MG:CC - Magna International: Growing EV Demand And Vehicle Production

2024-01-18 07:57:33 ET

Summary

- MG:CA's historical performance has demonstrated a strong recovery from the impact of COVID-19, as revenue has shown strong growth.

- Global light vehicle production is expected to remain strong, further supporting MG:CA's growth outlook.

- MG:CA joint venture with LG is expected to benefit from the accelerating growth in the EV market.

Magna International ( MG:CA ) is a company that specializes in designing, engineering, and manufacturing automotive parts. MG:CA's historical financial performance has demonstrated a strong recovery from the impact of COVID-19. During this time, margins have remained robust, with the exception of 2022, which saw a one-time impact related to its operations in Russia. An analysis of its 3Q23 results shows that sales continue to demonstrate strong growth, and margins have recovered to normalized levels.

Looking ahead, global light vehicle production is expected to remain strong, further bolstering MG:CA's future growth. Additionally, I anticipate that MG:CA's EV strategic initiatives will benefit from the accelerating growth in the EV market. Given its more favorable growth outlook compared to competitors and the potential for double-digit upside, I recommend a buy rating for MG:CA.

Historical Financial Performance

Over the last few years , MG:CA's past financial performance has shown robust recovery and growth from 2019 and 2020. In 2020 , its business was significantly impacted by COVID-19 as the demand for vehicles significantly dropped due to mandatory stay-at-home orders. In 2021 and 2022, revenue year-over-year growth rates have recovered to double-digit rates. The growth was mainly driven by higher global light vehicle production.

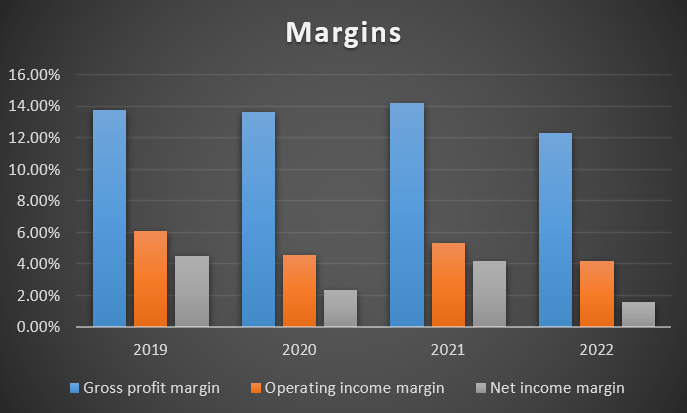

Author's Chart

In terms of profitability, I will be looking at its gross profit, operating income, and net income margin. Based on the chart, its margins contracted in 2022, and management attributed it to rising costs driven by inflation. The other driver for the contraction is caused by impairments related to its Russia operation as its operations in Russia remain substantially idle.

{kind=link}

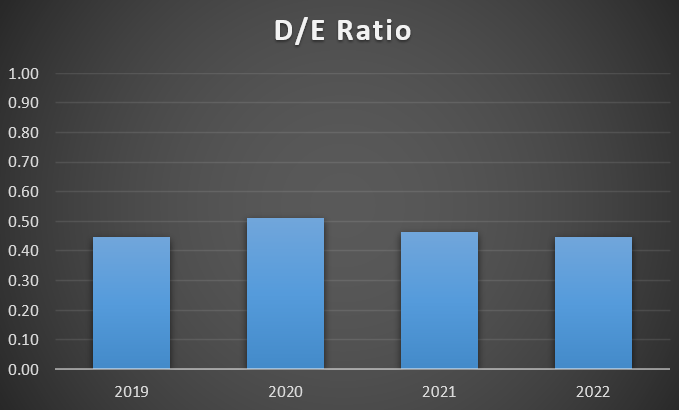

Moving onto its balance sheet, debt-to-equity [D/E] remained stable over the years. As a result of its prudent debt level, interest expense as a percentage of total revenue has been low and stable over the past four years. In 2022, interest expense as a percentage of total revenue reported was ~0.33%.

{kind=link}

Analysis of 3Q23 Earnings Results

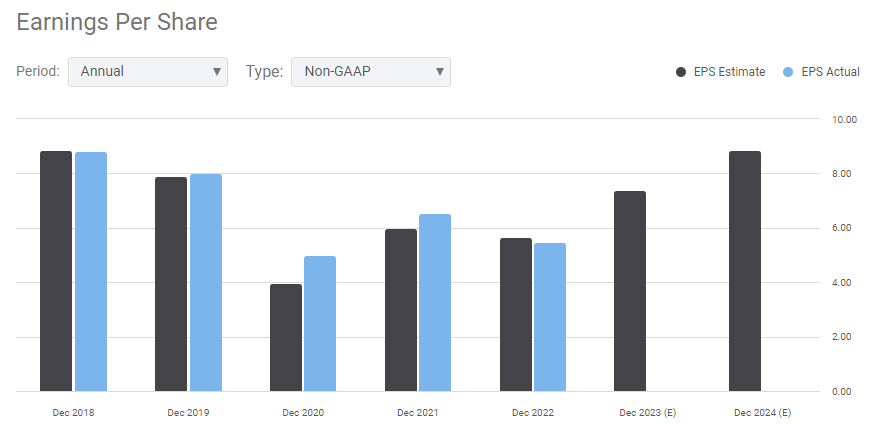

MG:CA reported strong 3Q23 results. Total sales grew 15% year-over-year, driven mainly by higher global production, its acquisition of Veoneer Active Safety in the previous quarter, and price increases to cover its higher production costs. During the quarter, the automobile sector was faced with the United Auto Workers strike. As a result, sales were partially offset by it. If we exclude this one-time event, which impacted sales by ~ $50 million, total sales growth for 3Q23 is even higher.

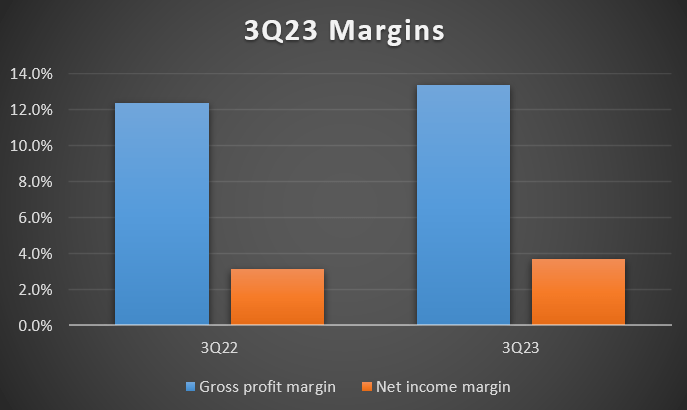

Moving onto profitability, its 3Q23 gross profit margin and net income margin have slightly improved vs. 3Q22. However, when compared to FY 2022's margins, the improvements are more significant. I believe the cooling inflation helped with its COGS and ultimately benefited its net income. In addition, in 2022, the margin compression was also caused by one-time impairment charges related to its Russia operation. Therefore, moving ahead, I anticipate its margins to remain robust.

{kind=link}

Strong Growth in Global Light Vehicle Production

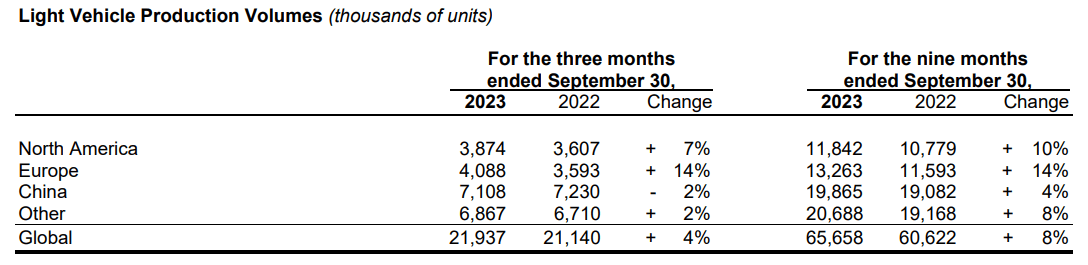

MG:CA's operating results are dependent on light vehicle production, mainly in North America, Europe, and China. It is dependent on the production level because it supplies systems and components to every major original equipment manufacturer [OEM].

Based on the following table, I am seeing strong growth in all regions except China for 3Q23, but on a 9-month basis, all the regions are growing with NA and Europe at double rates.

Overall, global light vehicle production for 3Q23 grew 4% year-over-year, mainly driven by improved supply chain conditions. In 2022, there was a significant disruption to the automotive industry caused by the semiconductor chip shortage. For 2023, the shortage has eased, and the growth in vehicle production is looking robust. Looking ahead, I anticipate that the strong growth in global light vehicle production in 2023 will bolster MG:CA's growth outlook.

{kind=link}

Accelerating Growth in EV

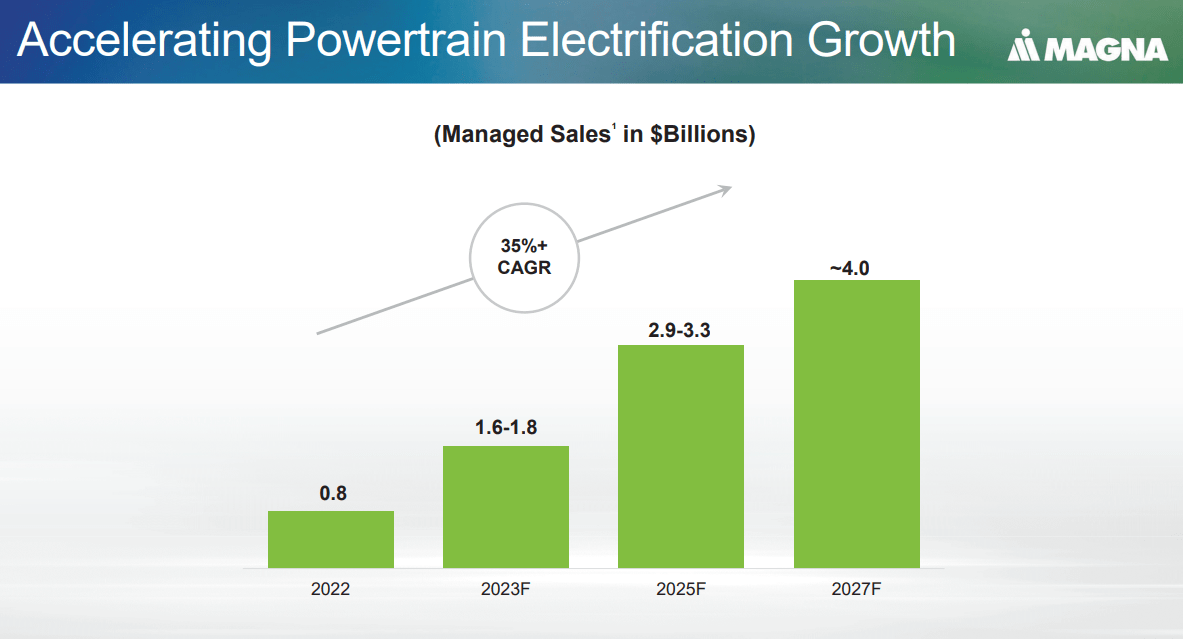

Based on the following graph , the EV powertrain is expected to grow until 2027. In 2022, it only accounts for ~$800 million of total sales, but by 2027, it is expected to reach ~$4 billion. This represents a CAGR of ~35% for the next three years.

{kind=link}

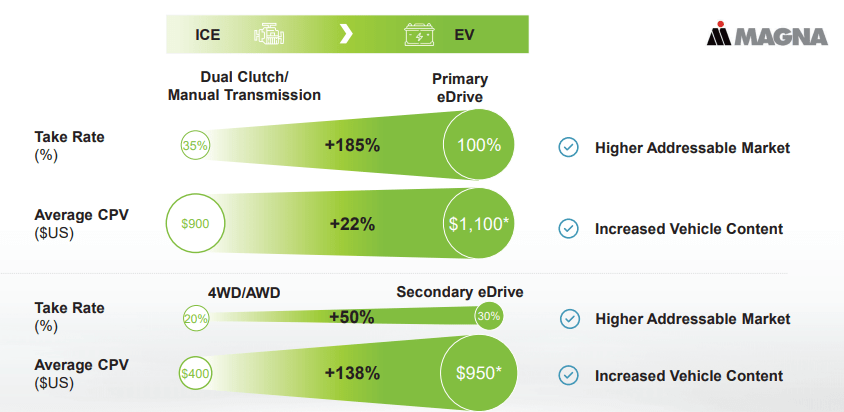

For primary eDrive in EVs, the average content per vehicle [CPV] is expected to be ~$1,100 vs. internal combustion engine [ICE] of $900, whereas for secondary eDrive, it is expected to be ~$950 vs. ICE's $400. In addition to the higher average CPV, the take rates in EV's for both powertrains are also much higher than the take rates in ICE. As such, as the EV market continues to grow, it provides the tailwind for MG:CA to grow as there is a growing addressable market and higher content opportunity.

{kind=link}

In 2021 , LG and MG:CA entered into an agreement to establish a joint venture [JV] called LG Magna e-Powertrain. This JV combines MG:CA's expertise in electric powertrain and automotive manufacturing with LG's experience in developing parts for electric motors. This LV has proven to be successful, as its growth has been accelerating over the years. In 2022, sales were ~$600 million, and it is expected to grow at 40% CAGR until 2025.

With the anticipated strong growth in powertrain electrification combined with the successful JV with LG and MG:CA's venture into electrification, I expect these tailwinds to drive its future revenue upward.

Comparable Valuation Model

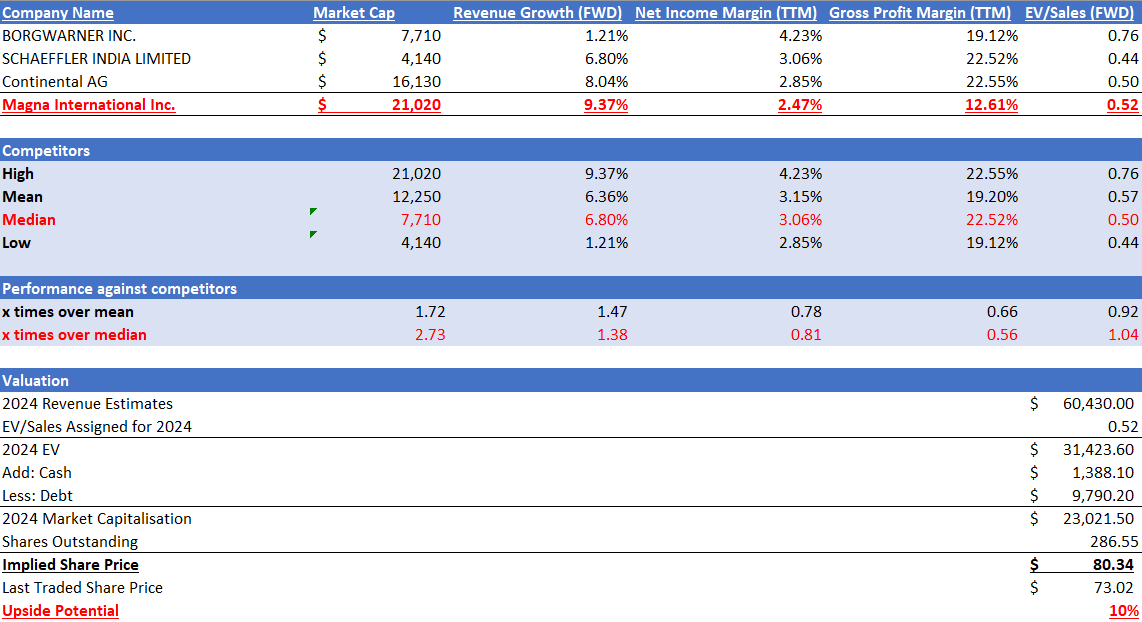

MG:CA operates in the automotive parts and equipment industry, and the competitors I have gathered operate in the same industry. In terms of size, MG:CA is significantly larger than its competitors' median. MG:CA has a market capitalization of ~$21 billion, while its competitors' median is ~$7.7 billion.

Despite its larger size, it outperformed its competitors in terms of forward revenue growth. MG:CA has a forward revenue growth rate of 9.37% vs. competitors' median of 6.80%, representing 1.38x over the median.

When it comes to profitability, MG:CA is slightly behind its competitors. It has a much lower gross profit margin of 12.61% vs. competitors' median of 22.52%. Despite its gross profit margin being almost half the median, MG:CA's net income margin TTM is not far behind that of its competitors. It has a net income margin TTM of 2.47% vs. the median of 3.06%.

In terms of valuation, MG:CA's forward EV/Sales ratio is mostly in line with its competitors' median. MG:CA's forward EV/Sales ratio is 0.52x, while the median is 0.50x. The reason forward EV/Sales ratio is picked as the valuation multiple is due to some of its competitors not having any forward P/E ratio, hence making P/E ratio not applicable.

The market estimates that MG:CA's revenue for 2023 is expected to reach $57.14 billion and $60.43 billion for 2024. Based on its financial strength and growth catalyst, as discussed above, it supports these estimates. In addition, the market revenue estimates are in line with management revenue guidance , further supporting their accuracy. By applying its current forward EV/Sales to its 2024 revenue estimates, my 2024 price target is $80.34, and this represents an upside potential of 10%.

Author's Valuation Model Seeking Alpha Seeking Alpha

{kind=link}

{kind=link}

{kind=link}

Risk

The main downside risk of buying MG:CA is related to the cyclical nature of the automotive industry. This industry is highly sensitive to economic downturns, which can lead to reduced demand for vehicles and consequently affect MG:CA, as it is a company that supplies automotive parts. Just a few days ago, US inflation of 3.4% for December 2023 was higher than the market estimate of 3.2%. This inflation data diminished the market's confidence in interest rate cuts and might cause macroeconomic uncertainties.

Conclusion

In conclusion, MG:CA has shown strong recovery and growth post-COVID-19, with revenue growing at double-digit rates. However, the net income margin contracted in 2022 due to one-time expenses related to its Russia operations, but I expect an improvement in margins in the upcoming quarters. The 3Q23 results are impressive, with revenue continuing to grow at double-digit rates and margins returning to 2021 levels.

Looking ahead, the strong growth in global light vehicle production and the expanding EV market are expected to bolster MG:CA's growth outlook, particularly benefiting its joint venture with LG.

Comparatively, MG:CA's forward revenue growth rate surpasses that of its competitors, and although its margin is slightly lower, the difference is minimal. Considering these growth catalysts and the potential for double-digit upside, I recommend a buy rating for MG:CA.

For further details see:

Magna International: Growing EV Demand And Vehicle Production