MPLX - Marathon Is Likely At Peak Earnings But MPLX Is A Hidden Gem

2023-03-20 09:48:03 ET

Summary

- MPC and other refiners are at peak earnings due to high crack spreads.

- However, much of MPC's value can be found in its midstream segment through its ownership of MPLX.

- The stock has some upside from here, but not enough.

Marathon Petroleum ( MPC ) is enjoying a huge boost from wide crack spreads, but the stock looks pretty appropriately priced based on more normalized earnings.

Company Profile

MPC is a U.S. refiner that operates in the Gulf Coast, Mid-Continent, and West Coast. Its refineries process a variety of light and heavy crude, as well as condensate, and produce transportation fuels, heavy fuel oil, and asphalt. It also manufactures NGLs, petrochemicals, and propane.

The Gulf Coast is its largest region with capacity of 1,189 mbpcd. In the region, it operates two large refineries located in Galveston Bay, Texas and Garyville, Louisiana. The Mid-Continent is its second largest region with capacity of 1,159 mbpcd. It has 8 refineries spread out across the region. On the West Coast, meanwhile, it owns 3 refineries with 550 mbpcd of capacity combined, located in California, Washington, and Alaska.

Gasoline represents about half its production, while distillates accounts for another ~36%. It gets about 69% of its crude supply from the U.S. and 20% from Canada. The rest mostly comes from the Middle East.

The company also owns 65% of midstream operator MPLX ( MPLX ). MPLX is a diversified midstream company focused on the gathering, transportation, and storage of crude and refined products. It also gathers, processes, and transports natural gas, as well.

Opportunities and Risks

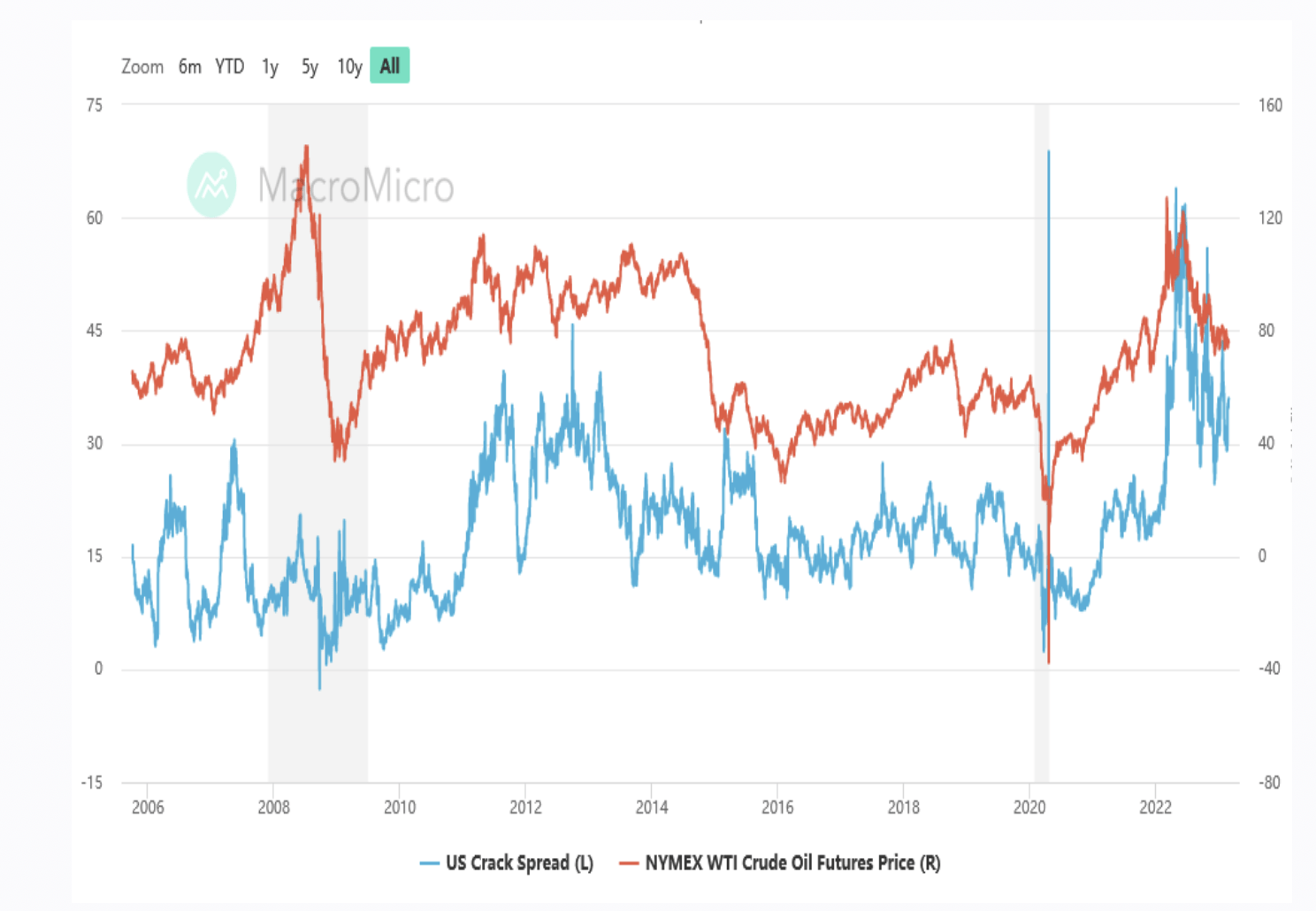

One of the biggest drivers of MPC’s business is crack spreads. In simplest terms, it is the difference between crude prices and refined product prices. On that front, MPC and other U.S. refiners have been enjoying robust refining margins with crack spreads well above historical levels.

Crack Spreads (Market Beat - Nasdaq)

{kind=link}

Crack spreads are near $35 today, which while down from times last year, are still way above historical levels of around $10.50 . Future spreads, however, indicate that the spread is set come down throughout the year, and end in the high teens at the end of the year.

{kind=link}

As such, MPC and other U.S. refiners are likely overearning at this point. The company saw its EBITDA nearly triple in 2022 to $24 billion from $9 billion. Q2 2022 saw enormously wide spreads, resulting in MPC generating a whopping $9 billion in EBITDA for that quarter alone.

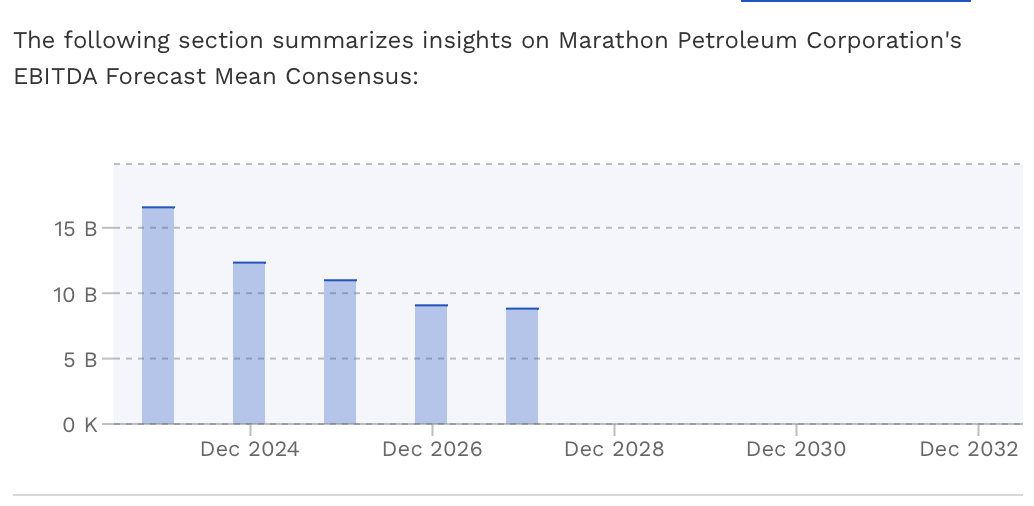

This can be seen reflected in analyst estimates, which see EBITDA continuing to drop in the proceeding years.

{kind=link}

MPC hasn’t built a new refinery since the 1970s, however, it has added capacity through projects. On that front, will add 40,000 barrels a day of capacity this year at its Galveston Bay Refinery through its STAR project. The additional capacity will come online injunction with the refinery’s turnaround in Q1, and begin to ramp in Q2.

Discussing the project on its Q4 call, CFO Tim Griffith said:

“A fair amount of the STAR scope has already been completed and put in service. So it's already earning a return. The remaining work that we have is really going to be completed with this planned turnaround that ends late in the first quarter, and then we'll be starting up the units in April. So we do expect STAR's EBITDA contribution to continue to ramp after startup in April and through the second quarter.

"The remaining scope is really going to increase crude capacity by 40,000 a day and also the resid upgrading capacity by 17,000 a day. So maybe a little background on that decision rather than expand the Galveston Bay cokers, we elected to upgrade the resid hydrocracker unit because it offers better conversion and increased liquid volume yield.

"So it was a better choice than the coker. The fractionation modifications that we made are also going to increase the diesel recovery, which is profitable. And then the refinery will also be able to process significantly more of the discounted heavy Canadian crude. So those are some of the reasons that drove us to that. So we feel really good about the economic drivers of the project. And with the current heavy crude discounts and the strong diesel margins, the near-term economics are better than when we sanctioned the project.”

The company is also doing other growth projects, both to make its refineries more efficient and in the area of low carbon. With the latter, it is spending $150 million in 2023 to complete the conversion of its Martinez facility to a Renewable Fuels plant JV with Neste. Management has said that it is looking to reduce its Scope 1 and Scope 2 greenhouse gas emissions by 30% by 2030; lower its midstream methane intensity 50% by 2025; and reduce its fresh water withdrawal intensity by 20% before 2030.

MPC took advantage of its strong earnings to aggressively buy back stock in 2022. It spent around $12 billion repurchasing nearly 131 million shares. In the process, it reduced its share county by almost 22% on the year. Management said it was continuing to buy back shares this year.

MPC has also been increasing its dividend, raising it 30% in Q4 to 75-cents per quarter. The significant share repurchases allows the company to really ramp up the distribution without having to outlay much more in cash payouts given the less shares. It’s also worth noting that MPC nicely benefits when MPLX raises its distribution, given its 65% ownership in the company. The refiner is getting about $2 billion in distributions from its midstream partner a year.

Valuation

MPC trades at a 4.3x EV/EBITDA multiple based on the 2023 EBITDA consensus of $16.57 billion. Based off of the 2024 EBITDA consensus of $12.3 billion, it trades at around 5.8x.

It trades at 6x forward EPS, with analysts forecasting 2023 EPS of $19.87.

It’s projected to see revenue fall -20% in 2023.

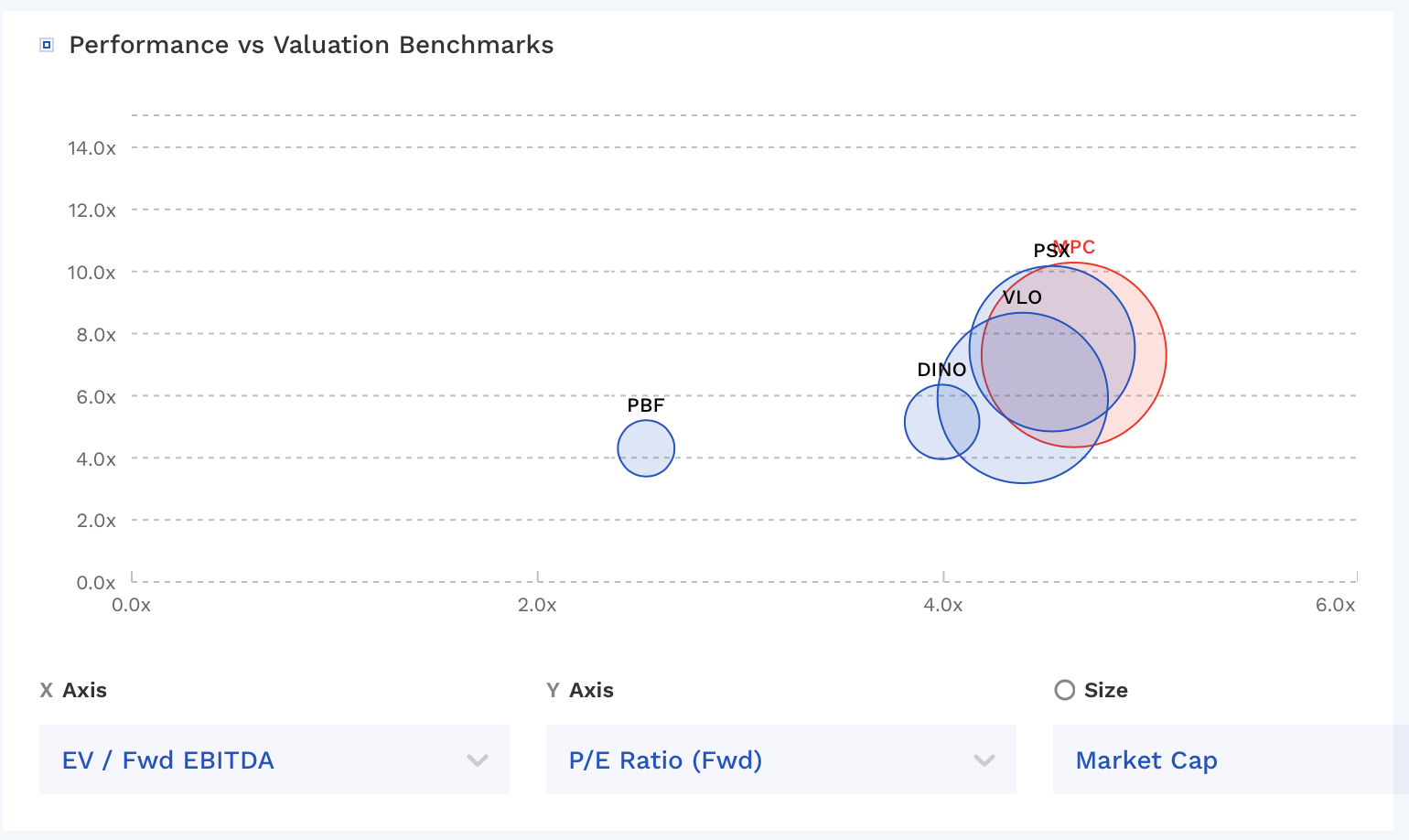

MPC’s stock generally trades in line with other refiners.

MPC Valuation Vs Peers (FinBox)

{kind=link}

Conclusion

All refiners currently look really cheap because they are at peak due to high crack spreads, and MPC is no exception. If we assume that the company will reduce its share count to 400 million in 2023 and that normalized EBITDA is around $9 billion ($6 billion from MPLX and $3 billon from refining), it trades at just over 7x.

That’s a decent multiple for a refiner, but a lot of the value of MPC is in the midstream segment, which typically gets a higher multiple. Thus I think the stock has some upside from here to $140 and but probably not quite enough to put it in the buy category. The longer crack spreads remain high, though, the better the investment MPC will be.

For further details see:

Marathon Is Likely At Peak Earnings, But MPLX Is A Hidden Gem