RANJF - ManpowerGroup At Risk Of Becoming Dead Money

2023-09-27 06:11:39 ET

Summary

- ManpowerGroup is one of the largest staffing companies in the world.

- Yet, it has been struggling: top-line growth is non-existent, and its peers have grown larger.

- In this article, I want to go over the most recent data to show if the company can be a decent investment or not.

Introduction

The FED and interest rates. Inflation and the labor market. Everyone looks at the latest release with new data about these economic data.

One way I like to look at the labor market is by keeping track of how the main staffing agencies perform and what they say about their future outlook.

ManpowerGroup (MAN) was once the leader of this highly fragmented industry. Now it has been surpassed by Randstad (RANJF) and Adecco (AHEXF). However, it still a very important global player worthy of consideration, with revenues hovering around $20 billion.

Manpower is Stagnating

I have gone over Manpower several times . The industry is sensitive to changes in the level of economic activity. Staffing activity usually goes up in two different situations: at the beginning of an economic recovery or when future economic growth is uncertain, leading companies to be more cautious with direct hiring.

Manpower has three main segments: contingent staffing; professional resourcing (Experis) and talent development and management (Talent Solutions). The company is trying to shift more of its operations from staffing to the other two because they are higher value services giving higher margins.

Overall, Manpower hasn't been able to grow for more than a decade, as shown below.

{kind=link}

The Swiss competitor Adecco was having the same problem. However, its turnaround may have already started.

The industry is very asset light. This makes its players able to generate consistent free cash flow. However, we have seen how Manpower hasn't really been able to grow it.

{kind=link}

What happened in 2020? In my previous articles, I explained a key concept worth recalling. That year, because of the pandemic, many companies didn't need staffing and related services. Therefore, many contracts came to an end and had to be paid by the end of the year. As a result, the item known as accounts receivable significantly changed. In fact, if accounts receivable increases, we see a reduction on the cash flow statement because sales are increasingly paid with credit instead of cash. Seeking Alpha reports this as a negative number because it is a "use" of cash that is seen as an outflow. On the contrary, if accounts receivable decreases, then we see increasing cash on the cash flow statement, as the company has been paid in cash. Seeking Alpha shows this with a positive number. In fact, it is a cash inflow.

So, that spike in FCF was actually a negative signal because it came from contracts coming to an end without being renewed.

What we would like to see is a steadily growing FCF coming from revenue growth and increased operating efficiency.

Currently, Manpower sports a 4% dividend yield, paid semi-annually, well-covered by a payout ratio just below 38%. In the past 5 years its CAGR has been 8%. It won't take many years for the company to reach a high payout ratio if it keeps hiking the dividend at this pace.

Recent Financials

When Manpower reported its 2nd quarter's results , it had to admit the operating environment was challenging both in the U.S. and Europe, leading to revenues of $4.9 billion, a 4% decline YoY. With gross profit margin at 17.8%, net earnings in the quarter were $65.2 million, versus $122.2 million a year earlier. EPS came in at $1.29 versus $2.29 in the prior year period.

Now, EPS were reduced by $0.29 in the quarter because of restructuring costs and Argentina non-cash currency translation losses because of the hyperinflationary economy of the country.

In any case, on a constant currency basis, revenues were down 3% YoY.

To improve its profitability, Manpower decided to wind down its Proservia business in Germany because the outsourcing business is not part anymore of its core strategy.

Manpower's cash flow statement for the first six months of the year saw a similar decline that actually led to negative operating cash of $31.2 million because of $370 million reported as other liabilities. Nonetheless, the company used its cash balance to repurchase $80 million of common stock and pay another $73 million in dividends, ending with $407.6 million in cash. After a few days, the company announced a new share repurchase program up to 5 million shares, which means, at today's share price, a program worth around $365 million.

Now, what is behind can't be changed, though it gives us an understanding of how the company operates. Let's look now at what Manpower is expecting. In its report, Manpower had to acknowledge that it

observed softening demand for staffing services due to increased economic uncertainty, and we expect this trend to continue. We believe that downside risks to the global economic outlook have continued to increase through the second quarter of 2023, and may worsen in future periods.

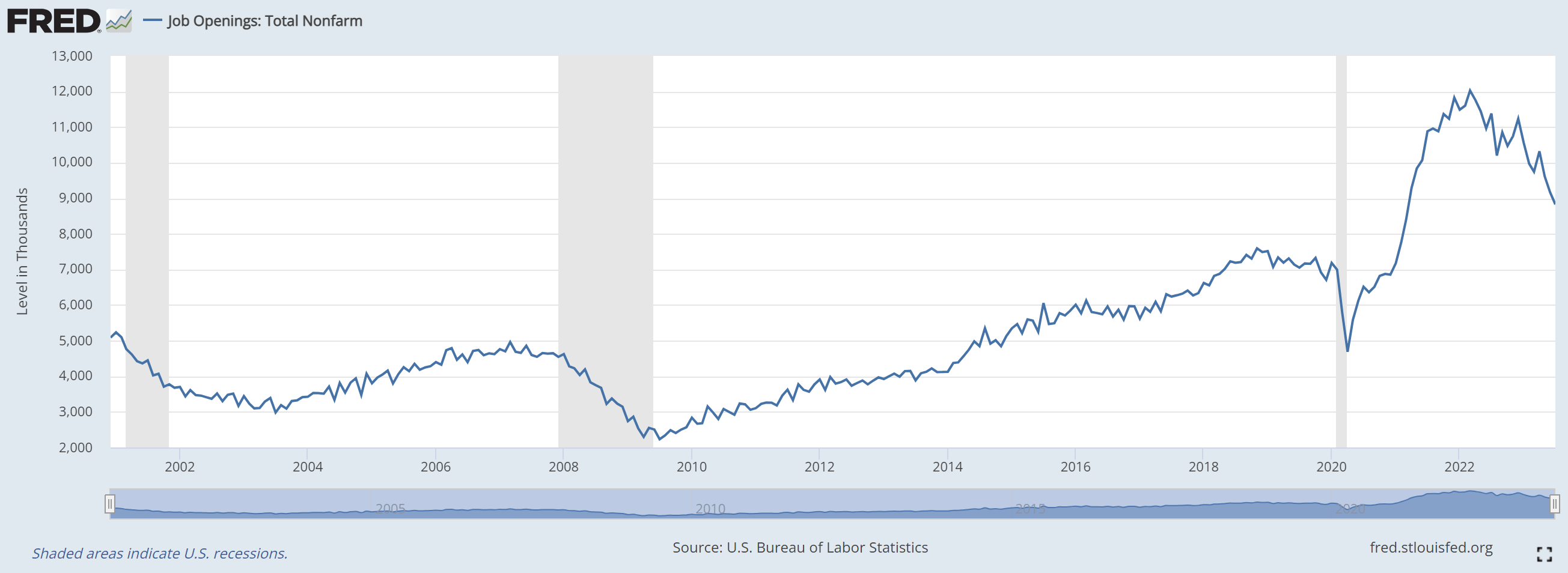

Quite a grim outlook. The FRED (Federal Reserve Bank of St. Louis), confirms this downward trend, which can be seen in the declining of new job openings in the U.S since the peak in early 2022.

{kind=link}

Yet, we can clearly see a still strong market, with job openings well above the usual range from 2000 to the pandemic.

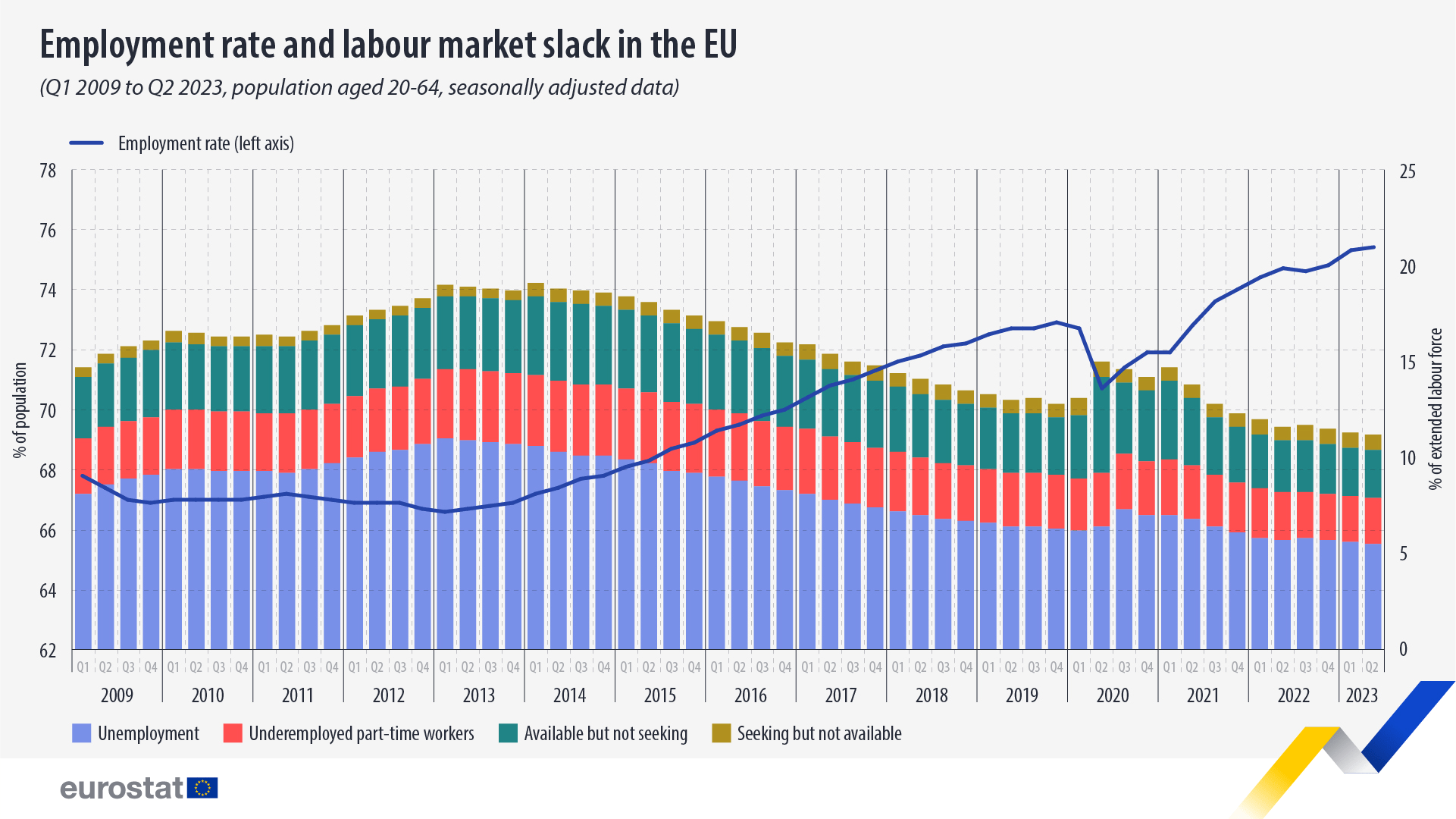

In Europe, the employment rate is high at 75.4%. However, labor market slack (the unmet demand for paid labor) amounted to 11.2%

{kind=link}

Overall, in the Western world, a slowing hiring trend is clear. In the meantime, the issue is the mismatch between demand and supply, with many companies seeking skills that workers don't have. This could actually create a favorable situation for Manpower's higher services business, focused at talent development and re-skilling processes.

Yet, during the last earnings call. Manpower reported weakness in these segments, as well.

Within Talent Solutions we saw a significant year-over-year revenue decline in RPO as we anniversaried high levels of permanent hiring across our key markets in the prior year period. Our MSP business saw revenue declines in the quarter as we reduced certain lower margin activity, while Right Management experienced significant revenue growth on higher outplacement volumes in the quarter compared to the record-low levels of activity in the prior year period. [...] Organic gross profit in our Experis brand decreased 13% in constant currency year-over-year. Permanent recruitment decreases within Experis drove the higher rate of overall GP decrease for the brand. Organic gross profit in Talent Solutions decreased 7% in constant currency year-over-year.

Now, even Randstad reported similar data. This shows the industry as a whole is suffering, though Randstad is still able to have a gross margin above 20%, while Manpower is well below.

Valuation

Manpower appears cheap, as Seeking Alpha valuation metrics show, giving it a B+. For sure, a TTM PE at 9.84 shows some value. Yet, as we look at the fwd PE we already move up to 12.33 signaling earnings estimates see Manpower still declining. We see that a B+ is also given to Manpower's dividend safety , with the dividend yield being graded with an A- and the dividend growth getting a B.

Yet, if we zoom out, I think we are before a value trap.

{kind=link}

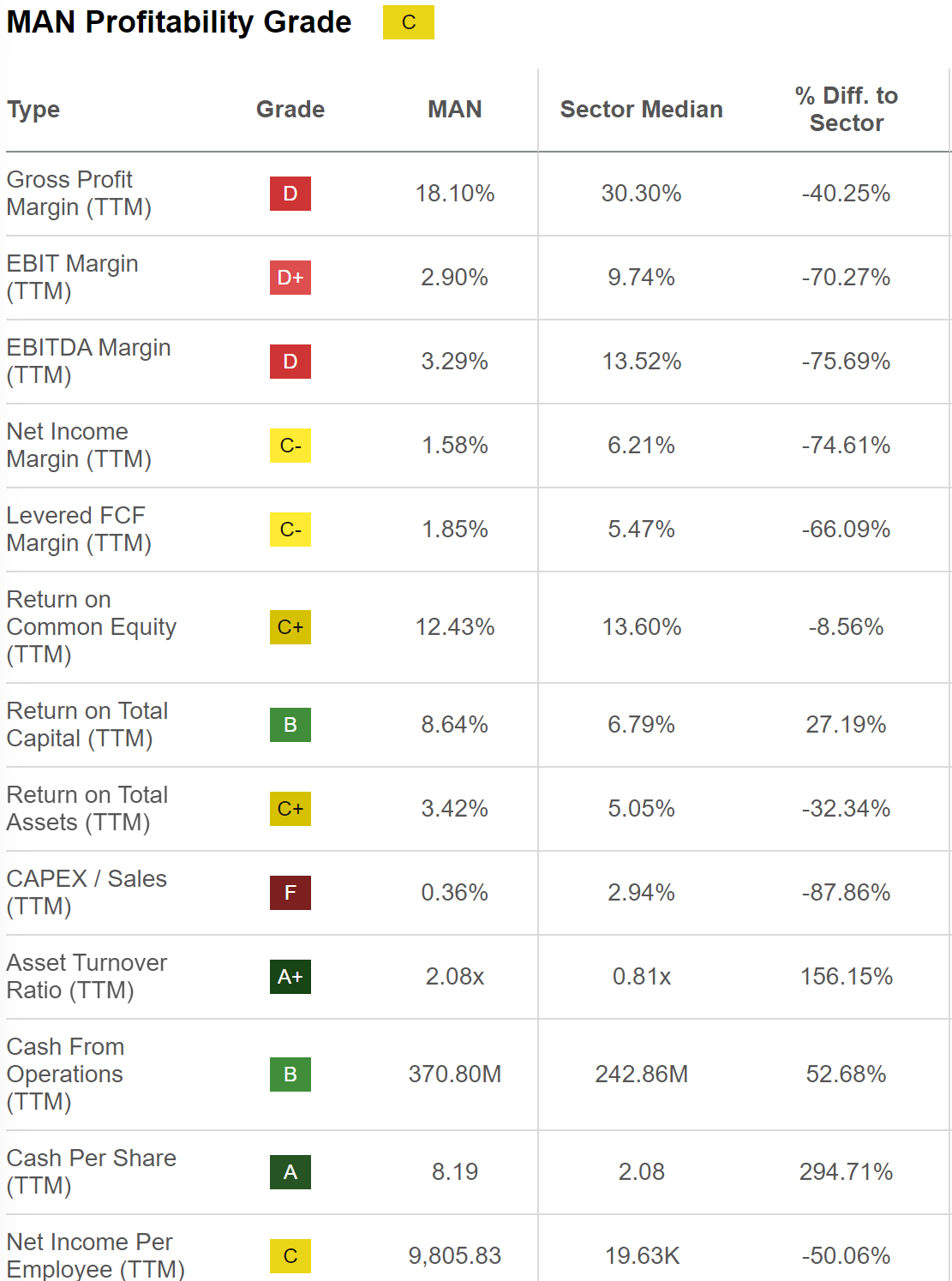

The overall profitability grade is a C. To me, profitability is much more important than valuation because a very profitable company can support a higher valuation while turning out as a great compounder over the long term.

While a C can be judged decent, a return on total capital of 8.64% is not enough to make Manpower enter my watchlist, where I want solid businesses with a return at least at 15%. In addition, I think it is concerning that Manpower has margins from 40 to 70% below the sector median.

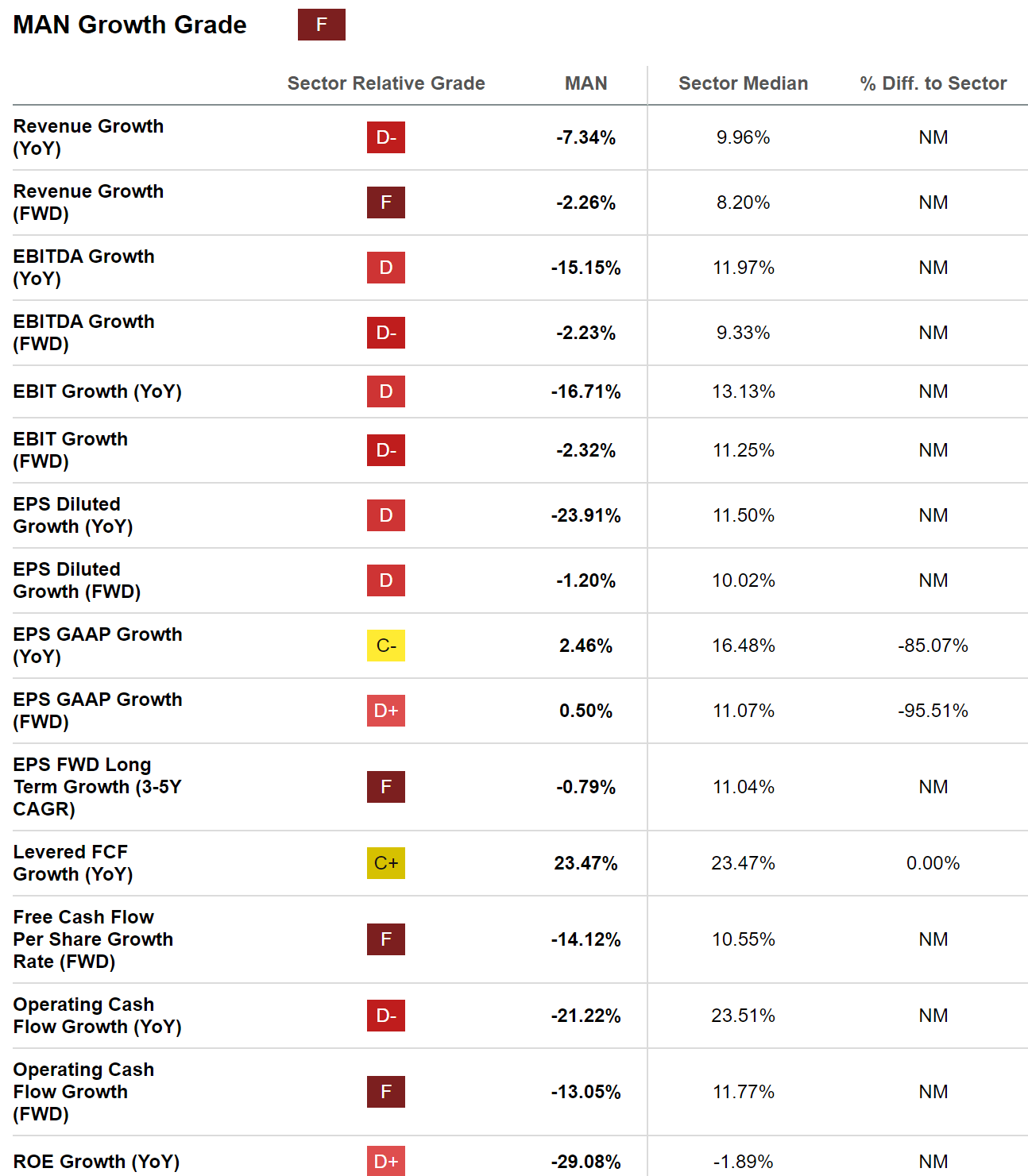

While some investors can believe Manpower's profitability is ok, here is what makes the company an investment at high risk of being dead money for many years to come. Manpower has not been growing and it rightly gets an F as its growth grade.

{kind=link}

The picture is quite clear. Manpower stagnates and, in the meantime, it is not becoming more efficient. I don't have an issue with top-line stagnation if the bottom-line improves or if the company has become so mature that it generates a constant stream of cash flow for its shareholders. Manpower, unfortunately, doesn't offer neither of these.

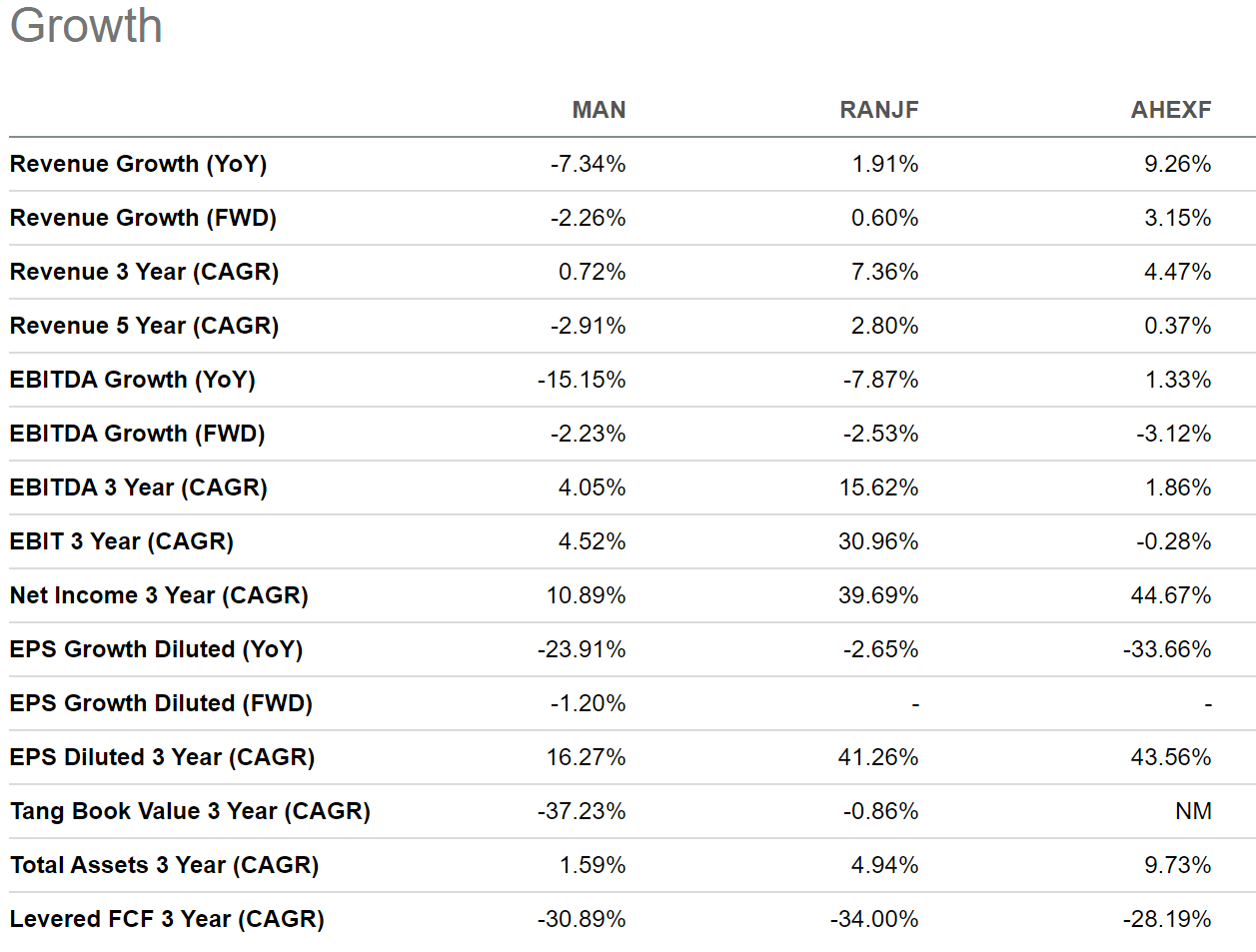

For clarity's sake, let's compare Manpower to its two main peers , Randstad and Adecco.

No matter how we look at it, Manpower severely underperforms its two main peers, with negative YoY revenue growth even both YoY and over 5 year. If we look at the 3 year CAGR growth, we are in stagnation territory with 0.72% vs. 7.36% achieved by Randstad and 4.47% by Adecco.

{kind=link}

As Manpower's revenue stagnates, its EBITDA seems to suffer as well, with YoY EBITDA down 15.15%. Net income growth is positive, but much below its peers, with Manpower having a 3 year net income CAGR at 10.89% while Randstad is almost at 40% and Adecco almost at 45%.

At the same time, Manpower has been overcome by Randstad even when looking at return on total capital, which was a traditional metric Manpower had above its two peers. In addition, it seems 2022 and 2023 have caused it to suffer more than Randstand and Adecco, which is actually improving its ROTC.

{kind=link}

All in all, Manpower lacks what I think is the right engine to become a true cash cow, bringing in a constant inflow of cash. This is why I think it is not correct to see its price/FCF multiple above Randstad's, given the very different situation the two companies are in.

{kind=link}

I haven't found in the recent earnings call any real fact that makes me think the company can quickly turn around the situation. A recent survey conducted by Manpower to collect the data for the employment outlook saw employers taking a "calculated approach to hiring", which is not exactly a tailwind for Manpower.

Therefore, given its lack of growth compared to the efforts Adecco has undertaken following Randstad, I believe Manpower's position in the industry is deteriorating. Not even a 4% yield can be a good enough reason to invest in a stock, in particular when bonds are yielding over 4% and are much safer. Better move away from it.

For further details see:

ManpowerGroup At Risk Of Becoming Dead Money