MGNI - Magnite Is A Recovery Candidate

2023-10-17 01:07:49 ET

Summary

- Magnite's stock has fallen due to a rough patch in the CTV and digital ad market, but it's well placed to benefit from a recovery in the market.

- The company is gaining market share and has finished integrating its acquisitions, allowing it to develop new solutions.

- A shift towards programmatic ads may hurt in the short term but will be beneficial in the long run, aided by new high-value services.

Magnite ( MGNI ) was a high-flying company whose stock reached $60+ on a wave of CTV enthusiasm and growth (much of it through acquisitions) but has now fallen back to earth as CTV and the digital ad market, in general, are going through a rough patch.

FinViz

Our optimism of 2022, which was predicated on CTV growth and integration benefits, whilst arguing any recession was already priced in, panned out only in part.

The recession hasn't materialized even if the digital ad market is going through a rough patch. The integration benefits have arrived with management expecting $100M+ in free cash flow this fiscal year.

The surprise has been the slowing of CTV growth. We didn't see that coming. Yet we think even that is priced in here and we see several reasons to be optimistic:

- The digital ad market will recover at some point.

- The company is gaining market share.

- The company is done digesting its acquisitions and integrating platforms and now has significant resources to develop new solutions.

- A shift towards programmatic ads hurt in the short-term but will be beneficial in the longer run, also with the help of new high-value services

- Management still guides for $100M+ in free cash flow this year.

Digital ad market

Management noticed softness in its managed service business, which is unfortunate as this is the business with the highest take rate. They argue that it's just an air pocket ( Q2CC ):

some of those campaigns appeared to be paused rather than completely taken off the table. We think that it's sort of, as our sales team described earlier, an air pocket for a few months here. And so we are comfortable with some recovery on the managed service front. And then I think the rest of the business, as Michael mentioned, from an ad spend share perspective, the business is actually very healthy

But we'll have to see about that. Growth is widely expected to be less buoyant compared to the pandemic heyday, but that's not surprising:

The B2B House

From Axios :

The slowdown in the ad market contributed to a massive sell-off across the media, entertainment and technology sectors last year. That resulted in a record number of layoffs and various cost-cutting measures at media and tech companies in 2022 and early 2023. Driving the news: Analysts are optimistic that advertising growth will improve in the second half of the year, with data showing the economy moving in the right direction.

- "We think the underlying tone is positive," Tim Nollen, Macquarie senior media tech analyst, wrote in an analyst note

- Nollen pointed to a newly-released second quarter GDP report that showed while consumer spending has slowed to +1.6%, business investment spending popped to +7.7%.

- "We have found this to be the most relevant leading indicator of ad spending historically," he added.

The last sentence also shows the precariousness of the optimism, a further slowdown in the economy could quickly sniff it out so we're not counting our chickens yet here, although it's likely to be the most important driver of the stock.

Market share and shift to programmatic

CTV ex-TAC (traffic acquisition cost) grew 8% y/y and DV+ ex-TAC grew 10% y/y, this isn't hugely above market growth at first sight. However, management noticed a significant trend in Q3 (Q2CC):

the largest and fastest-growing streaming players, the broadcasters, plus services and TV OEMs are all getting truly serious about programmatic and are taking share from smaller CTV publishers. We are seeing this shift manifest itself in our own partners, including Disney, Roku, Warner Brothers, Discovery, and Vizio who are moving more inventory toward programmatic transactions and away from traditional direct sold executions.

This is not revenue neutral (Q2CC our emphasis):

As all of those large sellers move direct-sold deals to publisher direct programmatic, they're becoming a bigger part of our ad spend mix but they are relying on services with lower take rates. What's not showing up in our financials is that we're growing market share at a far greater rate than our revenue would suggest .

Nevertheless, management sees a huge opportunity here longer term as it is winning these top-tier clients and with new higher-value SSP (sell-side platform) services when growth returns the rates will improve and this development will express itself in the financials.

New Services

What are these new higher-value SSP services? Management described:

- SpringServe

- ClearLine

- Magnite Access

- After the close of Q2, we can add the new Demand Manager features

That management mentioned SpringServe surprised us a little as this was an acquisition dating back to 2021, but management argues that it continues to win new ad-serving clients, introducing new formats and direct private marketplaces between agencies and premium publishers.

ClearLine was launched in April this year, it's a self-service direct video buying solution for ad agencies. Magnite Access is (Q2CC):

a suite of omnichannel audience data and identity products that make it easier for media owners and they are having advertising partners to maximize the value of their data assets, including a DMP, a data storefront, a secure solution enabling sellers and buyers to match datasets and more.

It's still partly in beta. Management argued we shouldn't expect much in the way of material financials from these yet, but in time they will produce that.

Cash flow

We think investors are to some extent overlooking the following:

Management projects $100M+ in free cash flow this year which on an expected revenue of $546.4M is a very healthy 18.3% free cash flow margin.

This is during macro headwinds (the TTM figure is even higher, as readers might have noted in the graph above) and with the seasonally stronger H2 still to come.

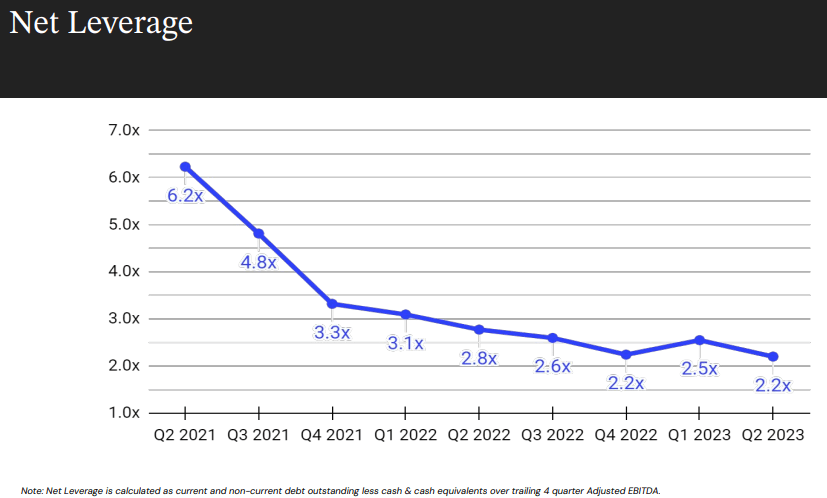

Cash flow confers options and should be cherished in times of high financing cost. One of the options the company is choosing is to deleverage. The company retired $40M of outstanding notes for $34M in cash resulting in a discount of 15% with $310M of notes left.

Over $90M or 23% of the notes have already been retired, and the total debt of the company is $638.6M with net debt at $372.3M.

There is a new $100M buyback fund in place for both the notes and stock, and management believes that net leverage, which was down to 2.2x from 2.5x at the end of Q1, will be below 2x at yearend.

{kind=link}

Apart from the considerable cash flow, cash was $266M at the end of Q2, an increase from $237M at the end of Q1.

Finances

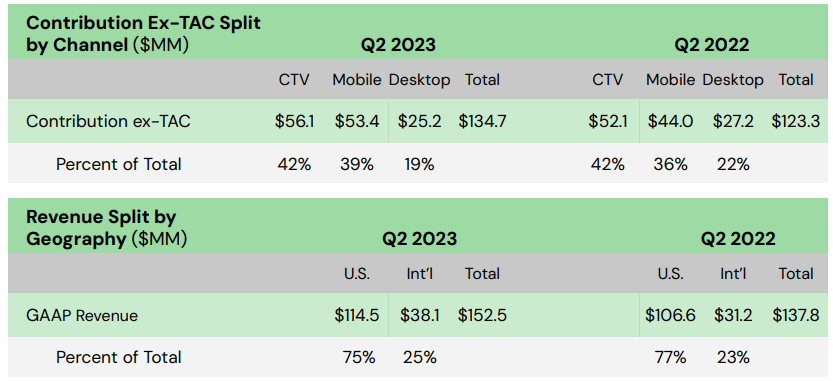

BY category and geography:

{kind=link}

A few notable developments that impacted financials:

- The ex-TAC contribution mix for Q2 was 42% CTV, 39% mobile, and 19% desktop.

- The MediaMath bankruptcy resulted in a one-off $4.5M bad debt charge.

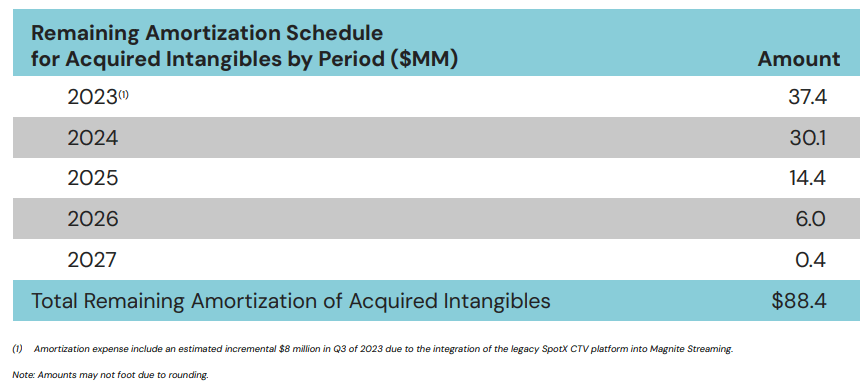

- The company's GAAP figures are hugely impacted by the $53M amortization expense (hence the large GAAP net loss).

- The company is basically done integrating various platforms and this will free up a huge amount of people and resources for developing new products.

{kind=link}

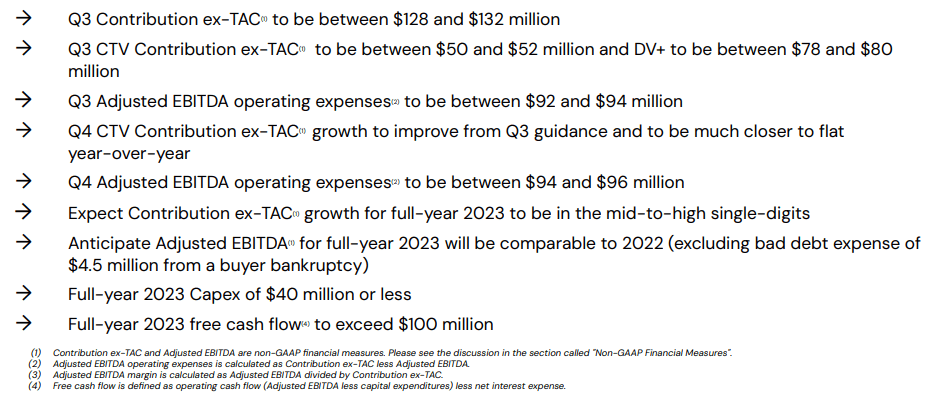

Guidance

{kind=link}

H2 has difficult comps due to high political spending in Q4 last year.

Valuation

There are 146M shares fully diluted, at $7.5 per share this amounts to a market cap of $1.09B and an EV of $1.47B, which produces an EV/S of 2.7x. With FY23 EPS estimated at $0.52 rising to $0.77 next year, the shares are cheap on an earnings basis.

Conclusion

There is quite a bit to like:

- The company is well-positioned to benefit from a recovery in the digital ad market, whenever that arrives.

- The company is gaining market share.

- The company is done digesting its acquisitions and integrating platforms and now has significant resources to develop new solutions, a few of these are already emerging.

- A shift towards programmatic ads hurt in the short-term but will be beneficial in the longer run, also with the help of new high-value services.

- Management guides for $100M+ in free cash flow this year and on a TTM basis, the company is actually already exceeding this by some margin, enabling it to reduce leverage.

- The shares are surprisingly cheap.

There are some concerns as well:

- The streaming revolution might have topped out, although the same doesn't necessarily apply to the ad market on streaming, which we think will continue to grow for quite some time.

- We don't know when the macro headwinds will subside and while it lasts the decrease in managed service and increase in programmatic has a negative effect on take rates and hence financials.

The upshot: There are good reasons to expect a significant rally in the shares when the clouds lift over the digital ad market, but it's very difficult to time this to perfection. One could accumulate some shares on dips and not expect too much near-time, even if the shares could take off at any moment.

For further details see:

Magnite Is A Recovery Candidate