MGDPF - Marathon Gold: After Plummeting 70% Last Year It's Time To Buy Again

Summary

- Why MGDPF underperformed to such an extent in 2022.

- The updated Feasibility Study and project economics.

- There are many other bullish factors that need to be taken into consideration about the NPV.

- MGDPF is trading at ~0.4x its fair value, and I’m looking for a vibrant rebound in 2023.

Marathon Gold ( OTCQX:MGDPF ) has done a round trip over the last four years, as its stock increased by several hundred percent from 2018-2021, but then the wheels came off in 2022. MGDPF was one of the worst-performing gold stocks last year, as shares were down over 70%.

I first started buying MGDPF in mid-2018 when the stock was 50-80 cents. I sold out of everything from late 2020 to late 2021 when the stock was ~$2.10-2.60, realizing a gain of 200%+. As I told subscribers of The Gold Edge in December 2021, when MGDPF was still at ~$2.50: " While I pounded the table on Marathon over the years, earlier this month I decided to move on from the stock. Considering its substantial outperformance and my concern about potential Capex inflation negatively impacting the NPV of the Valentine project, the risk/reward wasn't as appealing as before. " Since then, the pendulum has swung in the opposite direction, as now it's Marathon that has a far more appealing risk/reward compared to other companies in the sector, and it's time to buy again.

StockCharts.com

Let's back up a bit and discuss why MGDPF underperformed to such an extent in 2022.

As I warned in 2021, I believed project CapEx for the company's Valentine Gold project in Newfoundland, Canada, would jump considerably, which it did, going from C$305 million in the 2021 Feasibility Study to C$470-C$490 million in the revised September 2022 estimate, or a ~60% increase. The combination of the outperformance in the stock over the prior years and much higher CapEx (which would lower the NPV of the project) are the main reasons for the share price's dramatic fall in 2022.

Also contributing to the overall underperformance last year was the ~50% dilution announced in September, just after the revised CapEx figure was announced and after MGDPF had dropped considerably and was trading at multi-year lows. There were substantial warrants also included as part of the financing, which added to the selling pressure and underperformance.

However, I believed investors had punished MGDPF far too aggressively, and the company was truly well positioned at that stage, as:

- Valentine Gold was fully permitted.

- Marathon Gold was fully funded.

- The company was entering the construction phase.

- I felt that the latest project CapEx estimate was priced at a likely short-term top of the market.

- Marathon had substantially de-risked the project with its reverse circulation drill program, as RC drilling confirmed the grade and location of the gold according to the 2022 block model.

Given the stock's atrocious performance (which seemed completely washed out) and all of the positives just mentioned, the risk/reward on MGDPF a few months ago was the best it's been in years.

The only outstanding issue that could put more pressure on the shares was the updated Feasibility Study ((FS)), which was expected to be completed in Q4 2022. We already knew the updated CapEx figure, but it wasn't clear: 1) how much AISC would increase, and 2) how big of an impact the Berry deposit would have on the mine plan and economics.

The 2021 FS estimated that AISC over the life of mine would be US$833 per ounce, but the company stated in early 2022 that it expected a 15-20% increase in AISC compared to the prior years' estimate, and that didn't seem like a firm number.

Higher CapEx already drove down the value of the project, and higher OpEx would do the same. At $1,750 gold, I estimated an NPV of US$400-$450 million, compared to ~US$650 million in the previous study.

However, that didn't include the Berry deposit, which Marathon was incorporating into the updated FS as a 3 pit mine plan. Only the Leprechaun and Marathon deposits were included in the 2021 study, but Berry (which sits in the middle) has been thoroughly drilled and had enough ounces to be added to the updated FS. There are 1.1 million ounces of open-pit M&I gold resources defined at Berry at a stellar grade of almost 2 g/t. On paper, Berry seems like a home run. My only concerning question was about the strip ratio, which could negatively impact the economics. High-grade ore can overcome a high strip, which is the case for the Marathon and Leprechaun deposits. The updated FS would give us the answer on Berry as well. If Berry was viable, it could add another US$250-$300 million of value to the project. If Berry disappointed, the project's NPV might be as low as US$400 million.

{kind=link}

Marathon Gold

It didn't matter, though, whether Berry was economical or not, as Marathon was trading at a market cap of US$250 million at the lows a few months ago, which was a steep discount to the NPV of Valentine Gold even without Berry, and an enormous markdown if Berry did add considerable value to the project. Whatever the outcome, MGDPF was a bargain, especially when you consider a high-grade, open-pit project in Canada should trade at a premium multiple.

The updated FS would provide much more clarity on the project, including the impact of inflation on OpEx and whether Berry would make a notable contribution.

Now let's review the results of the updated Feasibility that were announced last month.

2022 Feasibility Study

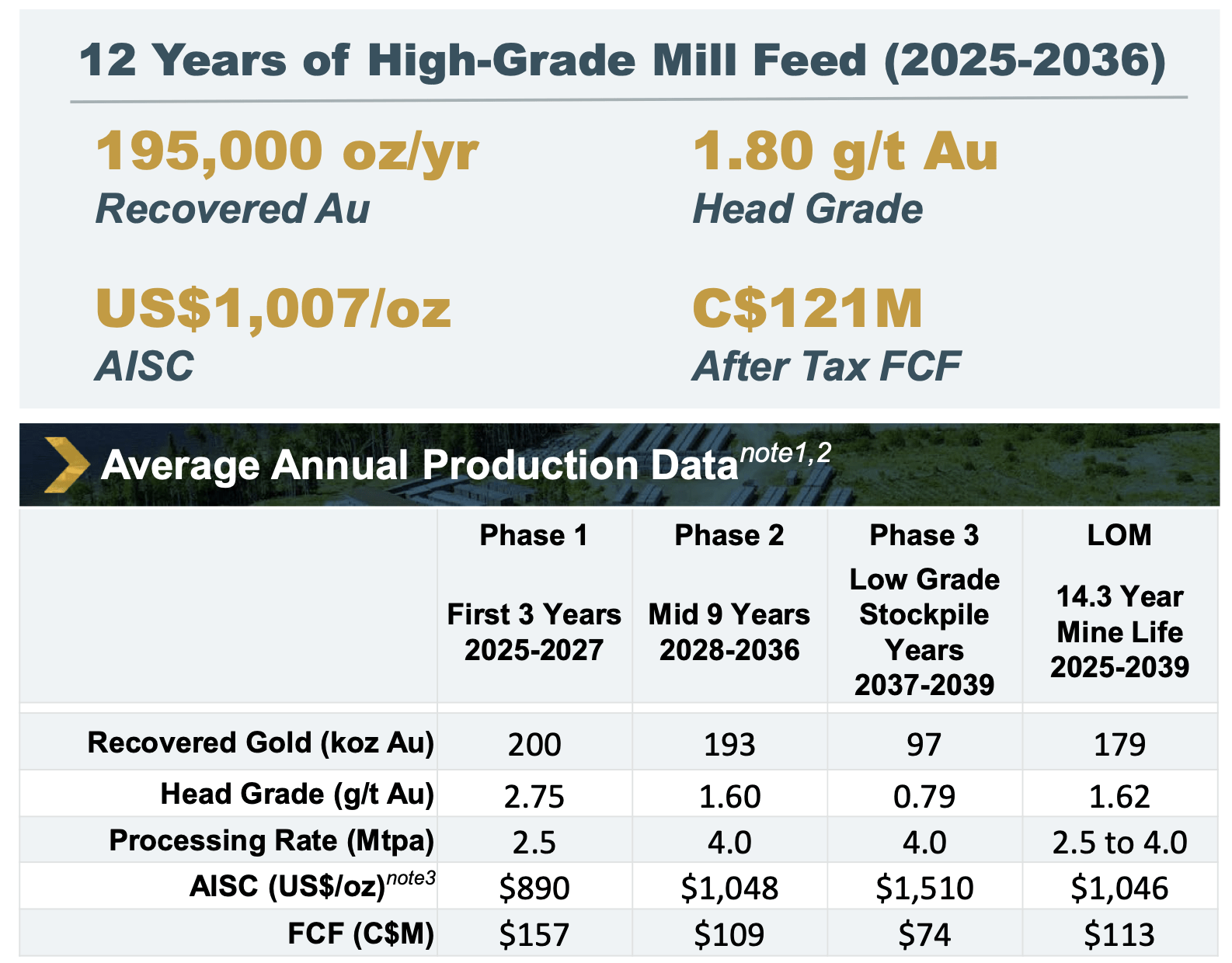

When I opened the press release and began reading the details, I was impressed right off the bat. Ounces added to the mine plan increased 31% compared to the previous FS, grade increased 20% to 1.62 g/t Au (previously 1.36 g/t Au), and high-grade mine life increased to 12 years at 195,000 ounces of gold production per year on average vs. 9 years at an average of 173,000 ounces annually. This was all thanks to Berry. AISC for the first 12 years is slightly above the high-end of the range MGDPF gave earlier last year, but still a bit of a relief. If you include the low grade stockpile years, the life of mine increases to 14 years, with 179,000 ounces of production per year at an average AISC of $1,046. As a side note, the goal of any company building a mine and stockpiling ore is to never have to process the stockpile, but rather to find more resources that have better economics. Exploration success could keep AISC around $1,000 or below (at least in today's dollars). Back on point, the first three years will see exceptionally high-grade production of 2.75 g/t gold and AISC below $900 per ounce, and at $1,700 gold, the mine will generate C$157 million of FCF during each of those years.

{kind=link}

Marathon Gold

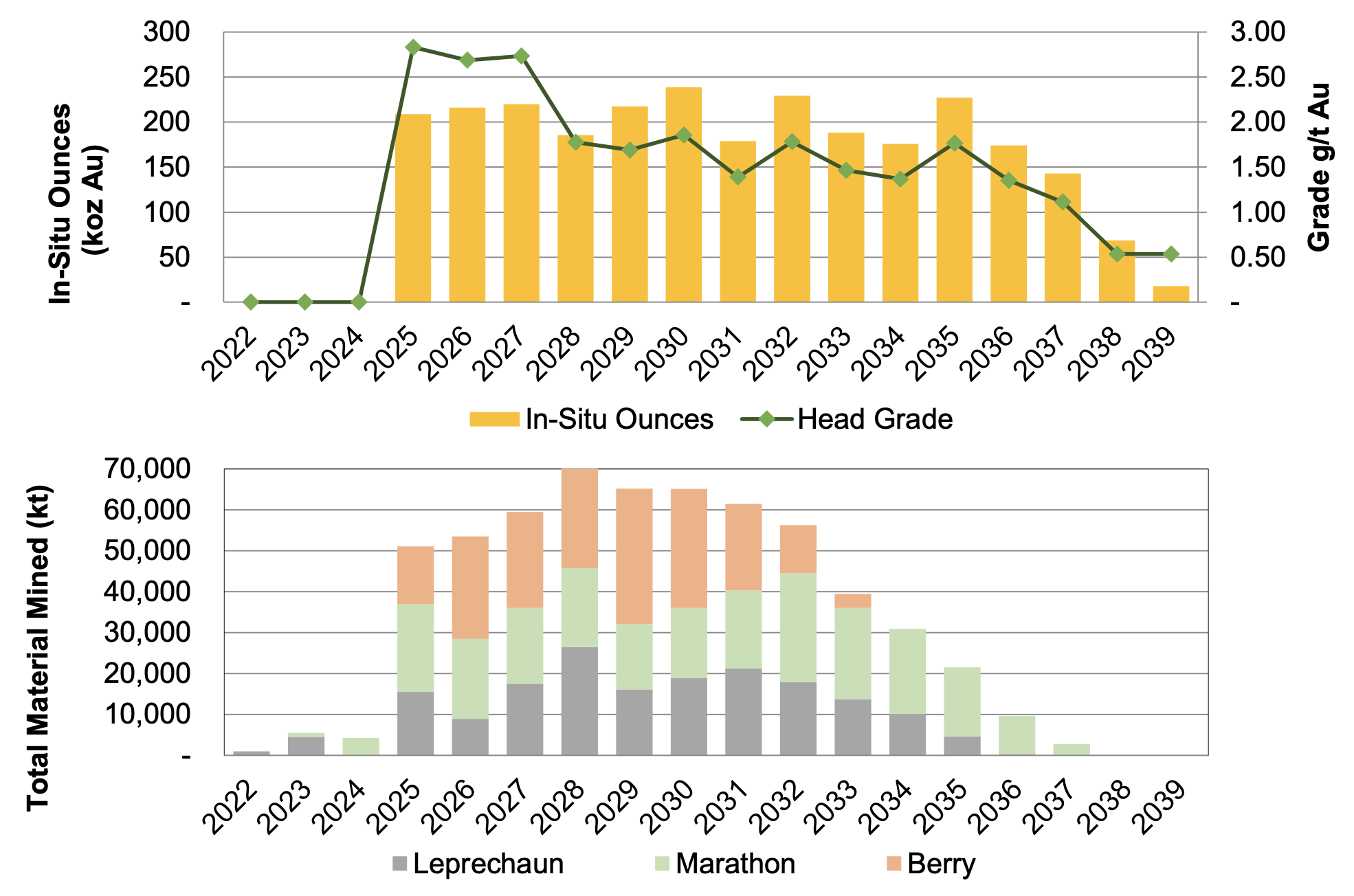

As the top graph shows, there is some variation in production in Phase 2 (2028-2036), but overall, it's a steady profile. The Marathon, Leprechaun, and Berry deposits will be mined simultaneously during the first 8-9 years, then Berry will be used for tailings and waste rock starting in 2034.

{kind=link}

Marathon Gold

At the end of the day, it all comes down to the economics, and those were a bit of a disappointment.

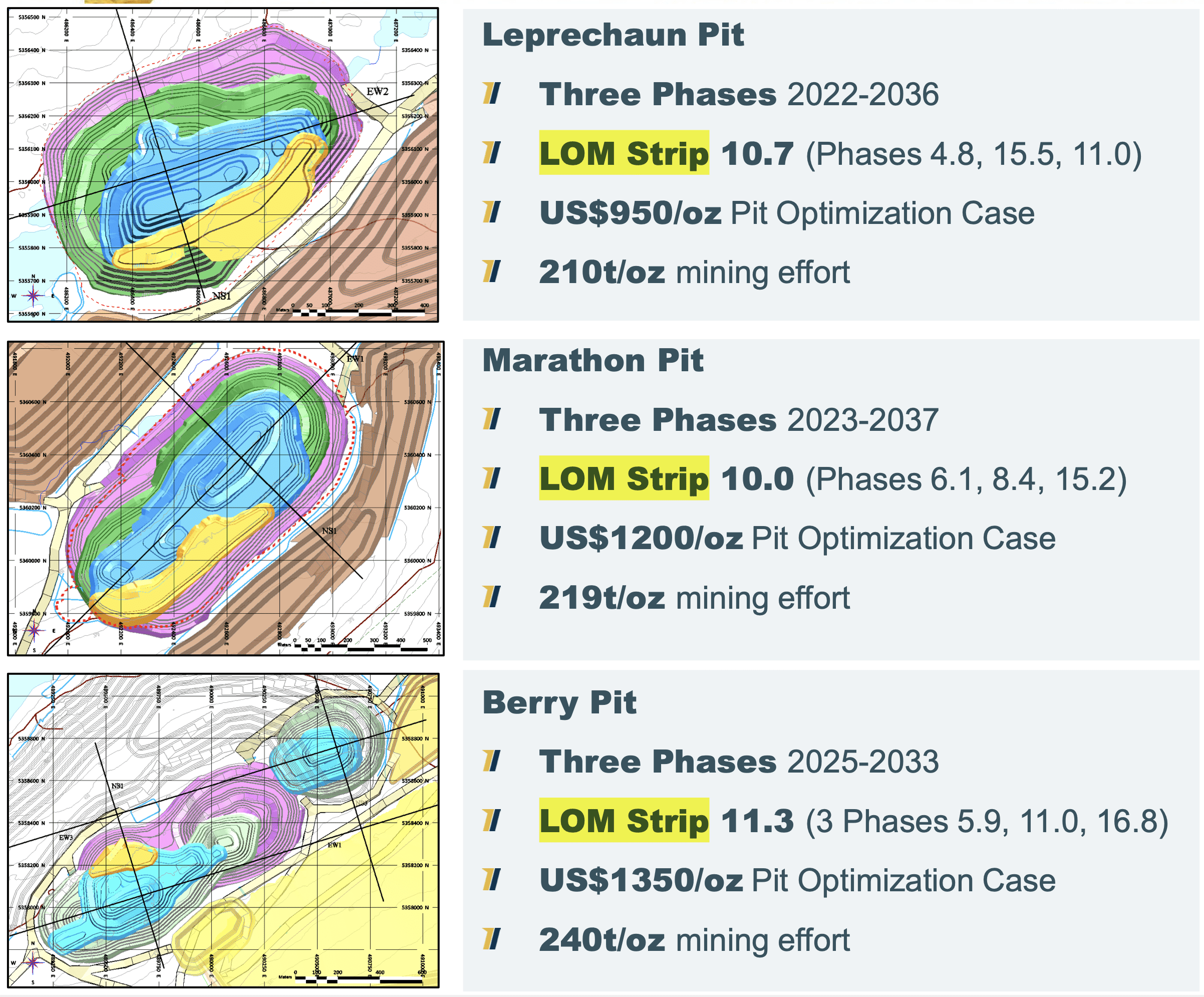

In the previous FS, the estimated combined strip ratio for the Marathon and Leprechaun pits was 7.2:1. Both pits saw a substantial increase in strip ratio in the updated FS, as Marathon tightened up the geological model in early 2022 and removed some of the marginal lower-grade blocks that were reporting to the stockpile years of the mine plan. The impact is a higher strip because those lower grade blocks that would have been included as ore are now counted as waste. These are swarms of flattish veins at high grades, and by removing marginal ounces from the plan, Marathon believes it's de-risking Valentine Gold and showing that even at a higher strip and less ore, the project works. The Berry pit has the highest strip ratio (no surprise), as it's estimated at 11.3 over the life of mine. The strip ratio for the entire project increased to 10.6:1.

{kind=link}

Marathon Gold

Strip ratio is simply the ratio of waste to ore in the mine plan. The higher the strip, the more of a negative impact it will have on the economics as there is more waste to remove vs. ore extracted. A high grade project like Valentine Gold can overcome a high strip, but still, the economics are impacted.

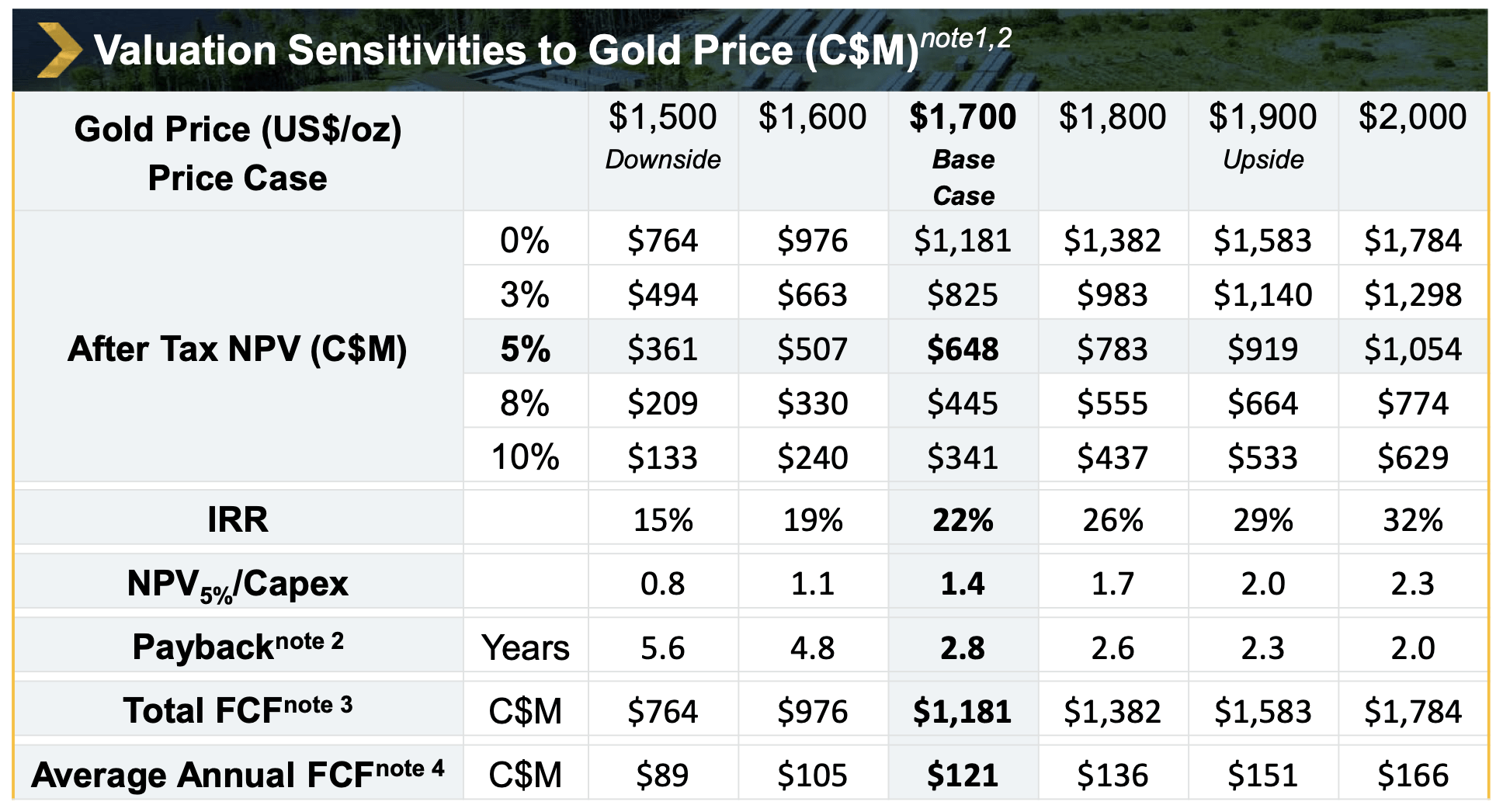

At $1,800 gold, the updated after-tax NPV (5%) for Valentine Gold is C$783 million, or US$587 million at a 0.75 CAD/USD exchange rate. This falls within the US$500-$700 million range I estimated in May 2022, but still more towards the low end. Berry does have a positive impact, but not as much as one might expect, which is what I've been concerned (and warned) about ever since Marathon discussed potentially adding the project to the mine plan last year.

{kind=link}

Marathon Gold

Having said that, there are many other bullish factors that need to be taken into consideration about the NPV.

1. Positive Grade Reconciliation

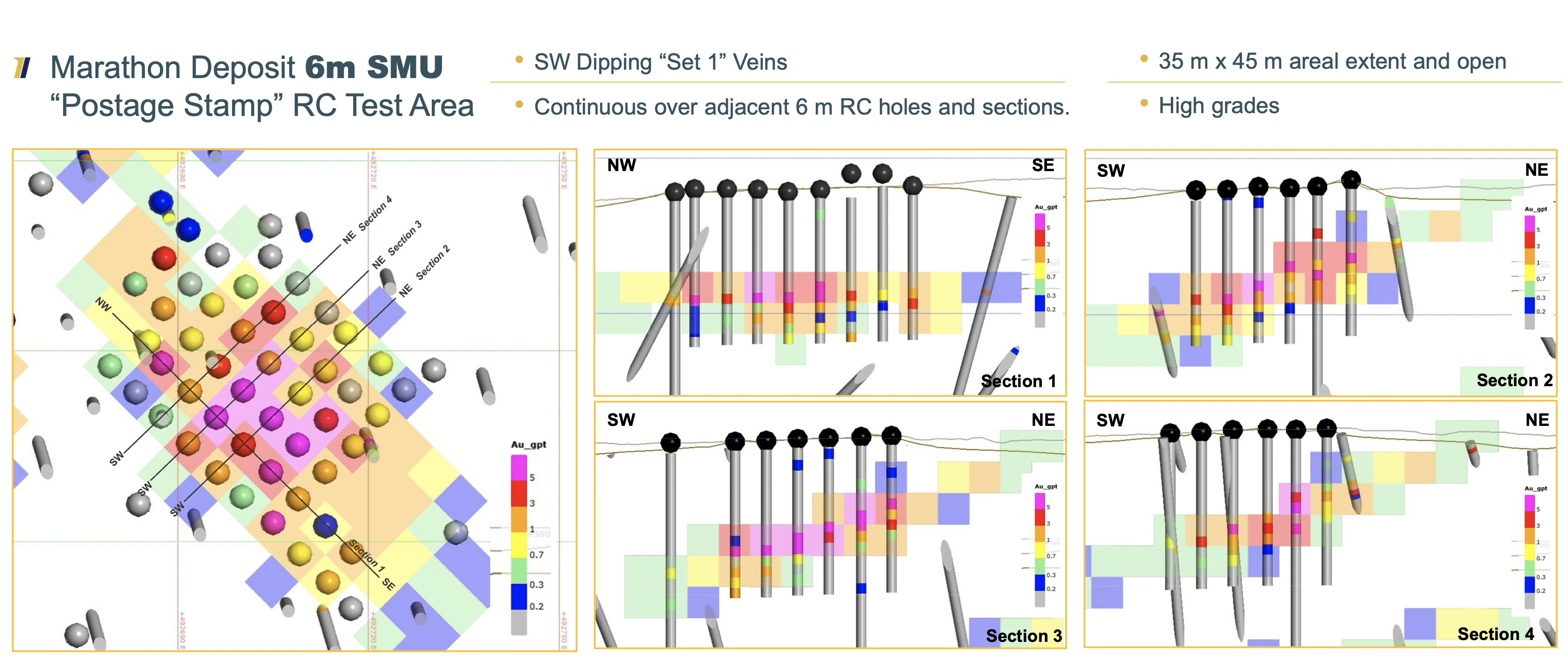

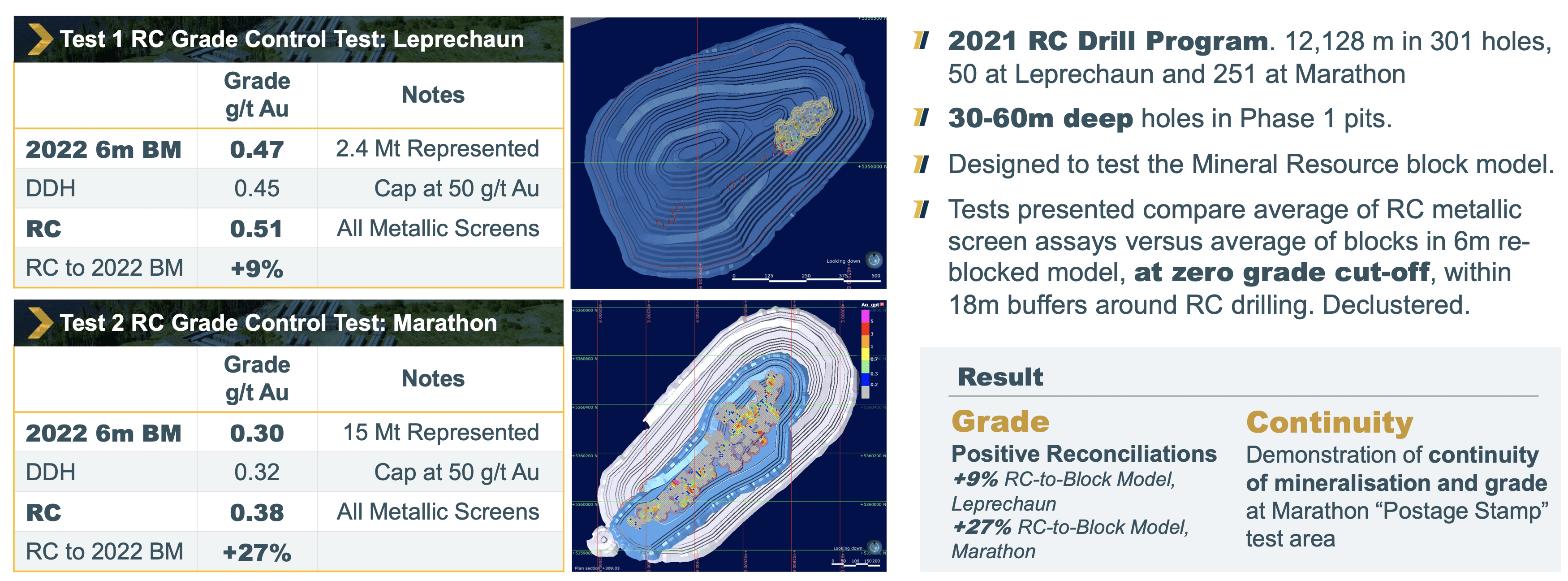

Marathon has substantially de-risked the project with its reverse circulation drill program. Years ago, the main risk I highlighted about the Valentine Gold project was the continuity of the mineralization and whether the gold was where it was supposed to be. The amount of drilling since then has greatly lessened that risk, and the diagram below shows that the RC drilling is further confirming the grade and location of the gold—according to the 2022 block model.

{kind=link}

Marathon Gold

As the two tables on the left show, the block model at Leprechaun estimated 0.47 g/t Au in the test shown, but RC drilling estimated 0.51 g/t gold, or a 9% positive reconciliation. The positive reconciliation at the Marathon pit was much higher at 27%. This doesn't mean the entire resource at both deposits is underestimated, but it does mean that in these areas, grade is coming in higher than the block model, and it does de-risk Phase 1 of the project and gives more confidence in the production estimates for the first three years. If there are more ounces than expected in Phase 1, that will improve the NPV. If that trend carries over to the rest of the phases (or even part of them), that will dramatically improve the NPV.

{kind=link}

Marathon Gold

Marathon announced a few days ago a 70,000 meter RC drill program at the Leprechaun, Marathon and Berry Deposits during 2023-2024, "with the objective of developing a grade control model to support early mine production reconciliation and forecasting, and building on the positive experiences of the 2021 RC drill program."

Positive results from this program will further solidify the estimated grade of the mine plan.

It's still too early to make any bold predictions on grade reconciliation. We won't know until we start to see production results. But I will say the RC drilling, in combination with the updated FS, means that Valentine Gold is about as de-risked at this stage as you can get for a project that just started construction.

2. Shifting Some Focus Back To Exploration

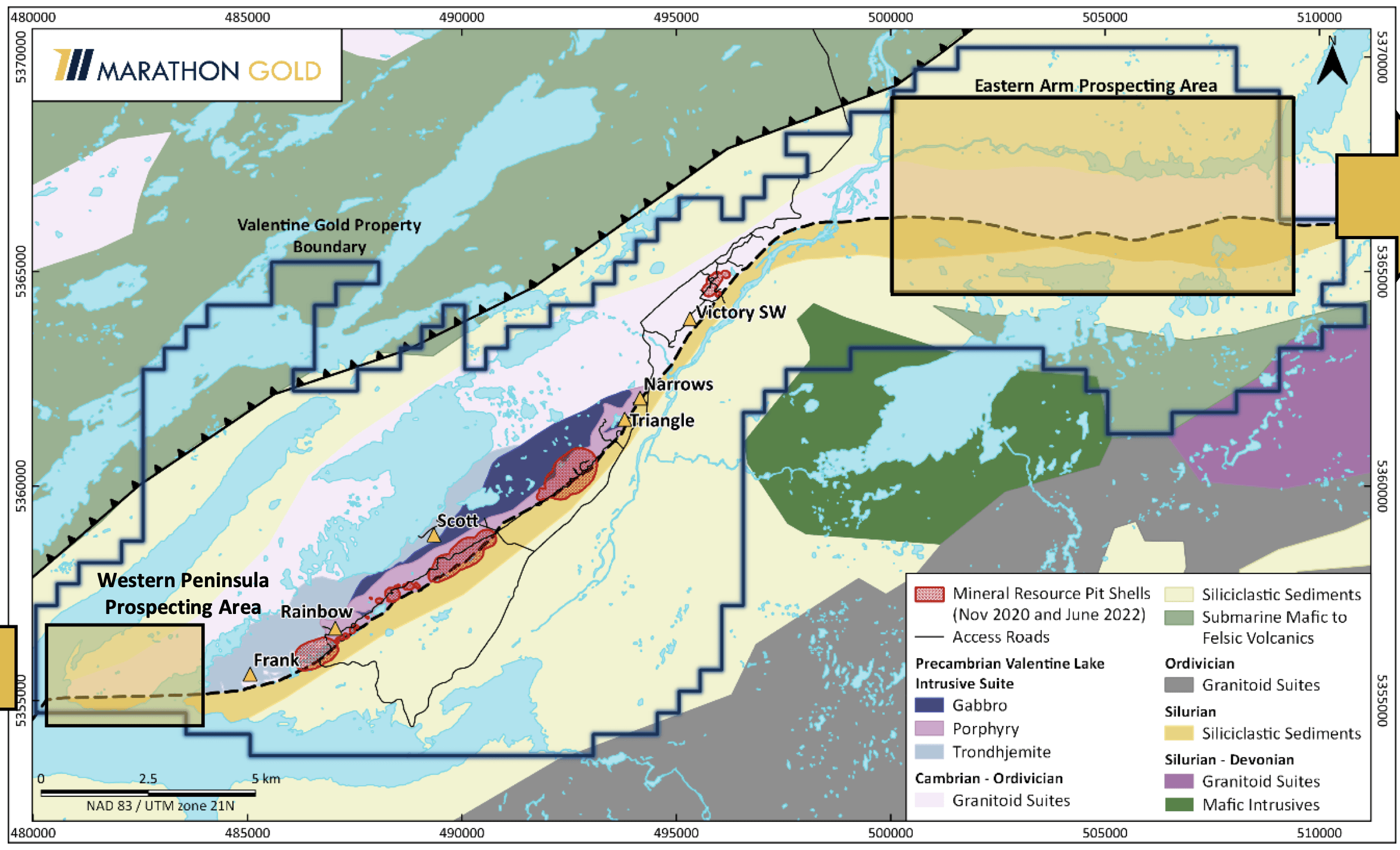

Now that the updated FS is complete and the mine is being built, Marathon can shift some focus back to exploration. There is still a considerable strike length of ground to explore at Valentine Gold. The map shows the extent of the land package, with the red shaded areas being the resource pit shells. While Marathon is drilling targets between the Leprechaun pit at the SW and Victory pit towards the NE, the company is looking at other prospective areas outside of this boundary, including a sizable area called the Eastern Arm (highlighted in yellow/orange) that host the continuation of the Valentine Lake shear zone. The company stated last week: " we see real potential for another major discovery on the scale of Berry elsewhere within the property. At the Eastern Arm prospecting area, we are now beginning to see significant gold geochemical anomalies emerging from our 2022 summer sampling, with till samples showing multiple pristine gold grains." The company is also looking more closely at the Frank Zone, which is adjacent to the Leprechaun Deposit.

{kind=link}

Marathon Gold

Exploration potential at Valentine Gold is exceptional and there could be more pits added to the mine plan in the future.

I also believe that Matador Mining ( OTCQX:MZZMF )—which has a smaller project to the southwest and a sizable land package on this same shear zone—could be a good acquisition target for Marathon. Lots of untapped potential in this underexplored area of the world that's just starting to be uncovered.

3. Not All Berry Deposit Infill Drilling Results Have Been Reported

There are infill drilling results for the Berry deposit that are still outstanding, and the company plans to provide updated geological and mineralization models for Berry that will integrate all of the 2022 drill results, which could potentially add ounces within the current mining pit shell. More ounces within the pit means less waste, a lower strip, and better overall return.

Valuation = 0.4x NAV

With the updated FS out of the way and the market having time to digest the news, there is far less risk in MGDPF this year compared to other miners.

The shares have begun to outperform again and are up 26% since the Feasibility was released, compared to a 9% increase in the HUI (an index of gold stocks). Despite the strong gains in MGDPF over the last month, the stock is still trading a deep discount to its fair value. The company's market cap is just under US$350 million, but at current gold prices and exchange rates, the NPV of the Valentine Gold project is US$648 million. MGDPF is trading at a little more than 0.5x NAV, and I'm not even including the C$164 million of net cash on the balance sheet as of September 30, 2022, which makes the discount even more extreme when using enterprise value.

Let's put it another way to really drive home the valuation discount.

The after-tax NPV (5%) on December 31, 2024 (or when construction is expected to be complete) is C$1.2 billion at $1,700 gold. Let's keep this at $1,865 gold as that's the current gold price and the price assumption I used above. At $1,865 gold, I would estimate the return at that point is ~C$1.44 billion.

The remaining capital cost for Valentine Gold was C$463M (US$347M) as of October 31, 2022. Marathon also has a C$355 million credit facility, which they will use to cover the rest of the build and for other expenditures and working capital over the next two years. By the end of 2024, net debt will likely be around C$350 million, assuming the project hits all construction and Capex targets.

Take the value of the project at that time and subtract the debt, and the fair value of MGDPF would be C$1.1 billion (or US$810 million). The stock is trading at ~0.4x that valuation now.

While I was disappointed that Berry didn't have a more positive impact, I anticipated this could be a possibility, and it was built into my model. MGFPF still remains deeply undervalued and is one of the best acquisition targets among all of the current gold development stocks.

I believe the shares are only at the beginning of what will be a vibrant rebound over the next 12 months.

Risks

Marathon is at the stage of development where the risk of negative news is at its lowest. The updated FS is complete, the CapEx and OpEx are based on the H2 2022 pricing environment and account for recent inflationary pressures, and construction is ramping up. Usually, it's pretty quiet during this period.

The Berry deposit will need to be permitted, but I don't expect any issues there.

The main risk at this stage is still inflation, or specifically, the timing of the inflationary cycle.

Inflation comes in waves, and Valentine Gold is a two year build. As I mentioned earlier, I believe that the project was priced at a likely short-term top of the inflation cycle. The question is when will the next inflation wave begin?

It's unlikely that Marathon will adjust CapEx higher anytime soon since the company just came out last month with the updated FS and inflation is cooling. However, if inflation begins to ramp up again during the middle of the construction phase, there will be a real risk of another increase in initial CapEx.

For further details see:

Marathon Gold: After Plummeting 70% Last Year, It's Time To Buy Again