PII - Malibu Boats: Good Company But Waiting For A Better Price

2023-11-02 22:33:07 ET

Summary

- Malibu Boats’ market capitalization has declined almost 49% since the peak in March 2021 and seems a bargain at the current price.

- Several long-term macro growth drivers could trigger a reversal in share price, but I believe the cyclical nature of the industry and the presence of near-term risks warrant caution.

- I rate the stock a Hold and will initiate a buy when the market capitalization falls further to around $840M or a price of $40 per share.

Introduction

Malibu Boats, Inc. ( MBUU ) share price reached a peak of $89 in March 2021, and has been on a steady downward trend ever since. It may seem like the right time to pick up the stock given the current depressed valuation and the prospects of several long-term growth drivers. Unfortunately, near term uncertainties like rising interest rates and an economic downturn may negatively impact the probability of a favorable investment return. Therefore, I believe waiting for an entry at a lower price, with a better margin of safety, can provide a greater chance in realizing a reasonable return.

Company Overview

MBUU designs, manufactures, and markets recreational powerboats, and has a market capitalization of about $1Bn in October 2023. Founded in 1982 focusing on the sub-segment Performance Sport Boats (“PSBs”), the company has maintained a leading market share in the PSB segment since 2003. MBUU operates in an oligopolistic market with two other companies; MasterCraft Boat Holdings, Inc. (Nasdaq: MCFT ) and Correct Craft (privately held).

Since an IPO in 2014, MBUU has expanded into two further segments through acquisitions; fishing boats and cruisers. Today, they hold the number one market share in 22’- 36’ cruisers as well. These segments are more fragmented, and other competitors include companies such as Brunswick Corporation (NYSE: BC ) and Polaris, Inc. (NYSE: PII ) among others. Utilizing an international dealer network, MBUU generates revenues when dealers purchase boats wholesale for sale to retail customers.

Financials

MBUU’s revenue growth since 2011 (the first year in which publicly disclosed financials are provided) has been phenomenal, growing at a Compound Annual Growth Rate (“CAGR”) of 24.5%. Besides possessing great management and products, this growth has also been powered by a combination of several macro trends.

Net migration phenomenon

With 95% of revenues generated in the USA, one factor impacting unit sales is the net migration of people to states where boating is popular, as an increasing population expands the total addressable market. Borrowing from MasterCraft’s Q1 FY 2022 Conference Call (Nov 10, 2021) , “...the top 25 states for the ski-wake category, most are benefiting from very positive demographic trends, including high levels of net migration. As more people move to boating friendly states and cities, our addressable market grows and drives additional consumer demand.”

According to data from Wikipedia listing the population of different US states, there has been a net migration to top boating states between 2010 to 2020, with the population growing at a CAGR of 1%:

| Population (Million) |

| 2010 |

| 2020 |

| California |

| 37.3 |

| 39.5 |

| Texas |

| 25.1 |

| 29.1 |

| Florida |

| 18.8 |

| 21.5 |

| North Carolina |

| 9.5 |

| 10.4 |

| Michigan |

| 9.9 |

| 10.1 |

| Arizona |

| 6.4 |

| 7.2 |

| Minnesota |

| 5.3 |

| 5.7 |

| South Carolina |

| 4.6 |

| 5.1 |

| Total |

| 116.9 |

| 128.6 |

| % CAGR |

| 1.0 |

Author generated table

Increasing affluent society

Another factor is an increasingly affluent society. The richer the population, the greater the purchasing power for luxury goods which expands the total addressable market. Data from Statista ( No. of families in the US and Percentage distribution of household income in the US ) reveals the number of families with incomes above $100K has increased at a CAGR of 3% between 2010 to 2020:

| Population (Million) |

| 2010 |

| 2020 |

| No. of families |

| 24.2 |

| 32.4 |

| % CAGR |

| 3 |

Author generated table

Growth in Dealerships

A third factor is the number of dealers. A greater number of dealers increases sales as dealers are the primary customer purchasing wholesale boats from boat manufacturers. Dealership figures from MBUU’s Annual Reports shows they have increased the number of dealers from 154 to 300 between 2012 to 2021, representing a 7.5% CAGR:

| MBUU dealerships |

| 2012 |

| 2021 |

| No. of dealers |

| 154 |

| 300 |

| % CAGR |

| 7.5 |

Author generated table

Pricing power

Retail prices of MBUU’s boats have increased at a 6% CAGR between 2012 and 2021, as given in MBUU’s Annual Reports. Assuming wholesale prices increased in tandem, MBUU has demonstrated the ability to raise prices at a higher rate than inflation:

| Price () |

| 2012 |

| 2021 |

| % CAGR |

| Malibu (lower price range) |

| 40 |

| 65 |

| 5.5 |

| Malibu (higher price range) |

| 130 |

| 215 |

| 5.7 |

| Axis (lower price range) |

| 40 |

| 70 |

| 6.4 |

| Axis (higher price range) |

| 75 |

| 120 |

| 5.3 |

| % CAGR (average) |

| 6 |

Author generated table

Acquisitions

MBUU has made several acquisitions. These include Maverick Boat Group (saltwater fishing segment) acquired in December 2020 for $150M , Pursuit (saltwater fishing segment) acquired in October 2018 for $100M , and Cobalt (22’-39’ cruiser segment) acquired in July 2017 for $130M .

At the time of acquisition, Pursuit had a revenue of $124M valuing it at a Price-to-Sales (“PS”) ratio 0.8. Cobalt had a revenue of $140M valuing it at a PS ratio 0.9. The revenue of Maverick Boat Group at the time of acquisition was not disclosed. Assuming MBUU acquired Maverick Boat Group at a PS ratio 1.0, revenue at the time would have been $150M. The three acquisitions combined would have added about $415M in revenues to MBUU.

Overview

MBUU generated revenues of $100M in 2011. The combined organic revenue growth drivers of 18% CAGR (1% from net migration, 3% from increasing affluent families, 8% from dealers, and 6% from price increase), would have resulted in revenues of $520M in 2021. The estimated total revenue including the $415M generated from acquisitions is calculated to be $935M in 2021. This matches closely with actual revenue of $927M that year. I am confident most of these growth drivers will continue into the future, albeit at a slower pace.

Understanding MBUU’s Net Margin Drivers

MBUU’s operations have been improving steadily due to the company's strategic initiatives.

Vertical integration

One such initiative is the push for vertical integration, which allows for greater cost efficiencies, control of the supply chain, and quality control. Innovation and R&D can also benefit from economies of scale as novel features introduced can be shared across brands.

Some examples include the in-house marinization of engines for Malibu and Axis brands starting in 2020. As mentioned in the MBUU Q4 FY 2023 Conference Call (Aug 29, 2023) , the same capability will be applied to Monsoon engines for Cobalt starting “...first quarter of fiscal 2024”. Another is the acquisition and addition of “Malibu Electronics to our vertically integrated model. We will only continue to see the benefits compound as we ramp up production in the quarters to come”, said Jack Springer, MBUU CEO, in the MBUU Q1 FY 2023 Conference Call (Nov 4, 2022) . There is also plant expansions such as at the Maverick Plant 2 which will “improve margin profiles for the Cobia and Pathfinder brands and Maverick Boat Group as a whole”, as mentioned in the MBUU Q3 FY 2022 Conference Call (May 10, 2022) .

Acquisition Synergies

Synergies from acquisitions can further raise margins. In the MBUU Q4 FY 2023 Conference Call (Aug 29, 2023), it was stated that “...in the first two years. Cobalt doubled its EBITDA” and that a “similar thing has happened twice now with the acquisition of Pursuit in 2018 and the acquisition of MBG in 2020, we began with a basis of much lower margins”, “...we expect to eventually be able to take all of our brands into that 20% EBITDA margin threshold”.

The effectiveness of these strategies is evidenced by an improving net margin, which has climbed from 8% in 2011 to 13% in 2022. In my opinion this will continue to improve. As depreciation, amortization and taxes account for about 4% of revenue currently, it is my opinion that net margins can rise to 15% in about three years assuming an EBITDA margin of 20% is achieved.

Note that net margins fell to 7.5% in 2023 due to a litigation settlement of $100M. The “Batchelder case” involved a fatal propeller strike which occurred in 2014. With the settlement concluded , a normalization of net margins can be expected. There is a potential for a small upside in the future as according to the 2023 Annual Report , MBUU “...contend(s) that the insurance carriers are responsible for the entirety of the $100 million settlement amount and related expenses”, and that they “…. intend to vigorously pursue our claims against our insurers to recover the full $100 million settlement amount and expenses”.

Risks

Despite the long-term growth drivers described above, there are short term sales headwinds which may weigh on investors and cause market sentiments to be bearish in the coming quarters.

The Federal Reserve has raised benchmark interest rates to the highest level in 15 years to fight inflation. A high interest rate increases floor financing costs for dealers, reducing their ability to buy boats wholesale. Floor financing refers to loans dealers incur to purchase inventory from boat manufacturers for display on their shop front. For consumers, high interest rates increase burden on household debt reducing discretionary income, and makes loans more expensive. Inflation and higher prices lead consumers to cut spending on nonessential goods. Together, these factors reduce dealers’ confidence in ordering wholesale, which will impact sales for MBUU. From MBUU Q4 2023 Conference Call (Aug 29, 2023), dealers are “...expressing caution in taking on new inventory amid rising interest rates, more normalized channels, recessionary concerns and weather driven order delays. Regarding interest rates, dealers have faced the effect of higher inventory levels on their lots, compounded with paying higher interest rates on that inventory which has driven their cost higher and made them more passive about carrying higher levels of inventory.”

In addition, revenue generated during the first and second quarters (July to December) are historically lower compared to the third and fourth quarters (January to June) when summer is approaching, as indicated by data from MBUU Quarterly Reports in the pre-COVID-19 years:

| 2017 |

| 2018 |

| 2019 |

| Percentage revenue 1Q and 2Q |

| 46% |

| 44% |

| 43% |

| Percentage revenue 3Q and 4Q |

| 54% |

| 56% |

| 57% |

Author generated table

With regards to prices, retail powerboat prices as given in MBUU’s Annual Reports have increased 9% on average between 2021 and 2023 due to COVID-19 induced demand as well as inflation:

| Prices () |

| 2021 |

| 2023 |

| CAGR % |

| Malibu (lower price range) |

| 65 |

| 80 |

| 10.9 |

| Malibu (higher price range) |

| 215 |

| 300 |

| 18.1 |

| Axis (lower price range) |

| 70 |

| 80 |

| 6.9 |

| Axis (higher price range) |

| 120 |

| 175 |

| 20.8 |

| Pursuit (lower price range) |

| 100 |

| 130 |

| 14.0 |

| Pursuit (higher price range) |

| 1200 |

| 1400 |

| 8.0 |

| Cobia (lower price range) |

| 55 |

| 60 |

| 4.4 |

| Cobia (higher price range) |

| 475 |

| 500 |

| 2.6 |

| Pathfinder (lower price range) |

| 50 |

| 60 |

| 9.5 |

| Pathfinder (higher price range) |

| 220 |

| 250 |

| 6.6 |

| Maverick and Hewes (lower price range) |

| 45 |

| 45 |

| 0.0 |

| Maverick and Hewes (higher price range) |

| 105 |

| 125 |

| 9.1 |

| Cobalt (lower price range) |

| 65 |

| 75 |

| 7.4 |

| Cobalt (higher price range) |

| 500 |

| 625 |

| 11.8 |

| Average CAGR % |

| 9.3 |

Author generated table

It is unlikely such elevated price increase can continue forever. In 2024, there is a possibility dealers may reduce prices. From MBUU Q4 2023 Conference Call (Aug 29, 2023), Jack Springer says “...at the retail level, prices I do think will come down next year…it’s not necessarily going to be on the wholesale side, but that retail customer will see pricing degradation.” While a decline in retail prices may not apply to wholesale prices, there is a good chance this limits the increase of wholesale prices by boat manufacturers.

As for 2024, the guidance given during the MBUU Q4 2023 Conference Call (Aug 29, 2023) is that they “...anticipate a year-over-year decline in net sales ranging from mid to high teens percentage,” with “consolidated adjusted EBITDA margin is expected to be down 300 to 400 basis points.” However, even “...looking at 18% to 20% down type of environment”, they believe they will be able to maintain “...an above 17% EBITDA margin” and that they “...can be extremely profitable even in a prolonged downturn”. In addition, the company carries no long-term debt, and has a revolving credit facility of up to $350M with a maturity date of July 8 2027, with $65M currently drawn.

Valuation

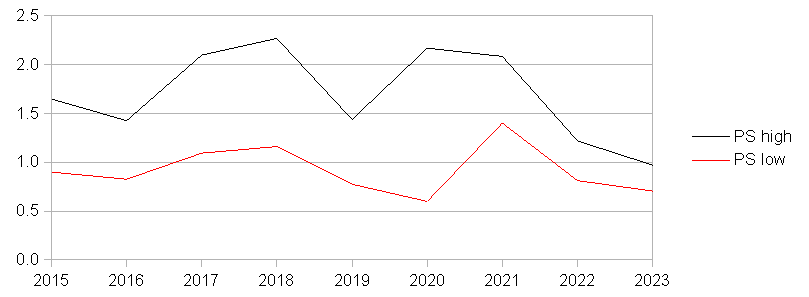

It is often tempting to extrapolate past results to derive an expected future growth. However, this is oftentimes too simplistic. Instead I analyze best and worst-case growth scenarios based on individual growth drivers and risks. For each scenario, I then apply three metrics; the PS ratio, estimated future sales, and a time horizon of three years to arrive at a value. From my experience, a fair PS ratio for companies depends on the longer-term revenue growth and net margins achievable. Given the assumptions mentioned above on an achievable net margins of 15%, I ascribe a fair PS ratio of 1.2 to MBUU which is equivalent to a PE ratio of 8. A PS ratio of 1.2 is also within the limits the market has valued the company as can be seen in the graph below:

{kind=link}

PS Ratio (Author generated table)

Best case scenario

My thesis is that MBUU can grow revenues organically at a CAGR of 10% in the long term. This is based on several assumptions which include:

-

Net migration and growth of affluent families continue to increase at a CAGR of 1% and 3% respectively.

-

Pricing increases at a slightly lower CAGR of 5% because of the large price surge that has occurred in the last couple of years due to COVID-19 induced demand.

-

Revenue growth from dealerships increases at 1% CAGR. Since 2021, the number of dealers has remained stagnant. This is likely because the number of dealers is close to saturation. According to the MBUU Q3 2023 Conference Call (May 03, 2023) , MBUU will still add additional dealers but this may be limited to only some of their 8 brands such as “...improving (the) Pursuit network to 45 or 50 over the coming, call it, year to 18 months, improving Pathfinder by 15 to 20 dealers over time.”

-

MBUU is successful in retaining a leading position in the recreational powerboat segments they compete in. Based on the emphasis during the quarterly earnings conference calls, this depends on two main capabilities which I am convinced will continue to improve; innovation and operational excellence.

With regards to innovation, MBUU regularly introduces new product features which is crucial to attract customers in a highly innovative and competitive industry. In addition, from the 2017 Annual Report , MBUU has “...demonstrated our ability to successfully defend our patented technology and now have five of the seven largest performance sports boat companies and almost all stern drive companies under license” with regards to their surf intellectual property.

Operational excellence is important because retail demand varies and “...50% or more of the boats are bought at the dealer lot” according Jack Springer in the MBUU Q4 2023 Conference Call (Aug 29, 2023). The ability to ramp up and down production quickly is critical as it allow the company to capture rising demand, and to cut back production in times of weakening demand reducing the risks of oversupply of inventory which may necessitate clearance via discounting.

Potential growth drivers not included due to uncertainty

There is also the possibility of further acquisitions which will increase revenue, but this is excluded from revenue estimates above because we do not know if any acquisition will occur. However, one potential acquisition could occur in the pontoon segment. The pontoon segment is the fastest growing segment in recreational powerboats. According to BoatingIndustry , there were 16.9% new pontoon registrations between 2019 and 2021, and pontoons made up 22% of total marine units registered in 2021.

As stated in the MBUU Q4 2023 Conference Call (Aug 29, 2023), “...we are going to be in pontoon. So, if there is no acquisition made, then we will greenfield pontoons. But both of those will be coming over the next, call it, a couple of quarters.”

The likelihood of acquiring a pontoon manufacturer exists firstly because of a “...highly fragmented Pontoon segment”, according to

MasterCraft’s (MCFT) Q4 FY 2019 Conference Call (Sep 12, 2019)Revenue per share may also increase if MBUU chooses to use FCF to repurchase shares and reduce outstanding share count. At a current market capitalization of $1B and FCF of $150M, this gives a FCF yield of 15% which the company could deploy for this purpose. Again, this is disregarded as it is not certain how MBUU will utilize their FCF.

Finally, there is a potential short-term trigger which would boost revenue. Natural disasters occur every few years resulting in the destruction of boats. While not immediate because of the economic and societal impact to affected areas, boats will eventually need to be replaced. The most recently disaster, Hurricane Ian, occurred in September 2022. Jack Springer said in the MBUU Q4 2023 Conference Call (Aug 29, 2023) “...we have not yet begun to see the replacement of boats related to Hurricane Ian. Many of our dealers believe this will be very significant as it has been estimated that 15,000 boats were totaled as a result of the hurricane.” In the past decade, other significant natural disasters include Hurricanes Harvey and Irma in 2017 and Hurricane Sandy in 2012, where an estimated 63,000 and 65,000 recreational boats were damaged or destroyed respectively. However, this is also excluded as it is not possible to determine how significant an impact this would have on MBUU’s sales.

An organic growth of 10% CAGR would increase revenues from $1.4B in 2023 to $1.85Bn in 2026. Applying a PS ratio of 1.2 gives a valuation of $2.2Bn.

Worst-case scenario

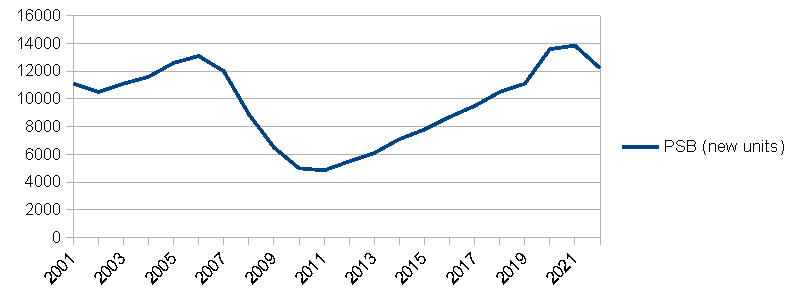

As PSBs are considered luxury goods, they are sensitive to interest rates and economic conditions. A sales decline of 50% is possible in an economic downturn, despite the long-term growth drivers being intact. In the event of an economic downturn, sales may be depressed for a substantial period. Data from MBUU’s Annual Reports shows that during the 2007 recession, the total number of new PSBs units sold per year in the USA fell from 13,100 to 4,850 units in the period 2006 to 2011, representing a decrease of 63%:

{kind=link}

PSB units sales, data from MBUU Annual Report and National Marine Manufacturers Association (Author generated chart)

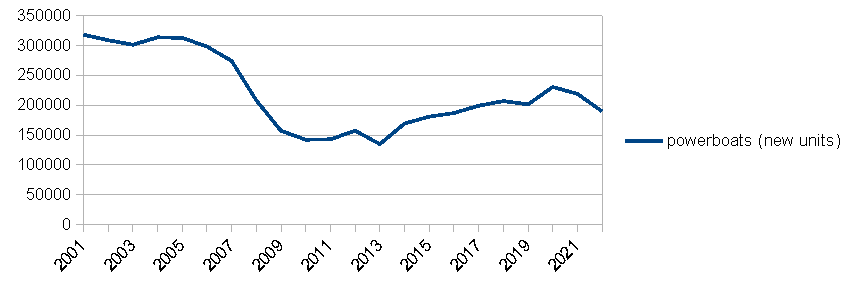

Recreational powerboats on the whole fared slightly better, with the total number of new units sold per year falling from 298,100 to 142,830 units in the same period, representing a decrease of 52%, according to figures from MBUU’s Annual Reports .

{kind=link}

Recreational Powerboats sales, data from MBUU Annual Report and National Marine Manufacturers Association (Author generated chart)

It took a decade for the total number of new PSBs units sold per year to recover to previous highs. As MBUU has publicly disclosed financials starting from 2011, the remarkable growth they have experienced could be attributed partly to a period of prolonged prosperity in the boating industry. With no information on how MBUU’s revenues were affected during the 2008 recession, we can only speculate that it followed the industry’s decline closely as they held a leading market share. As MBUU has expanded their product offerings beyond PSBs, I estimate their business would mirror the total recreational powerboats market more closely in future if a downturn were to occur.

The above phenomenon can be explained as during the 2007 recession, the median income in the USA fell approximately 7%, and the wealth of families fell over 40%, according to data from Pew Research Center . Conversely, during the economic recovery from 2011 to 2018, the median income in the USA increased approximately 15%, the fastest in four decades.

A 50% revenue decline from current sales would result in a revenue of $700M in 2026. Applying a PS ratio of 1.2 gives a valuation of $840M. A PS ratio of 1.2 is still appropriate because the long-term fundamentals of the business and net margins would remain intact.

Conclusion

MBUU is a company with compelling growth prospects. I value MBUU, in a three year time frame, to be in the range $840M to $2.2Bn. My investing strategy is largely based on Mohnish Pabrai’s investment philosophy “Heads, I Win; Tails, I Don't Lose Much.” I try to minimizing potential losses by buying into a stock only at the low end of my valuation. As such, I rate MBUU a Hold with a target entry price at a market capitalization of $840M, or a share price of about $40 with a current diluted outstanding share count of 21.3M shares.

For further details see:

Malibu Boats: Good Company But Waiting For A Better Price