MGDPF - Marathon Gold: Too Cheap To Ignore

2023-06-20 18:15:53 ET

Summary

- Marathon Gold is an undervalued gold developer with a fully funded project and strong fundamentals, trading at a fraction of what suitors have paid for Tier-1 jurisdiction ounces.

- The company has received a vote of confidence from the sector's largest royalty/streaming company, Franco-Nevada, and is on track for first gold pour in early 2025.

- With multiple paths to an upside re-rating, Marathon presents a solid opportunity for patient investors willing to invest in the junior space, with MGDPF trading at just ~2.4x FY2026 P/FCF.

Just over two months ago, I wrote on Marathon Gold ( MGDPF ), noting that the stock was trading at a very attractive valuation despite being near fully funded for construction at its Valentine Gold Project in Newfoundland and construction being 27% completed as of last quarter. This turned out to be a terrible call, and I was clearly wrong, given that while the stock enjoyed a brief bounce, it has since slid 16% lower from when I highlighted the stock as sitting in what appeared to be a low-risk buy zone at US$0.65. The consolation, if any, to being brutally wrong on my timing is that the fundamentals have arguably become stronger for Marathon, with its funding gap addressed, diesel prices continuing to drip lower, and the gold price finding firm footing above $1,900/oz, with a record 14 weeks spent closing above the psychological $1,900/oz level. Let's dig into recent developments below:

{kind=link}

Process Plant Site (Company Website)

All figures are in United States Dollars at a 0.75 CAD/USD exchange rate unless otherwise noted.

Recent Developments

Marathon Gold ("Marathon") released its Q1 results in mid-May, ending the quarter with ~$100 million in cash before its recent flow-through financing, and reporting that expected costs to completion at its Valentine Gold Project in Newfound were tracking in line with estimates, with just a 1% variance (~$3 million) with ~$302 million left to be spent after ~$39 million was spent in Q1. Meanwhile, from an overall completion standpoint, Valentine Project progress was sitting at 27% complete vs. a plan of 26% (ahead of schedule), with engineering at 71%, procurement at 51% and construction at 9%, with the project being LTI free since October 2022 with ~184,400 hours of work completed as of March. The result is that Marathon remains confident that first ore will be delivered to the mill by year-end 2024, with its first gold pour expected in early 2025.

In regards to other developments, Marathon recently announced that it had sold a 1.50% NSR (of which 0.50% was purchased for $7.0 million) for $45 million to Franco-Nevada Gold ( FNV ). This deal has doubled Franco-Nevada's exposure to the Valentine Project, a significant vote of confidence that Marathon shareholders should be elated with, since Franco-Nevada has not grown into the sector's largest royalty/streaming company with a ~$26.0 billion market cap by being sloppy. And while this isn't near the size of its deal for a gold stream on Tocantinzinho in Brazil, this is still a meaningful investment at $50+ million, with Franco-Nevada, in addition to purchasing shares comprising the back-end of a ~$5.2 million flow-through deal. This is great news for Marathon as it takes care of the minor potential funding gap that was still in place as of my previous update on Marathon in April.

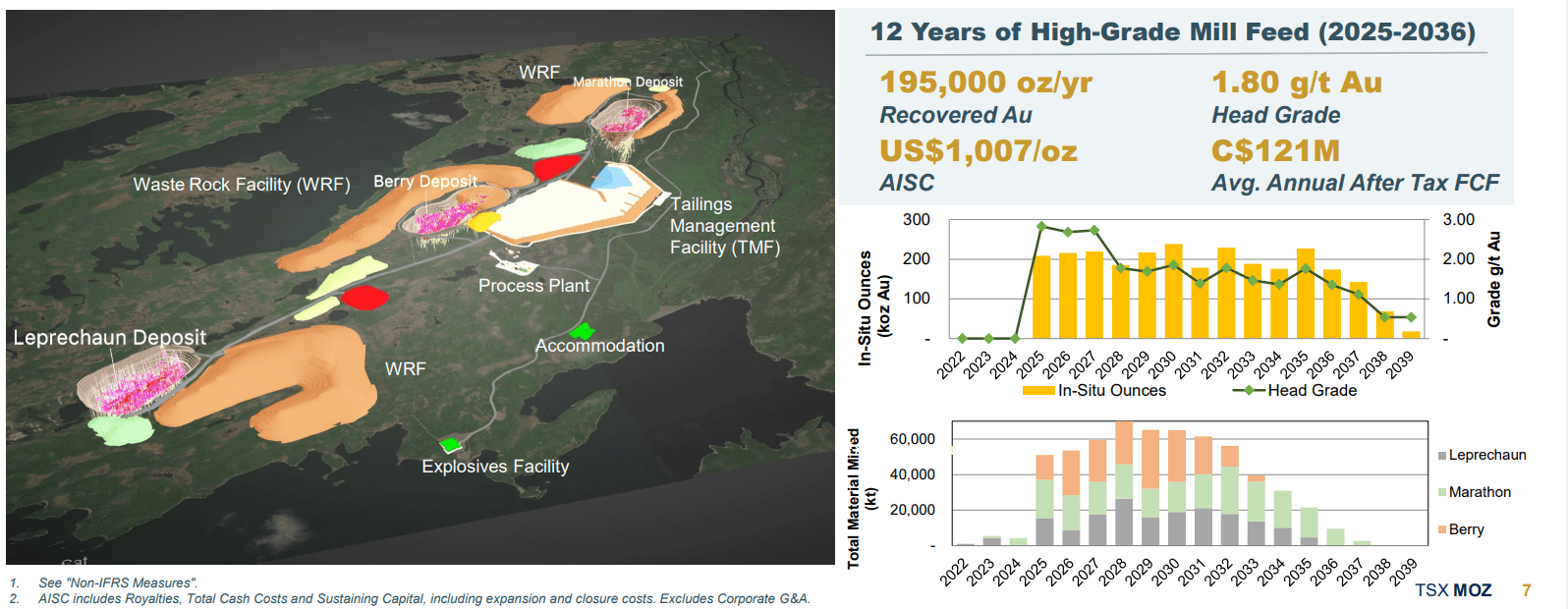

Once in production, Marathon's Valentine Mine will produce ~195,000 ounces per year for its first twelve years at industry-leading all-in sustaining costs of $1,007/oz. Even adjusting for potential inflationary pressures and assuming AISC of $1,050/oz (first three years at ~$925/oz adjusted for inflationary pressures), this would make Marathon one of the lowest-cost gold producers in North America vs. industry average AISC of ~$1,320/oz.

{kind=link}

Valentine Gold Project - 3-Pit Mine Plan (Company Website)

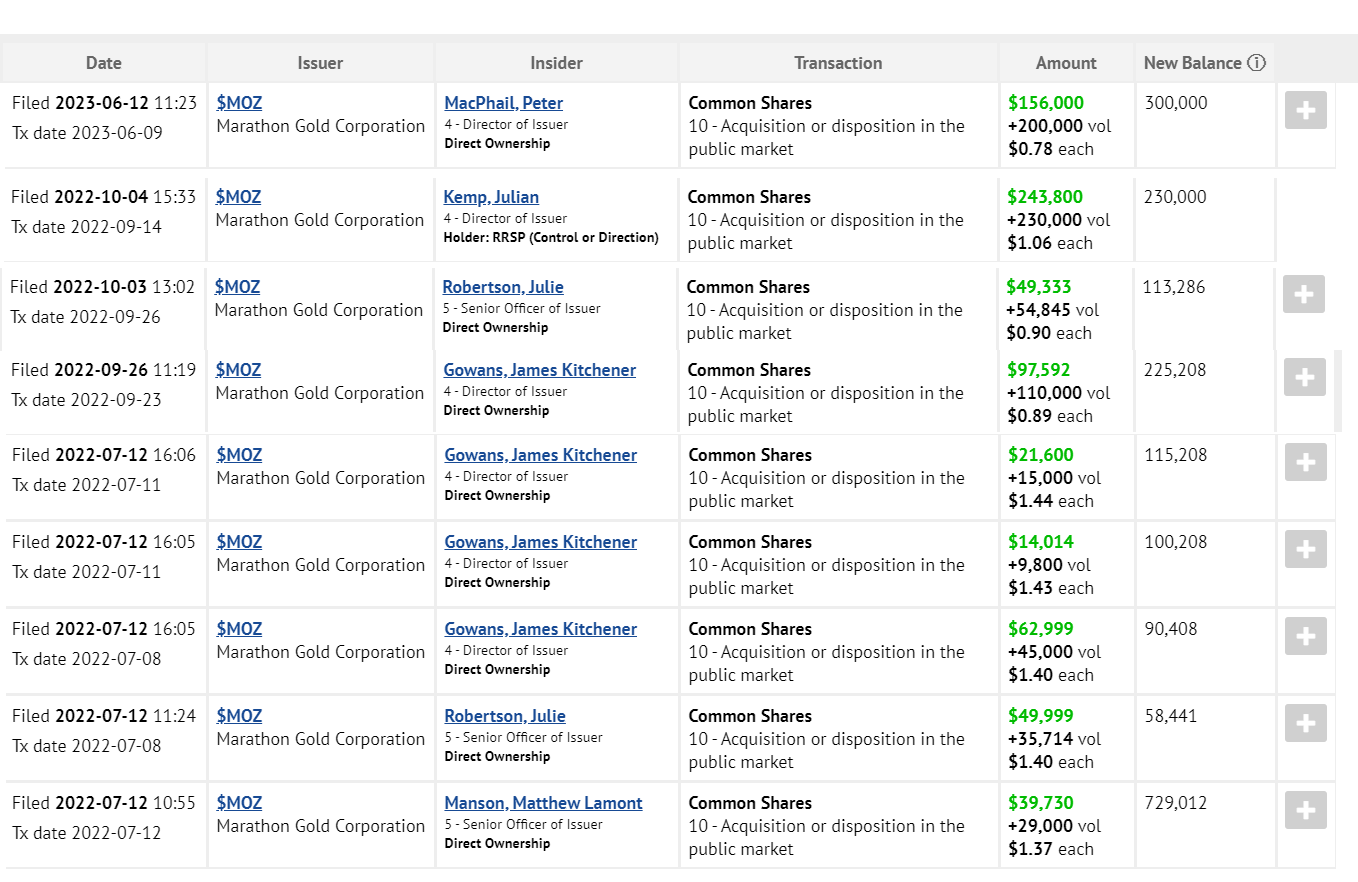

The result of the royalty sale is a minor hit to project NPV, but given the alternative of doing an equity raise at these prices, I think this was the right move. And while I'd prefer to see more insider buying, it's encouraging to see some insider buying over the past year at prices ranging from US$0.58 to US$1.08, with the most recent purchase coming from new Board Chair, Peter MacPhail, who was previously the COO of Alamos Gold ( AGI ). This is a meaningful addition given that he oversaw construction of YLG, Young Davidson, and initial expansions at Island. Combined with Marathon's CEO Matt Manson who oversaw construction of the massive Renard Diamond Mine that came in within schedule and budget and Tim Williams who served as VP Operations at Rio Alto/Tahoe (responsible for construction, ramp-up and operation of La Arena and Shahuindo open-pit mines in Peru), Marathon has considerable experience which should give investors added confidence that they can meet expectations at Valentine for construction and operations.

{kind=link}

Marathon Gold - Insider Buying (SEDI Insider Filings)

Unfortunately, despite addressing this funding gap to take any worries about a low-priced equity raise off the table and getting a solid price for an additional 1.50% NSR on this asset, Marathon has sunk another 20% in value, with the market pushing the stock toward new 52-week lows. If this were an un-funded developer with a dwindling cash balance and significant share dilution on deck, this might be alarming and cause for concern. However, Marathon is fully funded, has seen positive grade reconciliation from 2021 grade control drilling (301 holes complete with 50 at Leprechaun Pit and 251 at Marathon Pit) and has conservative grade caps in place at Valentine, suggesting that there's no reason to doubt this asset's potential to deliver at or above expectations. Hence, I see this continued weakness as sentiment driven vs. related to any negative fundamentals, and it's possible that a suitor might see this as an opportunity to diversify and add a Tier-1 jurisdiction project at an attractive price by acquiring Marathon if this weakness in the stock persists.

Takeover Potential?

It's no secret that suitors are hungry for assets in Tier-1 ranked jurisdictions like Canada, the United States, and Australia, especially as other jurisdictions see downgrades, with Mexico being one example given recent mining reforms, continued pressure on wages, and a history of blockades/strikes at multiple mines. We've seen clear evidence of this in recent deals with producers focused on top-ranked jurisdictions with mega acquisitions/mergers that included Saracen, Detour, Kirkland Lake, Pretium, and the recent deal for Newcrest ( NCMGF ). And, not surprisingly, we've seen a similar trend for developers, with names like Corvus, TMac, Apollo Consolidated, Monarch, Spectrum Metals, Battle North, Hardrock (Greenstone), Great Bear, Sabina Gold & Silver, and more recently Osisko Mining being the subject of takeovers or acquisitions of interests in these projects for hefty price targets. Marathon Gold certainly fits this bill, with a multi-million ounce permitted asset in Newfoundland, and one that has the Franco-Nevada's approval.

Outside of acquisitions, investors have rushed to bid up New Found Gold ( NFGC ) to a ~$950 million valuation in the same province at Queensway, with the Queensway Project unlikely to pour first gold before 2030 at this rate. Meanwhile, Marathon trades at less than one-third of the valuation while being fully financed for construction with a vetted resource), and it's barely 18 months away from its first gold pour. This is a massive divergence and has created an opportunity for patient investors to position in Marathon ahead of first gold pour and a significant upside re-rating. However, as we've seen in other sectors, many investors prefer to flock to what's hot and moving today. And while this can pay off short-term as a momentum trade, it's hardly an attractive way to invest over the long run (especially in a cyclical sector like precious metals), as evidenced by the violent falls from grace for past developers like Novo Resources ( NSRPF ), GoGold Resources ( GLGDF ), and even New Found Gold in its last run correcting ~75% from its June 2021 highs.

{kind=link}

Valentine Gold Project, Newfoundland (Company Report)

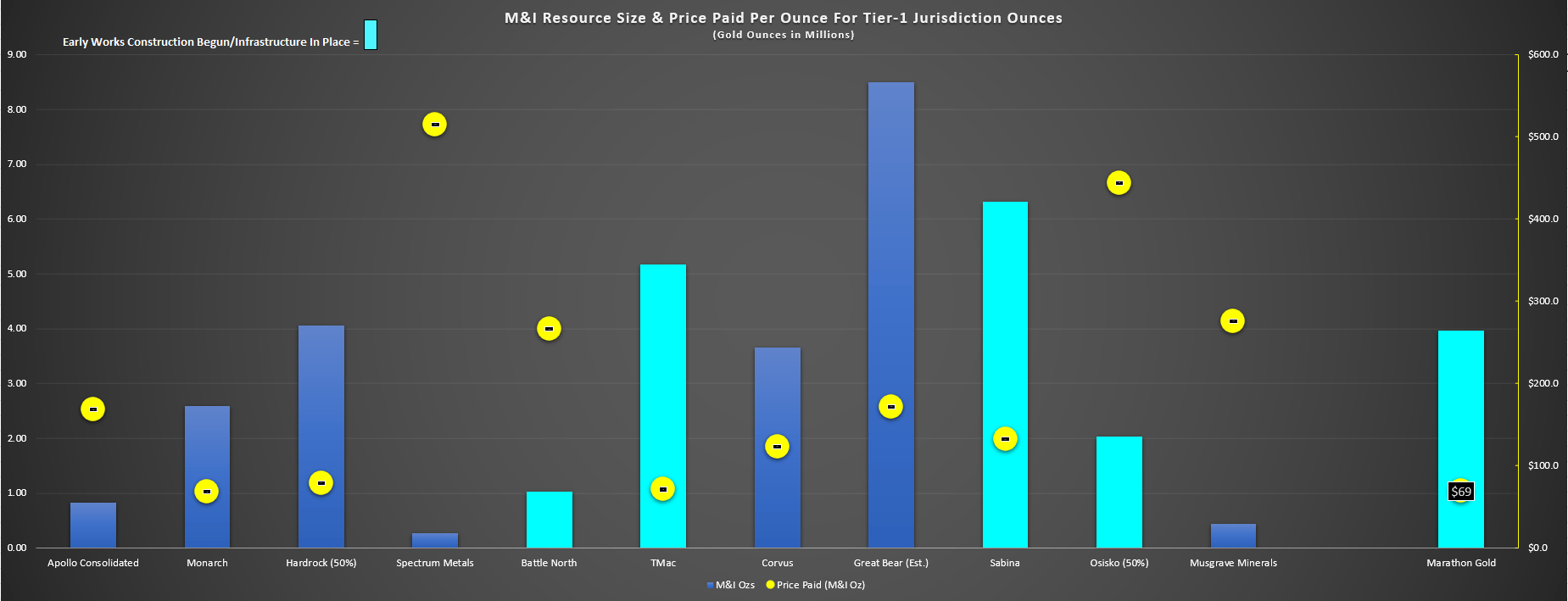

Some investors might argue that Valentine's 1.90 gram per tonne resource base is hardly comparable to the 5.0+ gram per tonne resource base that New Found Gold may eventually prove up at its Queensway Project (implying that it should command a premium). And while this may be true, time value to first cash flow always be considered and New Found Gold is several years away from a potential construction decision (let alone production) and has no resources in place currently. Plus, even if one disagrees with the comparison and current valuation discrepancy between New Found Gold and Marathon (~$950 million vs. ~$270 million valuation), we've seen multiple acquisitions over the past four years where suitors have been willing to pay a rich price to add ounces in Tier-1 jurisdictions. The average price paid for M&I? $210 per ounce of gold - over 3x Marathon's current valuation of ~$69 per M&I ounce at Valentine.

{kind=link}

M&I Resource Size & Price Paid Per Ounce For Tier-1 Jurisdiction Ounces (Company Filings, Author's Chart)

Digging into the chart above, we can see that there have been multiple acquisitions over the past few years, and not does Marathon have a much larger M&I resource base than the deal over $120 million (~3.96 million ounces vs. ~3.17 million ounces), but it's more advanced than most of these companies/projects as well. In fact, only ~36% of the projects had begun early works construction or had infrastructure in place (Battle North, Sabina Gold & Silver, Windfall, TMac Resources), and the average price paid in these deals was a premium to the average for all projects at ~$229/oz. Meanwhile, the median price paid was ~$199/oz. So, despite Marathon being more advanced than the average project, and similarly advanced to other developers that commanded a premium valuation, it trades at a depressed valuation today and a fraction of the median/average.

I have labeled TMac Resources as a developer given that Agnico Eagle has clarified that it purchased Hope Bay for the exploration upside, and because the company placed it into care & maintenance shortly after the acquisition. Great Bear's price paid has assumed 8.5 million M&I ounces in line with its contingent consideration as part of the 2021 deal or 11.5 million total resource ounces.

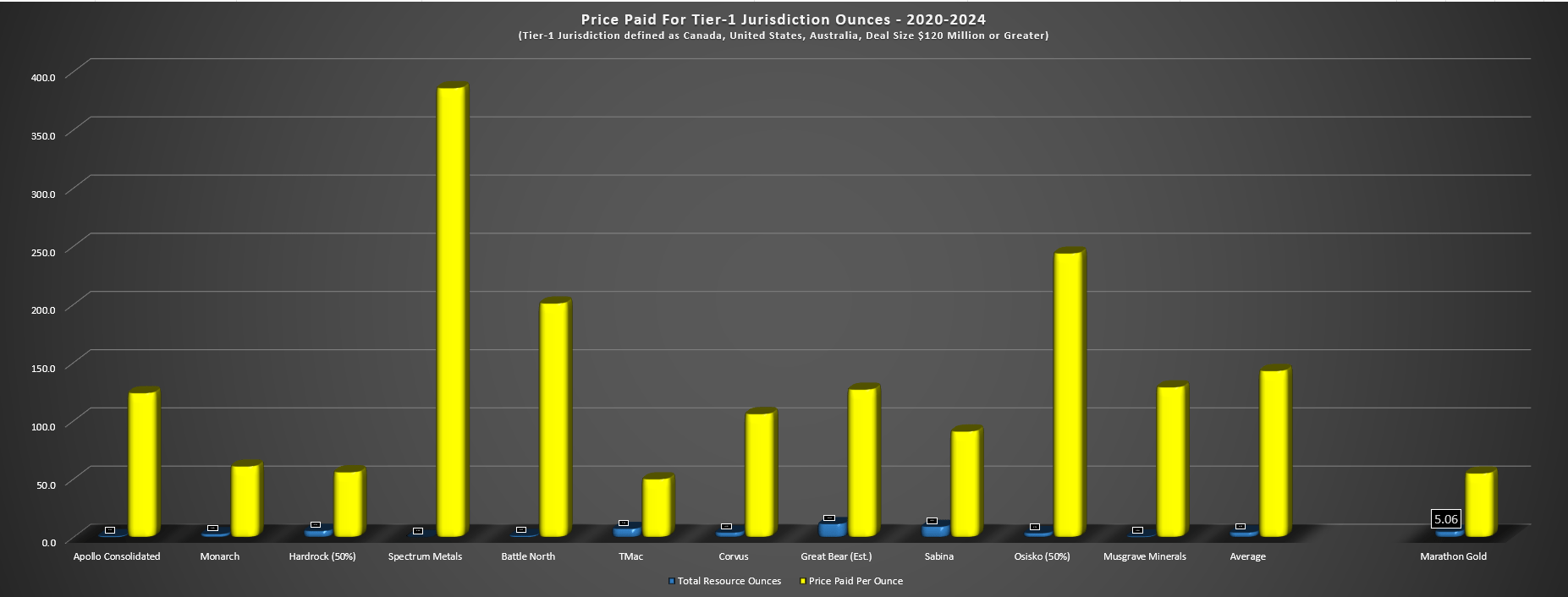

Finally, if we look at the price paid for total ounces as to not exclude earlier stage projects without Pre-Feasibility/Feasibility level work, the average price paid for Tier-1 ounces has been ~$143/oz, with the most recent offer for Musgrave Minerals coming in near ~$130/oz. Today, Marathon has a larger resource than the average developer that's been acquired or price paid for an interest in a project, yet it trades at just ~$55/oz on measured, indicated, and inferred ounces. And based on what I believe to be a likely year-end 2025 resource of ~5.4 million ounces, Marathon is trading at barely ~$50/oz using a fully diluted market cap of ~$273 million. Hence, with a project of this quality (medium-grade future open-pit mine with simple metallurgy in a safe jurisdiction) with considerable exploration potential, I am shocked that we haven't seen a suitor step up to the plate to takeover the company at these prices.

{kind=link}

Tier-1 Jurisdiction Developers/Projects - Resource Size (Total Ounces) & Price Paid Per Ounce (Company Filings, Author's Chart)

Even if use conservative assumptions and assume a 40% discount to the average price paid for M&I ounces since 2020 (~$210/oz x 0.60 = $126/oz x 3.96 million ounces = $499 million), this would place a fair value on Marathon Gold of ~$499 million or US$0.99 per share, pointing to an 83% upside from current levels. And while all of this hypothetical analysis is great if a suitor is mulling over a bid for the company already, it doesn't do much good if the company isn't acquired which is certainly a possibility. However, as I will outline in the next section, the stock is just as heavily undervalued if it's able to head into production, and arguably even more undervalued given that the company is trading at barely 2.3x price to FY2026 free cash flow estimates.

Valuation

To be ultra-conservative, we will assume ~507 million shares outstanding for Marathon Gold, which includes ~402 million shares outstanding following its recent flow-through financing, ~88 million out-of-the-money warrants, and ~17 million options. I have purposely not included any money from the proceeds of these warrants or options under the assumption that it will go toward future debt repayment, and I have given no value to its cash position of ~$100 million as this will go toward corporate G&A and construction. Under these assumptions, and based on a share price of US$0.54, Marathon trades at a market cap of US$273 million. If one prefers to assume none of the warrants or options are exercised given that the majority are well out of the money at today's prices, its market cap comes in at ~$217 million. In order to be conservative, I prefer to use the fully diluted figure as I think there's a very good shot at the warrants being exercised with 15 months remaining on most of these warrants.

I have made conservative assumptions in my NPV (8%) estimates with higher mining costs, processing costs, and slightly higher sustaining capital to account for minor cost creep.

{kind=link}

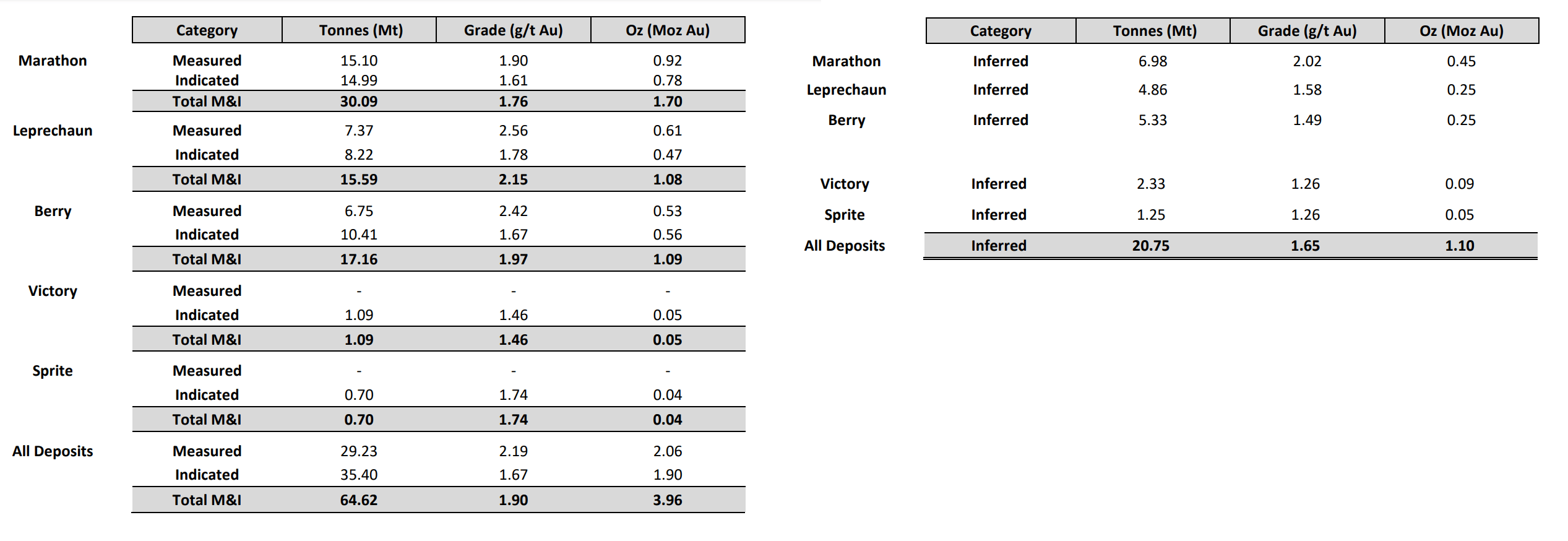

Total M&I & Inferred Ounces by Deposit (Company Filings)

As discussed in my previous update, I don't see any way to justify using a 5% discount rate for developers in the current interest rate environment, and I think an 8% discount rate is far more appropriate, especially given the rising cost of capital for developers. However, even at an 8% discount rate ($1,900/oz gold price), the estimated NPV at Valentine after accounting for Franco Nevada's added royalty (1.50% - 3.00%) comes in at ~$433 million. If we apply upside to ~1.40 million M&I ounces outside of the reserve base at an $80/oz value (1.27 million M&I ounces [+] a 10% conversion rate on inferred ounces), this would translate to an additional upside of ~$112 million. This places no value on additional exploration upside along its 32-kilometer gold trend, with Marathon's fair value coming in at $545 million. If we subtract out $90 million in estimated corporate G&A over the mine life, Marathon's fair value comes in at $455 million or US$0.90 on a fully diluted basis.

{kind=link}

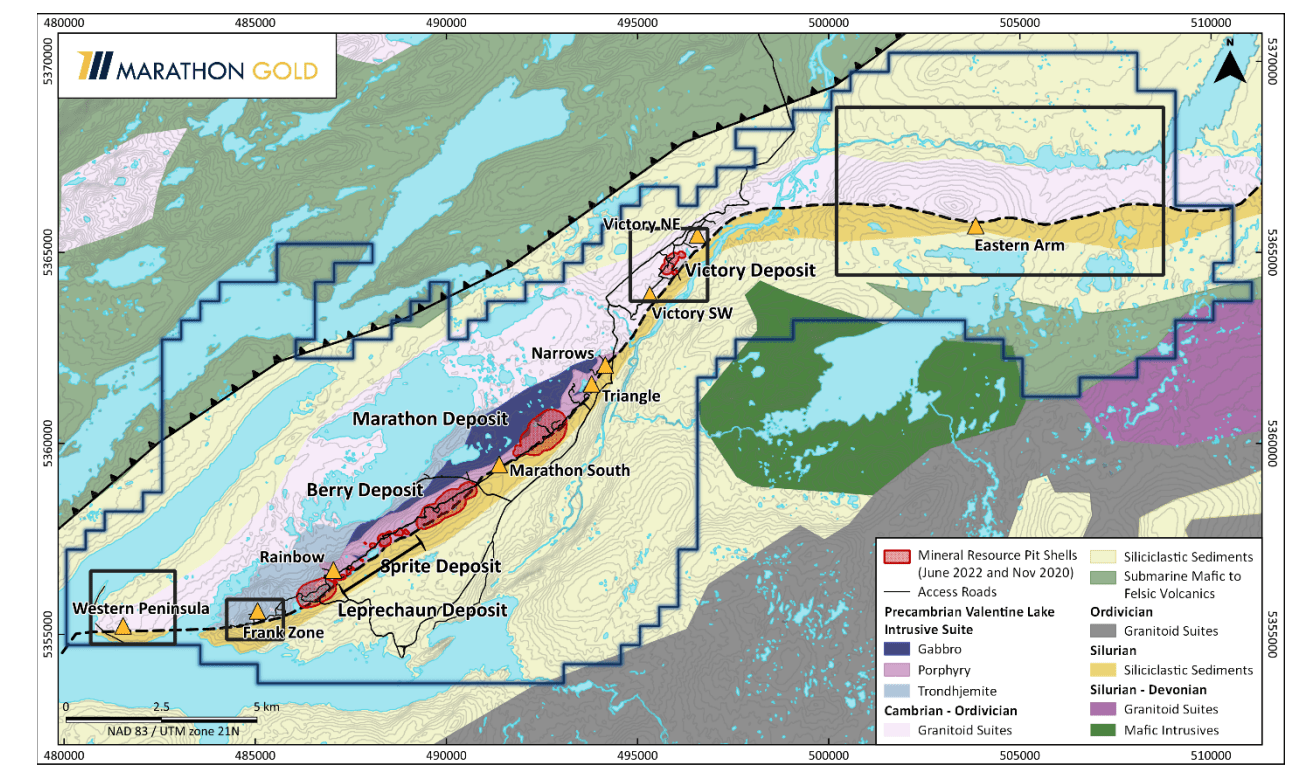

Marathon Gold - 30+ Kilometer Gold Trend & Current Resource Pits (Company Website)

While this fair value estimate of US$0.90 might not seem like much upside (67% to fair value), it's important to note that this makes very conservative assumptions, with higher operating costs baked in, a conservative discount rate (8%) and assumes that the gold averages just $1,900/oz from 2025 to 2039. I would argue that the latter is a very conservative assumption, but it's best to have a high hurdle rate and use ultra-conservative assumptions to justify taking on the added risk of owning a gold developer vs. a producer. That said, this looks at what Marathon might be worth under conservative assumptions while in construction today, and it doesn't look at where the stock can trade once it gets closer to production. And as we've seen sector-wide, a double-digit free cash flow multiple is not unusual for producers with sub $1,000/oz all-in sustaining costs in Tier-1 jurisdictions, which Marathon will be once Valentine reaches commercial production.

Given that Marathon is still over two years away from its first year of meaningful free cash flow generation, I believe a 70/30 weighting to its fair value on an NPV (8%) basis vs. its fair value on a free cash flow basis is reasonable. In addition, I think a 2-year forward free cash flow multiple of 6.0 is more conservative given that we're over two years from material free cash flow generation, and this is a non-producing asset. Under the assumption of a $1,950/oz gold price in FY2026, Marathon should generate ~$115 million in free cash flow, pointing to a fair value of $690 million or US$1.36 per share. If we apply a 30% weighting to this fair value (US$1.36 x 0.30 = US$0.41), and a 70% weighting to its fair value on an NPV (8%) basis (US$0.90 x 0.70 = US$0.63), this points to a fair value for Marathon on a blended P/NAV and P/FCF basis of US$1.11 per share.

So, regardless of whether Marathon ends up being acquired ahead of its first gold pour in Q1 2025, the stock is dirt-cheap at ~2.4x FY2026 free cash flow estimates and 0.63x P/NPV using an 8% discount rate, with an estimated fair value of US$1.11. This points to a 105% upside to fair value and it assumes that we see zero upside progress in the gold price between now and 2039 and merely trade at an average of $1,900/oz. Therefore, any upside in the gold price is a bonus for investors. In fact, it would not shock me to see Marathon Gold trade above US$1.30 by Q3 2025 once sentiment improves, and it starts trading more on near-term free cash flow potential vs. currently trading on capex blowout concerns mixed with exhausted investors throwing in the towel after what's been a relentless downtrend in the stock.

Risks

Marathon Gold is not generating positive cash flow today, it is at least two years away from generating any material free cash flow, and in a worst case that we see inflationary pressures accelerate, it is possible that the company could see another revision to its upfront capital costs at Valentine. I would argue that the risk of a further capital revision is quite low given that costs for some consumables look to have peaked in Q3/Q4 2022. Plus, as noted, the company is sitting on ~$145 million in cash after the royalty sale (excluding $5 million in flow-through dollars) and ~$180 million in available credit, more than covering the ~$300 million in costs left to completion (~$320 million including corporate G&A expenses). Plus, it's worth noting that the ~$320 million cost estimate to completion (construction + estimated corporate G&A) bakes in a ~$29 million contingency, with costs-ex contingency being ~$291 million for project construction + estimated corporate G&A. Hence, I would argue that the risk of taking on any additional debt or seeing further share dilution is quite low.

Given that I see the risk of further share dilution as low and given that Marathon is building Valentine in a period where we have seen a material decline in the rate of change for inflation, I don't see the same risks as there were for Argonaut Gold ( ARNGF ) and Iamgold ( IAG ) when I warned against owning these stocks in H2-2021 when inflationary pressures were worsening. Plus, Marathon's Valentine Project is much smaller in size with a ~6,900 tonne per day throughput rate to start vs. ~37,000 tonnes per day for Cote Gold and the Magino Mine which was built to handle closer to 13,000 tonnes per day. So, with significant share dilution in the rear-view mirror, a strong cash position, and significant and upgraded capacity on its debt facility, I see this as one of the lower-risk names in the junior gold space, even if it does trade at a lower valuation vs. some higher-risk junior peers that aren't fully funded nor permitted today.

Finally, from a gold price perspective, there are obviously risks to producers if we were to see a decline in the gold price below $1,700/oz, but I don't see this applying to Marathon. This is because the company is likely to produce gold at sub $950/oz AISC in its first three years even when accounting for inflationary pressures, and from a valuation standpoint, I've already baked in capex inflation and operating cost inflation into my estimates to derive my fair value on an NPV (8%) basis. So, while Marathon could see a further decline in its share price if sentiment worsens in the sector and the gold price heads lower, I see the company as far better positioned than its gold developer peers with industry-leading future AISC margins and the fact that it's fully funded with a small buffer in place.

Summary

No matter how one slices in, Marathon Gold has quickly become arguably the most undervalued gold developer in the sector on a risk-adjusted basis, with the company trading at a fraction of what suitors have paid for Tier-1 jurisdiction ounces, less than 2.4x FY2026 free cash flow estimates, and barely 0.60x P/NPV using a more appropriate 8% discount rate for developers. This is despite it having a vote of confidence from the sector's largest royalty/streaming company that's doubled down on Valentine (1.5% NSR --> 3.0% NSR), and it's despite Marathon being six months closer to construction than it was when it entered the year at a higher valuation. Obviously, I could be wrong here, and this weakness could continue as the proverbial babies get thrown out with the bathwater. However, with suitors continuing to validate their interest in advanced Tier-1 projects with industry-leading margins (Marathon estimated AISC of $920/oz in the first three years) through takeover deals, I see multiple paths to an upside re-rating.

Some investors might prefer to steer far clear of developers given the capex blowouts we've seen sector-wide, and this isn't an unreasonable decision. However, it's important to note that Marathon completed this study in a period of near peak inflation and while labor costs have remained sticky, we have seen inflation cool off in other areas, suggesting a low likelihood of any capex blowout for Marathon and the potential that it delivers into its estimated cost to completion of ~$347 million which includes a $29 million contingency. So, with a low likelihood of any material capex revision, the company being fully funded and Marathon being barely 18 months away from being one of the sector's lowest-cost Tier-1 producers (~200,000 ounces at ~$925/oz AISC from 2025 to 2028) I see the stock as a steal at current prices. Therefore, I have continued to accumulate a position in the stock on weakness.

For further details see:

Marathon Gold: Too Cheap To Ignore