MFC:CC - Manulife: Time To Take Some Profits

2023-12-19 01:10:09 ET

Summary

- Manulife Financial Corporation's shares have outperformed the S&P 500 and iShares US Insurance ETF by over 11.5%.

- The company's Q3-2023 results showed strong APE sales and a 35% increase in core earnings per share.

- Underneath those numbers, there are some big detractors from the core earnings.

- We tell you why we took the preferreds off the board, and why it might be time to consider doing the same with the common.

Note: All amounts discussed are in Canadian Dollars unless disclosed otherwise.

On our last coverage of Manulife Financial Corporation ( MFC ) ( MFC:CA ) we weighed in on the common and preferred shares. For the common, we looked at it from every angle and felt that you were unlikely to get poor returns from that entry point. The valuation was modest, and the only real risk was a protracted bear market. The shares have delivered spectacularly since then and even beaten the AI-bloatware loaded S&P 500 ( SPY ). The shares have even beaten the iShares US Insurance ETF ( IAK ) by over 11.5% or close to 50% annualized.

We examine the Q3-2023 results and tell you why you may want to look to book profits. We also go over why we sold out of our preferred shares.

Q3-2023

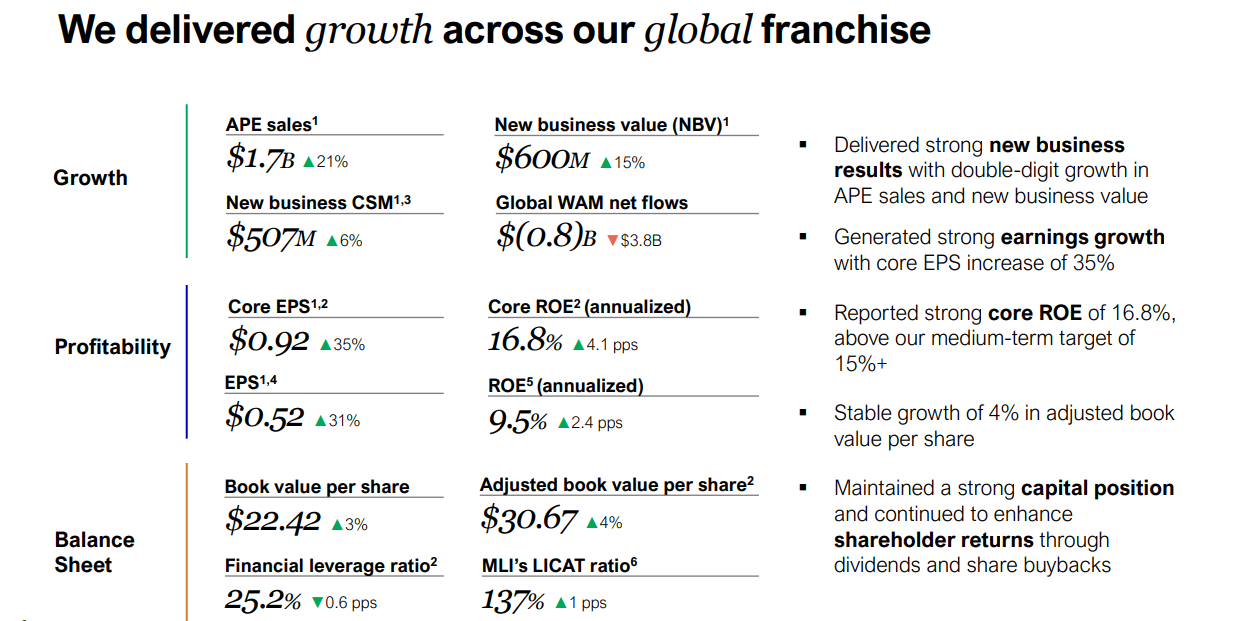

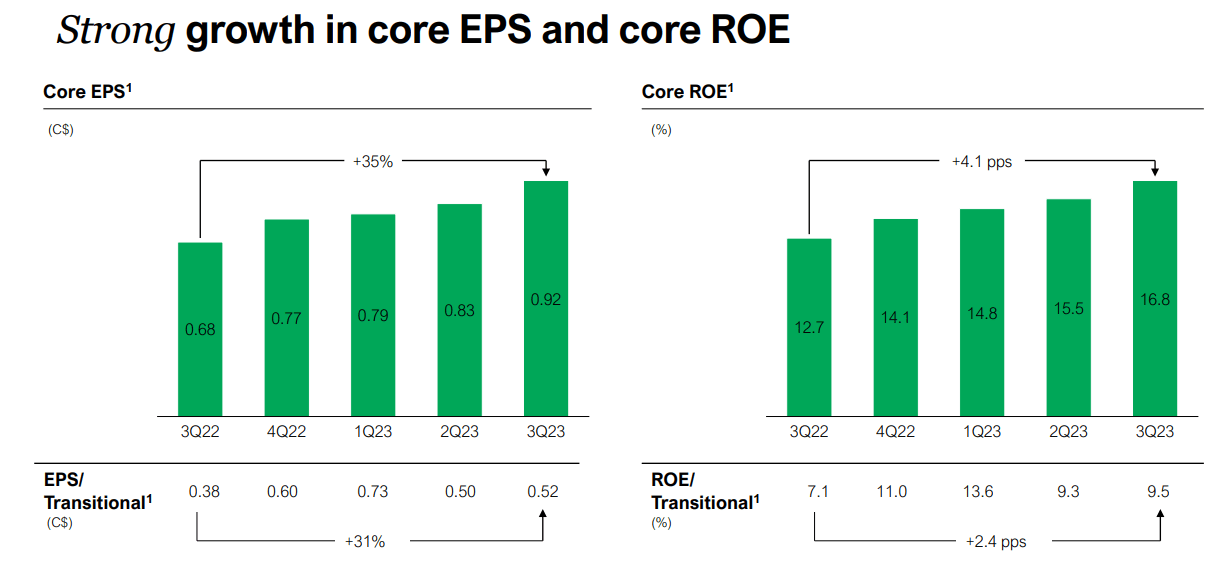

Manulife delivered what appeared to be a solid quarter. The company highlighted strong APE sales and a core earnings per share of 92 cents a share. The latter was up 35% year over year.

{kind=link}

With Manulife you always have a lot of variation between the reported and "core" numbers. The company shows that the core numbers keep moving up over time and that is what one should focus on.

{kind=link}

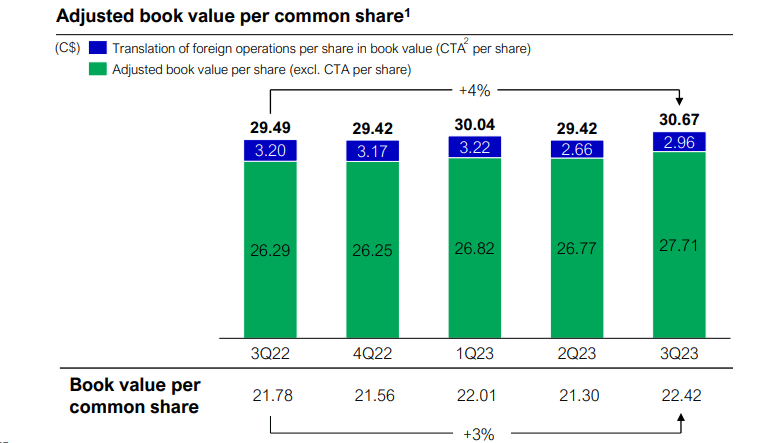

It also highlights that adjusted book value per common share tends to rise steadily over medium periods.

{kind=link}

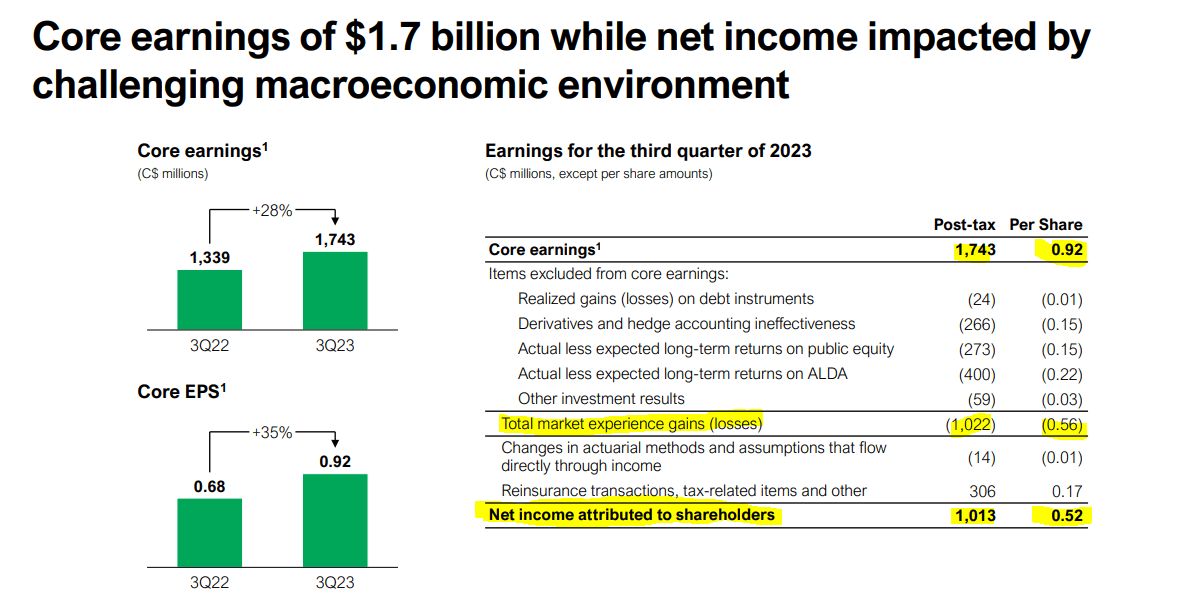

But there were some warts below the surface. The beat on core earnings (consensus estimates were close to 83 cents a share) was largely driven by lower taxes. There was a huge chasm between operating and core earnings this quarter, and the losses on the alternative long duration assets or ALDA were noteworthy.

{kind=link}

Now, some of those pressures are likely off as the Fed telegraphed a pivot, and we will see core earnings likely move below the reported earnings in Q4-2023 or Q1-2024. But those ALDA assets can create a big downside torque in a bear market. Manulife is aware of this as well, and it is looking to reduce some exposure.

Risk Reduction

Post Q3-2023, as financial conditions eased, Manulife signed off on a deal to reduce its long-term care exposure.

Reinsuring $13 billion of reserves, including $6 billion, or 14% of total LTC reserves, to Global Atlantic and its partners• Represents largest ever LTC reinsurance transaction• Ability to transact with leading reinsurance counterparty and its LTC reinsurance partner further validates the prudence of our LTC reserves and assumptions• Releases $1.2 billion of capital, which we intend to fully return to shareholders via share buybacks, resulting in core EPS and core ROE accretion• Attractive earnings multiple of 9.5 times and 1.0 times book value multiple• Reduces the risk from legacy blocks, including a 12% reduction in LTC morbidity sensitivities• Expect to dispose $1.7 billion of alternative long-duration assets (“ALDA”)• Represents a full risk transfer with significant structural protection, and with a highly experienced counterparty and its partners• A major milestone in reshaping our portfolio with core earnings2 contribution from LTC and variable annuities further reduced to 11% from 24% in 2017

Source: Manulife

The multiple was good and the reduction released some reserves, which MFC will use for a buyback. Analysts were generally positive on the transaction.

Apart from LTC, the reserves range across multiple product lines including payout annuities and whole life policies helping Manulife dispose C$1.7 billion of alternative long-duration assets ((ALDA)), the company said.

The transfer, which is expected to close in the first half of 2024, will improve profitability and the risk profile of the inforce business, Costantini said.

"Long term care is one of the most riskiest products for life insurance, they were able to unload it and unload it at a decent valuation," Morningstar analyst Suryansh Sharma said.

Source: Reuters

We like it as well. This needs to be pointed out though. The transaction is just 14% of its book. LTC sensitivities will only be reduced by around 12%. So this rush to expand the valuation may be a little premature.

Valuation

MFC's valuation is extremely tricky. The stock always looks cheap on an earnings basis and then years of earned money gets destroyed in a recession. The company has been reducing the riskier aspects of its business. But what is left is the low margin life-insurance business that should not be valued at high multiples. On the asset management side, there is pressure from fee compression as ETFs and other products keep moving towards 0.00% in fees. Looking at a pure price to tangible book value, MFC is moving to the upper end of its average over the last decade.

This 10 year timeframe though includes changes in the way tangible book value was calculated once IFRS 17 was implemented (see here for details ). Our take here is that the ratio is still applicable, but you need to give MFC a wider berth on this metric and not assume 1.685X is very expensive (just a tad high). Ultimately, it comes down to where you stand on the macro and we don't think this is a great time for MFC this late in the cycle.

Hence we think this is a good opportunity book gains for those long and believe that 2024 will provide opportunity to pick this back up significantly cheaper. We still rate the shares a "Hold" over here and would move to "Sell" rating over $24.00 USD.

Preferred Shares

While we did not own the common, we did dabble in two of Manulife's preferred shares. We had recommended Manulife Preferred Shares Series 13, ( MFC.PR.K:CA ) in June 2023 at a price of $19.00 . The preferred shares are up 16% and have delivered a total return near 19% or at about 35% annualized. They were recently reset.

With respect to any Series 13 Preferred Shares that remain outstanding after September 19, 2023, holders thereof will be entitled to receive fixed rate non-cumulative preferential cash dividends on a quarterly basis, as and when declared by the Board of Directors of Manulife and subject to the provisions of the Insurance Companies Act (Canada). The dividend rate for the five-year period commencing on September 20, 2023, and ending on September 19, 2028, will be 6.35000% per annum or $0.396875 per share per quarter, being equal to the sum of the five-year Government of Canada bond yield as at August 21, 2023, plus 2.22%, as determined in accordance with the terms of the Series 13 Preferred Shares.

6.35% on par works out to about 8.36% on the price we recommended it but at the current price of $22.05, we are looking at roughly 7.11%. That comes to a more average yield for the risks that Manulife has and we would consider exiting.

We had also touched on another issue Manulife Financial Corporation PFD CL A SER 2 ( MFC.PR.B:CA ) and recommended a buy at $16.93 on October 5 . We sold these as they moved over $19.00. We no longer believe these offer a good risk-reward even at $18.50. For those looking for comparable quality fixed rate issues with better yields, we would look to Brookfield Renewable Partners L.P. Class A Preferred Limited Partnership Units Series 18 (TSX: BEP.PR.R:CA ), which we covered recently .

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Manulife: Time To Take Some Profits