LOAN - Manhattan Bridge: Juicy 9% Dividend But A Risky REIT Play

2023-04-24 08:28:35 ET

Summary

- In this article, we discuss one of the smallest mortgage REITs on the market, NY-based Manhattan Bridge Capital.

- The company is run by just five people who have a great track record of building a high-quality book of residential and commercial loans.

- While the company has a 9% yield protected by its sturdy loan book, I do not like the risk/reward of investing in this company, despite my expectation of peer outperformance.

Introduction

This year, I have written an increasing number of articles focusing on high-yield stocks (like this one ). After all, there are plenty of good reasons to add (some) high-yield investments to one's portfolio. Moreover, in light of the ongoing banking turmoil, investors are looking for opportunities in the finance space.

In 2019 - I cannot believe it was almost four years ago - I wrote an article covering New York-based Manhattan Bridge Capital ( LOAN ) , a mortgage REIT with a fat dividend and a management team of just five people.

In this article, I will revisit this company, especially because people are increasingly interested if I still believe that it's a good company.

So, without further ado, let's get to it!

Mortgage REITs Make Me Nervous

(What a way to start a Mortgage REIT article...)

I believe that most of my regular readers know that high yields make me nervous. After all, we can assume that the higher the yield, the lower the expected capital gains. Once yields come close to double digits, there's a high chance of buying a stock that comes with negative long-term total returns.

{kind=link}

In the high-yield category, I'm usually an opponent of mortgage REITs. As the chart below shows, the price return of the iShares Mortgage Real Estate ETF ( REM ) was negative 64% over the past ten years. However, this ETF yields 11.6%, which is very juicy. Nonetheless, even if investors had reinvested every penny of these dividends (without paying any taxes on it), the total return would still be negative 1% over the past ten years. The Vanguard High Dividend Yield ETF ( VYM ), which yields 3.1%, doubled during this period - and that's without incorporating dividends! The total return was 165% during this period. In other words, investors need a very good reason to go for high mortgage yields, given the high probability of underperformance and the unfavorable risk/reward.

With that said, LOAN is different. Over the past ten years, it returned 300%, excluding dividends. The total return was 730%.

Over the past five years, LOAN returned 3.6%, which beat the REM total return by 23 points.

So, with that in mind, let's answer the question: what's LOAN?

The Company Behind LOAN

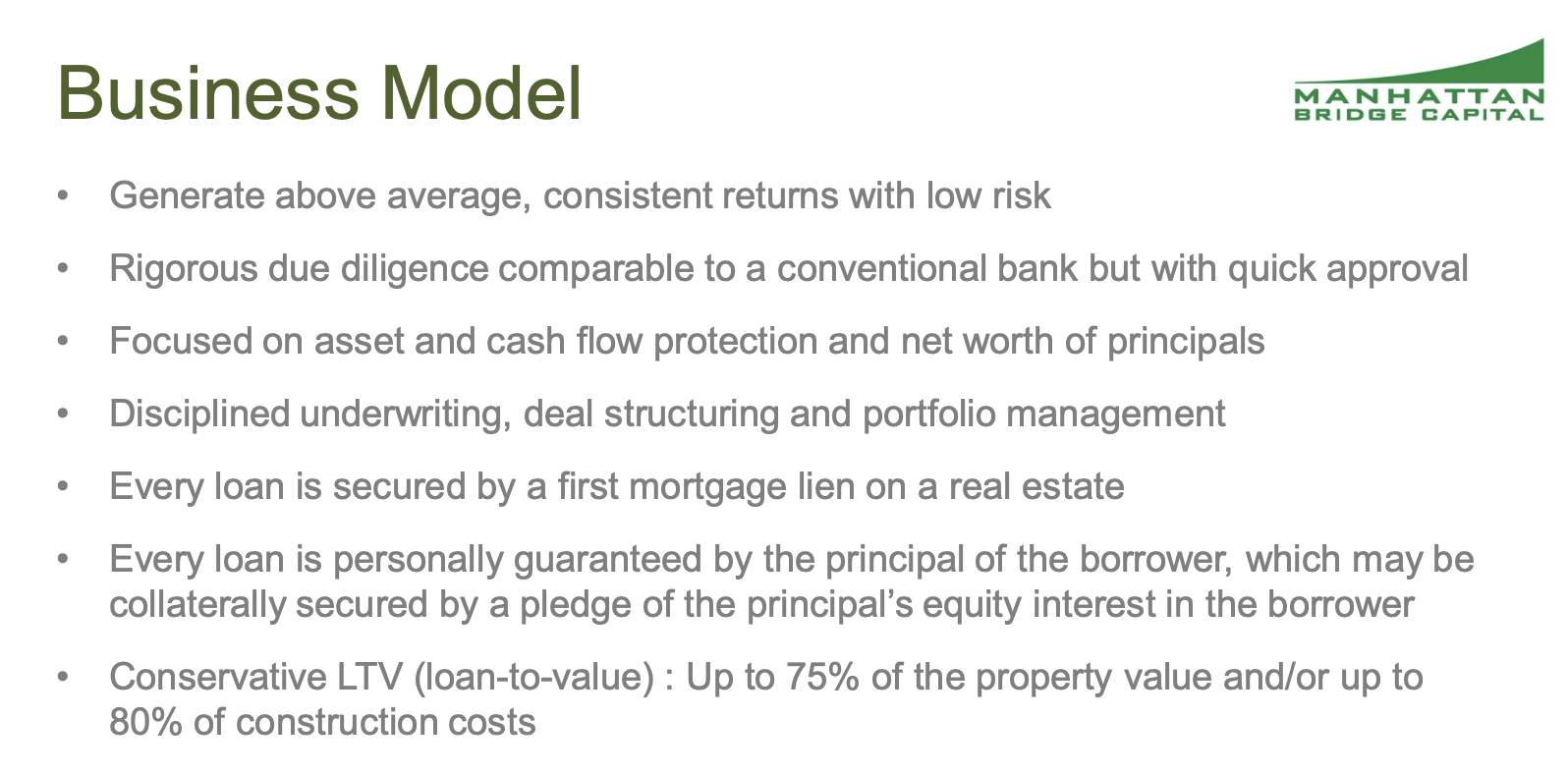

Manhattan Bridge Capital is a very small mortgage REIT. The company has a market cap of slightly less than $60 million. As of December 31, 2022, the company has five employees. While it uses outside lawyers and independent professionals for its operations, it's a very small and focused company with a lot of experience.

Its CEO is Assaf Ran, who founded the company in 1989. He owns 23% of all outstanding shares.

While there are obviously high risks that come with buying a company run by five people, I believe that it is a benefit in the mortgage industry, as the company is extremely careful and rigorous when it comes to deciding which deals to fund. Large corporations are usually way more prone to economic risks due to their size.

As the name already suggests, the company is based in New York, where it specializes in offering short-term, secured, non-banking loans to real estate investors.

Essentially, the company calls itself a leading hard money lender.

These loans are used to fund property acquisition, renovation, rehabilitation, or improvement projects located in the New York metropolitan area, including New Jersey and Connecticut, and Florida.

{kind=link}

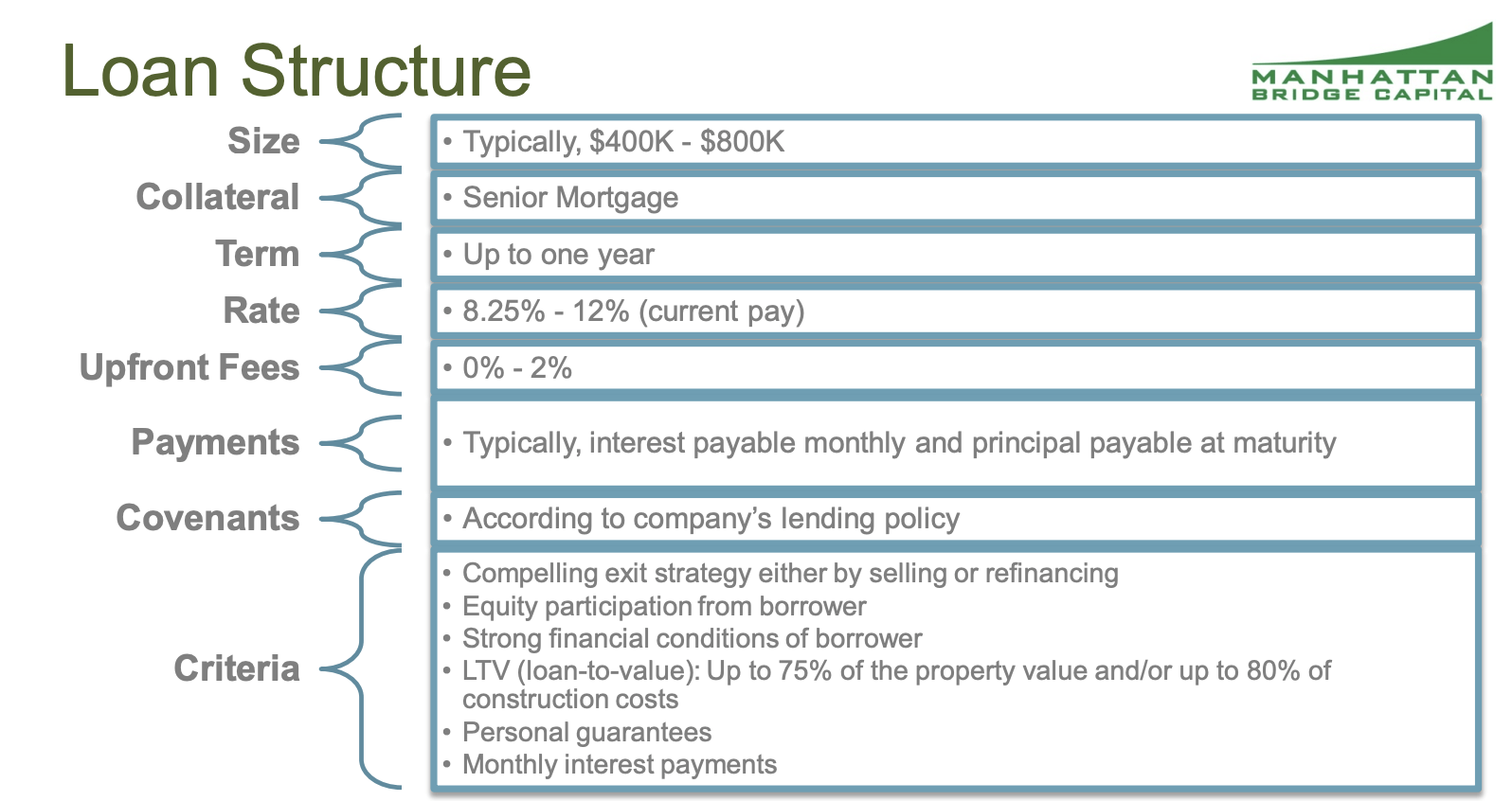

Each loan is secured by a first mortgage lien on real estate and is personally guaranteed by the borrower's principal(s). The maximum amount of any loan is the lower of 9.9% of the aggregate amount of LOAN's loan portfolio, or $3.5 million. Its loans usually have a maximum initial term of 12 months, bear interest at a fixed rate of 9% to 12% per year, and are subject to origination fees and other fees related to underwriting and funding the loan.

{kind=link}

On April 19, the company reported its 1Q23 earnings. LOAN reported a net income of $1.26 million, which translates to $0.11 per share. This is a decrease from $1.43 million or $0.12 per share for the same period last year. The decrease is primarily due to a significant increase in interest expense because of higher LIBOR/SOFR rates and a special bonus to officers in 2023, partially offset by an increase in interest income.

This is what the company said regarding higher general and administrative expenses in its 10-Q :

General and administrative expenses for the three months ended March 31, 2023 were approximately $496,000 compared to approximately $361,000 for the three months ended March 31, 2022, an increase of $135,000, or 37.4%. The increase is primarily attributable to a special bonus to officers in 2023 for extending the Webster Credit Line, and increases in payroll, marketing, travel and meals expenses, partially offset by a decrease in advertising expense.

LOAN's total revenue increased by 13.4% to $2.4 million. The increase in revenue was due to an increase in lending operations and higher interest rates charged on commercial loans. The majority of the revenue, roughly $1.95 million, represents interest income on secured commercial loans offered to real estate investors, while approximately $444,000 represents origination fees on such loans.

Furthermore, the company authorized a buyback program. It aims to repurchase up to 100,000 common shares between April 2023 and April 2024.

Unfortunately, stock-based compensation makes these buybacks look like a drop in a bucket.

Regardless, and related to its decision to spend money on buybacks, the company remains upbeat, despite significant challenges facing the commercial real estate market. According to Assaf Ran (emphasis added):

The high interest environment contributed to our revenue increase. However, our interest expense almost doubled versus the same quarter a year ago. Generally, we have experienced slower and riskier real estate markets in our geographic areas of operation, together with tight liquidity and less competition. Yet, due to the strength of our loan portfolio, we suffered no losses and impairment expenses .

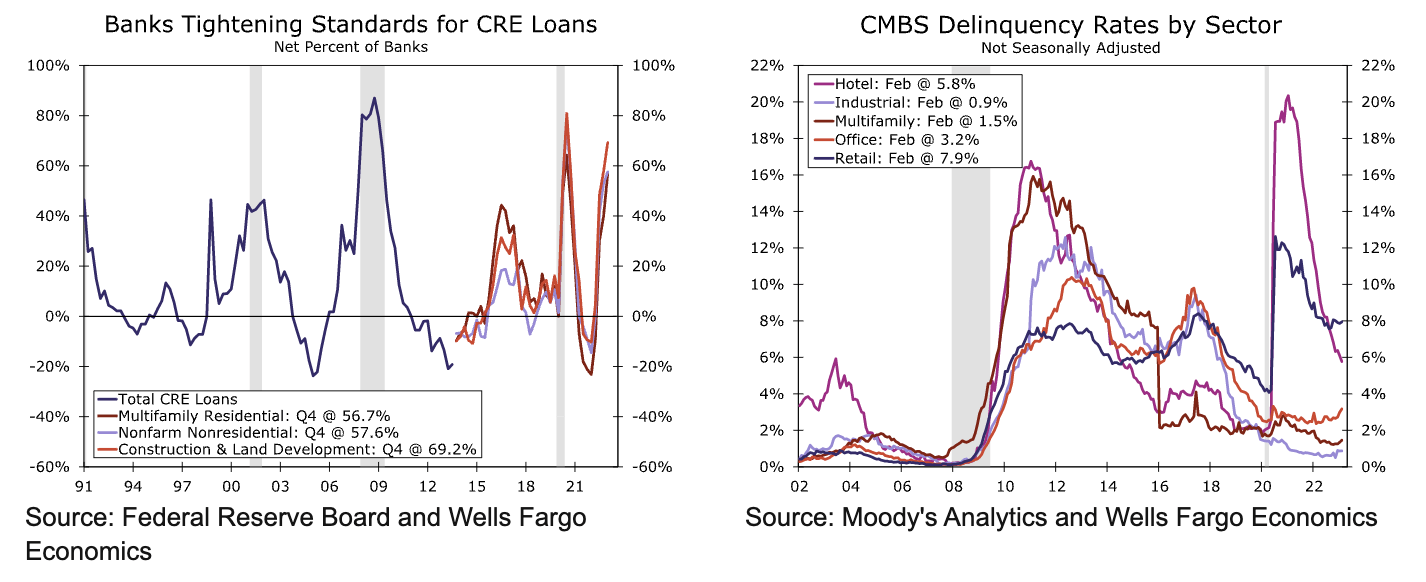

Based on these comments, I recently wrote a real estate-focused article that highlighted rising risks in commercial real estate. It confirms LOAN's comments, as delinquency rates are further rising, fueled by tighter financial conditions.

{kind=link}

Based on that context, not only is LOAN not encountering any impairment expenses and losses, but it also enjoys limited commercial real estate exposure. The company currently holds $72 million worth of loans. $59 million consists of developers-residential loans. Commercial loans are just $11 million. Not a single client accounted for more than 10% of the company's total loan book, which is something the company keeps in mind when working on new loans.

The LOAN Dividend & Valuation

LOAN currently pays a dividend of $0.1125 per share per quarter. This translates to a yield of 9.0%.

The dividend is not consistent, as LOAN is a mortgage REIT. It is obligated to distribute at least 90% of its taxable income to shareholders. As this taxable income is highly volatile, we're dealing with a dividend that has seen its ups and downs in recent years.

While the dividend could see a steep decline in case the company occurs losses on its loans, I expect the dividend to remain rangebound on a prolonged basis due to the absence of both high-growth opportunities and somewhat limited downside risk.

Furthermore, shares are trading at 1.3x the tangible book value. That is an attractive valuation that comes with elevated macroeconomic risks. If confidence returns and lower rates allow the company to boost its income, I have little doubt that shares will trade close to 2x their tangible book value.

The company does not have a consensus price target. The last price target was given in 2017, which (obviously) isn't relevant anymore.

I think that under normal economic circumstances, LOAN will likely move back to the $7 to $8 range.

FINVIZ

So, what to make of this company?

Takeaway

LOAN, a mortgage REIT, is an intriguing investment option. Despite its small size, it has a track record of outperforming its peers in the industry, thanks to its high-quality loan book and competent management. The company is selective in its deals, ensuring that the risk/reward ratio is optimal.

The company offers an attractive 9% dividend, which is protected by its sound loan quality, even in times of elevated credit risks. However, I would not recommend LOAN to investors seeking high yields. The company's success is heavily dependent on a few managers, and the potential financial risks associated with its loan quality make it less appealing.

Rather, I prefer to invest in a more secure industry that offers lower yields. Although LOAN is a well-managed company that could provide high income to investors, the risk/reward ratio is not worth it. Furthermore, liquidity risks could arise due to its small size, making it difficult to buy or sell significant positions.

In summary, LOAN stock is a sound investment with the potential to reward investors with high income over an extended period. Nevertheless, due to its small size and potential financial risks, it may not be the best option for investors seeking high yields or those looking for a more liquid investment option.

For further details see:

Manhattan Bridge: Juicy 9% Dividend But A Risky REIT Play