MAN - ManpowerGroup: Performance And Forecast Impacted By Macroeconomic Challenges

2023-10-30 21:09:08 ET

Summary

- ManpowerGroup Inc.'s third-quarter results showed a decline in revenues due to economic uncertainties and reduced demand for staffing services in North America and Europe.

- The company's adjusted EBITA also declined significantly, influenced by restructuring and hyperinflationary effects.

- The outlook for ManpowerGroup remains cautious, with anticipated challenges in Europe and Israel, leading to a hold rating for the company.

Summary

Readers may find my previous coverage on ManpowerGroup Inc. ( MAN ) via this link . My previous rating was a hold, as I believed ManpowerGroup’s near-term share price would be significantly impacted by the short-term weakness due to the new guidance and persistently high inflation in the Europe region. I am reiterating my hold rating on MAN, given the vulnerabilities highlighted in their third quarter results and insights from the earnings call, both for the present and the forthcoming quarter.

Valuation

Based on my view of the business, I project a 6% decline in MAN’s revenue for FY23. This projection aligns with the midpoint of the guidance provided by management during their earnings call . For FY24, I expect a modest growth of 1%, consistent with market predictions. My assumptions are driven by several factors. In the third quarter, MAN experienced a dip in revenues, attributed to economic uncertainties that prompted organizations to maintain their existing workforce and curtail their dependence on staffing services, particularly in North America and Europe. The adjusted EBITA also witnessed a notable decline, influenced by restructuring and the hyperinflationary effects in Argentina. Furthermore, the subdued demand from technology clients suggests potential headwinds in the tech sector, putting pressure on MAN’s revenue prospects.

Geographically, while the U.S. showed resilience, MAN faced difficulties in Europe, where restructuring costs and declining revenues in crucial markets like the UK were prominent. Moving forward, the company's outlook remains guarded, with anticipated hurdles extending into the subsequent quarter, notably in Europe and Israel. This outlook, coupled with a predicted deceleration in recruitment endeavors and anticipated drops in earnings and revenue, highlights the challenges MAN faces, reinforcing a hold rating.

Based on author's own math

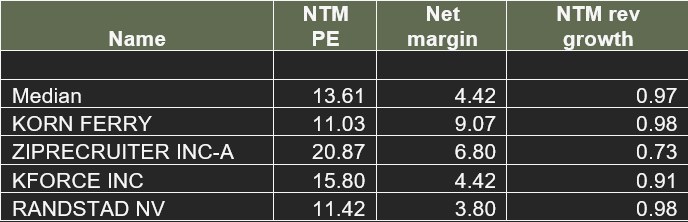

Peers overview:

{kind=link}

Currently, MAN is trading at a forward Price/Earnings ratio of 12x, which is below its peer median of 13.61x. This lower valuation seems justified considering its net margin of 2.23% is beneath the peer median. Additionally, its projected growth rate for the next 12 months is a negative 3%, aligning with its peers. Given the modest 2% implied upside, I continue to recommend a hold rating for MAN in this period.

Comments

During the third quarter , MAN reported somewhat lackluster performance The revenue for the third quarter was $4.7 billion, marking a 5% year-over-year decline in constant currency. The decline in revenue was driven by increased economic uncertainty and headwinds, which caused organizations to hold onto their existing permanent workforce and reduce their reliance on staffing and permanent recruitment services, especially in North America and Europe. In addition, it's important to note that the adjusted EBITA experienced a significant decrease, dropping by 36% in constant currency terms when compared to the same period in the previous year, driven by factors like restructuring, Argentina's hyperinflationary foreign exchange charges, and a small loss on sale. The reported EBITA margin was 1.7%, and the adjusted EBITA margin was 2.5%.

During the earnings call, it was highlighted that the demand from enterprise technology clients continued to be subdued during the quarter. This subdued demand was observed both in the U.S. and in Europe. The overall sentiment was that the tech demand was not as robust as they might have hoped for. This is an indication of broader challenges in the tech sector or specific challenges faced by MAN in meeting the demands of its tech clients, which will have a direct impact on its revenue outlook. From a geographical perspective, while there was sequential stability in the U.S. for the third quarter heading into the fourth quarter, the global view presented a different picture. Specifically, while Talent Solutions and Experis remained stable on a global scale, the MAN brand showed signs of weakness. This weakness was predominantly observed in Europe.

Additionally, there were restructuring charges in Europe, with $15 million being attributed to Germany. This was largely related to head office rightsizing and activities associated with the ongoing winddown of Proservia. The Nordics saw a restructuring charge of $7 million, mainly due to workforce optimization. There were also modest additional charges in the UK, the Netherlands, and Belgium. Specifically, in the UK, which is the largest market in the Northern Europe segment for MAN, there was a 15% decrease in revenues on a days-adjusted constant currency basis during the quarter. This was a further decline from the 12% decrease observed in the second quarter.

Based on the observed trends in the third quarter and the activity in October, MAN's forecast for the upcoming period is cautious. The company anticipates that the challenges faced in the third quarter will persist into the fourth quarter. Specifically, there are expectations of further declines in their MAN businesses in Europe. The forecast also highlights concerns regarding their Israel business, which is expected to see a significant reduction in activity due to the ongoing conflict in the region.

Another area of concern is the permanent recruitment activity, which is expected to continue slowing down. However, the company is taking cost-cutting actions to offset these challenges. For the fourth quarter, MAN is forecasting underlying earnings per share to be in the range of $1.17 to $1.27. This projection includes an unfavorable foreign currency impact of $0.01 per share. In terms of revenue, the company's constant currency guidance range indicates a decrease between 4% and 8%. At the midpoint, this represents a 6% decrease. Factors such as net dispositions and fewer working days contribute to an organic days-adjusted constant currency revenue trend of about a 5% decrease.

Risk & conclusion

A potential upside to my hold rating is if inflation recedes to below the Fed's target rate of 2%. Should inflation align with the Fed's target, it would likely deter further interest rate hikes. Historically, interest rates and economic growth have had an inverse relationship. A reduction in interest rates typically stimulates economic growth, which in turn can boost hiring. Such a scenario would positively influence MAN’s prospects and its share price.

In the third quarter, MAN exhibited a subdued performance, with revenues declining due to economic uncertainties that led businesses to retain their workforce and reduce dependency on staffing services, particularly in North America and Europe. Restructuring, hyperinflationary effects, and other factors all contributed to a significant decline in the company's adjusted EBITA. There was a noticeable dip in demand from technology clients, suggesting challenges in the tech sector that could impact MAN’s outlook. Geographically, while the U.S. remained stable, the MAN brand faced challenges in Europe, with restructuring charges and revenue declines in key markets. The company's outlook for the upcoming period is cautious, expecting these challenges to continue, especially in Europe and Israel. Given the modest implied upside and the challenges mentioned above, I maintain my hold rating for the company.

For further details see:

ManpowerGroup: Performance And Forecast Impacted By Macroeconomic Challenges