MGY - Magnolia Oil & Gas Continues To Grow Production With A Low Reinvestment Rate

2023-11-17 16:46:29 ET

Summary

- Magnolia Oil & Gas Corporation expects to deliver high-single digits production growth in 2023 and 2024, with a reinvestment rate of under 50%.

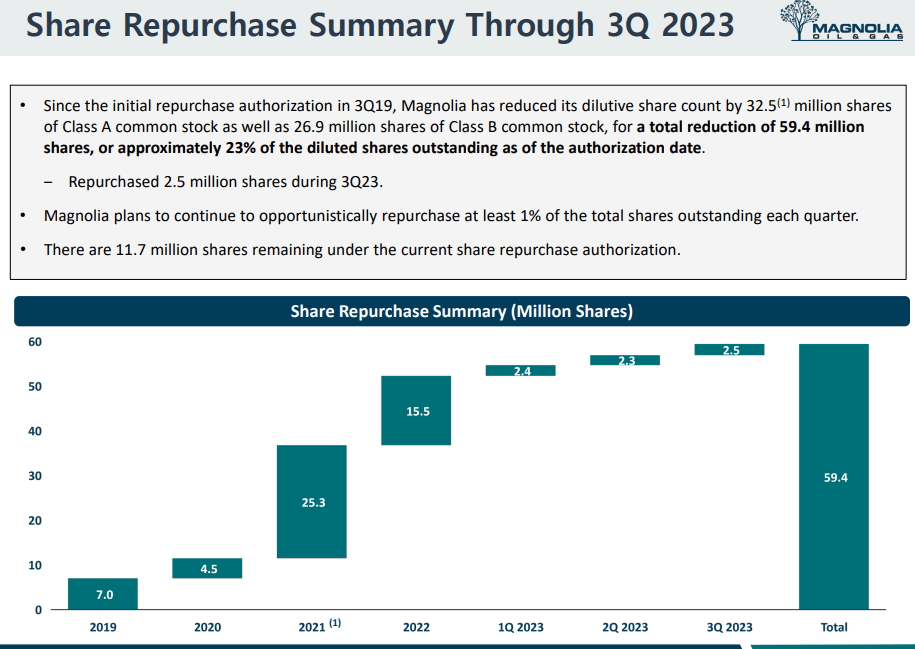

- This gives it funds to continue share repurchases. It has repurchased around 48 million shares since the start of 2021.

- Magnolia's oil cut has been decreasing with its focus on its high-return Giddings asset.

- It recently acquired oilier Giddings assets, though, which should help boost its oil cut back up a couple percent.

Magnolia Oil & Gas Corporation ( MGY ) has been efficiently growing its production and now expects 8% production growth (not including its recent Giddings acquisition ) in 2023, with a 6% to 7% decrease in capital expenditures compared to 2022.

Including the impact of the acquisition, Magnolia also expects to deliver high-single digits production growth (for both total production and oil production) in 2024, with a reinvestment rate of less than 50%.

This will give Magnolia the ability to continue significant share repurchases while also having the option to increase its dividend from its current $0.115 per share quarterly rate.

I am keeping my estimated value for Magnolia at $26 to $27 per share at long-term $75 WTI oil and $3.75 NYMEX gas for now. Magnolia's capital efficiency has improved, with Giddings well costs (per foot) down 15% since the beginning of 2023. Magnolia's oil cut has trended downwards though as a result of its focus on Giddings (which typically still provides superior returns to its Karnes acreage). Near-term prices for NGLs and natural gas are relatively weak though, and below my longer-term expectations.

Q3 2023 Results

Magnolia reported 82,651 BOEPD (40% oil) in Q3 2023 production, which was a 1% increase in total production, but a 4% decrease in daily oil production compared to the 81,881 BOEPD (42% oil) that it reported in Q2 2023.

Magnolia previously mentioned that it expected total production to be around the same in Q3 2023 as it was in Q2 2023, so its overall production did a bit better than that. Magnolia's oil production has taken a hit from its focus on its Giddings asset, which accounted for around 75% of Magnolia's total production in Q3 2023. Magnolia's Giddings production was only 34% oil in Q3 2023, but it has been prioritizing development there over Karnes since Giddings provides better returns for the company.

Magnolia indicated that its D,C&F cost per foot at Giddings has gone down by 15% since the start of 2023, and this has allowed it to grow total production (albeit with a lower oil cut) with a relatively low reinvestment rate. Magnolia reported $239 million in adjusted EBITDAX in Q3 2023, while its D&C capex was 44% of adjusted EBITDAX at $104.3 million.

Giddings Acquisition

Shortly after I last looked at Magnolia in early September, it announced a $300 million bolt-on Giddings acquisition. Magnolia indicated that after purchase price adjustments it expected to pay $260 million in cash. There is also another $40 million in contingent cash consideration potentially due by December 2025 depending on commodity prices.

The acquisition involves 48,000 net acres in Giddings. Magnolia expects production to be around 5,000 BOEPD (70+% oil) at closing in Q4 2023. This is significantly oilier than Magnolia's 34% oil cut for its Giddings production in Q3 2023. This acquisition may boost Magnolia's oil cut in Giddings up to around 37%.

Magnolia also mentioned that the price involved a 2.9x multiple to estimated 2024 EBITDA, with a free cash flow yield of above 20%. This was based on strip prices at the time, which would have been around $80 WTI oil.

At the current strip of $75 WTI oil (CL1:COM) instead for 2024, the estimated multiple would be closer to 3.1x 2024 EBITDA with a free cash flow yield of approximately 19%. This acquisition is expected to close around the end of November.

Potential 2024 Outlook

Based on Magnolia's comments , I am modeling its 2024 production at around 90,000 BOEPD, including 37,300 barrels per day in oil production. This is near double-digits production growth compared to 2023, although production growth would be 4% to 5% without the Giddings acquisition.

At current 2024 strip of $75 WTI oil and $3.15 NYMEX gas, Magnolia may be able to generate $1.335 billion in oil and gas revenues.

| Type |

| Barrels/Mcf |

| $ Per Barrel/Mcf |

| $ Million |

| Oil |

| 13,614,500 |

| $73.50 |

| $1,001 |

| NGLs |

| 9,136,862 |

| $20.00 |

| $183 |

| Gas |

| 60,591,825 |

| $2.50 |

| $151 |

| Total Revenues |

| $1,335 |

I've assumed a $475 million capex budget for Magnolia in 2024, which would be a reinvestment rate of under 50%. This may be a conservative estimate of Magnolia's 2024 capex, since it has made significant progress in improving capital efficiency and may be able to deliver high-single digits growth with a lower budget.

| $ Million |

| Lease Operating |

| $160 |

| Gathering, Transportation and Processing |

| $46 |

| Taxes Other Than Income |

| $73 |

| Cash G&A |

| $70 |

| Net Cash Interest |

| $0 |

| Capex |

| $475 |

| Cash Income Taxes |

| $55 |

| Total |

| $879 |

This results in a projection of $456 million in free cash flow for Magnolia in 2024 after cash income taxes, or around $2.20 per share based on its expected fully diluted share count for Q4 2023.

{kind=link}

Magnolia has been diligently reducing its share count, so much of its free cash flow will likely go towards share repurchases, while it also has room to increase its dividend again.

Conclusion

Magnolia has been able to grow production with a reinvestment rate of under 50%. In Q3 2023, it reported a reinvestment rate of 44% and I project its 2024 reinvestment rate to be under 50% at current strip prices as well.

This gives Magnolia plenty of funds for share repurchases, and it has effectively repurchased around 48 million shares since the start of 2021. Magnolia also appears capable of increasing its dividend while continuing its current rate of share repurchases.

Magnolia's estimated value is between $26 to $27 per share at long-term $75 WTI oil and $3.75 NYMEX gas. It should be able to reduce its fully diluted share count below 200 million shares by mid-to-late 2024.

For further details see:

Magnolia Oil & Gas Continues To Grow Production With A Low Reinvestment Rate