earnings potential from profits made by Dianthus from Magenta's pre-merger assets.

Dianthus Therapeutics

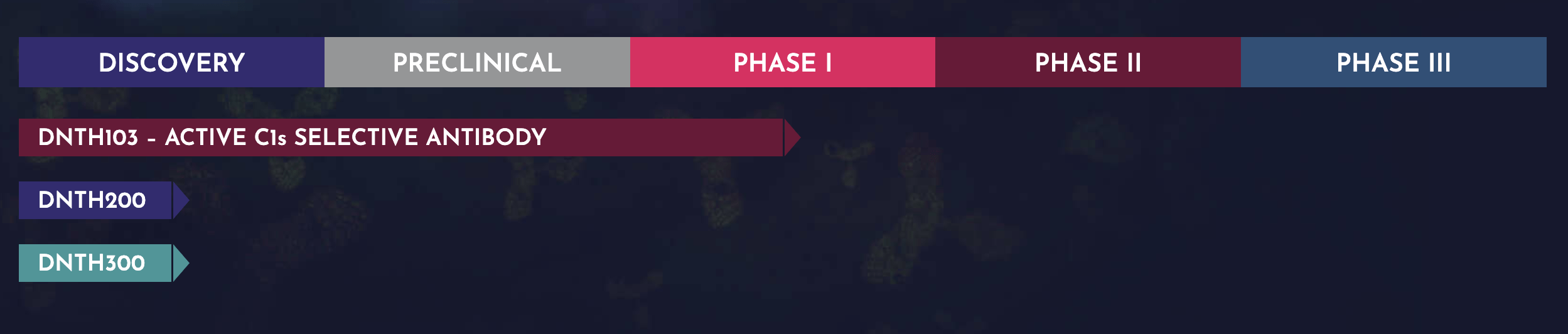

Dianthus Therapeutics is a clinical-stage private biotech company based in Waltham, Massachusetts. The company aims to advance antibody complement therapeutics to potentially reduce dosages and frequency. DNTH103 is the main drug the company is developing in its pipeline and is currently at Phase 1 of clinical trials.

{kind=link}

Dianthus Therapeutics

DNTH103

DNTH103 is a monoclonal antibody being developed with the goal of treating serious autoimmune diseases like type 1 diabetes and multiple sclerosis, among others. The drug suppresses complement C1s protein and is given through a simple injection under the skin, which is intentionally designed to make treatment easier and less frequent. The drug's frequency reduction is achieved through YTE half-life extension technology, which increases the drug's longevity in the body. The drug has several upcoming trials, and the company hopes that it will deliver results as expected. Dianthus has an extensive vision for the drug's potential, with expectations that the drug will start a new trial for treatment of the condition Myasthenia Gravis in early 2024, alongside expectations to start trials for Cold Agglutinin Disease ((CAD)) in late 2024.

In November 2022, Dianthus transitioned into a clinical stage company as its main drug, DNTH103, advanced from preclinical studies to its Phase 1 study. The current Phase 1 trial is examining how safe single and multiple doses of DNTH203 are when administered to healthy adult volunteers. The trial is also assessing its potential side effects and its ability to suppress complement cascade. DNTH103 is also competing with a previously approved FDA therapy for CAD called Enjaymo. However, Enjaymo binds to both active and inactive C1s protein, which means that patients must take the medication at higher frequency to reduce symptoms. According to Simrat Randhawa , M.D., Chief Medical Officer at Dianthus Therapeutics, "All currently approved complement antibody therapies indiscriminately bind to both active and inactive complement proteins – meaning a large, sometimes frequent dose must be administered while a significant portion of the drug acts unnecessarily on inert proteins." Essentially, the problem with Enjaymo and other similar drugs approved for complement therapies is that a heavy dosage must be administered while a large portion of it acts on inactive proteins that do not necessarily cause symptoms.

Financials

In 2022, Dianthus reported a total revenue of $6.4 million, growing over 334% from 2021's total revenue of $1.5 million. The company also incurred a loss from operations of over $29 million in 2022, a significant increase from $13 million in 2021. Despite this, the company holds over $75 million in total cash and cash equivalents with less than $1 million debt, which is over 1000% greater than its cash from the year prior. The company only spent $139,000 in capital expenditures in 2022, but the company is likely to spend significantly on capital expenditures in the next 1–3 years to finance clinical trials and further research and development, provided that the company's vision for DNTH103 consists of future clinical trials to treat various other conditions. Therefore, investors should continue to expect cash flow negative throughout the next few years. Moreover, Dianthus raised $100 million from its Series A funding round in 2022 which mostly counteracted its cash loss from operations, and in May of this year, Dianthus secured $70 million of private investment in common stock and pre-funded warrants from a myriad of healthcare investors. Following the closing of the merger, the combined cash from both Magenta and Dianthus is expected to reach a total of $180 million. Dianthus will use this cash on capital expenditures relating to the advancement of Dianthus' pipeline, and it is anticipated that it will finance these operations throughout mid-2026 . Overall, Dianthus' financials look very attractive to me, and despite being operationally cash flow negative of $29 million in 2022, the company has the necessary resources to achieve high growth in the coming years.

Risks

The main concern with Dianthus right now is that it is an early clinical stage company, with only one drug that has potential in its pipeline. The other two are not even undergone preclinical trials. Regardless of solid financials and future growth potential, Dianthus is a cash burning company at the end of the day, and will likely be operationally cash flow negative for years to come. How will the company be able to continuously fund clinical trials and research and development for not just DNTH103 but also its two other drugs in the pipeline after year 3 when cash runs out and the company does not have a consistent source of cash flow? While current combined cash from Dianthus and Magenta can fund operations throughout 2026, but the problem is that the company has no effective plan to generate cash after that. It is likely that the company will have to depend heavily on leverage and funding, or it will have to issue new shares that dilute current shareholders. For any medication or treatment to be FDA approved, it takes, on average, 10 years from initial discovery to full approval, with clinical trials taking 6–7 years of the 10.

Additionally, Magenta shareholders only own 21.3% of the combined company following the merger, and while shareholders will be issued contingent value rights and will have the opportunity to generate additional income from profits of the combined company, these rights have not been specified yet, and neither has a time frame for their implementation been provided. Like I mentioned above, it is very unlikely the company will bring in substantial profits in the formative years of its clinical stage trials.

Conclusion

Overall, if DNTH103 can establish its safety and demonstrate greater potency at lower doses, and thereby reducing the frequency of intake, then it has the potential to be successful and profitable. This will allow DNTH103 to capture a larger market share for treatments for CAD and potentially outperform competitors like Enjaymo. I anticipate the closing of the merger will be supportive of the stock price in the third quarter, given that the stock increased following both the death of the patient as well as the company's announcement to end operations and pursue exit opportunities. For those that currently own shares of MGTA, my recommendation would be to not sell at this time. While I would recommend a Buy, I advise waiting until the deal closes, as an updated financial report of the combined company can provide investors with a more accurate assessment of the company's health.

For further details see:

Magenta Therapeutics: Potential Upside In The Merger, Wait To Buy More