MGIC - Magic Software Enterprises Sees Slower Growth In 2023

2023-05-25 15:54:40 ET

Summary

- Magic Software Enterprises reported its Q1 2023 financial results on May 18, 2023.

- The firm provides outsourced IT software development and related services to organizations worldwide.

- Management has guided to relatively slow revenue growth in 2023 and the firm is exposed to slowing industries such as technology and telecom.

- In the near term, I'm Neutral [Hold] for MGIC.

A Quick Take On Magic Software Enterprises

Magic Software Enterprises ( MGIC ) reported its Q1 2023 financial results on May 18, 2023, missing revenue and meeting EPS consensus estimates.

The firm provides organizations with an array of IT software development and related consulting services.

Given management's tepid growth estimate for 2023 and the potential for further macroeconomic headwinds, I'm Neutral [Hold] on MGIC in the near term.

Magic Software Overview

Israel-based Magic Software Enterprises was founded in 1983 to provide outsourced software development services to customers in Israel and overseas.

The firm is headed by Chief Executive Officer Guy Bernstein, who has been with the firm since 2007, was previously CEO of Emblaze, Magic's former controlling shareholder. He is also Chairman of Sapiens International and Matrix IT, both of which are subsidiaries of Formula Systems.

The company's primary offerings include the following:

-

FactoryEye.

-

Integration platform.

-

Low code development.

-

Web application framework.

-

EDI service platform.

-

Mobilization and modernization.

The firm acquires customers through its direct sales, marketing, and business development efforts and through partner referrals and word of mouth.

Magic Software's Market & Competition

According to a 2021 market research report by 360 Market Updates, the global market for IT strategy consulting was an estimated $58.2 billion in 2019 and is forecast to reach $143 billion by 2025.

This represents a forecast CAGR of 16.2% from 2020 to 2025.

The main drivers for this expected growth in IT consulting are a large transition from on-premises, legacy systems to cloud-based environments with complex architectures.

There is also expected growth in the number of industries adopting digital transformation strategies, such as manufacturing, finance, and retail, as well as a growing demand for improved customer experience.

IT outsourcing firms can also leverage their expertise to help companies develop and maintain new or better business models which are better suited to the digital world.

Also, the COVID-19 pandemic likely pulled forward significant demand to modernize enterprise systems, resulting in increased growth prospects for digital transformation consultancies.

The growth of IT consulting and outsourcing is expected to continue due to the evolving digital landscape, increased demand for improved customer experience, the need to develop and maintain new or better business models, and the accelerated demand for modernization due to the pandemic.

Major competitive or other industry participants include:

-

Globant.

-

Thoughtworks.

-

EPAM.

-

Slalom.

-

Accenture.

-

Deloitte Digital.

-

McKinsey.

-

BCG.

-

IDEO.

-

Cognizant Technology Solutions.

-

Capgemini.

-

Computer Task Group.

-

Company in-house development efforts.

Magic Software's Recent Financial Trends

-

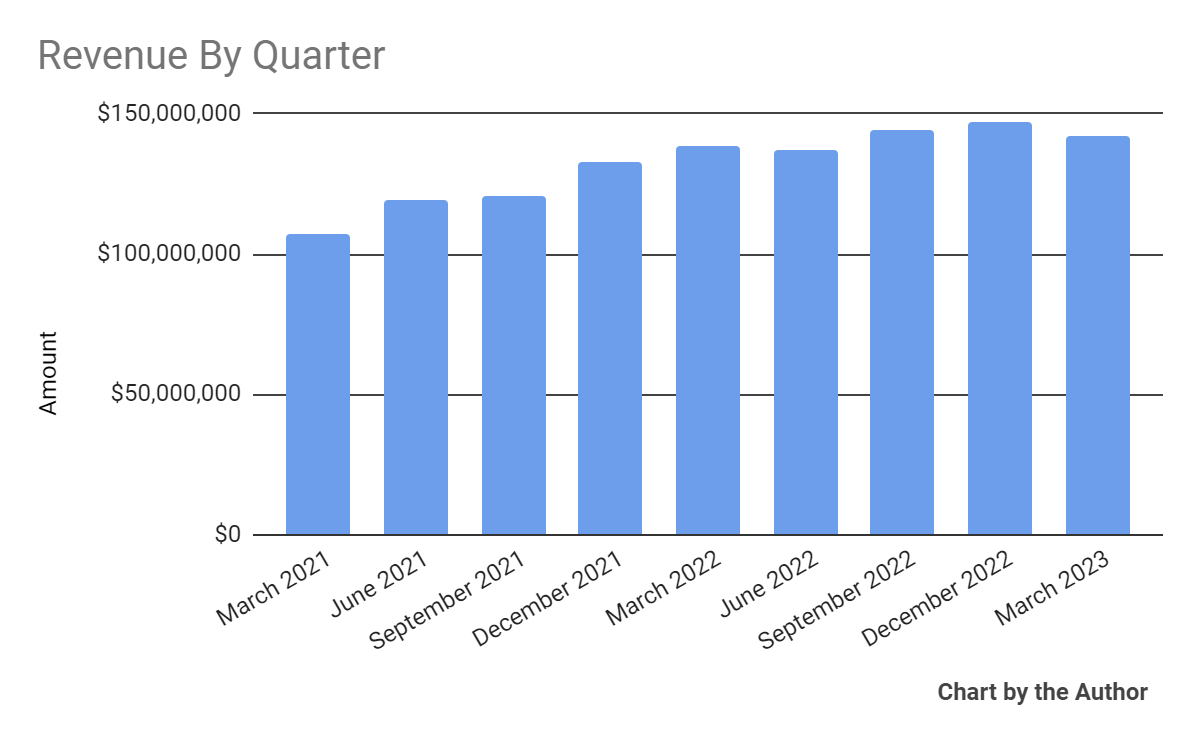

Total revenue by quarter has grown per the following chart:

Total Revenue (Seeking Alpha)

-

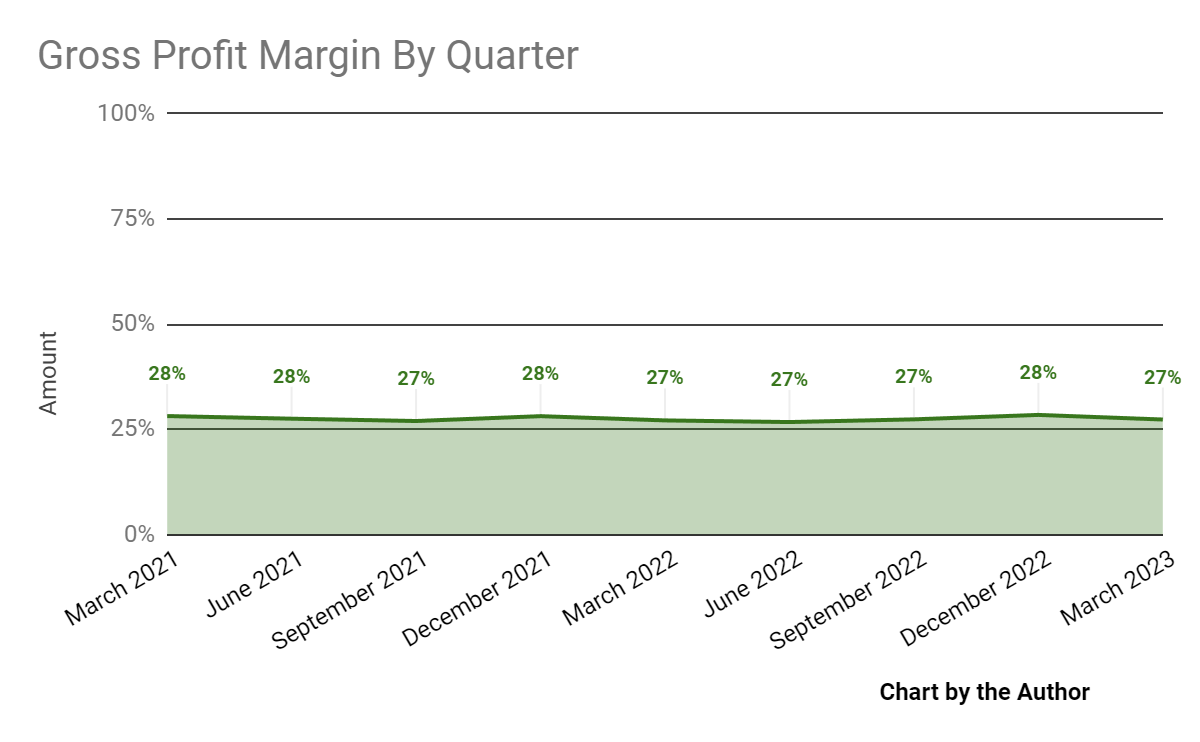

Gross profit margin by quarter has varied within a narrow range:

Gross Profit Margin (Seeking Alpha)

-

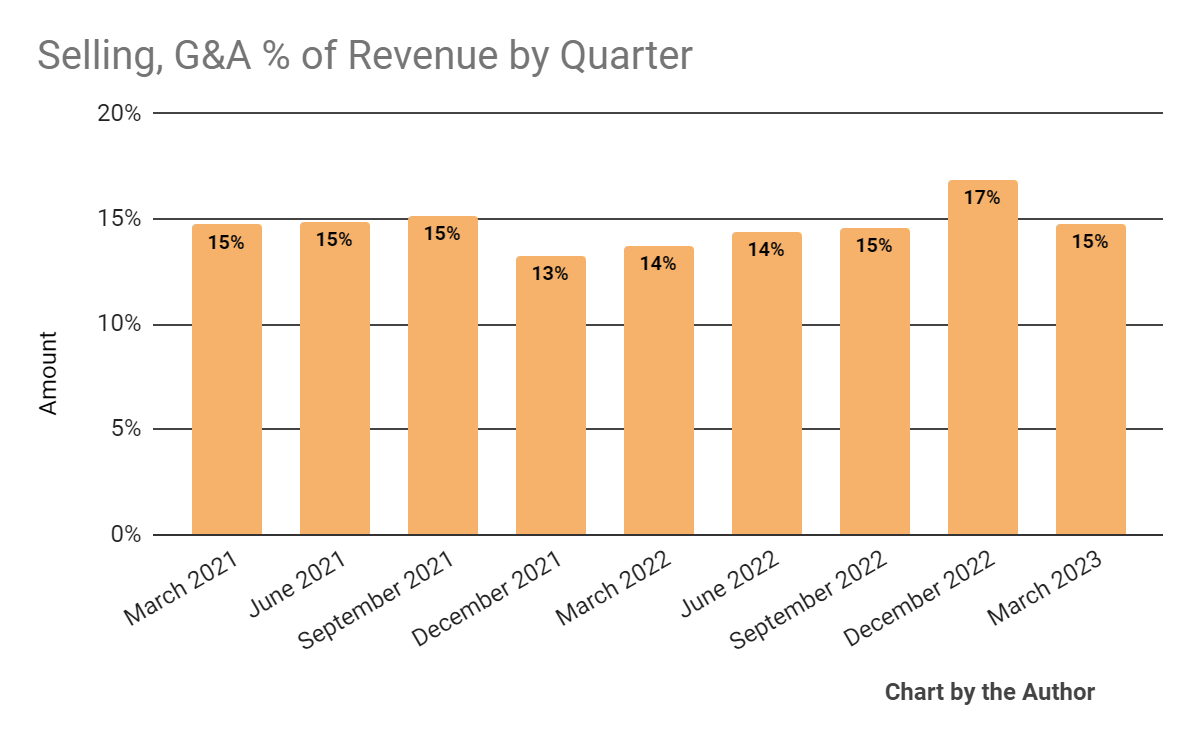

Selling, G&A expenses as a percentage of total revenue by quarter have produced no discernible trend:

Selling, G&A % Of Revenue (Seeking Alpha)

-

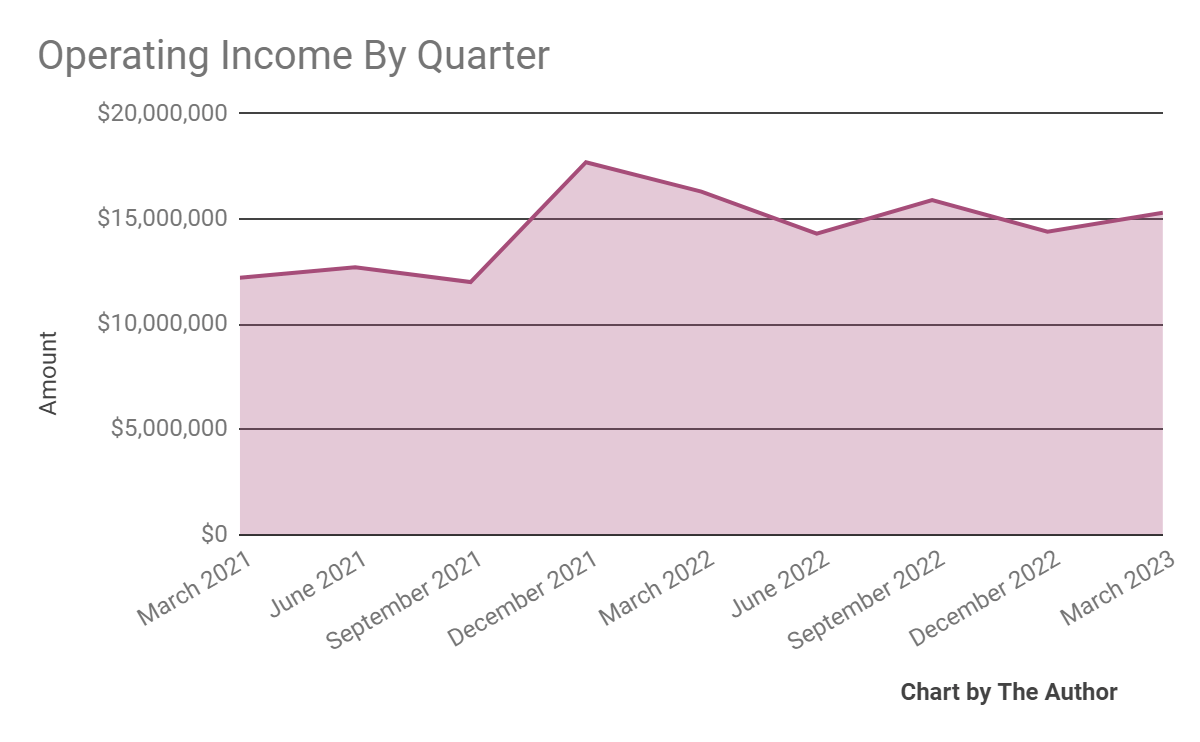

Operating income by quarter has trended slightly higher recently:

Operating Income (Seeking Alpha)

-

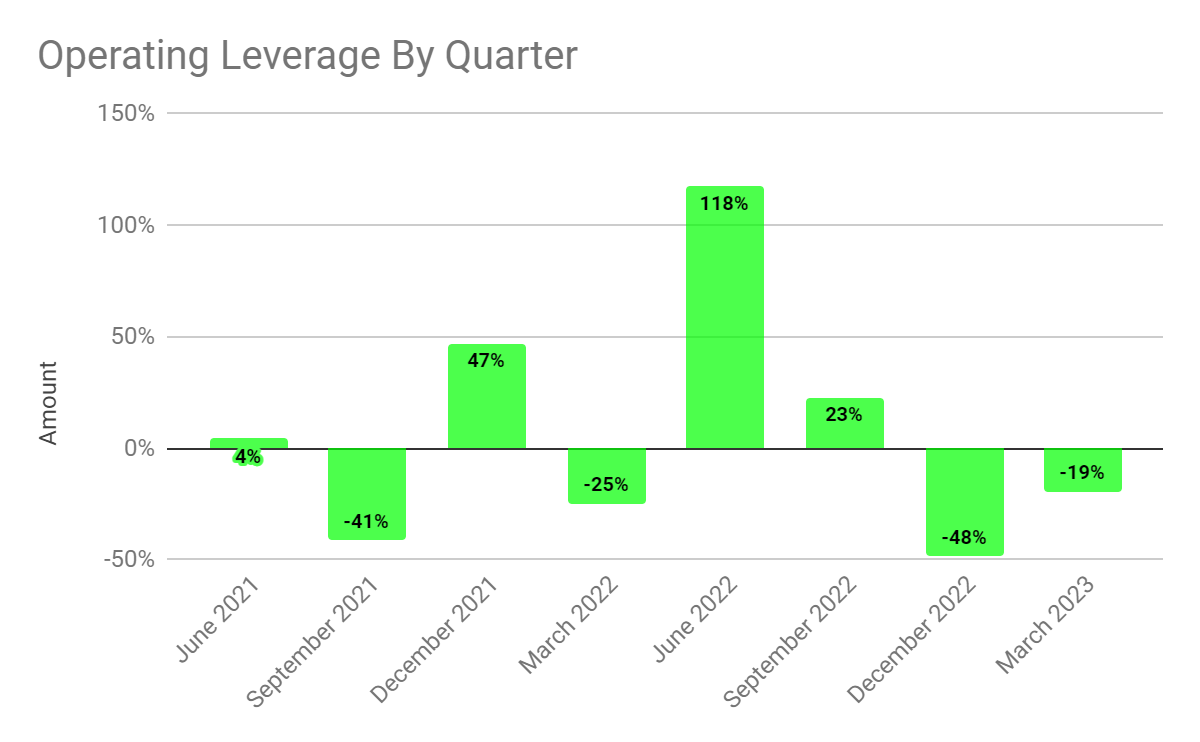

Operating leverage by quarter has turned negative in the last two quarters:

Operating Leverage (Seeking Alpha)

-

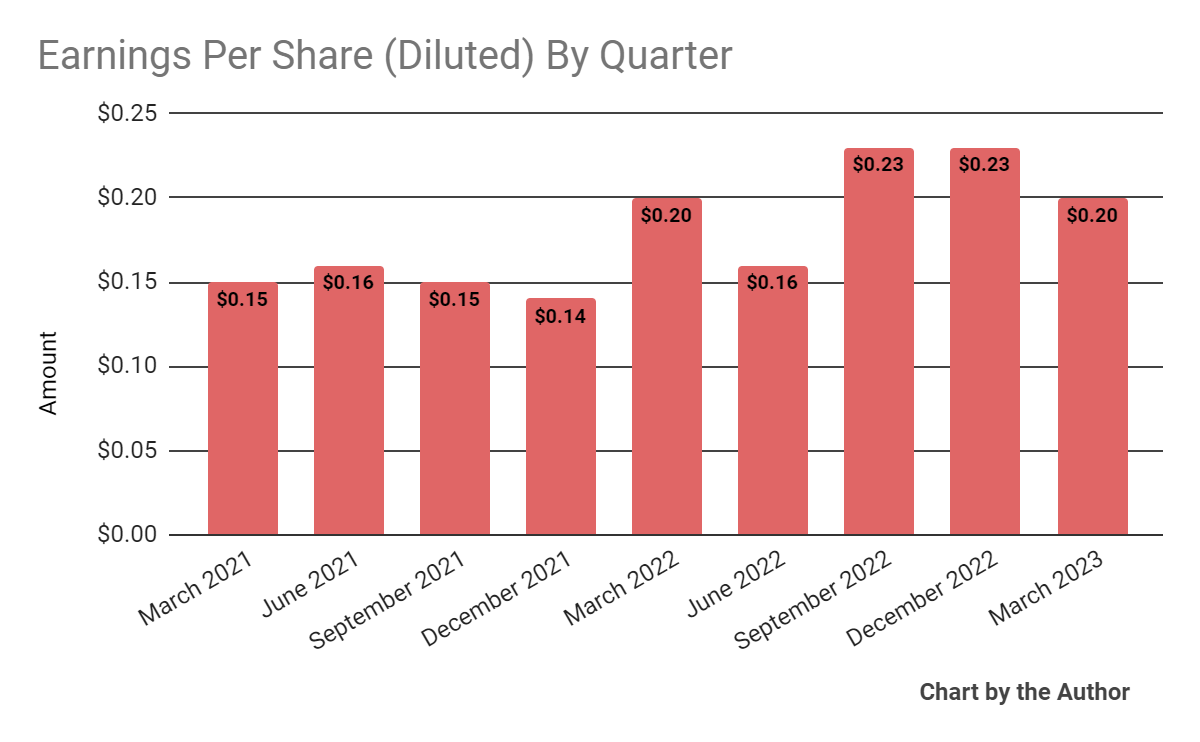

Earnings per share (Diluted) have trended higher in recent quarters:

Earnings Per Share (Seeking Alpha)

Total revenue by quarter has grown per the following chart:

{kind=link}

Total Revenue (Seeking Alpha)

Gross profit margin by quarter has varied within a narrow range:

{kind=link}

Gross Profit Margin (Seeking Alpha)

Selling, G&A expenses as a percentage of total revenue by quarter have produced no discernible trend:

{kind=link}

Selling, G&A % Of Revenue (Seeking Alpha)

Operating income by quarter has trended slightly higher recently:

{kind=link}

Operating Income (Seeking Alpha)

Operating leverage by quarter has turned negative in the last two quarters:

{kind=link}

Operating Leverage (Seeking Alpha)

Earnings per share (Diluted) have trended higher in recent quarters:

{kind=link}

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

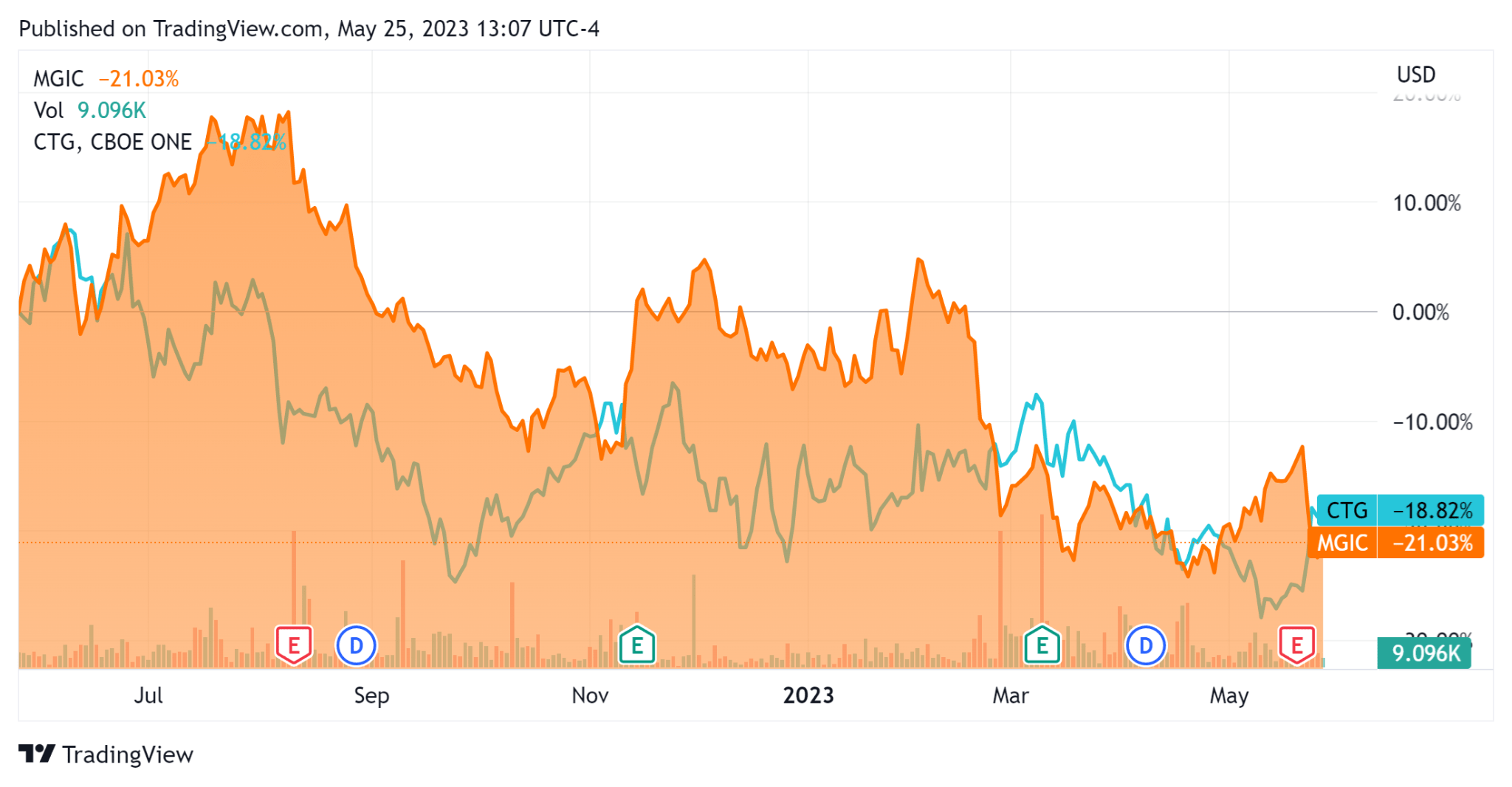

In the past 12 months, MGIC's stock price has fallen 21.03% vs. that of Computer Task Group (CTG)'s drop of 18.82%, as the chart indicates below:

52-Week Stock Price Comparison (Seeking Alpha)

{kind=link}

For the balance sheet, the firm ended the quarter with $106.4 million in cash, equivalents, and short-term investments and $67.4 million in total debt, of which $26.2 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was $58.1 million, of which capital expenditures accounted for $4.5 million. The company paid only $2.6 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Magic Software

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 1.2 |

| Enterprise Value / EBITDA |

| 9.4 |

| Price / Sales |

| 1.1 |

| Revenue Growth Rate |

| 11.5% |

| Net Income Margin |

| 7.2% |

| EBITDA % |

| 12.6% |

| Net Debt To Annual EBITDA |

| -0.5 |

| Market Capitalization |

| $670,120,000 |

| Enterprise Value |

| $672,840,000 |

| Operating Cash Flow |

| $62,600,000 |

(Source - Seeking Alpha)

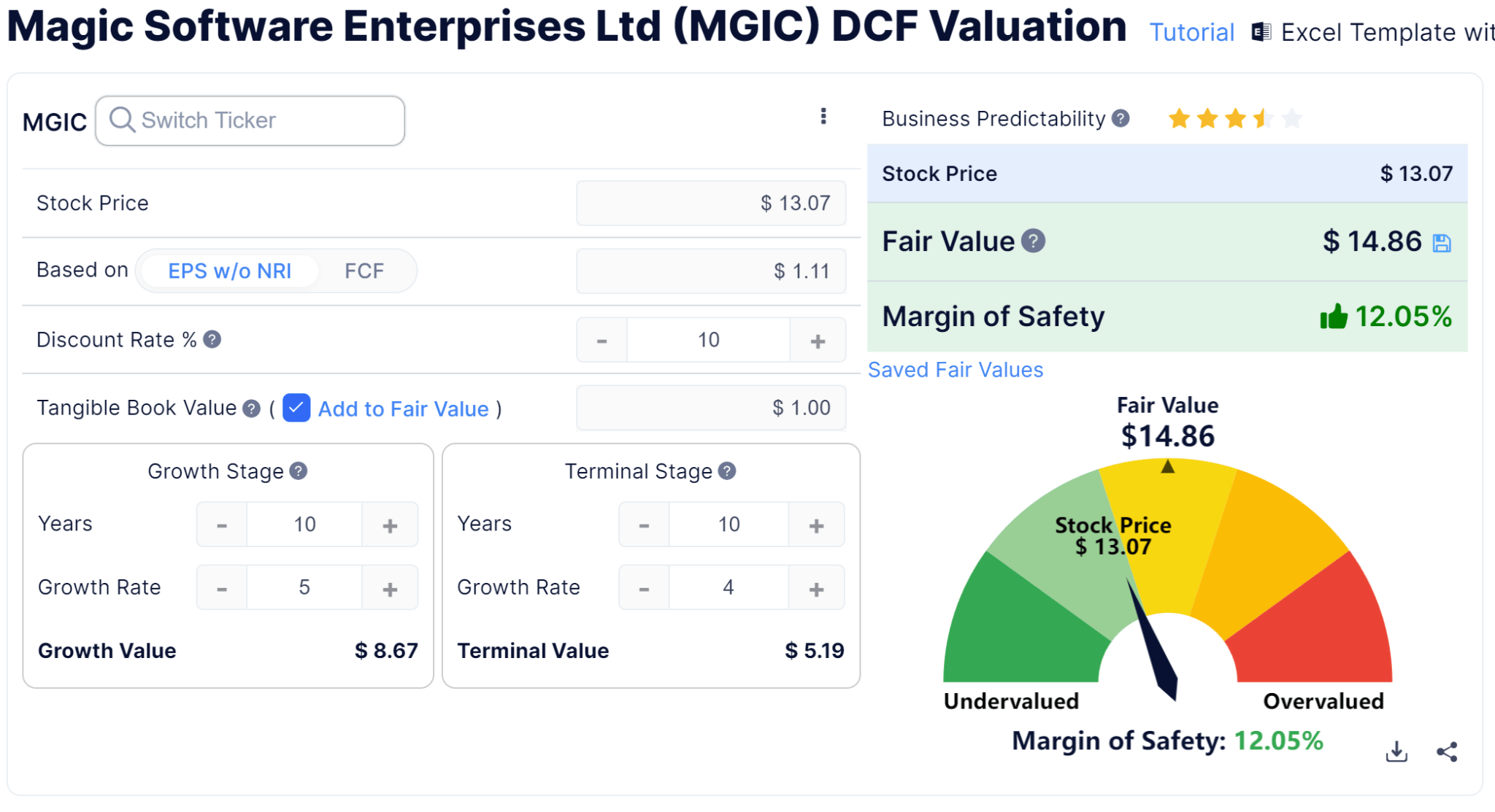

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm's projected growth and earnings:

Discounted Cash Flow Calculation - MGIC (GuruFocus)

{kind=link}

Assuming generous DCF parameters, the firm's shares would be valued at approximately $14.86 versus the current price of $13.07, indicating they are potentially currently undervalued, with the given earnings, growth, and discount rate assumptions of the DCF.

Commentary On Magic Software

In its last earnings call (Source - Seeking Alpha), covering Q1 2023's results, management highlighted its strategic focus on mature industries of healthcare, defense, and financial services.

This focus can help to mitigate slowdowns in the technology and telecom sectors, which can be subject to more cyclical forces and volatility.

Management reiterated its interest in an M&A element to its growth strategy, but is proceeding with caution.

Leadership did not disclose any company or customer retention rate metrics.

Total revenue for Q1 2023 rose 2.7% year-over-year and gross profit margin grew by 0.2 percentage points.

Selling, G&A expenses as a percentage of revenue increased one percentage point and operating income dropped 6.1% year-over-year.

Looking ahead, management guided to topline revenue growth in 2023 of 3.9%, which would be quite a significant drop from the nearly 18% growth that 2022 produced over 2021.

Regarding the company's financial position, the firm has ample liquidity and negative net debt to EBITDA while generating impressive free cash flow.

Regarding valuation, my discounted cash flow calculation suggests that the stock may be slightly undervalued at its current level, but that is only if the firm outperforms on its topline revenue growth estimate in 2023.

The primary risk to the company's outlook is the continued slowing macroeconomic environment, especially in the United States, which accounted for 51% of the company's revenue during the quarter.

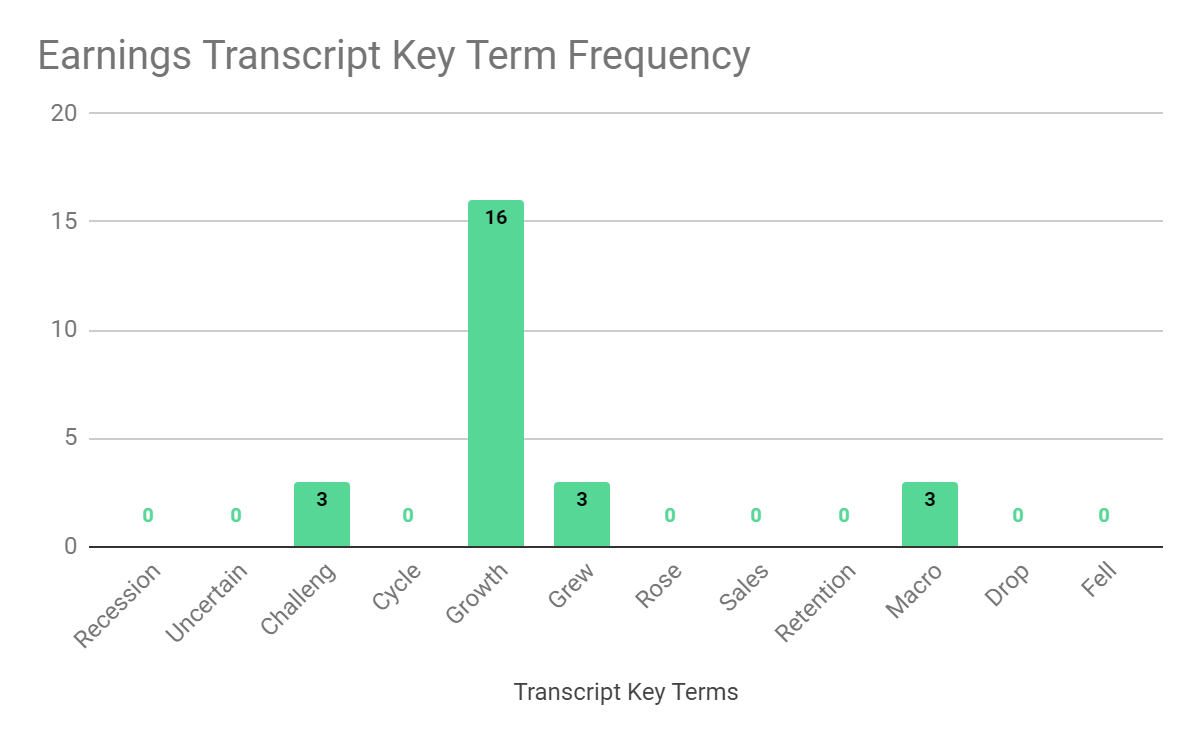

From management's most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below:

Earnings Transcript Key Term Frequency (Seeking Alpha)

{kind=link}

I'm most interested in the frequency of potentially negative terms, so management cited 'Challeng[es][ing]' three times and 'Macro' three times.

The negative terms refer to the difficult macroeconomic environment the firm's customers are experiencing in some respects.

A potential upside catalyst to the stock could include a lower cost of capital environment going forward, due to a potential pause in U.S. interest rate hikes if it occurs.

However, given management's tepid growth estimate for 2023 and the potential for further macroeconomic headwinds, I'm Neutral [Hold] on MGIC in the near term.

For further details see:

Magic Software Enterprises Sees Slower Growth In 2023