TNET - ManpowerGroup: Upside Still Exists Despite Concerns Over Weakness

Summary

- ManpowerGroup may have seen revenue fall recently, but profits and cash flows are looking nice.

- Weakness has been an issue on the sales front, and the picture looks set to worsen in the quarters that lie ahead.

- Even so, shares are cheap, and the company offers additional upside from here.

Buying into attractively-priced companies can be a fantastic way to generate positive returns in the market. One really good example that I could point to in this regard is human resources firm ManpowerGroup ( MAN ). At its core, the company offers workforce solutions and services to its customers, with its network extending through 75 different countries and territories. Recently, we have seen some weakness in the company's bottom line. But that has not stopped the firm from generating robust cash flows and appreciating nicely compared to what the broader market has experienced. Although I do expect some additional weakening to occur in the quarters to come, shares are priced low enough now that they offer an attractive upside even after outperforming the broader market over the past several months. Because of this, I have no problem keeping it at the 'buy' rating I had it at previously.

Great results, all things considered

Back in the middle of April 2022, I wrote an article discussing the investment worthiness of ManpowerGroup. In that article, I talked then about how the company did not look like an excellent firm. At the same time, however, shares of the business were trading on the cheap. When factoring in the totality of the picture, I felt as though the risk-to-reward ratio for shareholders in the company looked favorable. This ultimately led me to rate the company a 'buy', which reflected my belief at the time that shares should outperform the broader market for the foreseeable future. So far, that call has proven to be pretty accurate. While the S&P 500 is down 10.6%, shares of ManpowerGroup have generated an upside of 2.2%.

{kind=link}

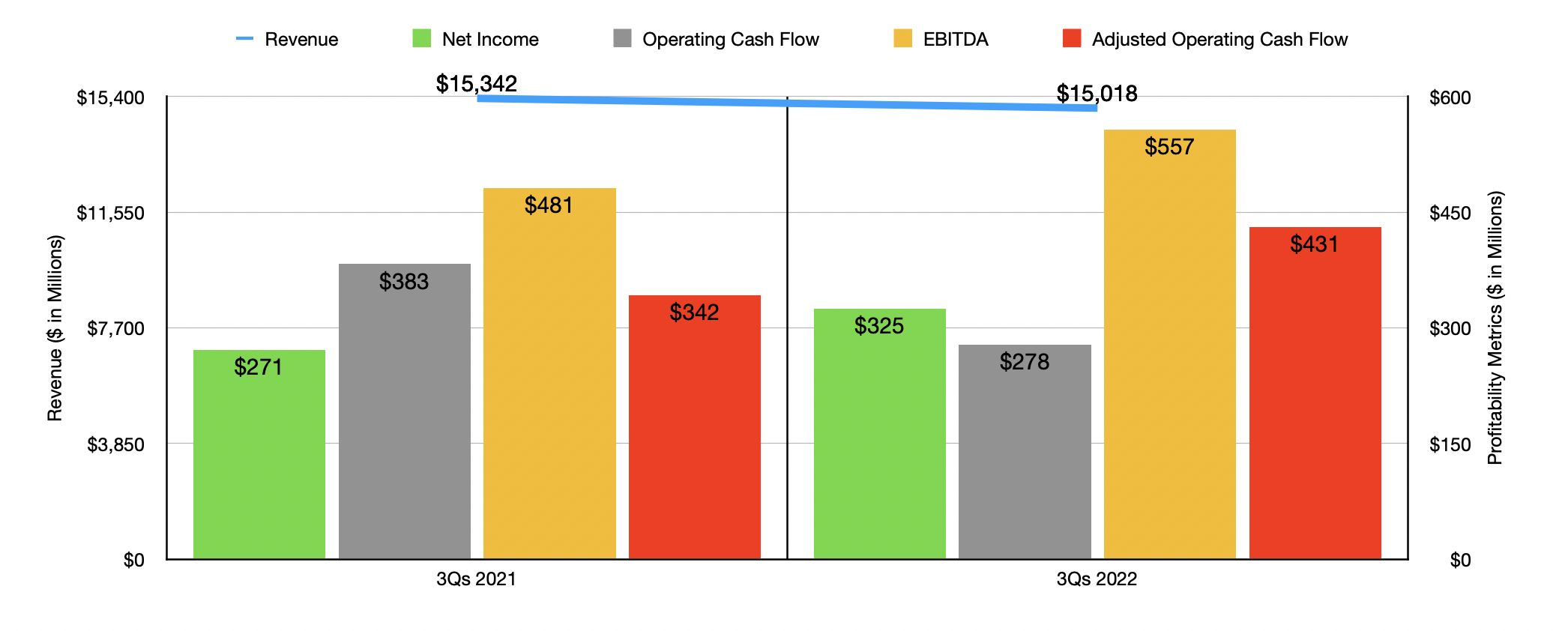

For the most part, this return disparity seems warranted. Consider, for instance, how the company performed during the first nine months of its 2022 fiscal year. Yes, sales did weaken year over year, dropping by 2.1% from $15.34 billion to $15.02 billion. At first glance, this looks rather painful. But it's worth noting that, on a constant currency basis, sales growth would have been 6.9%, with organic constant currency revenue rising 3.6%. The pain for the enterprise, then, was driven pretty much entirely by foreign currency fluctuations. This is not to say that there was not some weakness elsewhere. For instance, in France, which is the largest market that the company has in its Southern Europe region of operations, reported a revenue decline of 6.8%. Although this number would have been positive on a constant currency and organic constant currency basis, the firm did cite supply chain constraints as a factor that negatively impacted demand for its staffing services. In Northern Europe, revenue was hit even harder, falling 11.9%. This was actually the only major area in which, on a constant currency basis, sales weakened, falling 1.5% year over year. This was largely due to the sale of its operations in Russia and reduced demand for its services and other nations.

Even though the company experienced some pain on its top line, bottom line results have largely been positive. Net income, for instance, totaled $325.1 million in the first nine months of the company's 2022 fiscal year. This represents a sizable improvement over the $271.3 million generated the same time one year earlier. Operating cash flow, unfortunately, fell year over year, dropping from $382.9 million to $289.2 million. But if we adjust for changes in working capital, it would have risen from $342.1 million to $430.8 million. And over that same window of time, EBITDA for the business also increased, rising from $481.2 million to $557.4 million.

{kind=link}

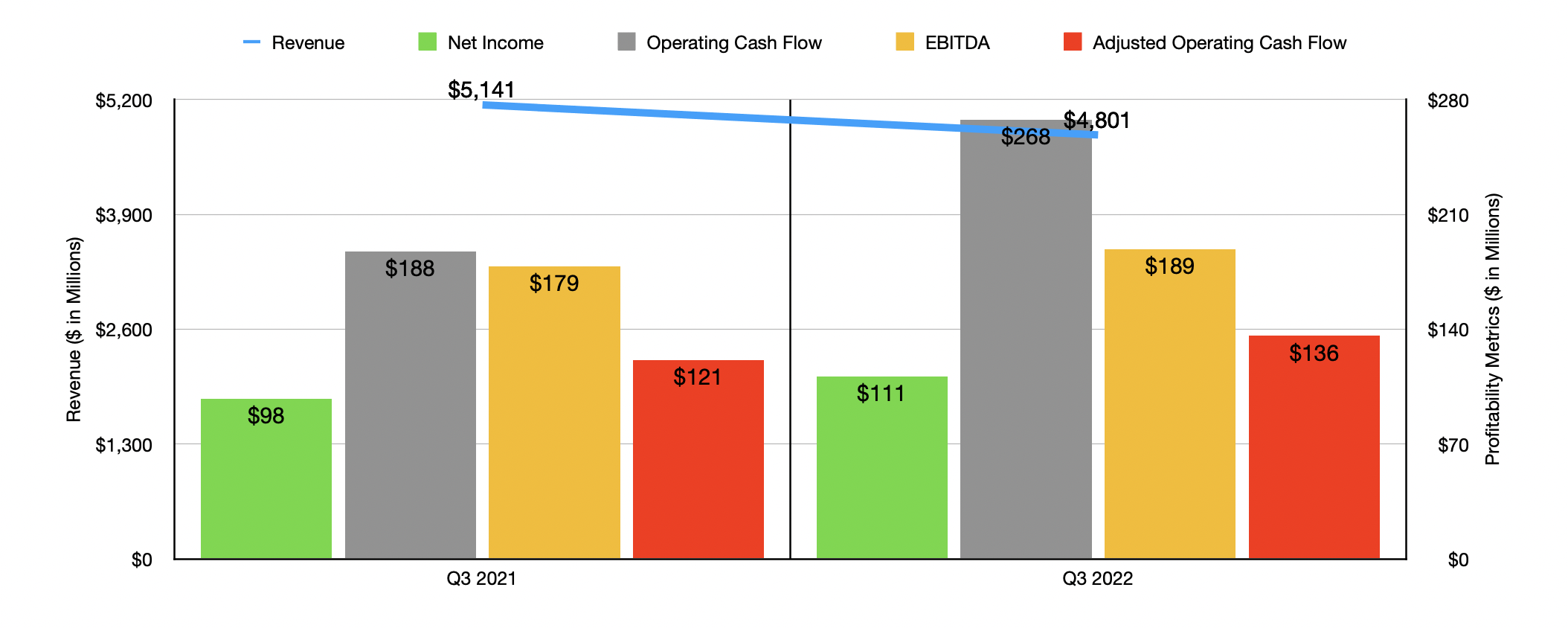

The results experienced in the first nine months of 2022 look very similar to the results experienced in the third quarter alone. Revenue of $4.80 billion was lower than the $5.14 billion reported at the same time one year earlier. On the other hand, net income rose from $97.7 million to $111.3 million. Operating cash flow actually increased in this case, jumping from $187.5 million to $267.9 million, while the adjusted figure for this inched up from $121.3 million to $136 million. And finally, EBITDA for the company also improved, rising from $178.5 million to $188.8 million. In the most recent data provided by management, the firm did warn that some signs of softening are beginning to show in hiring. This comes even as the hiring outlook remains strong in the US.

When it comes to the 2022 fiscal year in its entirety, management did say that earnings per share should be between $2.11 and $2.19 for the final quarter. That is in spite of the fact that foreign currency fluctuations should impair the company to the tune of $0.38 per share. This would imply a net income, using midpoint figures, of $437.5 million for the entirety of 2022. Management has not provided guidance when it comes to other profitability metrics. But if we annualize results experienced so far in the first nine months of 2022, we would anticipate adjusted operating cash flow of $641.2 million and EBITDA of $763.1 million.

{kind=link}

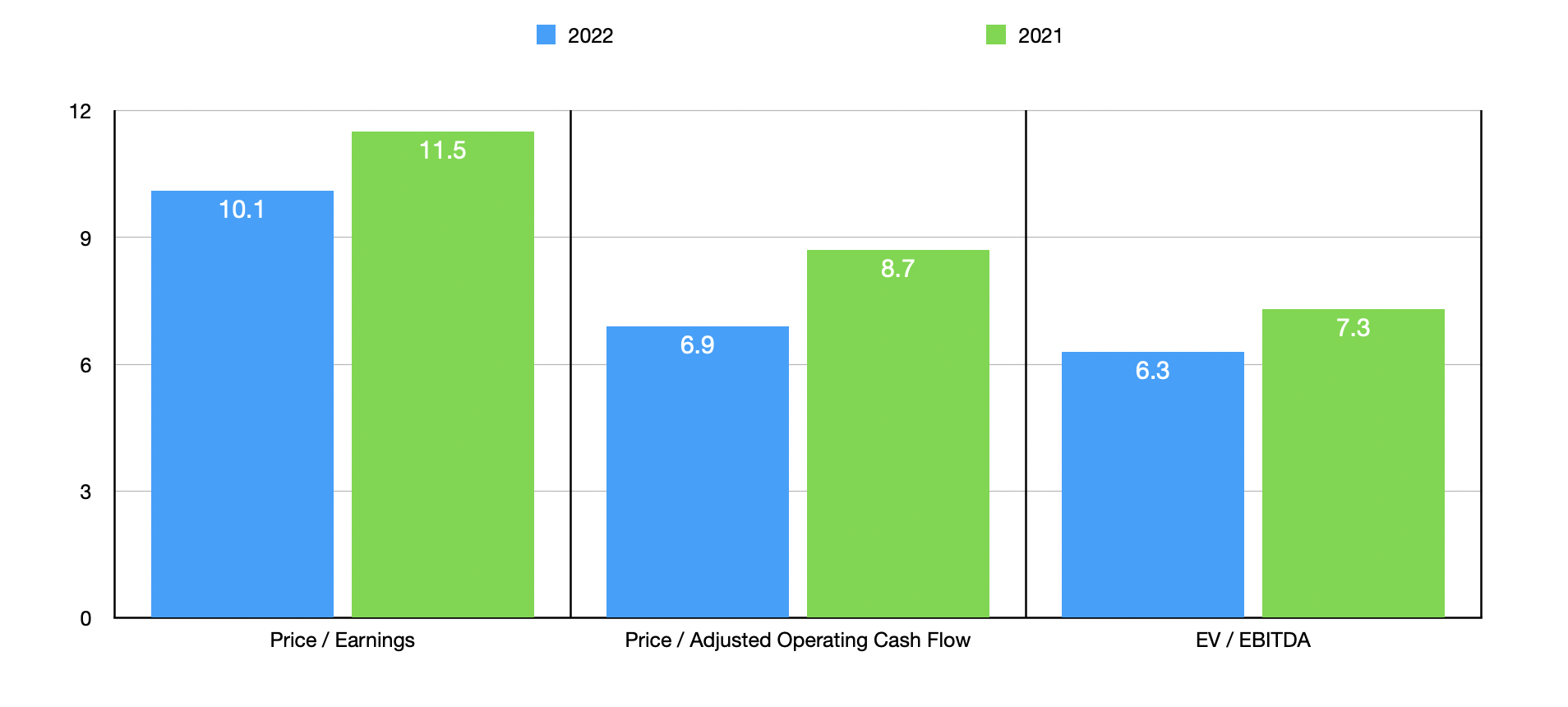

Based on these figures, the company is trading at a forward price-to-earnings multiple of 10.1. The forward price to adjusted operating cash flow multiple should be 6.9, while the forward EV to EBITDA multiple looks to be 6.3. As you can see in the chart above, shares are now cheaper than what we would get if we were to use data from the 2021 fiscal year. But even reverting back to those numbers would not be a sign of the stock is anything other than undervalued. Shares of the company are also cheap relative to similar firms. As you can see in the table below, I compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 8.7 to a high of 55.2. Using the price to operating cash flow approach, the four companies with positive results ranged from a low of 6.3 to a high of 29.5. And when it comes to the EV to EBITDA approach, the range was from 4.6 to 15.2. In all three cases, only one of the five companies was cheaper than our prospect.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| ManpowerGroup |

| 10.1 |

| 6.9 |

| 6.3 |

| TriNet Group ( TNET ) |

| 12.7 |

| 15.4 |

| 6.8 |

| ASGN Inc. ( ASGN ) |

| 14.9 |

| 29.5 |

| 8.0 |

| Insperity ( NSP ) |

| 28.6 |

| 13.2 |

| 15.2 |

| Alight ( ALIT ) |

| 55.2 |

| N/A |

| 13.0 |

| Korn Ferry ( KFY ) |

| 8.7 |

| 6.3 |

| 4.6 |

Takeaway

From what I can see, looking at the data, investors should be prepared for a slowdown in activity that could impact ManpowerGroup over the next several quarters. This may deter some investors from buying into the stock. Certainly, for those who want to time the market, now might not be the greatest time to buy. But the fact of the matter is that shares of the company look cheap, both on an absolute basis and relative to similar firms, and the market for its services will ultimately recover. Given these factors, I have no problem rating the company a 'buy' just like I did previously.

For further details see:

ManpowerGroup: Upside Still Exists Despite Concerns Over Weakness