KELYB - ManpowerGroup: Various Challenges Facing The Job Market

2023-10-02 06:53:31 ET

Summary

- ManpowerGroup operates in a competitive industry facing changing dynamics, contributing to growth stagnation.

- The business has a good business model but is unable to generate a financially accretive moat.

- The company has experienced 5 consecutive quarters of negative growth and we do not see growth materially returning in the near future.

- Despite the weak financial performance, MAN is trading at an NTM premium to its historical average. This implies it is slightly overvalued.

Investment thesis

Our current investment thesis is:

- MAN operates in a highly competitive industry that is experiencing changing dynamics, as technology increasingly encroaches on the traditional model. We believe MAN is positioned to maintain its current position but its "slice of the pie" will continue to be threatened. This has contributed to growth stagnation.

- Current economic conditions are weighing on the business, with 5 consecutive quarters of negative growth. We do not see growth returning in the immediate future.

- MAN is trading at a premium to its NTM historical average despite the weak financial performance. We do not currently see upside.

Company description

ManpowerGroup ( MAN ) is a global workforce solutions provider, offering a range of services including temporary staffing, permanent placement, workforce management, and talent development. The company operates across various industries and geographies.

Share price

MAN's share price performance during the last decade has been underwhelming, as a lack of financial development in conjunction with a reasonable valuation has contributed to a lack of multiple expansions.

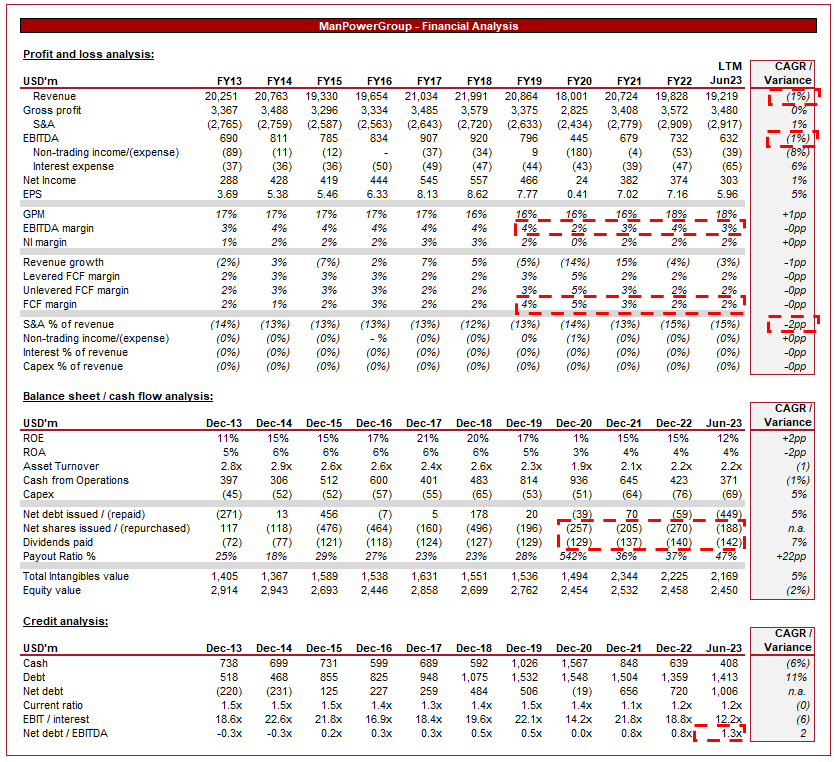

Financial analysis

Manpower Group financials (Capital IQ)

{kind=link}

Presented above is MAN's financial performance.

Revenue & Commercial Factors

MAN's revenue has been flat during the last 10 years, with a (1)% CAGR and 5 fiscal years of negative growth. This is a reflection of the difficult period the company has faced, yet has comfortably maintained its existing level.

Business Model

MAN offers a range of workforce solutions, including temporary staffing, permanent placement, workforce consulting, talent development, and outsourcing services. The company's object is to assist businesses in navigating workforce challenges and optimize their human capital strategies. These services are provided through 3 key segments.

{kind=link}

The expansion of services provided to deepen its integration within a corporate's operations is a natural development, as it allows MAN to improve its economics by delivering more value-added services. Currently, 56% of GP is from Manpower and 44% is from Experis and Talent Solutions. The latter have delivered growth and margin improvement, while Manpower enhances the company's brand and expertise within the industry.

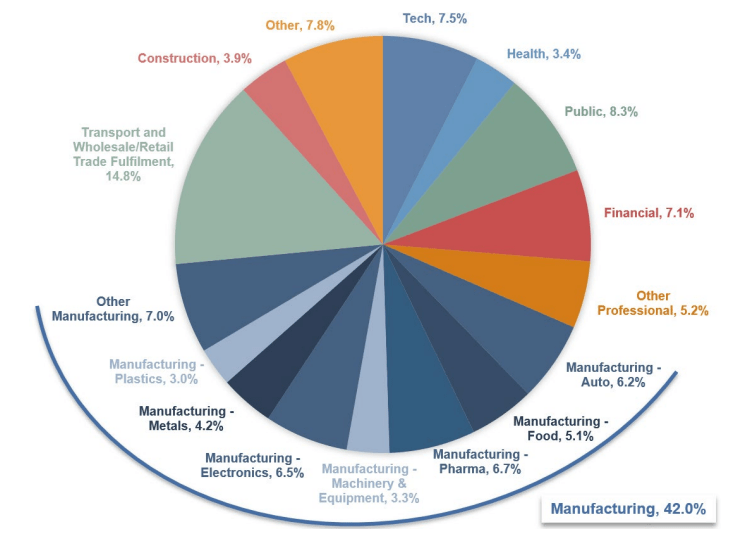

MAN serves a diverse client base across various industries, including manufacturing, finance, healthcare, technology, and more. Its broad range of services allows it to cater to the specific needs of different industries and from an operational perspective, maximizes its earnings potential and value from its brand. Its reliance on manufacturing is primarily the reason for its robust (while underwhelming) growth, with consistent demand for individuals in a labor-intensive industry with high turnover.

{kind=link}

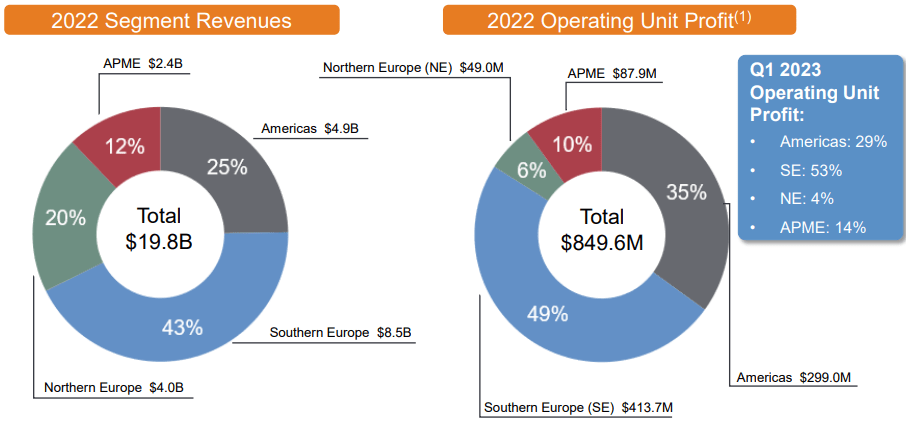

MAN operates in multiple countries around the world, allowing it to tap into global labor markets and offer solutions tailored to regional workforce dynamics. This is a critical quality of the company, as the demand for roles is highly correlated with the economic development of a country. Operating across several regions allows for diversification benefits.

Revenue by geography (Manpower Group)

{kind=link}

Similar to its peers, MAN focuses on talent development and upskilling, helping individuals acquire the skills needed for the evolving job market. This aligns with the growing importance of reskilling and upskilling in the face of technological advancements, as many industries experience a shortage of employees. This effort increases the ability of MAN to successfully deliver on mandates.

MAN leverages its access to labor market data and trends to provide insights that help businesses make informed workforce decisions. Beyond this, the company has developed a "HR tech stack", providing broad workforce expertise to HR teams. This can further support its value proposition, allowing for margin improvement and reduced reliance on incrementally filling more roles.

{kind=link}

Competitive Positioning

Man's key competitive advantages are:

- Brand. MAN's brand is synonymous with HR/workforce services, providing trust to potential clients that it is able to deliver on their needs to a high quality.

- Deep expertise. MAN's industry expertise allows it to support clients with HR needs, tailoring its services to add value, rather than simply acting transactionally (filling roles only).

- Global reach. MAN's global presence is highly valuable for multinationals that are seeking a global partner to support their HR needs.

- Talent pool. MAN's access to staff seeking employment is critical to its ability to deliver on mandates. This relates to the brand point above, as MAN's reputation for a high quantity of roles ensures that individuals seeking jobs will consider it.

This said, there is clearly a reason the business has lacked growth. We believe the following factors are key barriers and contributors to reduced activity:

- Changes in labor market dynamics. Global labor markets have materially changed in the last decade, such as the rise of the gig economy, and an increasing number of corporates taking recruitment activities in-house.

- Automation and Technology. The rise of automation and technology-driven recruitment activities is threatening the traditional model. LinkedIn ( MSFT ) has taken significant market share from the traditional recruitment agencies, allowing corporates to easily engage with individuals directly. Our view is that automation in conjunction with AI could further reduce the relevance of recruitment firms.

- Remote Work Trend. The acceleration of remote work arrangements due to the pandemic has changed employee motivations, contributing to disruption in the labor force.

- Competition. The workforce solutions industry is highly competitive, with both traditional players and new entrants vying for market share. The lack of ability to develop a wide moat has restricted MAN's ability to achieve competitive improvement, particularly as the industry is highly fragmented globally. ManpowerGroup competes with companies such as Adecco Group ( OTCPK:AHEXF ), Randstad ( OTCPK:RANJF ), and Kelly Services ( KELYA ).

Economic & External Consideration

Current economic conditions represent near-term headwinds for MAN. The business performed extremely well following the pandemic period, as resilient conditions contributed to rapid wage inflation and recruitment, as supply lagged demand. This has broadly normalized, contributing to high inflation.

This is having the opposite effect now, with demand slowing and monetary action taken to compound this further. This discourages recruitment due to the fear of reduced future demand.

MAN is feeling the impact of this, with 5 consecutive quarters of negative growth. During this period, margins have slightly contracted, reflecting the degree to which the business is struggling. In the most recent quarter, revenue declined (4.3)%, with OPM down (1.4)% YoY.

We suspect revenue performance will continue to be disappointing, with unemployment levels broadly leveling off in MAN's markets. Improvement will come as expansionary policy returns, which is likely to be in late 2024.

Margins

MAN operates with slim margins, that reflect the highly competitive nature of the industry. MAN's margins have traded flat during the historical period and we do not believe there is scope for material improvement, as it is a labor-heavy business and so will see costs scale proportionately.

Balance sheet & Cash Flows

Cash flows have been utilized aggressively to distribute to shareholders, with consistent dividends and buybacks. Despite the poor profitability, the business has consistently generated an attractive yield. With the company conservatively financed, this is likely sustainable going forward (although current levels may need to soften due to demand).

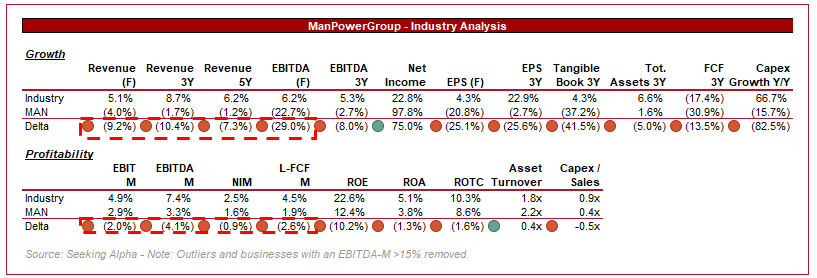

Industry analysis

Human Resource and Employment Services Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of MAN's growth and profitability to the average of its industry, as defined by Seeking Alpha (19 companies). We have heavily adjusted this cohort to capture comparable companies, given the cohort includes highly profitable tech businesses.

MAN's performance is underwhelming, with lower growth and margins. Even when we consider the business on an ROE basis, it is materially lacking. This is a reflection of the commoditized nature of its specialty.

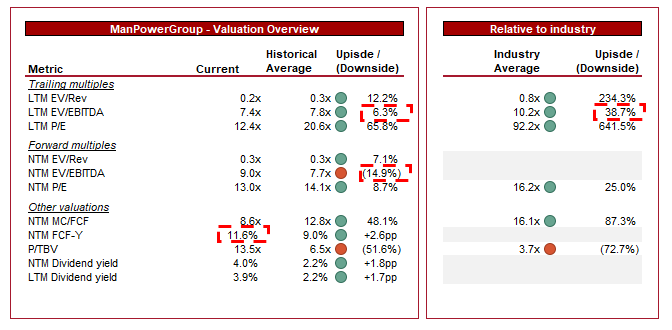

Valuation

{kind=link}

MAN is currently trading at 7x LTM EBITDA and 9x NTM EBITDA. This is a premium to its historical average on a NTM basis.

A premium to its historical average is unjustifiable in our view. The company's commercial profile is essentially unchanged during this period, with revenue growth continuing to be mild and margins flat. A discount to the industry average is correct in our view, as this would adequately factor in the weaker financial performance.

Based on this, we do not observe any material upside. The 39% EBITDA discount to its peers is reasonable without implying upside while the premium to its historical NTM EBITDA feels unreasonable. This assessment is compounded by the headwinds ahead and the general unattractiveness of its industry.

Final thoughts

MAN's capital allocation strategy has allowed the business to generate good returns relative to its financial performance. The company has seen growth and margin stagnation, characteristics we do not believe will be alleviated.

The business does show hints of attractiveness, namely a FCF yield of 12%, but we broadly consider the stock unattractive. There is no ability to materially grow a financially beneficial moat while the company continues to face intense competition.

For further details see:

ManpowerGroup: Various Challenges Facing The Job Market