MGY - Magnolia Oil & Gas Has A New Sheriff In Town

2023-08-04 18:20:52 ET

Summary

- The Eagle Ford strategy looks solid for Magnolia Oil & Gas Corporation despite issues.

- The Eagle Ford location often has profitability comparable to the Permian without the takeaway issues that often develop in the Permian.

- The Giddings area holdings are the focus of future upside potential.

- The new CEO needs to prove his effectiveness over the next few years.

- The conservative balance sheet lowers financial risk tremendously.

Magnolia Oil & Gas Corporation (MGY) is an oil and gas producer that is located in the Eagle Ford of Texas. The Eagle Ford often has comparable profitability to the far more advertised Permian. But the issues of the Permian caused by the "mad rush" of companies to participate in the Permian is absent in the Eagle Ford. That means that takeaway issue of the Permian that often cause higher transportation costs combined with price discounting are absent in the Eagle Ford. When it comes to actual execution, the Eagle Ford often compares favorably to a lot of Permian producers due to those issues and more.

Back in September 2022, the company announced the passing of the former Chairman, Steven Chazen. Oftentimes, the loss of a major officer in a small company can usher in a period of uncertainty. But it does appear that the company has the people in place to execute the original vision for the company.

The new President and CEO, Christopher Stavros, now has been in the position for nearly one year. He has a finance background as well as analysis prior to working for Magnolia. The next few years should demonstrate his leadership and vision skills (or lack thereof).

Acreage

Management began with acreage in a well-known part of the Eagle Ford and then acquired a sizable position in a more speculative play that is emerging as a future production area. The result is that there is more than enough acreage to keep this management busy for a long time to come.

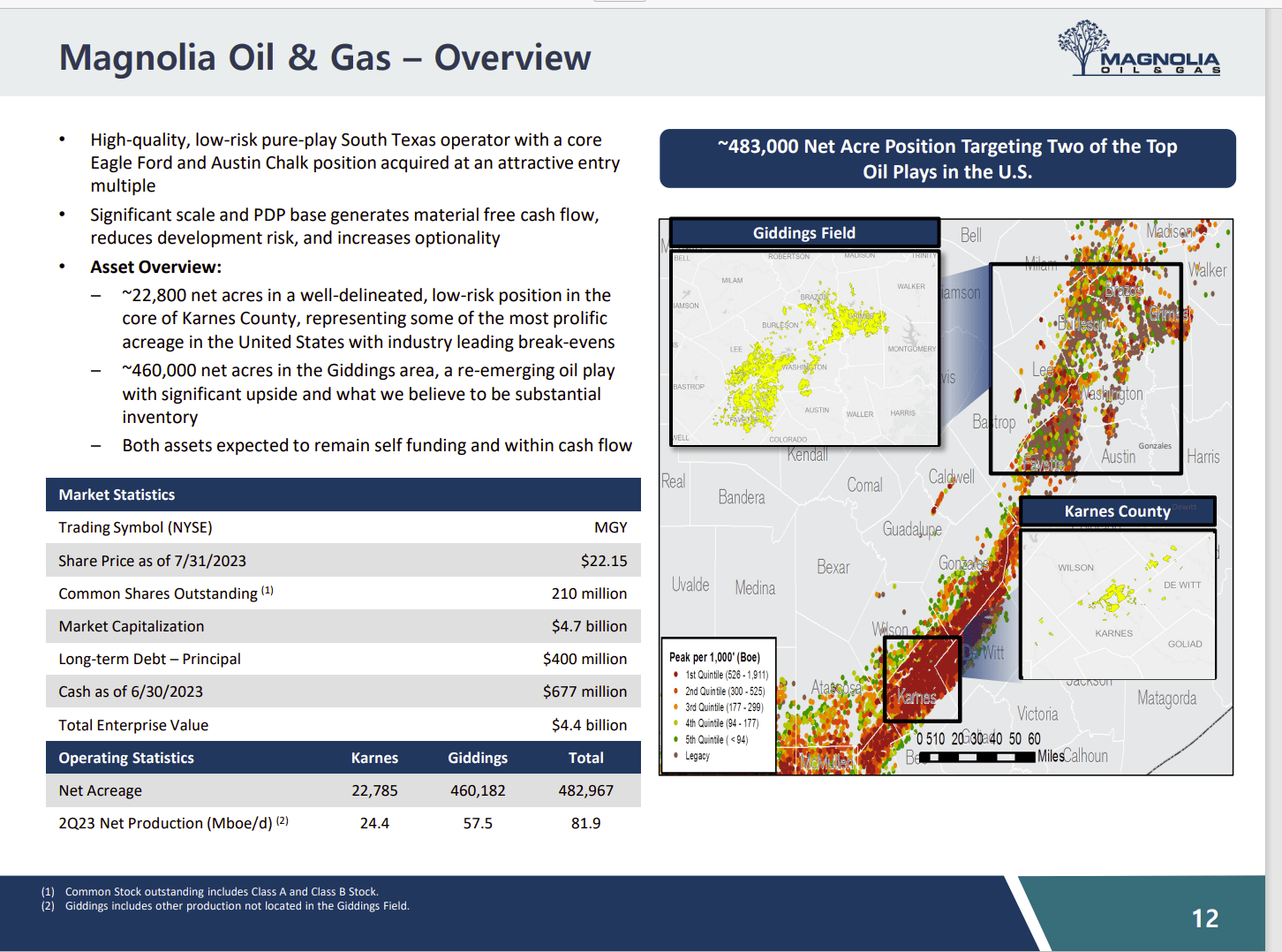

Magnolia Oil & Gas Lease Position In The Eagle Ford (Magnolia Oil & Gas Earnings Slide Presentation Second Quarter 2023)

{kind=link}

Management has a relatively "sure thing," if that is possible in the upstream business with the Karnes County acreage. That acreage should provide relatively reliable (superior) results and cash flow needed to help with the larger acreage position.

The larger acreage position was likely made possible due to continuing technology advances sweeping the upstream business. That re-emerging part in the slide is a critical statement because that happens a lot in the upstream business. Right about the time an investor is sure that a play is "over with," along comes some new technology that revitalizes the play.

Therefore, the acreage position and the company itself are likely to become more valuable over time if management is correct.

Finances

Management keeps a lot of flexibility on the balance sheet by maintaining a negative net debt position. In theory, management could spend the cash portion of that position and still have a low debt ratio that would maintain considerable financial flexibility.

But the finances are in place in case a bargain become available or should management decide to grow production faster than is the case currently.

The upstream business has very low visibility. So, it is very hard to fault management for taking a conservative position (financially). That cash and the bank line could be very handy during the cyclical downturns that occur periodically in this industry.

Management has also repurchased stock from the periodic secondary offerings by large shareholders. This helps to offset the effect of more publicly available stock in the market.

Results

Magnolia is one of the higher valued companies that I follow. But the lease position is one of the best, and it shows in both cash flow and free cash flow as well as earnings.

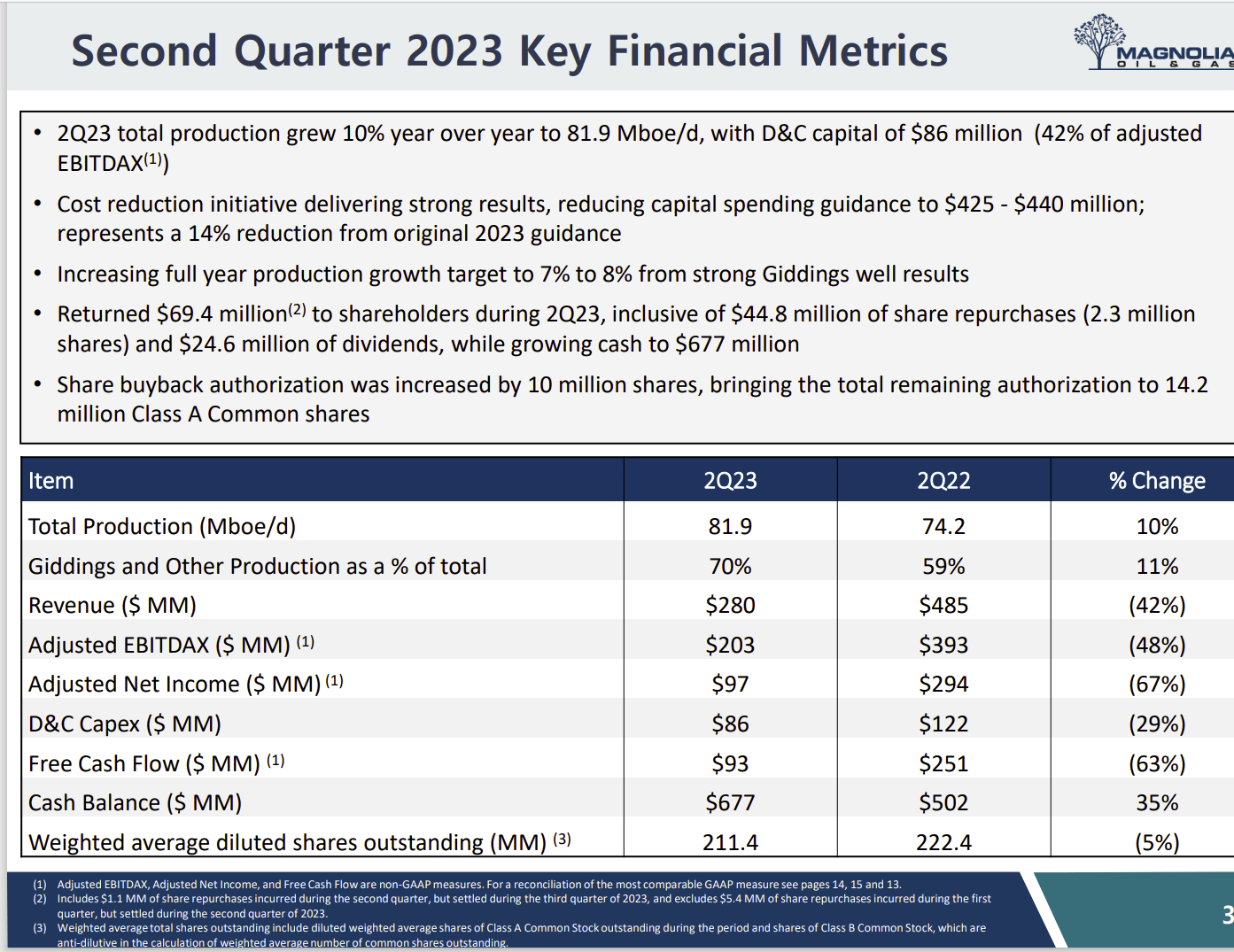

Magnolia Oil & Gas Second Quarter 2023, Operating Results (Magnolia Oil & Gas Earnings Conference Call Slides Second Quarter 2023)

{kind=link}

Management has clearly been building the cash balance, which has increased significantly since the previous fiscal year. A dividend has been initiated. But the emphasis here is likely to remain on growth. Therefore, income investors probably need to look elsewhere. This is a company that is likely to be built to be sold at the right price. The main objective here will therefore be capital appreciation.

The Eagle Ford has low enough costs that production growth can continue under some very hostile industry conditions. The negative net debt position would also allow for such a strategy. The advantage of growing during downturns is that service costs are often much cheaper. Therefore, the returns on wells drilled (that take advantage of higher recovery prices) is often higher.

More importantly the cyclical growth story will result in higher earnings during the recovery and a more substantial performance when prices decline. The low breakeven points of Eagle Ford wells combined with the negative net debt should allow for profits when many in the industry are losing money.

Key Takeaways

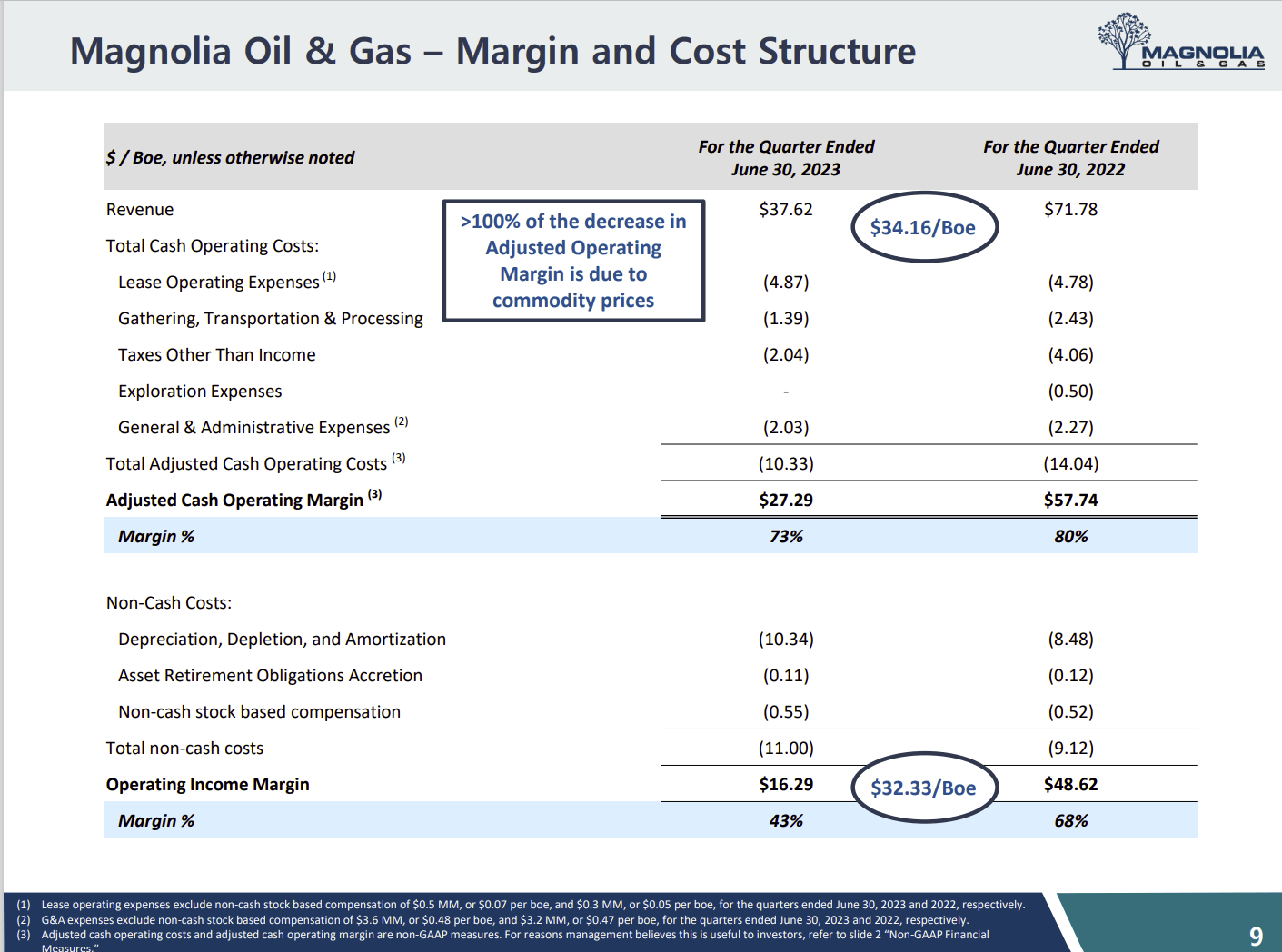

At current prices, this company has some of the best margins in the business.

Magnolia Oil And Gas Per Barrel Costs Summary (Magnolia Oil & Gas Earnings Conference Call Slides Second Quarter 2023)

{kind=link}

As shown above, Magnolia has lease operating cash costs that are closer to a natural gas producer combined with the more valuable income stream of an oil producer. That is a huge competitive advantage in the industry and one that is likely to last for years to come.

Also note that the depreciation cost is relatively cheap as well. That depreciation cost can run as high as $20 per barrel in some of the companies I follow. Therefore, the well drilling and completion costs are industry leading on a per barrel basis.

Even with oil prices down substantially from a year ago, the company still has extremely wide margins. The corporate costs appear to be low enough that very profitable wells are going to mean a very profitable company even at lower prices than is the case currently.

Summary

Magnolia Oil & Gas Corporation management has to prove itself. The previous chairman left some big shoes to fill, as he was a known entity in the industry. But it appears he left a company in very good shape with a superior strategy behind.

For those investors who can tolerate a little more management uncertainty (until this management has a track record), Magnolia Oil & Gas Corporation may be a consideration.

In the meantime, the Eagle Ford location, combined with the above average profitability (as shown by the wide margins), augur well for the future. The conservative balance sheet takes a lot of the small company upstream risk "off the table."

For me the company is a strong buy (but above average risk) for those that consider small companies based upon the strong balance sheet and the Eagle Ford location (not to mention the great financial results). But Magnolia Oil & Gas Corporation is not for everyone, as this is primarily a growth story.

For further details see:

Magnolia Oil & Gas Has A New Sheriff In Town