VICI - Make REIT Hay While The Sun Is Shining

2023-10-25 07:00:00 ET

Summary

- REITs have experienced a significant decline in share prices, but there's an opportunity for value investors to take advantage of current market conditions.

- The potential for the Federal Reserve to stop hiking interest rates and for a positive economic recovery create a favorable environment for REITs.

- Three recommended REITs to consider are VICI Properties, Alexandria Real Estate, and American Tower, which offer strong fundamentals and potential for growth.

I’m sure you know the saying, “Make hay while the sun shines.” It’s a common English proverb that advises listeners to take advantage of opportunities when they arise.

This makes sense from a farming perspective (or, really, any other one), which the saying is obviously based on. Gathering crops is a lot easier to do in good weather, after all. And there’s only so much good weather you can expect in a given season.

In other words, ideal opportunities only come around every so often.

Another way of saying it is “carpe diem,” which translates from Latin to mean “seize the day.” But no matter the turn of phrase, I’m all about taking advantage of real estate investment trusts.

Now most readers will say that the sun isn’t shining on REITs right now. And they’d be right.

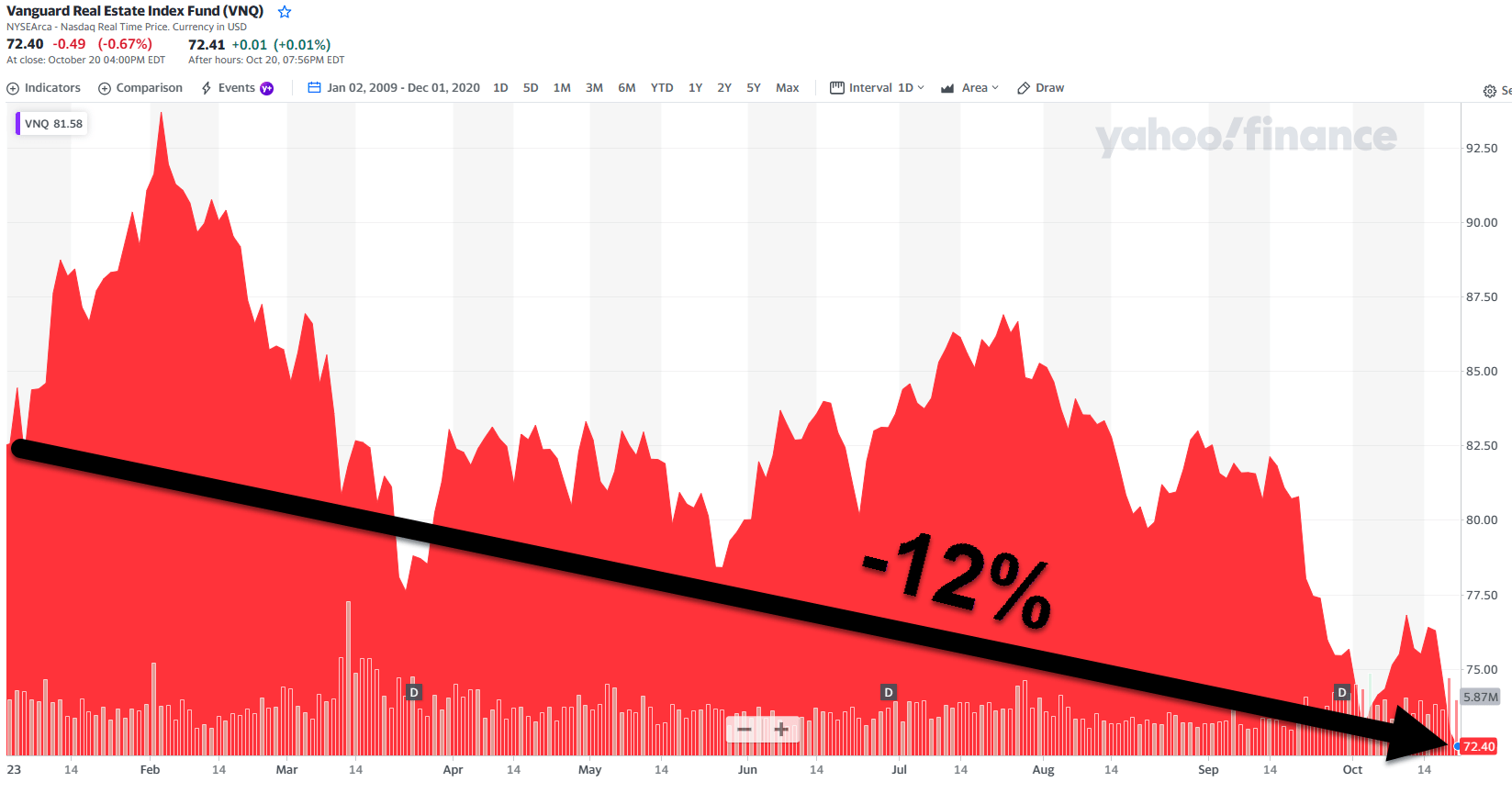

Shares in the Vanguard Real Estate Index Fund ETF Shares ( VNQ ) are down by about 12% this year:

{kind=link}

Yahoo Finance

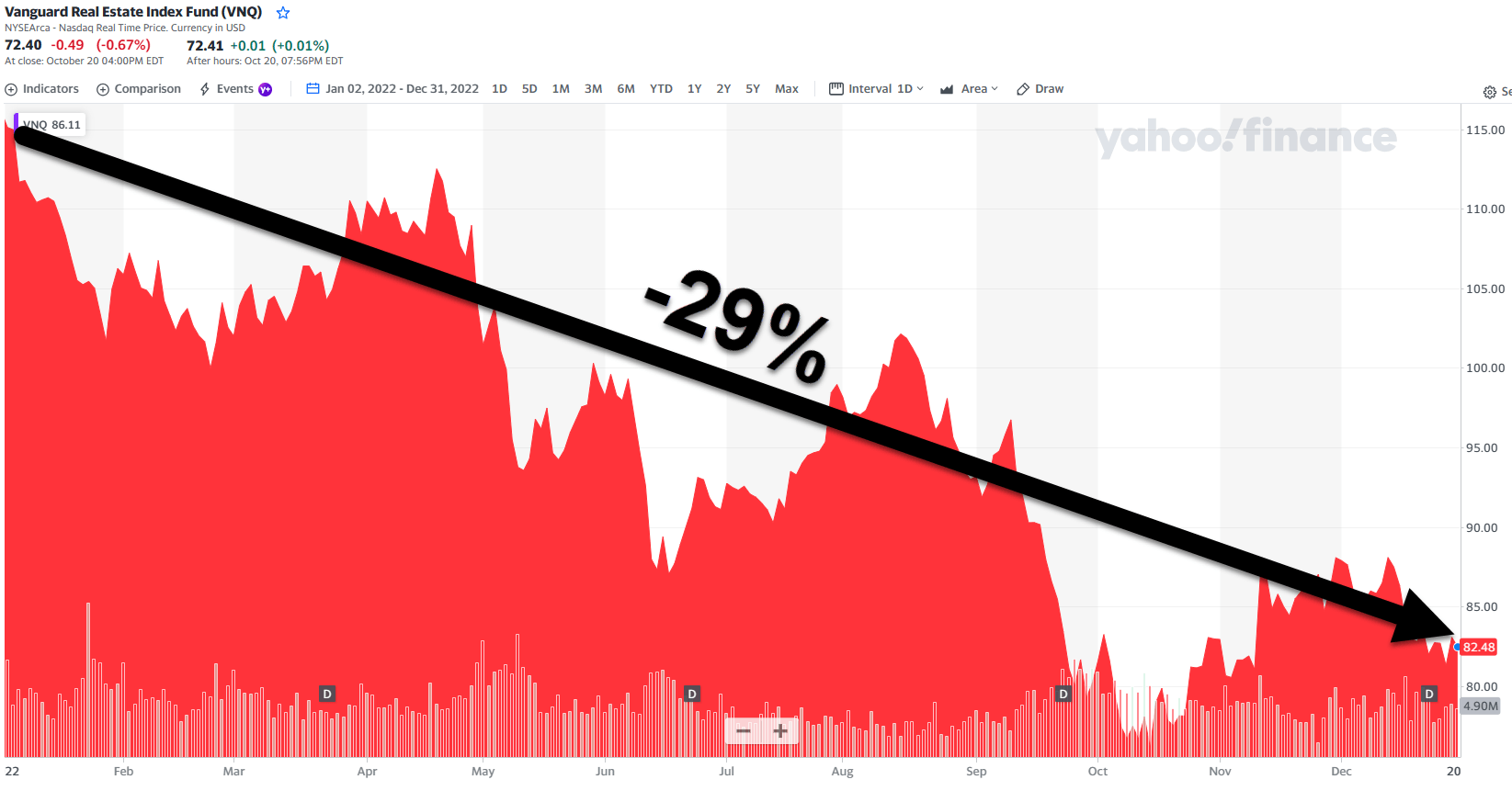

That’s on top of 2022, where shares fell 29%:

{kind=link}

Yahoo Finance

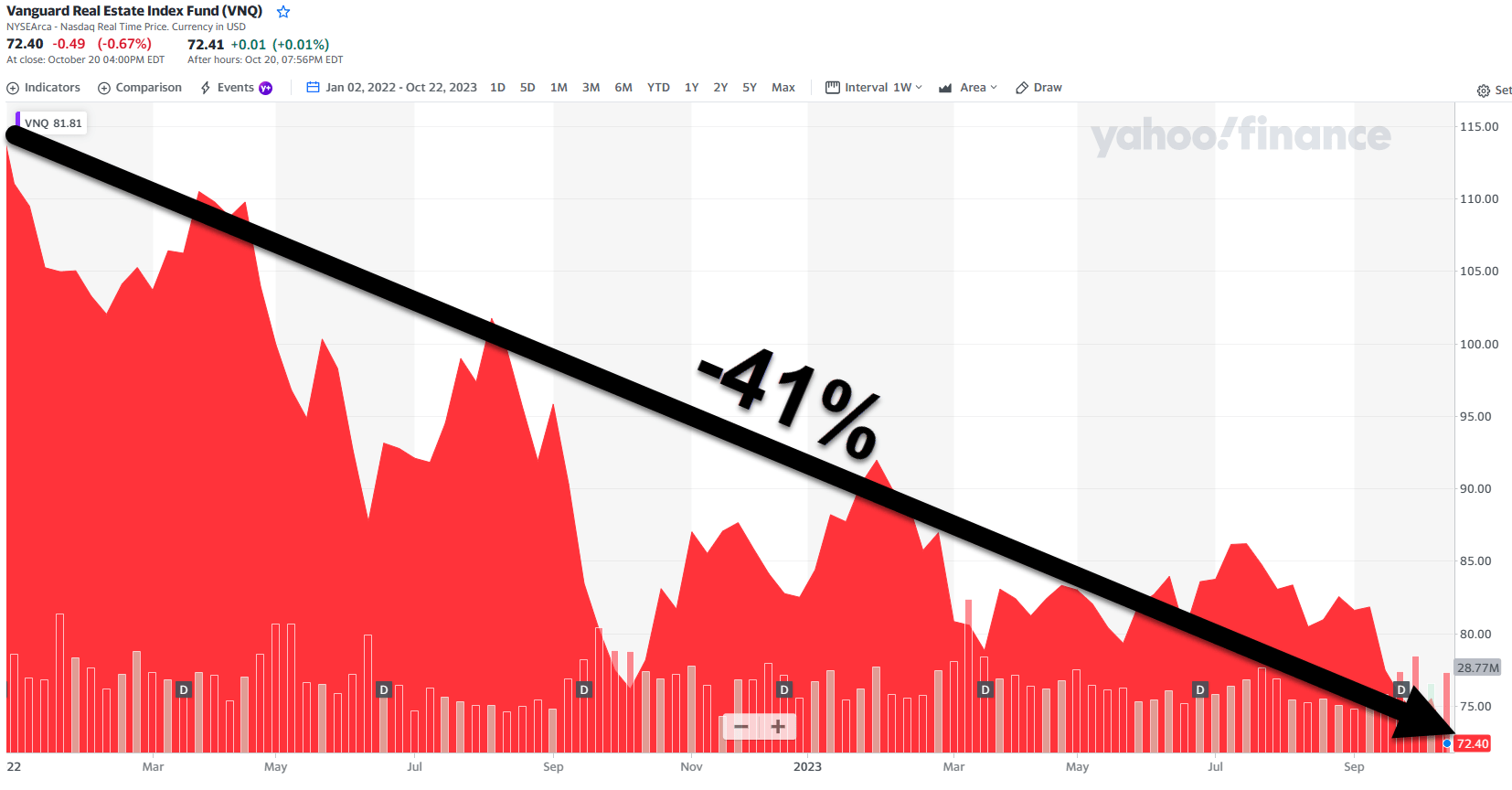

Which means REITs have dropped a whopping 41% since that January:

{kind=link}

Yahoo Finance

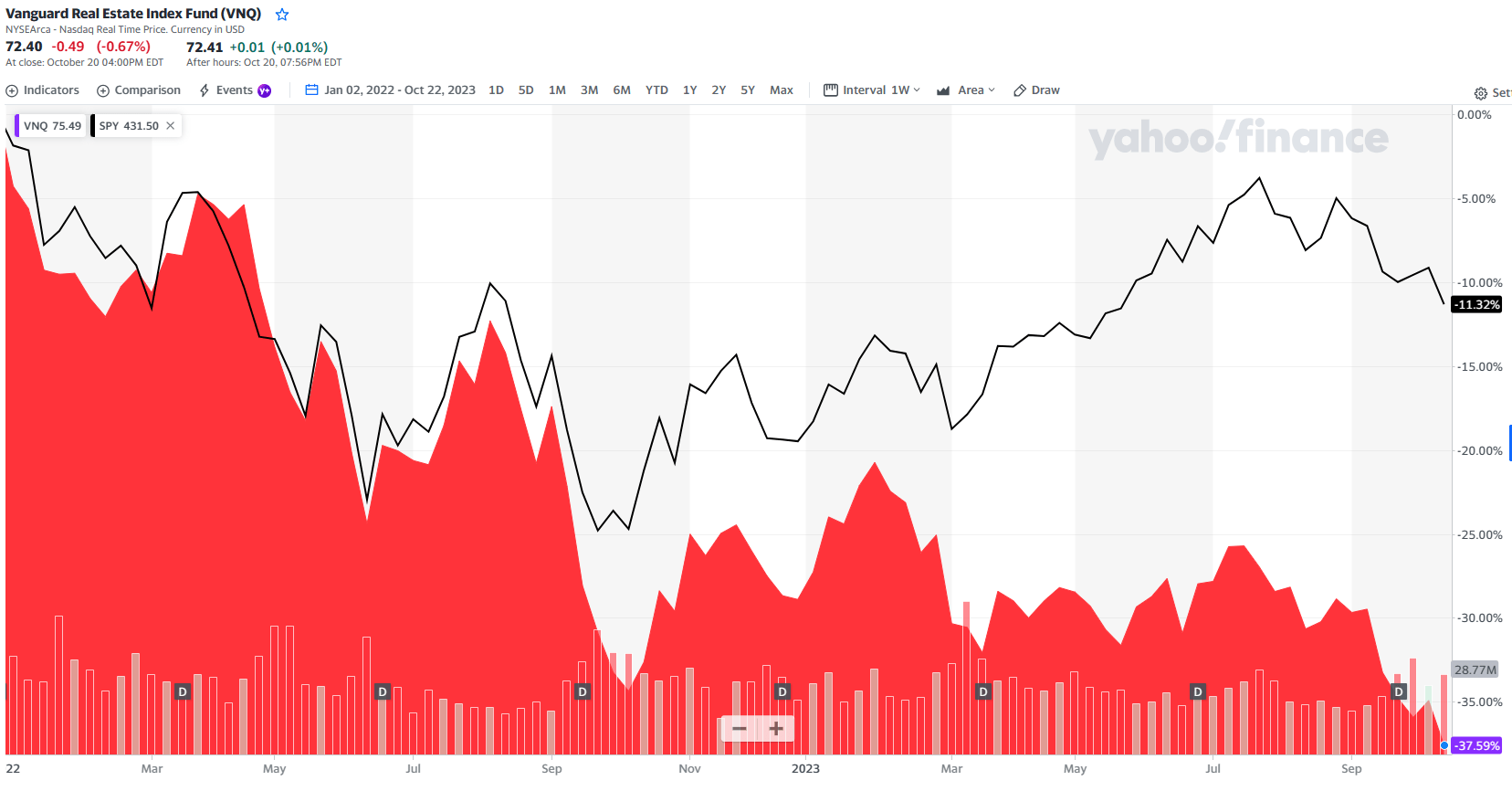

The S&P 500 ( SPY ), meanwhile, only fell 11%:

{kind=link}

Yahoo Finance

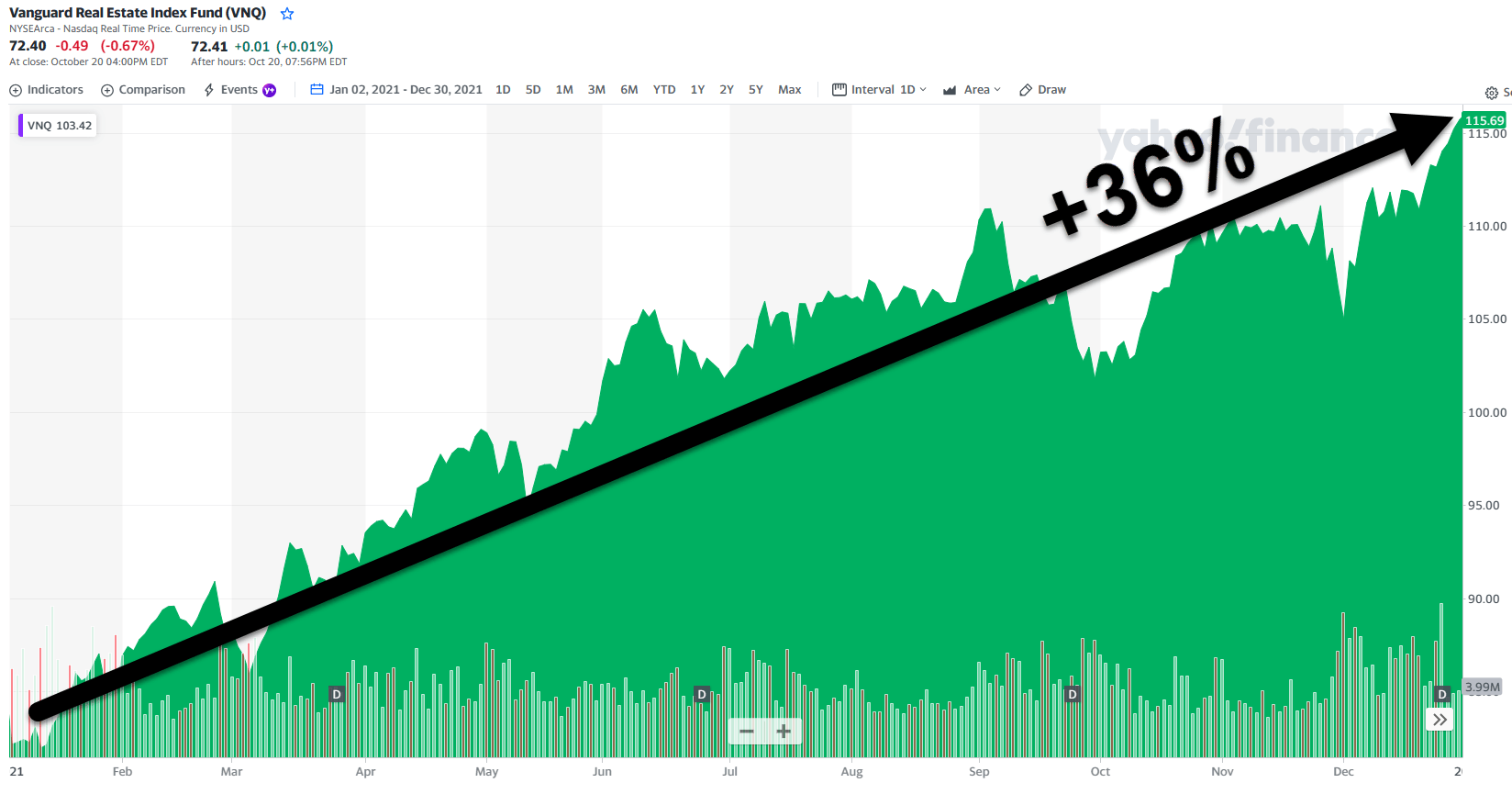

It’s hard not to pine for the “good ol’ days” of 2021 when REITs were up more than 36%:

{kind=link}

Yahoo Finance

But here’s why I’m smiling anyway…

I’m a value investor who believes the sun will shine again on REIT-dom. In which case, the opportunity to act is actually now.

The Federal Reserve Factor

Mr. Market has presented many attractive entry points for REITs this year. As macroeconomic headwinds persist, their valuations have declined intensely.

Yet their fundamentals remain strong. And since history shows that the best entry points happen during early-cycle recoveries, we’re very excited to see what we’re seeing.

“But what about the Federal Reserve?” some of you might automatically – and understandably – ask.

Well, the Fed is expected to stop hiking interest rates in the near term. Last week, Chair Jerome Powell pointed to long-term Treasury yields and their historic price advances as good news.

With that sign duly noted and if inflation progress continues, the Fed could stop raising rates altogether. “We have to let this play out and watch it” is how Powell put it. “But for now, it is clearly a tightening in financial conditions.”

Basically, “higher bond rates are producing tighter financial conditions” just like interest rate hikes. And there’s no need to overdo it.

Those comments mirror a number of his colleagues’ recent remarks.

Could we still be surprised after Nov. 1, when the Fed’s next meeting concludes? Of course!

And I will quote The Wall Street Journal here, which recently wrote :

“Still, robust economic activity has made it difficult for the Fed to declare an end to rate rises, and Powell stopped short of doing so last week. Tim Duy, chief economist at SGH Macro Advisors said: ‘Powell is not going to signal a hard stop to rate hikes. He’s always going to dangle the possibility of another hike.'”

However, as he immediately added, “But the data needs to change markedly to push the Fed in that direction.”

When Will the Sun Shine Again in REIT-Dom?

Here’s more you need to know: REITs typically deliver above-average returns at the end of rate-hiking cycles. As Cohen & Steers explains :

“While past performance does not predict future results, private real estate property prices continue to decline, and we believe this is a contrarian signal that listed REITs are likely to generate positive returns over the next 12 months.”

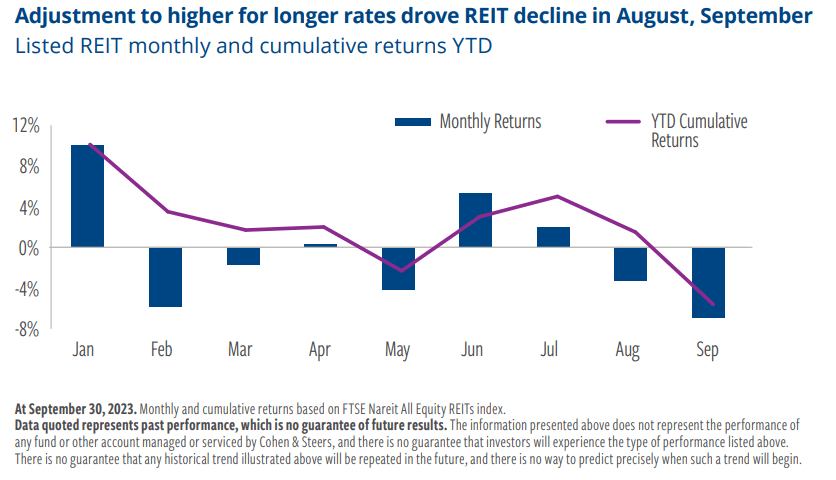

So let’s consider the facts once again, starting in September when REITs sold off 7%. That was the worst month of the year and represented the third-worst September performance since 1995.

{kind=link}

Cohen & Steers

Then, REITs faced continued headwinds at the start of October. Returns fell by around 5% as of Oct. 23.

As Cohen & Steers also explains :

“The markets are returning to an ‘old normal’ of higher rates and higher inflation. These transitions are often hard, especially given the unprecedented amount of central bank intervention that drove markets over the past decade plus. However, with valuations back to levels last seen 7–10 years ago, the sector is screening as attractive, in our view.”

REITs now trade at an approximate 6.1% implied cap rate vs. the 5.7% historical average since 2010.

In which case, let’s end these pre-recommendation words with a quote from legendary value investor Benjamin Graham:

“You are neither right nor wrong because the crowd disagrees with you. You are right because the data and reasoning are right.”

I’m just following where the latter two factors are pointing.

Now let's dig into three of my favorite REITs...

VICI Properties ( VICI )

VICI is a triple-net real estate investment trust (“REIT”) that invests in experiential properties such as gaming, hospitality, and entertainment destinations.

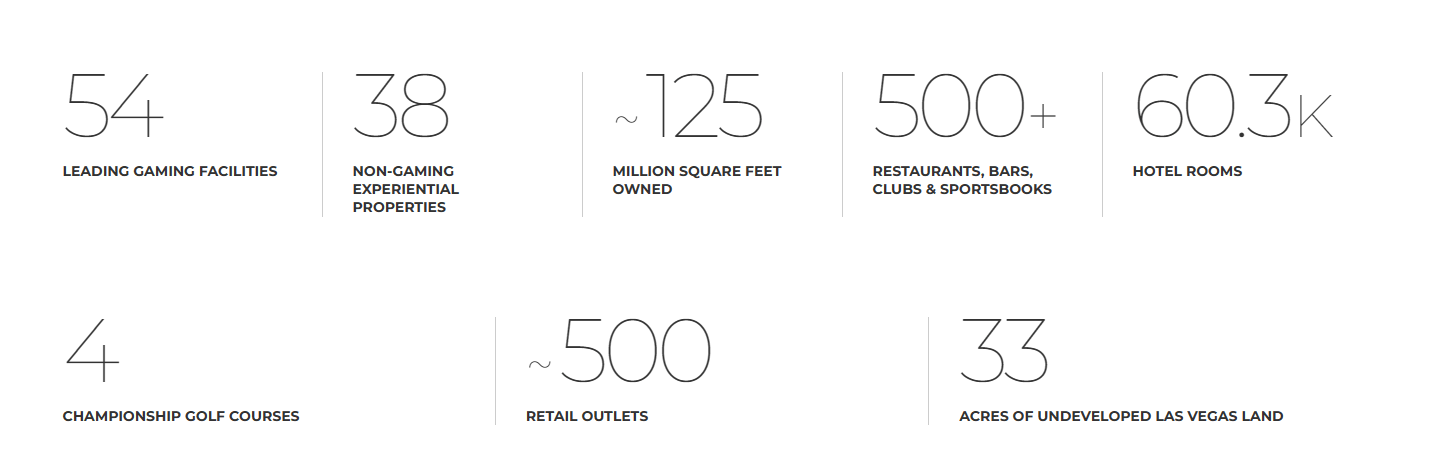

VICI’s portfolio consists of 92 experiential assets that consist of 54 gaming properties and 38 non-gaming properties which are located in the United States and Canada.

VICI’s gaming facilities include iconic trophy properties such as Caesars Palace, the Venetian Resort, and MGM Grand, all three of which are located on the Las Vegas Strip.

In total their portfolio of experiential real estate covers 125 million square feet and includes more than 60,000 hotel rooms, approximately 500 retail outlets, and roughly 500 bars, restaurants, sportsbooks, and nightclubs.

Additionally, VICI owns four championship golf courses, 33 acres of under or undeveloped land next to the Las Vegas Strip, and recently announced the sale leaseback of 38 bowling entertainment centers from Bowlero Corp., which VICI acquired for $432.9 million at an acquisition cap rate of approximately 7.3%.

{kind=link}

VICI - IR

VICI has high tenant concentration with its top two tenants (Caesars / MGM Resorts) contributing more than 75% of their annual cash rent. While VICI has very high tenant concentration, they also have very long lease terms, and the portfolio holds iconic properties that are virtually irreplaceable.

When including all of the tenant renewal options, their top tenant Caesars has a weighted average lease term of 32.1 years, and their second largest tenant MGM Resorts has a weighted average lease term of 51.8 years.

The chart below is somewhat outdated since it was listed prior to the acquisition and sale leaseback with Bowlero Corp. ( BOWL ).

After the Bowlero transaction, VICI’s portfolio has expanded from 54 gaming properties to 92 experiential properties and their tenant count has been increased from 11 to 12.

VICI - IR

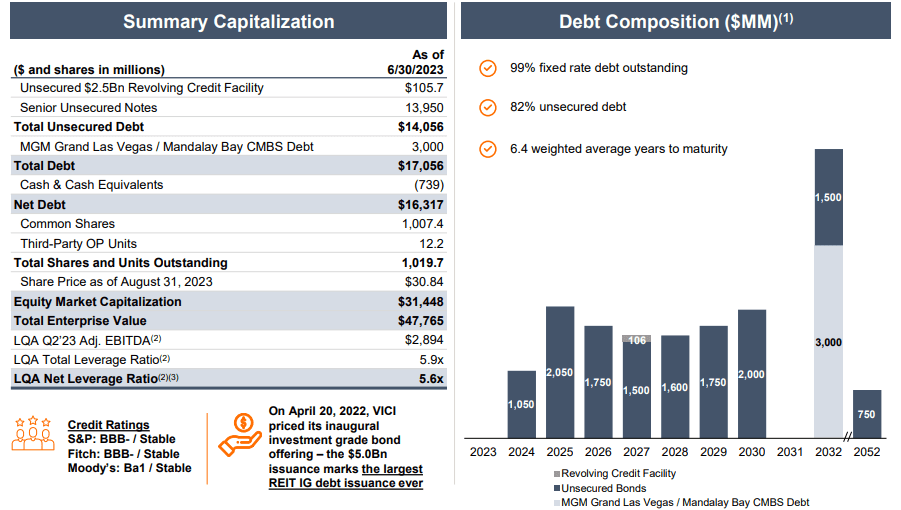

VICI is investment-grade with a BBB- credit rating from S&P Global and has sound debt metrics including a net leverage ratio of 5.6x, a long-term debt to capital ratio of 42.32%, and an EBITDA to interest expense ratio of 3.92x.

Additionally, VICI’s debt is 82% unsecured, 99% fixed rate, and has a weighted average term to maturity of 6.4 years.

{kind=link}

VICI - IR

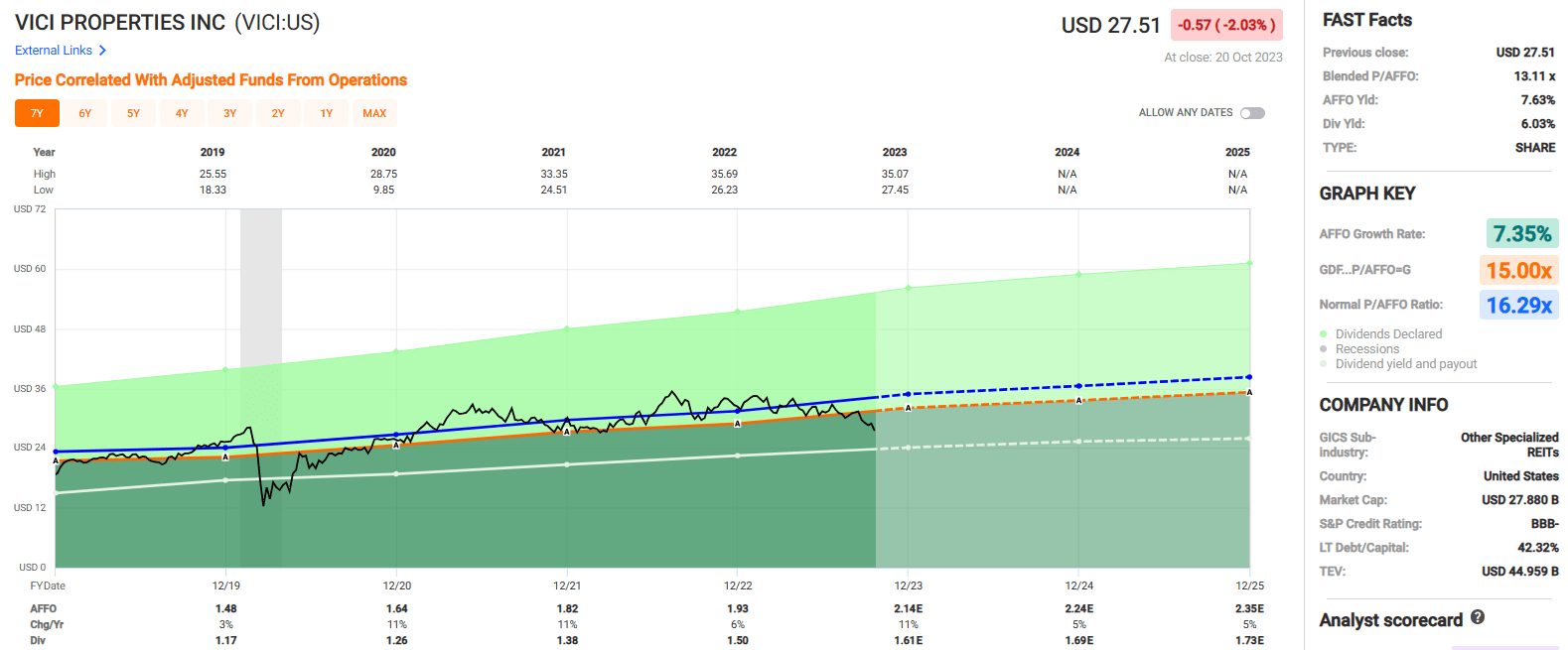

Since 2019 VICI has delivered an average adjusted funds from operations (“AFFO”) growth rate of 7.35% and an average dividend growth rate of 10.80%.

The stock pays a 6.03% dividend yield that's well covered with an AFFO payout ratio of 77.72% and currently trades at a P/AFFO of 13.11x, which compares favorably to their normal AFFO multiple of 16.29x.

We rate VICI Properties a Buy.

{kind=link}

FAST Graphs

Alexandria Real Estate ( ARE )

Alexandria is an office REIT that develops and owns Class A/A+ life science properties which are located in AAA innovation cluster locations in Boston, San Francisco, Seattle, New York City, San Diego, the Research Triangle, and Maryland.

ARE leases out laboratory space to leading biotech and pharmaceutical companies such as Moderna, Pfizer, and Bristol-Myers Squibb, as well as top academic institutions such as Harvard University and the Massachusetts Institute of Technology.

While many of its office REIT peers have recently been adding life science properties to their portfolios, ARE has a massive first-mover advantage as the REIT has had an exclusive focus on the life science real estate niche since its founding in 1994.

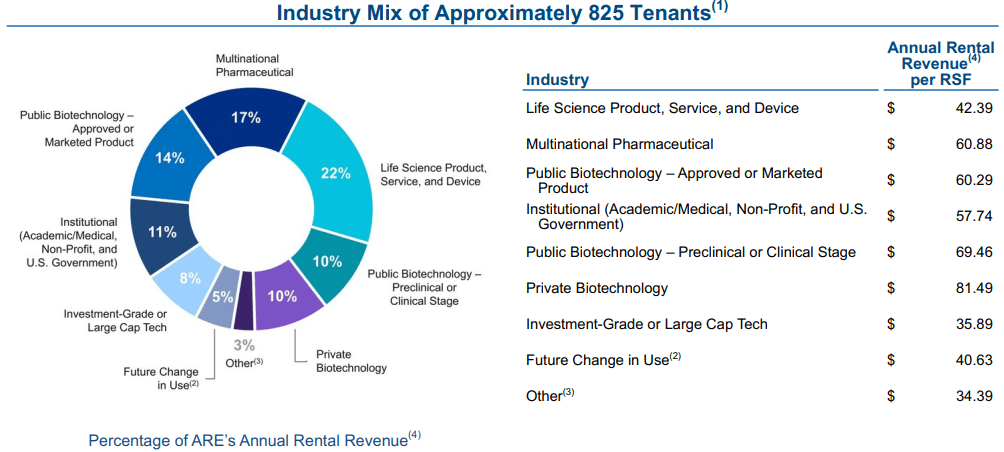

ARE’s properties are leased to around 825 tenants and approximately 49% of the rent comes from large cap publicly-traded companies or investment-grade rated tenants.

They're well diversified by tenant with their top tenant (Bristol-Myers) only making up 3.5% of the annual rent and their top 20 tenants combined only making up 31.4% of the annual rent.

ARE has a total asset base in the United States covering approximately 74.9 million square feet, which includes 41.1 million rentable square feet of operating properties that have a 93.6% occupancy rate and a weighted average remaining lease term of 7.2 years.

In addition to their operating properties, ARE has 14.7 million rentable square feet of properties undergoing construction or in development and 19.1 million square feet allocated for future development.

{kind=link}

ARE - IR

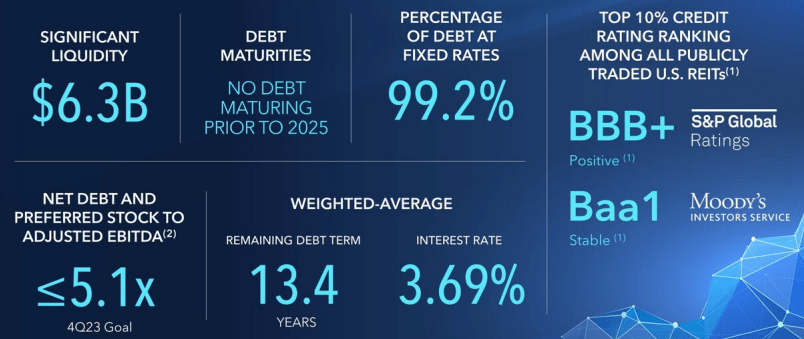

One of Alexandria’s strongest qualities is its investment-grade balance sheet. They have a BBB+ credit rating from S&P and a Baa1 credit rating from Moody’s.

Additionally, they have a fortress-like balance sheet with a net debt and preferred stock to adjusted EBITDA of 5.2x, a fixed charge coverage ratio of 4.7x, and a long-term debt to capital ratio of 38.85%.

Its debt is 99.2% fixed rate with a weighted average interest rate of 3.69% and a weighted average term to maturity of 13.4 years. Plus, the company had approximately $6.3 billion in liquidity as of the end of the second quarter and no debt maturities until 2025.

{kind=link}

ARE - IR

Another strong quality that ARE has is its historical growth rates. Since 2013, ARE has delivered an average AFFO growth rate of 5.16% and an average dividend growth rate of 8.62%.

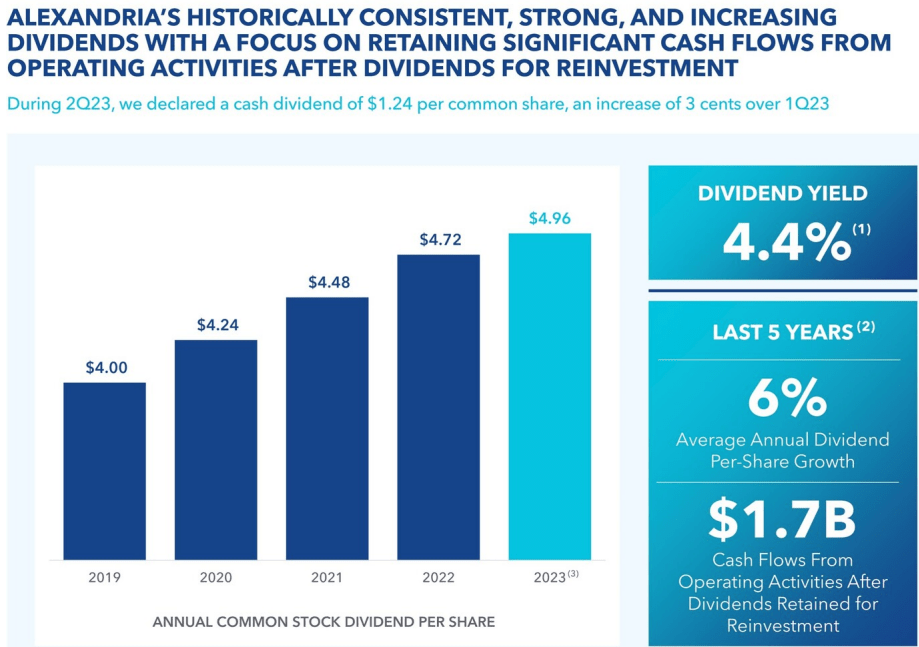

Analysts expect AFFO per share to increase by 10% in 2023, and then increase by 7% and 4% in the years 2024 and 2025, respectively. More recently, over the past five years, ARE has had an average annual dividend per share growth rate of 6% and has retained $1.7 billion in cash from operating activities after dividends were paid.

Additionally, ARE’s estimated 2023 dividend of $4.96 per share represents a 5.1% year-over-year increase when compared to the dividend of $4.72 per share paid in 2022.

{kind=link}

ARE - IR

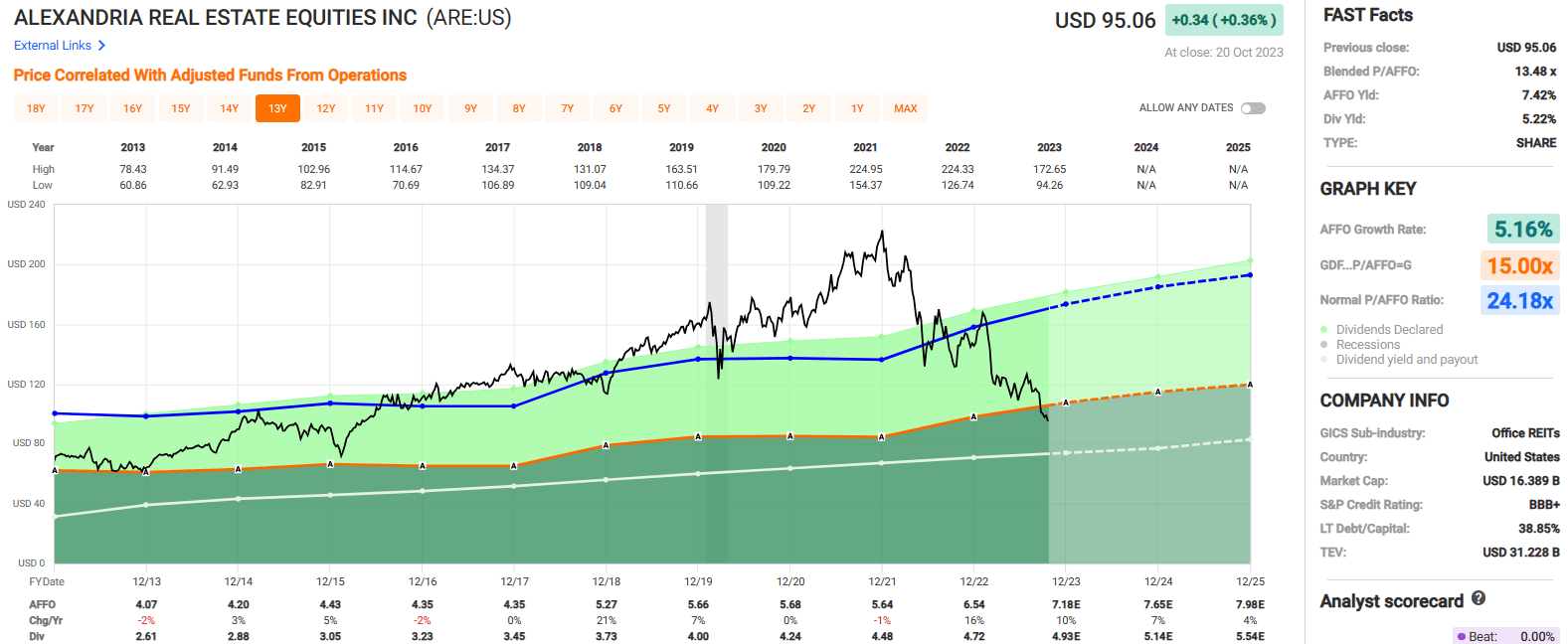

Alexandria’s stock is currently trading at multi-year lows with prices not seen since 2016. Over the past 10 years, the stock has traded at an average AFFO multiple of 24.18x whereas it's currently trading at a significant discount with a Price to AFFO of 13.48x.

Similarly, the stock is paying a historically large dividend yield of 5.22%, compared to their 5-year and 10-year average yield of 2.94% and 3.00%, respectively.

Their current dividend is well covered with an AFFO payout ratio of 72.17%, which leaves plenty of room for further dividend increases and plenty of retained earnings to pay down debt, buy back shares, or reinvest into additional life science properties.

We rate Alexandria Real Estate a Strong Buy.

{kind=link}

FAST Graphs

American Tower ( AMT )

American Tower is the second largest REIT when measured by market capitalization with a total market cap of approximately $74.80 billion, second only to Prologis ( PLD ).

The company invests in a portfolio of cell towers and other communications real estate that can host multiple tenants such as wireless service providers and television broadcast companies.

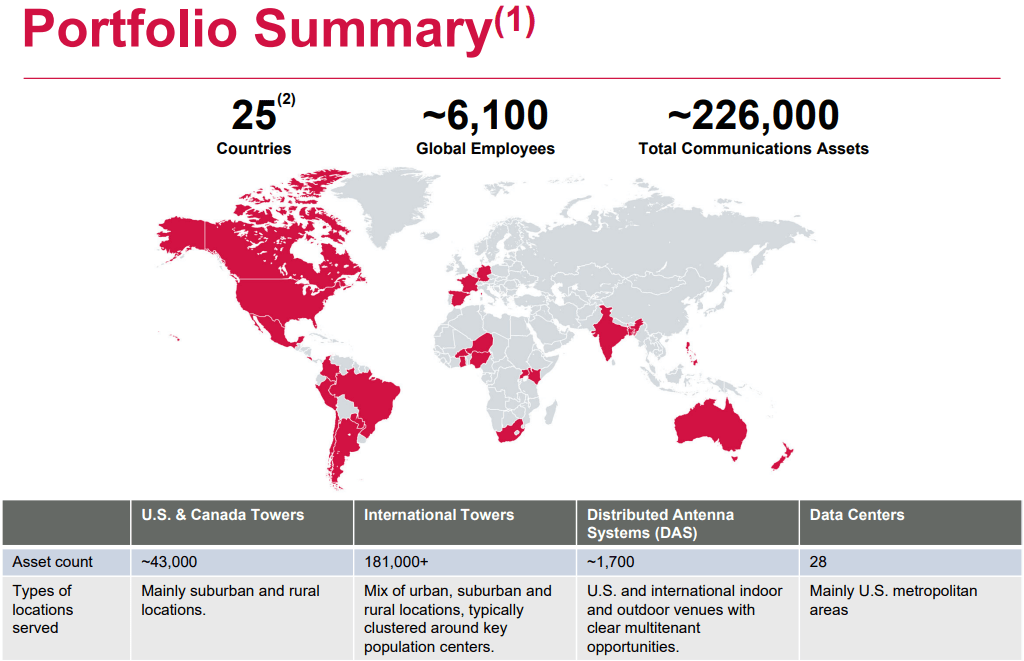

AMT has a global reach with a portfolio of roughly 226,000 communications sites that are located in 25 countries and across six continents.

AMT’s primary source of revenue is rental income generated through their multi-tenant communications sites, but they also provide services including zoning, permitting, and third-party tower site management to generate ancillary income. In total, AMT’s portfolio of communications infrastructure consists of:

- Approximately 43,000 cell towers in the U.S. and Canada

- More than 181,000 international cell towers

- Approximately 1,700 distributed antenna systems

- 28 data centers

{kind=link}

AMT - IR

American Tower’s largest tenants are T-Mobile, AT&T, and Verizon that made up 16%, 14%, and 12% of AMT’s second quarter property revenue respectively in the U.S. and Canada.

International pass-through revenue represented 15% of AMT’s Q2-23 property revenue, international tenant revenue made up 30%, and AMT’s portfolio of data centers contributed 8% to their Q2-23 property revenues.

AMT - IR

American Tower has an investment-grade balance sheet with a BBB- credit rating from S&P Global. They have a conservative net leverage ratio at 5.3x, a long-term debt to capital ratio of 82.49%, and an EBITDA to interest expense ratio of 6.54x.

AMT’s debt is 85.4% fixed rate, an improvement from 77.5% as of the end of 2022, and their weighted average term to maturity is 6.1 years. Additionally, AMT has a ton of dry powder with $8.2 billion in total liquidity as of June 30, 2023.

AMT - IR

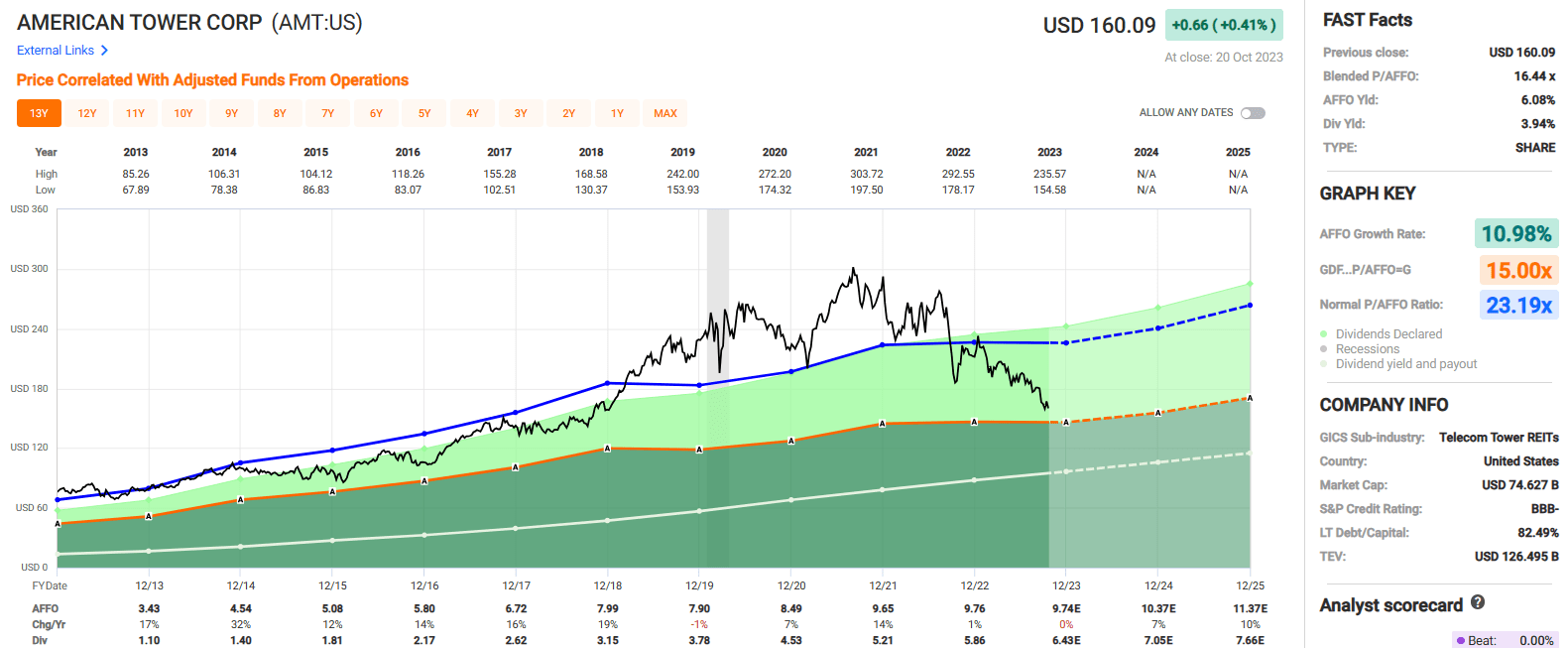

American Tower has some of the best growth rates in the REIT space with a blended average AFFO growth rate of 10.98% and an average dividend growth rate of 20.70% over the last 10 years.

Analysts expect AFFO per share to remain flat in 2023, but then increase by 7% in 2024 and increase by 10% in 2025.

AMT pays a 3.94% dividend yield that is very secure with an AFFO payout ratio of just 60.04%. The stock currently trades at a P/AFFO of 16.44x, which is a significant discount to their average AFFO multiple of 23.19x.

We rate American Tower a Strong Buy.

{kind=link}

FAST Graphs

I’m not the weatherman.

I know you’re asking yourself right now:

“How can Brad know when the sun will shine in REIT-dom, he’s no weatherman.”

That’s true.

I’m more like a REIT farmer who insists on planting high-quality seeds that will grow into everlasting gobstoppers.

That’s kind of like Jack and the Beanstalk, a fairytale in which Jack and his mother grew to be very rich and they lived happily ever after.

Stay tuned for my next article (tribute to Frank Sinatra).

"The best is yet to come."

Happy SWAN investing!

For further details see:

Make REIT Hay While The Sun Is Shining