MGIC - Magic Software: A Cheap IT Pick With A High Dividend Yield

2023-11-02 23:37:24 ET

Summary

- Magic Software Enterprises is an IT product and solutions provider with a history of growth through small acquisitions.

- The stock has a low forward P/E ratio of 9.2 and a high dividend yield of 6.40%.

- The company's financials are mostly stable, with a healthy EBIT margin and stable revenues.

- At the current price, I see Magic Software's risk-to-reward as good.

Magic Software Enterprises ( MGIC ) is an IT product and solutions provider. The company has a history of achieving growth through constant small acquisitions. Magic Software has achieved a stable earnings level with quite little turbulence in the company’s EBIT margin. The stock seems to currently trade at a very cheap level, as the stock has a forward P/E of 9.2 and a dividend yield of 6.40%. To take a further look into the valuation, I constructed a discounted cash flow model to demonstrate the cheap valuation in a more thorough way.

The Company & Stock

Magic Software provides information technology products and solutions. The company’s products include data driven manufacturing monitoring, analytics cloud services, as well as multiple platforms and frameworks for code development and similar processes. Magic Software’s solutions are mostly around integration of third-party applications, with solutions such as SAP ERP integration, Oracle JD Edwards integration, Microsoft SharePoint integration, and Salesforce integration. The company has a good amount of well-known customers – for example, Magic Software’s customers include Coca Cola, Nespresso, Nintendo, Microsoft, Vodafone, and the World Bank.

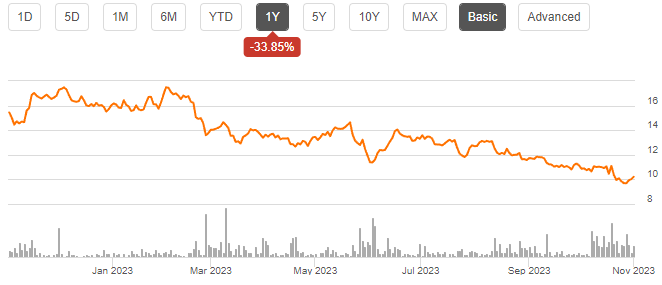

The stock hasn’t performed very well recently – in a year, Magic Software’s stock has lost around a third of its value:

{kind=link}

The stock does have a very good dividend yield, though. Currently, Magic Software’s forward dividend yield is estimated at a figure of 6.40%, higher than the majority of growing companies especially in the IT industry.

Financials

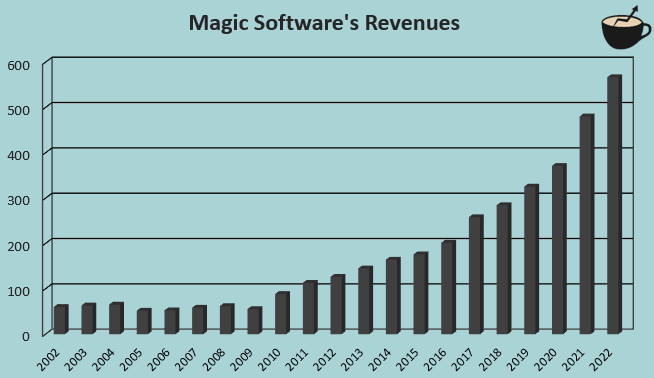

Magic Software’s revenues have grown well in the past two decades. From 2002 to 2022, the company’s compounded annual growth rate has been 11.9%:

{kind=link}

The revenue growth started to accelerate from 2010 forward. The company seems to have had a change in its strategy in the year, as Magic Software has had cash acquisitions in every year beginning in 2010. From 2010 to 2022, Magic Software’s cash acquisitions add up to a sum of $188 million – compared to the company’s current market capitalization of $502 million, the acquisitions make a good part of the company’s growth and current operations.

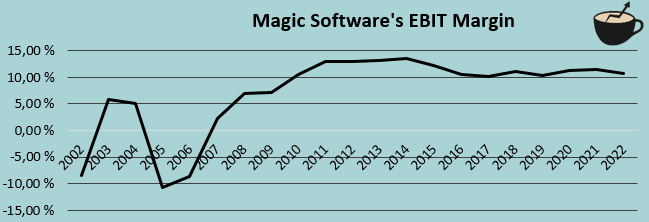

At the same time that Magic Software’s acquisition-focused strategy began, the company’s EBIT margin also reached a good level. From 2002 to 2022, Magic Software’s average EBIT margin is 7.2%, but from 2010 forward into 2022, the average margin is 11.6% with mostly stable figures:

{kind=link}

With trailing figures, Magic Software’s margin stands at 10.6% , near the figures that the company has achieved in recent years.

Valuation

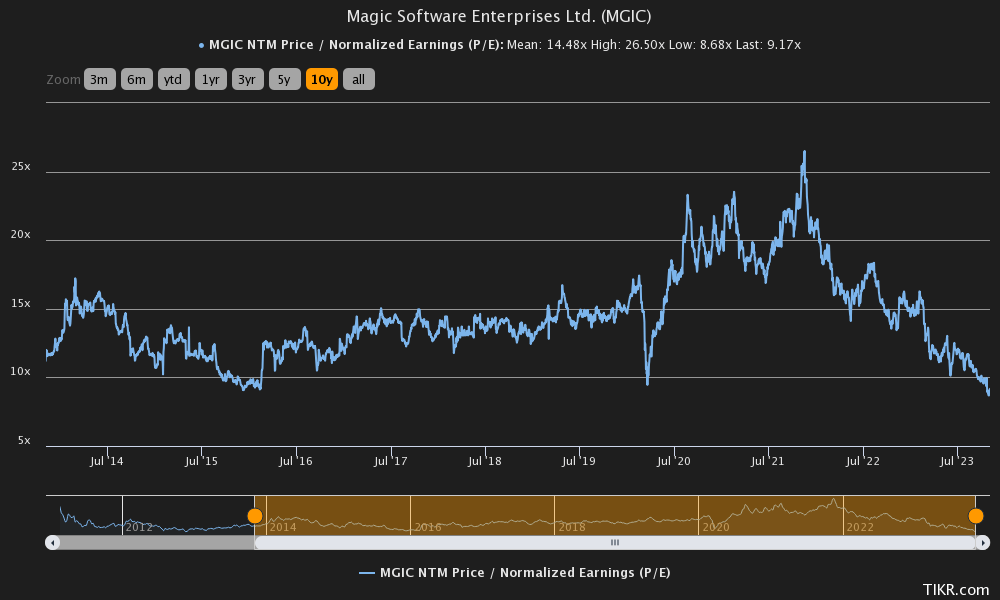

Currently, Magic Software trades at a forward P/E ratio of 9.2, around 37% below the company’s ten-year average and at near the company’s lowest point in the period:

{kind=link}

In my opinion, the P/E ratio seems quite low for Magic Software as the company grows slightly and has quite stable operations. To further analyse the valuation and to estimate a rough fair value for the stock, I constructed a discounted cash flow model in my usual manner.

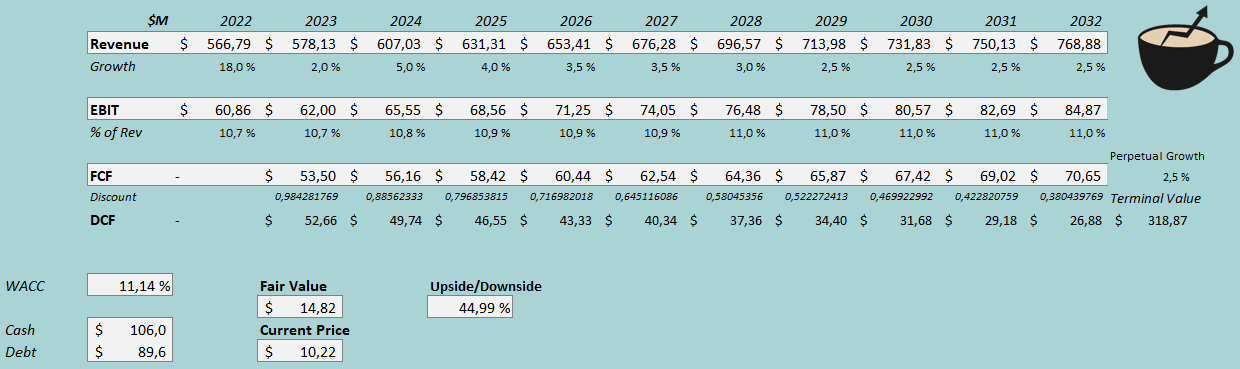

In the model, I estimate Magic Software’s growth to be 2% in 2023, in line with the company’s guidance of revenues between $570 million and $580 million. After the year, I estimate a higher amount of growth at an estimate of 5% for 2024. Beyond the year, I estimate Magic Software’s growth to slow down in steps into a perpetual growth rate of 2.5% from 2029 forward. In total, the revenue estimates correspond to an organic CAGR of 3.1% from 2022 to 2032 – I believe that the estimated growth is very reasonable to expect.

For Magic Software’s EBIT margin, I estimate a mostly stable future. For 2023, I estimate the margin to stay at the 2022 level of 10.7%. After the year, I estimate slight leverage into a margin that’s closer to the 2010 to 2022 average of 11.6% - in the model, the EBIT margin scales into a figure of 11.0%, achieved in 2028. The estimated margin is still below Magic Software’s average in the period; I believe that the estimate is quite conservative. The company has a good cash flow conversion, as the accounting earnings include a good amount of amortization from previous acquisitions.

In total, the mentioned estimates along with a weighted average cost of capital of 11.14% craft the following DCF model with a fair value estimate of $14.82, around 45% above the current price at the time of writing, representing a fair forward P/E of 13.3 with analysts’ estimates – Magic Software seems to be priced with a significant undervaluation:

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In the past twelve months, Magic Software has had $1.9 million in interest expenses. With the company’s current amount of interest-bearing debt, Magic Software’s interest rate comes up to a figure of 2.12%. The interest rate seems very low, and Magic Software’s interest expenses have fluctuated largely between quarters. I believe that the interest rate could well be higher in reality, but in the absence of a better figure to use, I use the estimated 2.12%. Magic Software leverages debt quite moderately, and I estimate the company’s long-term debt-to-equity ratio to be 10%.

On the cost of equity side, I use the United States’ 10-year bond yield of 4.73% as the risk-free rate. The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the US, made in July. Yahoo Finance estimates Magic Software’s beta at a figure of 1.18 . Finally, I add a small liquidity premium of 0.5%, crafting a cost of equity of 12.20% and a WACC of 11.14%.

Takeaway

At the current price, Magic Software seems to be priced quite attractively. The company pays a good dividend yield. In addition, the company expands its operations through constant small acquisitions. Magic Software is preparing for a softer growth in 2023 as the guidance points towards a low single-digit growth in the year, but I believe that the softness represents a buying opportunity – my DCF model estimates the stock to be quite significantly undervalued with estimates that I see as mostly conservative. For the time being, I have a buy rating for the stock.

For further details see:

Magic Software: A Cheap IT Pick With A High Dividend Yield