MGIC - Magic Software Should See Improved Cash Flow And Tailwinds From Labour Shortage

2023-03-10 16:13:45 ET

Summary

- Often subcontracted, which is a better alternative to lead contractors than hiring more people nowadays, positions them generally well in a strong labour market.

- Their constant currency growth does not show an alarming change in growth profile, owing to their idiosyncratic profile.

- Finally, their inorganic growth strategy should work better in a lower multiple environment, and if not they'll have more FCF for shareholders to benefit from.

- Valuation is not too bad at 14x PE either.

Magic Software (MGIC) continues to demonstrate strong results. They seem to be well positioned, not showing signs of a deceleration enough to change its profile from a growth issue. They are even growing their discretionary marketing investments, and the cash flow profile is improving, with no further jumps in receivables being witnessed that might have unnaturally supported growth. Moreover, they are tackling the labour situation well, and are even beneficiaries of it in a way that we'll detail further. While some pressure on sales velocity is being seen across the sector, their smaller idiosyncratic profile is playing in their favour.

Note on the Q4

{kind=link}

Highlights (Q4 2022 PR)

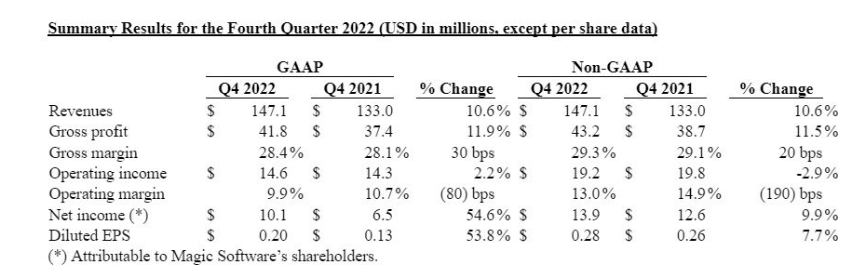

The 10.6% revenue growth was actually closer to 17% on a constant currency basis, and 70% of it was organic , meaning a little over 11% organic growth on a constant currency basis. North America lead the growth, explaining the differential caused by the FX considerations. While there's some deceleration from the headline 18% growth achieved in the FY, 10.6% headline is still very good accounting for currency hits.

Professional services grew in the mix, but primarily from the inclusion of new consultancy oriented acquired companies now consolidated into the results. Despite the GM pressures inherent from higher professional services in the mix interacting with labour inflation, labour tightness is also a tailwind for the company in terms of topline growth. Often MGIC is subcontracted as part of a general cloud migration or integration effort when working with Tier 1 companies, and in a tight labour market the economics of subcontracting to add to your manpower is a better option for the lead contractors in these projects than adding to their headcount. In general, subcontracting has a host of advantages related to the onus of employing people, and with payroll data still showing strength and secular growth in cloud markets remaining, this is something that plays in favour of MGIC.

GM actually improved YoY primarily owing to pricing effects and utilisation, where they managed to improve gross margins in professional services from 20% to 21%, but some bloat in the G&A put pressure on the net income margins. Primarily there was growth in marketing expenses that put pressure on the net income, and most of this growth was discretionary - the company is still scaling its marketing expense to some extent. However, 50% of the growth is coming from the inorganic addition of TGG marketing expenses, which was also responsible for the growth of professional services in the mix.

Bottom Line

Valuation is quite compelling at 14x. Since the growth is secular, an earnings yield at around 8% is pretty attractive since it will grow with secular topline growth. A demonstration of GM growth in professional services despite labour market tightness, where labour market tightness is also somewhat of a tailwind for their Tier 2 idiosyncratic profile, is another reason to be relatively confident in sustained growth.

Moreover, cash flows are trending in the right direction. 2021 saw a massive bloat in receivables that has seemed sustainable and shouldn't be repeated. Operating cash flows have therefore improved markedly. Moreover, the investing cash flow is being punished by a high item coming from the acquisition of TGG. Assuming no equally large M&A deals occur this year, FCF could grow from around $30 million to $50 million. With operating incomes currently running at $60 million, a return to normalcy in the FCFs highlights a cash generative profile.

However, we should highlight the receivables bloat. It was questionable last year, and has remained at these high levels, albeit not growing further to create growth. Still, the credit terms are quite loose. Revenues are around $560 million a year, and receivables are around $150 million, signaling quite loose credit terms with customers and pretty long receivable days around 100 days. While bad debt shouldn't become an issue considering the economic climate is relatively stable, although subject to some recessionary pressures, it is something that investors should consider. It possibly comes from more interaction with Tier 1 customers and operating in a subcontracted manner, where receivables have started to convert slower with this kind of business. But the sudden jump in 2022 leads us to believe that credit terms simply loosened and we still don't like that.

For further details see:

Magic Software Should See Improved Cash Flow And Tailwinds From Labour Shortage