XOP - Marathon Oil Is A Buyback Monster

2023-05-04 13:39:16 ET

Summary

- In this article, I start by updating my thesis that the oil supply is increasingly bullish for long-term prices by highlighting new developments in the Permian.

- While I remain a long-term bull, short-term demand fears are doing a number on oil prices and its drillers, including Marathon Oil Corporation, one of America's most efficient onshore drillers.

- Hence, by using Marathon Oil's just-released Q1 2023 earnings, I explain what makes this driller so powerful and why buyback-focused investors might enjoy adding MRO stock to their portfolios.

Introduction

It's time to talk about Marathon Oil Corporation ( MRO ) , the buyback-focused onshore producer in the United States. The company has been a holding in my trading portfolio until I decided to focus on income-generating oil stocks. After all, MRO isn't the place to be for dividends but the king of buybacks.

In this article, we'll dive into what makes Marathon an attractive stock, including oil market opportunities and challenges and its just-released quarterly earnings.

So, let's get to it!

Supply Versus Demand

As most readers may have noticed, energy markets are a bit in turmoil.

What we are currently witnessing is a battle between the supply and demand side, and demand is winning - at least for now.

As I wrote in prior articles ( like this one ), we're dealing with significant supply headwinds that could pave the way for a prolonged uptrend in oil prices - especially if demand comes back.

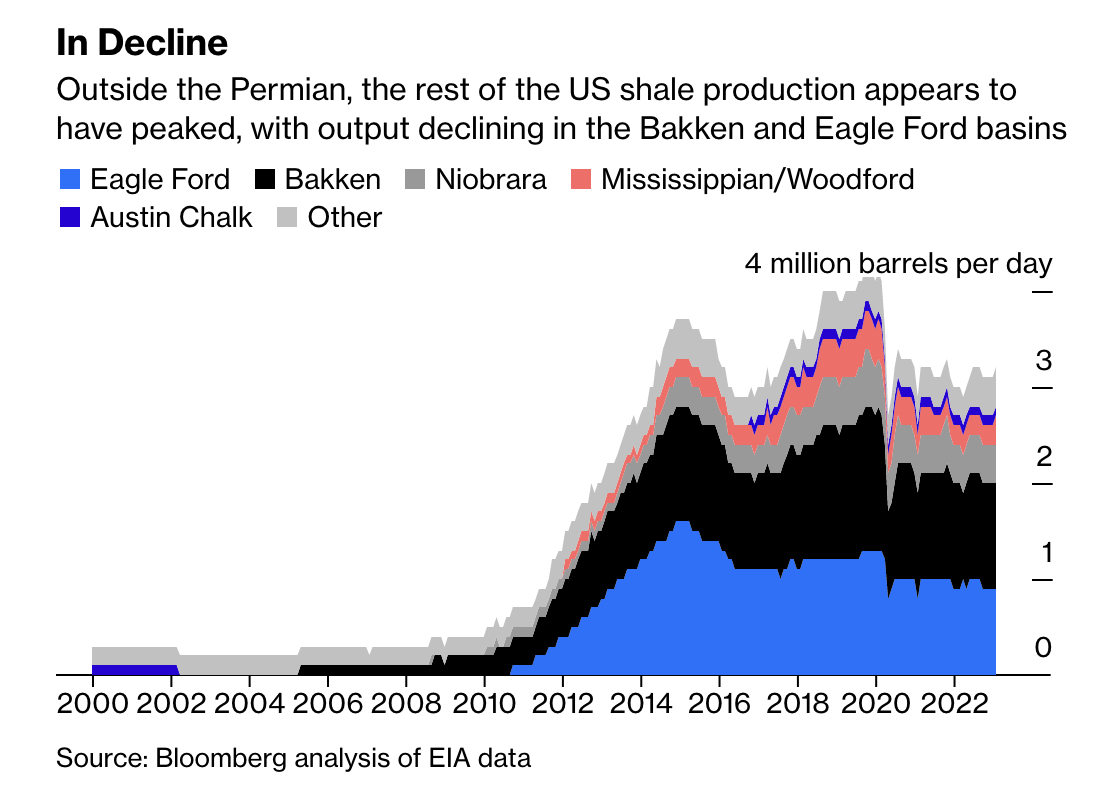

The problem for consumers and everyone dependent on cheap energy is that the engine of supply growth is slowing. In the United States, all basins except for the Permian are seeing a rapid slowdown in production.

{kind=link}

While the Permian is still providing growth, we're witnessing weaker production growth. Legacy production is falling more rapidly.

When legacy oil production in a basin falls more rapidly, it means that the easy-to-reach oil reserves have already been exploited, and the remaining oil is more difficult and expensive to extract. As a result, boosting production becomes more expensive, and oil companies may have to invest in new technology or exploration to maintain production levels.

{kind=link}

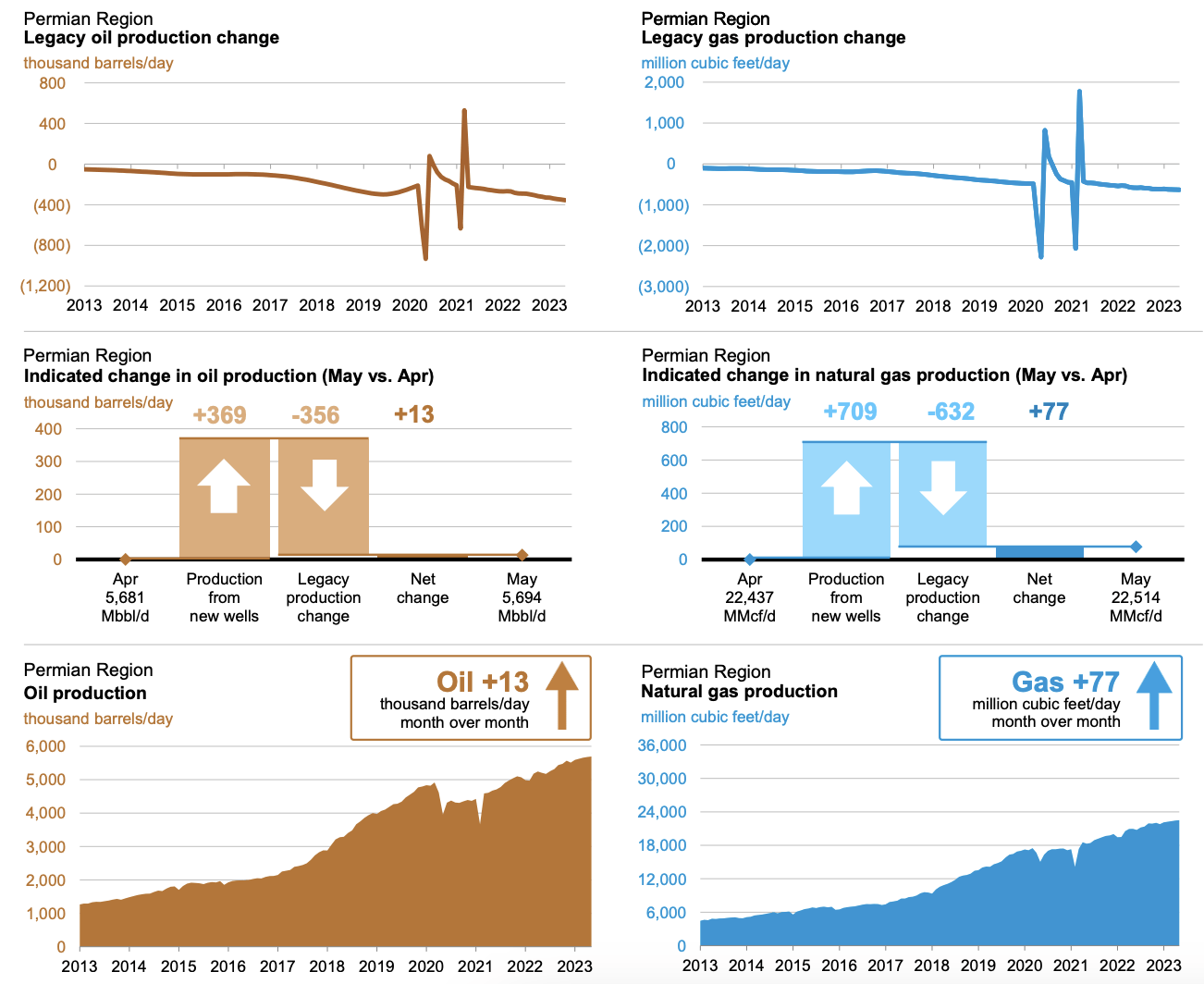

While gas production in the Permian has risen above its prior highs, oil production is having a harder time growing. In April, new wells barely offset the declining production from legacy operations. This was confirmed by my former colleague, energy expert Tracy Shuchart in a recent podcast.

Furthermore, on March 8, The Wall Street Journal reported that frackers are hitting fewer big gushers in the Permian Basin. Major operators are running out of good wells, which also confirms the aforementioned production trends.

Oil production from the best 10% of wells drilled in the Delaware portion of the Permian was 15% lower last year, on average, than top 2017 wells, according to data from analytics firm FLOW Partners LLC. Meanwhile, the average well put out 6% less oil than the prior year, according to an analysis of data from analytics firm Novi Labs.

When adding that OPEC is eager to defend $70 Brent with its new pricing power - with the US out of the picture, it can, once again, determine prices - we get a situation that will likely result in a prolonged uptrend in energy prices. My base case is $100 WTI in a situation of rebounding demand.

Unfortunately (for oil investors), demand has become an issue.

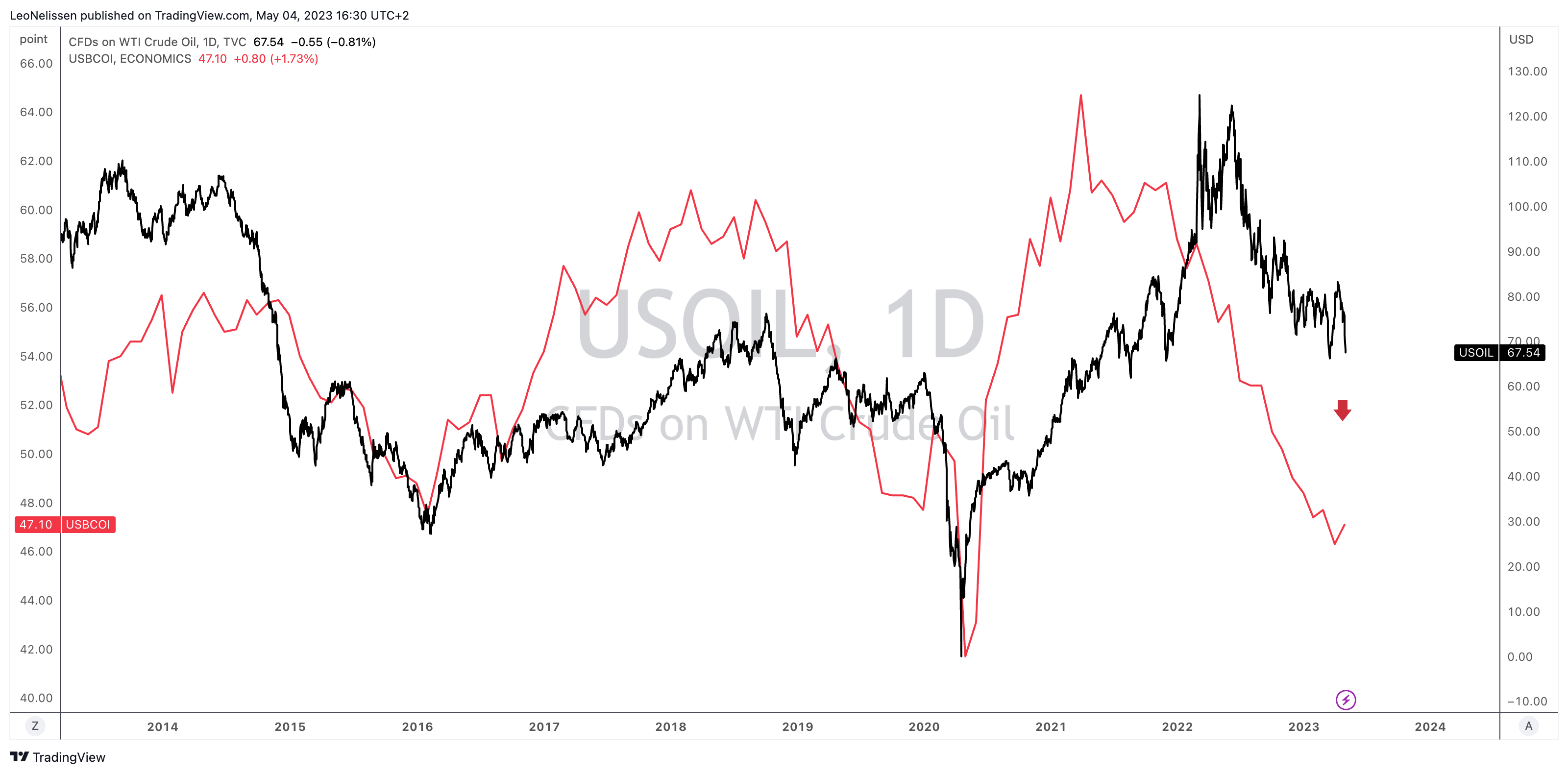

The chart below compares the ISM Manufacturing Index to the price of WTI oil. Economic sentiment has come down significantly, which is amplified by banking woes and a Fed that isn't yet communicating a high likelihood of rate cuts.

TradingView (Red = ISM Manufacturing Index, Black = NYMEX WTI)

{kind=link}

Hence, we're not in the uncomfortable part of the long-term bull case of oil: the cyclical downswing.

The way I'm dealing with this is by buying energy on weakness.

Currently, my dividend portfolio holds a 16% energy exposure, and I intend to increase it further during the current market downturn. Although I initially had doubts about increasing my exposure to this sector, I recognize that missing out on the opportunity to invest in the best drillers while they are undervalued could prove to be a mistake if my optimistic predictions come true.

One of the stocks that deliver tremendous value on weakness is Marathon Oil.

The Benefits Of Marathon Oil

Marathon Oil is one of America's largest onshore oil producers, with a history that goes back to 1887. Then, it was operating as The Ohio Oil Company before being purchased by Mr. John D. Rockefeller's Standard Oil a few years later.

Fast forward almost 140 years, and we're dealing with an independent onshore producer with a market cap of roughly $14 billion.

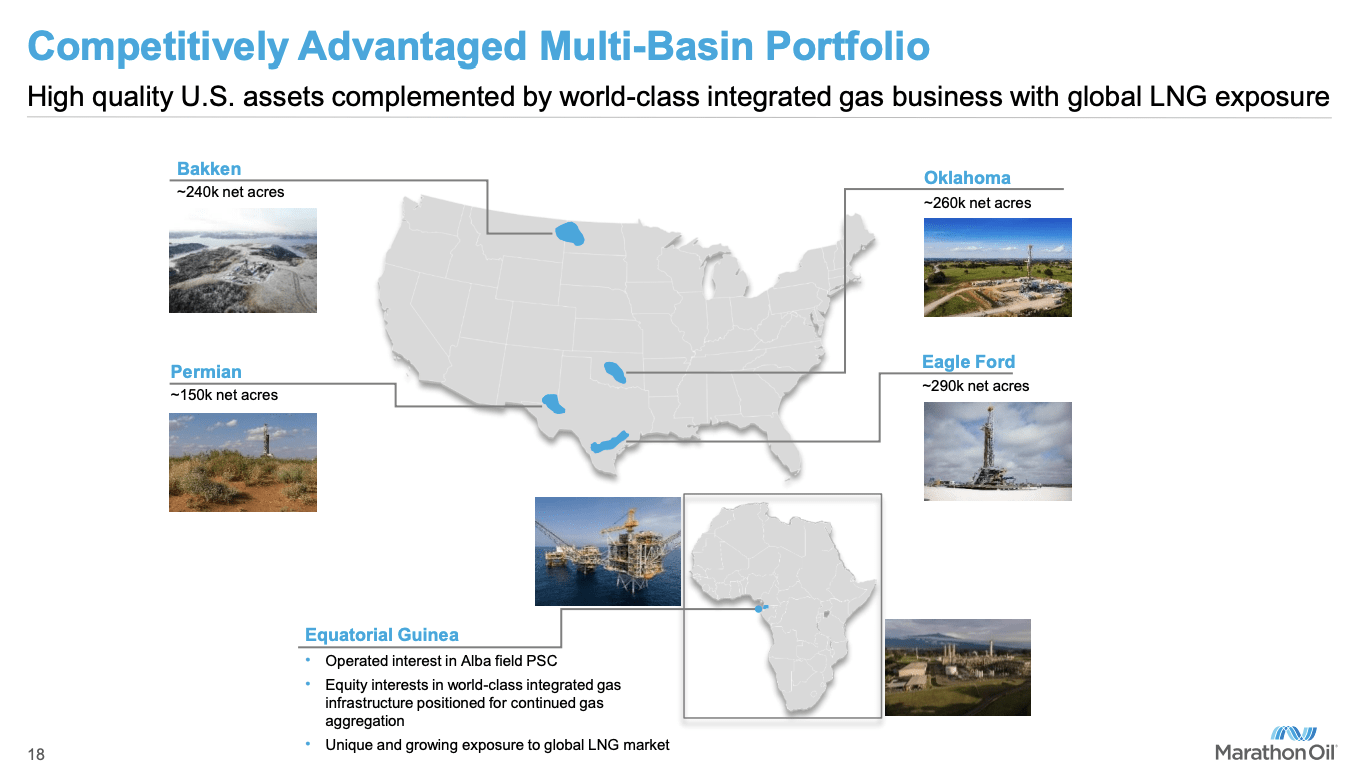

Headquartered in the beautiful city of Houston, Texas, MRO produced 396 thousand barrels of oil equivalent and 186 thousand barrels of oil per day.

Its largest operations are in the Eagle Ford basin, where it produced 144 thousand barrels of oil equivalent per day in the first quarter.

{kind=link}

One of the things MRO is most proud of is its capital return program. Like most major oil producers, MRO is now sitting on a healthy balance sheet , which allows the company to distribute most of its cash to shareholders.

In the first quarter of this year , management retired $70 million in gross debt and remarketed $200 million of tax-exempt bonds. The company has a BBB- credit rating (investment-grade) and an expected 2023 net leverage ratio of just 1.0x EBITDA.

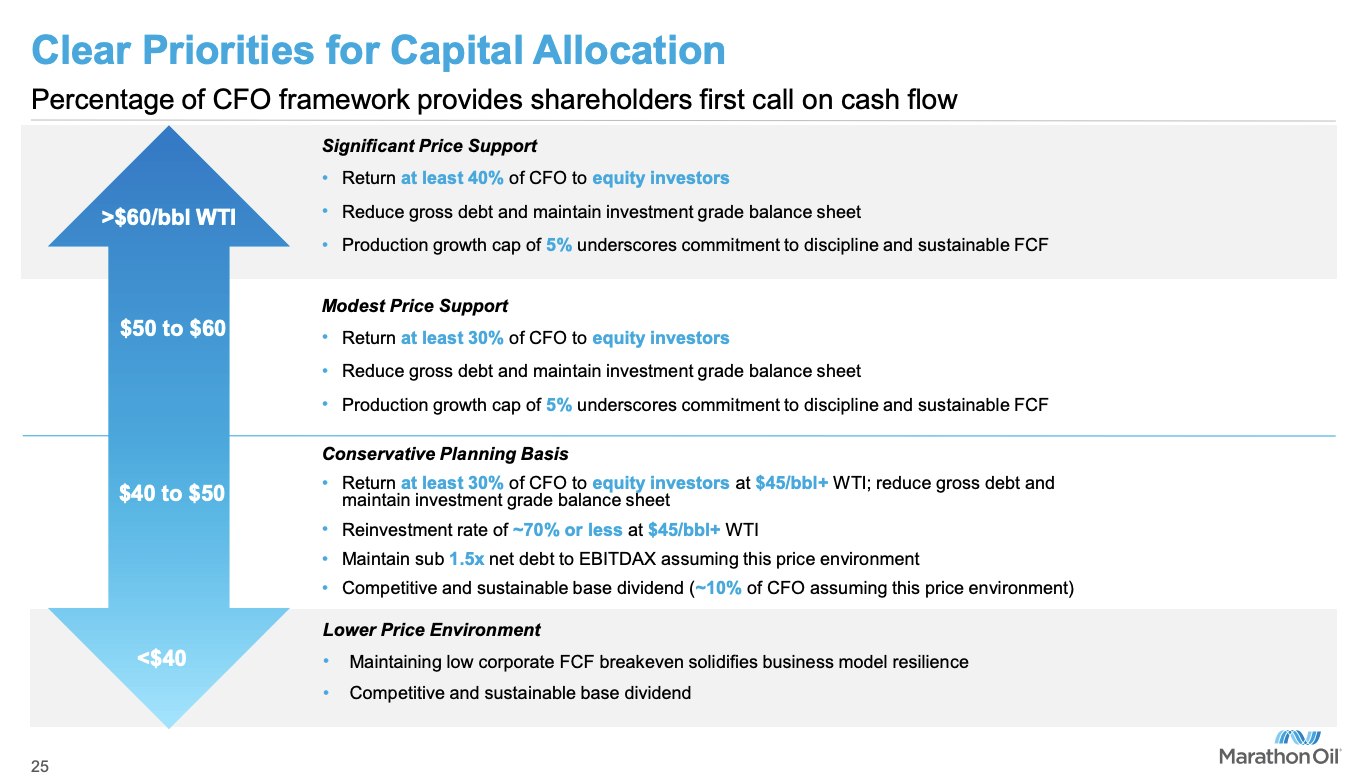

The company's cash flow-driven capital return framework is viewed as unique, as it provides investors with the first call on cash flow and insulates shareholder returns from the effects of capital inflation.

Essentially, what this means is that it has a target to distribute a set part of its cash from operations. Most oil companies target a free cash flow payout, which is operating cash flow minutes capital expenditures. So, that's what the company is saying when it makes the case that this distribution plan shields investors from capital inflation.

The overview below shows that the company aims to distribute 40% of its operating cash flow at oil prices above $60 per barrel. Between $40 and $60, the company aims to distribute at least 30% of operating cash flow. What's also important is that the company does not aim to grow production by more than 5%, regardless of how high oil prices soar, which shows the renewed commitment to growth discipline in the industry.

{kind=link}

In the first quarter , the company exceeded its 40% target, distributing 42% of its operating cash flow. In 1Q23, the company repurchased $334 million worth of shares (2.5% of its market cap) and distributed $63 million through its base dividend.

- The company currently pays a $0.10 per share per quarter dividend. This translates to $0.40 per year or 1.8% of its share price. This is not a high yield, and it does not come with a special dividend. In January, the company hiked its dividend by 11.1%.

- Over the past three years, the company has repurchased more than 20% of its shares (1Q23 is not yet visible in the chart below).

Though peers have now migrated to our model. We were an early proponent of shareholder repurchases and our dollar cost averaging approach since October 2021 has delivered a peer-leading 22% reduction in our shares outstanding. The strength and durability of our shareholder return profile underpinned by strong free cash flow generation and capital efficiency. - Marathon Oil.

The absence of a special dividend is disappointing to me. I am a big believer in high dividend payouts, as I see energy stocks as cash cows (to put it bluntly). That's also why I recently explained (in this article ) that I considered selling Exxon Mobil Corporation ( XOM ), which I have done (but more on that later).

Marathon disagrees with me. The company believes that buybacks are a more efficient means to drive per-share growth than increasing the base dividend, which it has raised eight out of the last ten quarters. That is correct, and it has certainly led to an outperforming share price versus its exploration and production peers.

Over the past three years, MRO shares have returned 320%, outperforming the SPDR S&P Oil & Gas Exploration & Production ETF ( XOP ) by a wide margin.

Don't get me wrong. I'm not saying the company is making the wrong move by focusing on buybacks. It's the most tax-friendly way to (indirectly) distribute cash. It's just not my style. However, it's perfect for investors who prefer buybacks.

With that in mind, the company's operations are highly efficient and capable of generating a tremendous amount of cash - especially at elevated oil prices.

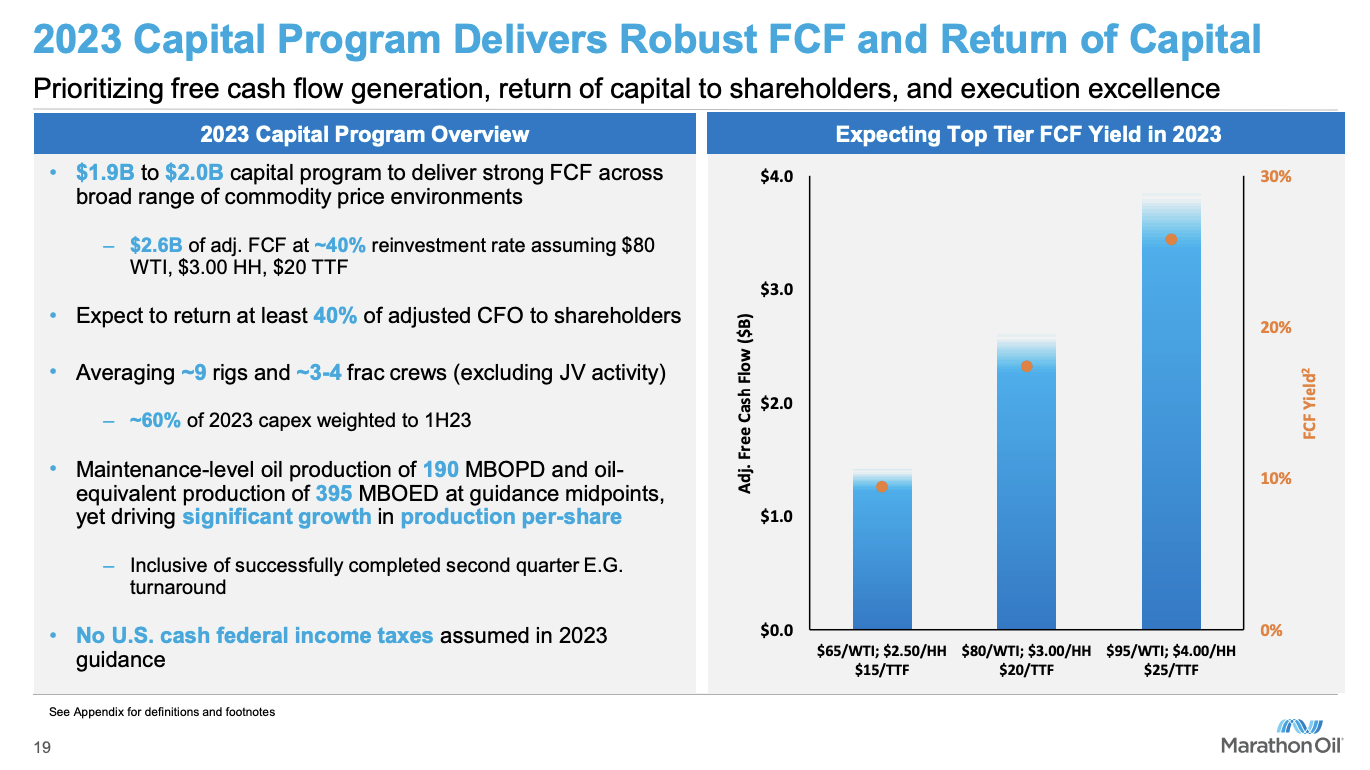

MRO is free cash flow breakeven at $40 WTI, which makes it one of the most efficient producers in the world. This means that at $80 WTI, the company has a free cash flow yield of almost 20%, which shows how much buyback potential this company has. At $95 WTI, the company has a free cash flow yield of roughly 28%. In other words, if oil prices start a sustainable rally at elevated prices, the company can show its true buyback potential. While I prefer dividends, I believe that MRO will likely outperform my oil holdings.

{kind=link}

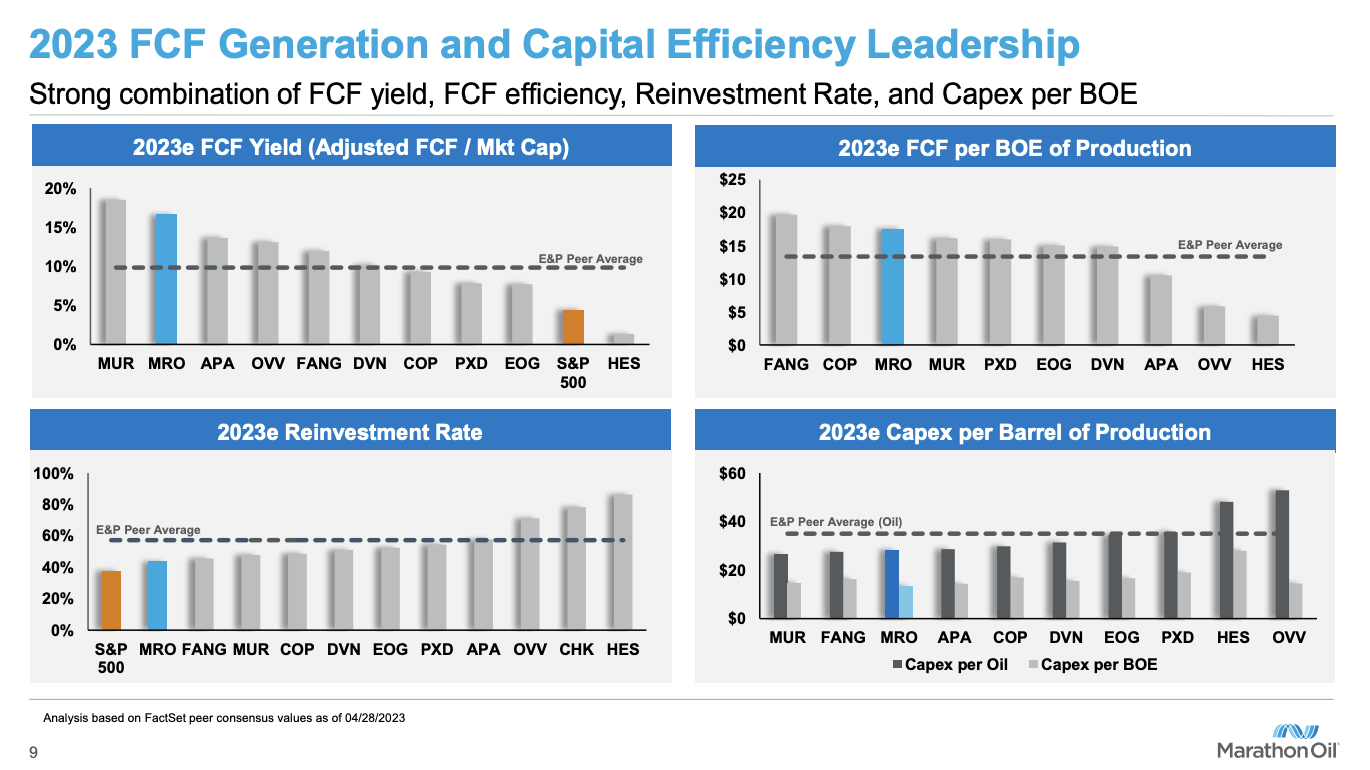

MRO is also winning when looking at other metrics like free cash flow per unit of production and reinvestment rates.

{kind=link}

Furthermore, MRO's first quarter 2023 earnings call revealed that its full-year capital spending and production guidance is unchanged and that the company is on track to deliver its 2023 business plan, which benchmarks at the top of its peer group. The metrics they prioritize include total shareholder distributions relative to market capitalization, free cash flow yield and efficiency, reinvestment rate, and capital efficiency, free cash flow breakeven on both pre-and post-dividend basis, and growth in production per share, which basically means using efficient production to enhance value for the company and its owners.

Adding to that, last year, the company acquired Ensign. This acquisition was successfully integrated ahead of schedule and allowed the company to boost production in the Eagle Ford basin, and MRO saw excellent results from its initial wells to sales.

Speaking of M&A, MRO has a minimum of 10 years' worth of high-quality inventory. That is a lot, and it will give the company time to find new resources in the years ahead. It is not forced to engage in risky M&A deals just to be able to maintain production. That is very important to keep in mind.

Ensign alone has more than 15 years' worth of inventory. Including lower-quality plays, it's fair to assume that MRO is sitting on more than 20 years' worth of inventory.

Takeaway

I remain a long-term oil and gas bull. Supply continues to be constrained, as even the world's oil supply growth engine is now weakening. On top of that, we see that OPEC is using its new pricing power to its advantage, which makes a long-term supply boost even more unlikely.

However, on the demand side, we're seeing weakness, as investors are pricing in a hard landing. Banks are struggling, economic growth expectations are weakening, and the Fed isn't likely to give the economy an easy exit from this mess.

Hence, MRO is struggling - at least on the stock market.

Its shares are 35% below their 52-week high and down 20% year-to-date.

FINVIZ

I am convinced that MRO is a great investment on weakness for buyback-focused investors looking to buy an efficient driller.

The company checks all boxes.

- It has ten years' worth of high-quality inventory (20, including all of its assets).

- The company's free cash flow breakeven point is at $40 WTI, which is industry-leading.

- It has a healthy balance sheet, allowing it to distribute most of its cash to shareholders.

- The company has a 40% operating cash flow payout target, which is unique in the industry.

- At elevated oil prices, MRO becomes a buyback beast with potential free cash flow yields close to 30%.

If I were focused on buybacks instead of dividends, I would be a buyer of Marathon Oil Corporation at current prices. However, because economic demand is weakening, I would be a gradual buyer to average down if the opportunity presents itself, which is likely going to happen.

For further details see:

Marathon Oil Is A Buyback Monster