BOIL - Marathon Oil: What To Expect From 2023

Summary

- Investors should take the comments from Pioneer's CEO seriously regarding the headwinds facing U.S. shale.

- Marathon isn't immune to rising Capex costs either.

- However, even with higher costs and lower oil prices, the FCF yield suggests more upside is possible.

- In the short term, it isn't clear if the market will focus more on the Q4 earnings and buybacks or on the 2023 Capex guidance.

Investment thesis

We are about a month away from Marathon Oil's ( MRO ) earnings call , so I found it a good time to revisit my thesis, especially in the light of recent downgrades from the street. The majority of analysts are also downwardly revising their earnings estimates:

{kind=link}

Full-year 2022 EPS estimates now stand at $4.55, reflecting a 5.95x P/E multiple. The consensus estimate for 2023 is $3.58 per share.

WTI oil ( CL1:COM ) averaged $95 for 2022 while the latest short-term energy outlook from the EIA forecasts $77 for 2023, so to some extent this makes sense. There are also concerns about oilfield services inflation. In November 2021, MRO guided toward $1.0 billion annual Capex to keep production flat; in February 2022, the Capex for 2022 was set at $1.2 billion; yet, in November 2022, it was revised up to $1.4 billion. So comparing '22 to '21, it is basically a 40% increase for essentially the same production.

On the other hand, even if we assume another 40% YoY Capex growth for 2023, at $77 WTI, Marathon will still earn a 14%+ FCF yield. Marathon has also shown itself to be the most aggressive of the large U.S. independents when it comes to share buybacks; this should continue providing a floor for the stock price.

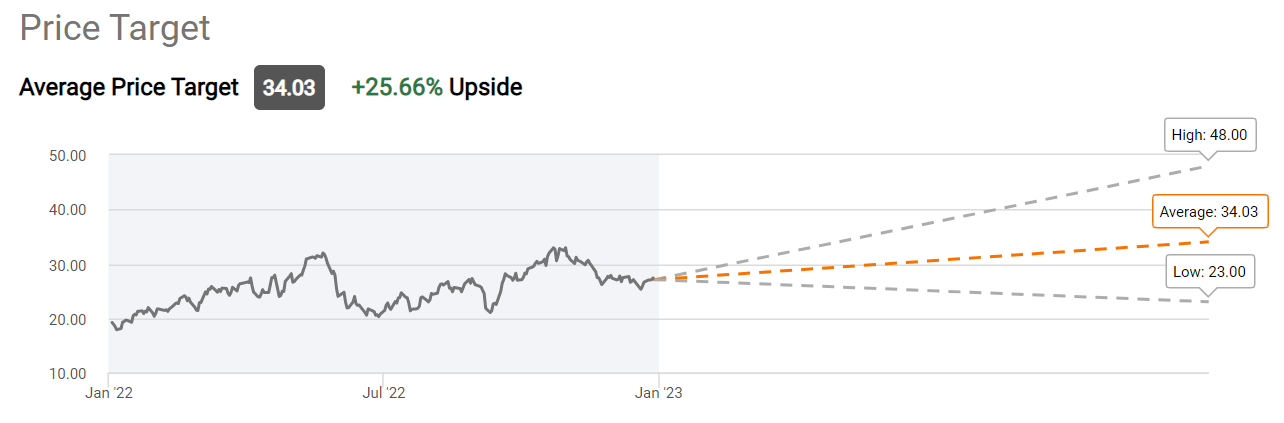

Overall, I remain bullish and can still see MRO ultimately going to $37 if oil prices remain where they are today; my target would correspond to a 10% FCF yield.

The average street target is $34 although there is a wide range around it:

{kind=link}

Background

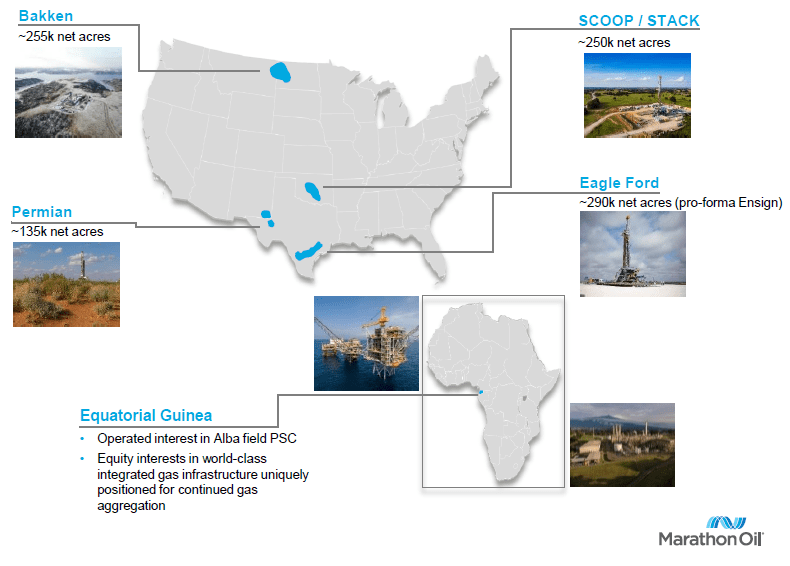

I have covered Marathon before and you can see my prior articles here . While MRO derives significant income from its operation in Equatorial Guinea, it remains mostly a U.S. shale player and that will remain the case after the Ensign acquisition closes:

{kind=link}

Like many of its U.S. shale peers, Marathon has been prioritizing cash returns to investors over growth. The Capex is meant to maintain production flat.

U.S. shale may face headwinds

U.S. shale has been the pivotal global producer for quite some time now, but signs are emerging that shale production may have peaked already or will do so soon. Two of the main culprits are rising oilfield services inflation and E&P companies running out of top-tier drilling locations.

The CEO of Pioneer ( PXD ), one of the largest shale producers, made some very interesting comments recently (my highlights):

We have the Permian - about a year or two ago, I stated it was going to go to about 8 million barrels a day to 2030. The EIA has it at 5.5 million barrels of oil per day. We have lowered that to about 7 million by 2030. The reason we've lowered it is that people - obviously, the effects of moving to what I call stack development in both the Delaware and also in the Midland basin. And that's combining either the Bone Springs or the Sprayberry, depending on which basin you're in, the shallower formation with the Wolfcamp zones. It's better to drill four wells or six wells, all at the same time to get the best performance. Also, there are a lot of companies that are moving - they're running out of inventory. They are moving to tier two and tier three inventory.

Also, I'll make a point. Chevron made a point recently that they were going to produce 1.2 million to 1.5 million barrels of oil equivalent per day by 2040. But this is the first time somebody put out a number that far, there's only three companies in my prediction that will be over 2030 in the Permian Basin over a million barrels of oil equivalent per day, that's Chevron, Conoco and Pioneer. There are the only three that have an inventory that deep, can take it over a million barrels of oil equivalent per day.

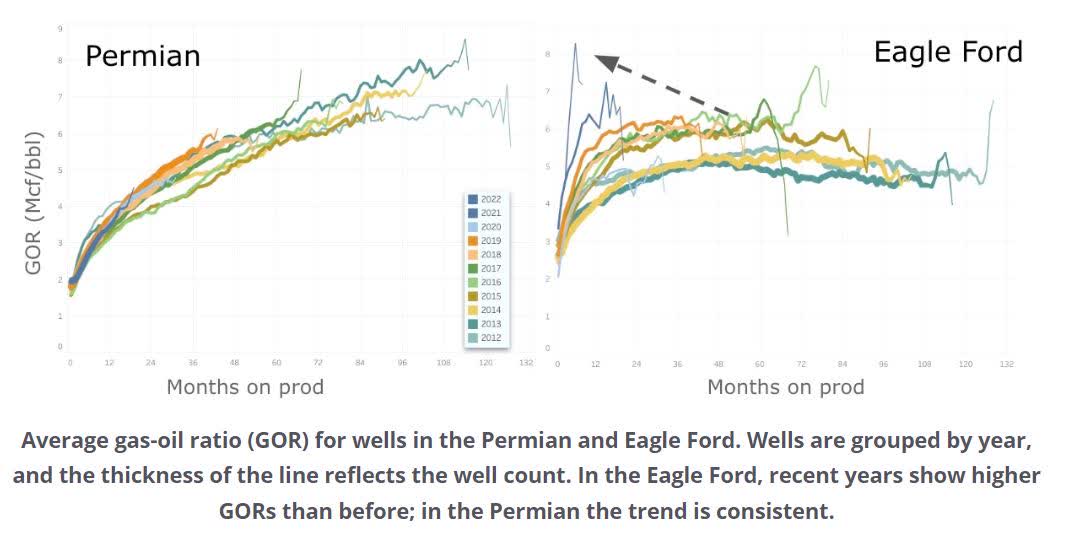

Now what's going to happen over time. The gas/oil ratios in the entire Permian Basin will continue to go up. We're seeing that. You'll see the percent oil drop for all those companies, most likely below 50% over the next 10 years. And the gas itself will get up to about 30 BCF. We're going to need a gas pipeline, at least about every 18 months to two years going forward.

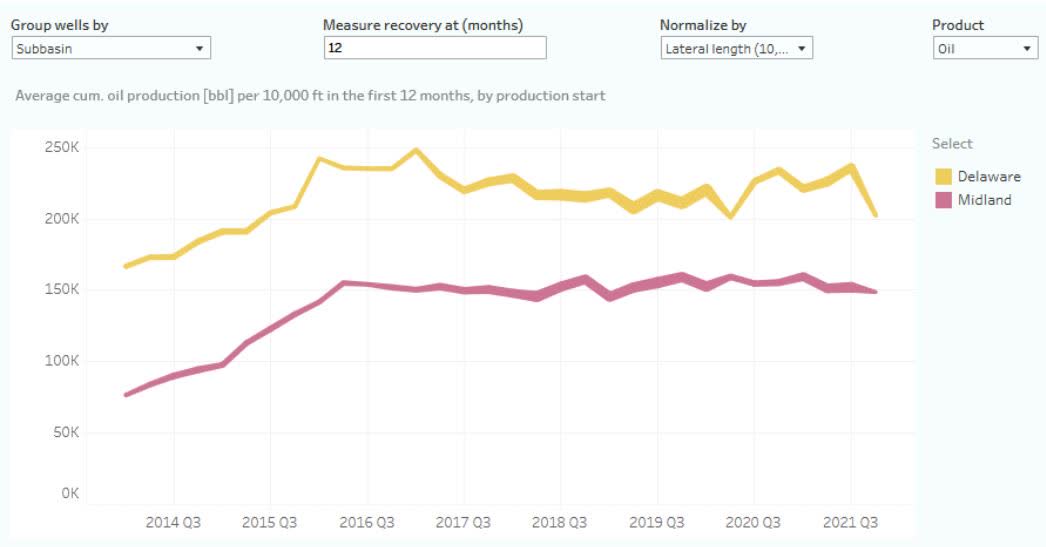

A relevant chart from Shaleprofile also suggests that well productivity (normalized by lateral length) may have peaked already:

{kind=link}

Shaleprofile isn't yet seeing wells getting more gassy:

{kind=link}

They believe the rising gas-oil ratio in the Eagle Ford reflects more of a strategic choice by operators to drill in gas-rich locations, but this data is also only through August 2022. So the comments by Pioneer's CEO which focus on the next 10 years may very turn out true.

Not all is bad news

Shale won't run out of oil tomorrow. Rather, over time, more expenses, capital and operating, will be needed to produce the same amount of oil as before, as with any depletable resource. Neither does a company with declining business or cash flows have to be a bad investment as value also depends on the price at which the company is offered; Altria ( MO ), for example, seems to do just fine despite secular headwinds in its main business.

Also importantly, behind the basin "averages", not all companies are the same; some have better acreage than others and will fare a lot better. Marathon's more recent Permian wells from 2021-2022 appear on par with the years before:

Shaleprofile

So does Eagle Ford:

Shaleprofile

In the Bakken, Marathon's 2022 well performance seems a bit under:

Shaleprofile

The Ensign acquisition should also help Marathon maintain its pipeline; from the press release (my highlights):

The transaction significantly expands Marathon Oil's Eagle Ford position through the addition of 130,000 net acres with 97% working interest located primarily in the prolific condensate and wet gas phase windows of the play. The Company estimates it is acquiring more than 600 undrilled locations, representing an inventory life greater than 15 years , with inventory that immediately competes for capital in the Marathon Oil portfolio. The acreage is adjacent to Marathon Oil's existing Eagle Ford position, enabling the Company to further leverage its knowledge, experience, and operating strengths in the Basin, while materially increasing its Basin scale to 290,000 net acres and contributing to optimized supply chain accessibility and cost control in a tight service market.

My sense is that most of the less profitable acreage may be with private companies; public companies seem to have better-quality inventory, and, among public companies, Marathon's management has one of the best reputations. So while MRO can't escape the rising cost curve either, I think they will do better than the average.

Valuation update

I started with the cash flow from operations (or CFO) posted by Marathon for the last four quarters since October 2021. The CFO has a strong correlation with the WTI price, so I estimated what 2023 CFO should be based on $77/bbl. I then quite conservatively assumed that 2023 Capex will grow by another 40% from the already higher 2022 Capex:

Seeking Alpha; EIA; Author's Calculations

I still got to a 14%+ FCF yield. Needless to say, if oil prices rebound as I think they may , we will quickly revert to the 20%-25% yields we saw in 2022. If we remain in the high 70s, I still see a strong case that Marathon remains undervalued. Note my analysis doesn't include Ensign; my guess is Ensign would improve the numbers, but we'll have to wait for MRO's management to release more data.

The buybacks should continue

Marathon's cash return framework is crystal clear and I don't want to repeat it here. Basically, if WTI is above $45+, there shall be cash returns to equity investors. And they walk their talk; here is how MRO's share count reduction compares to some peers:

| Ticker |

| Shares Q3, millions |

| Shares 2021, millions |

| Reduction |

| MRO |

| 635 |

| 743 |

| 14.5% |

| APA ( APA ) |

| 323 |

| 346 |

| 6.7% |

| Conoco ( COP ) |

| 1246 |

| 1302 |

| 4.3% |

| Ovintiv ( OVV ) |

| 249 |

| 258 |

| 3.4% |

| Oxy ( OXY ) |

| 908 |

| 934 |

| 2.8% |

| Pioneer ( PXD ) |

| 237 |

| 242 |

| 2.1% |

| Devon ( DVN ) |

| 654 |

| 663 |

| 1.4% |

| Diamondback ( FANG ) |

| 175 |

| 177 |

| 1.1% |

| Hess ( HES ) |

| 306 |

| 308 |

| 0.5% |

| EOG ( EOG ) |

| 587 |

| 585 |

| -0.3% |

Source: Seeking Alpha; Author's Calculations

Marathon leads the group by a mile and it matters; almost 15% EPS growth will be added just from the buybacks themselves.

Closing words

Shale's best years may be coming to an end as I discussed in my recent macro article , but that doesn't mean every shale producer is in the same boat. Everyone sure faces oilfield services inflation, but some companies have better inventory are more adept management than others. I think Marathon is above average on both metrics and its shareholder friendly policy should continue helping the stock in 2023 too.

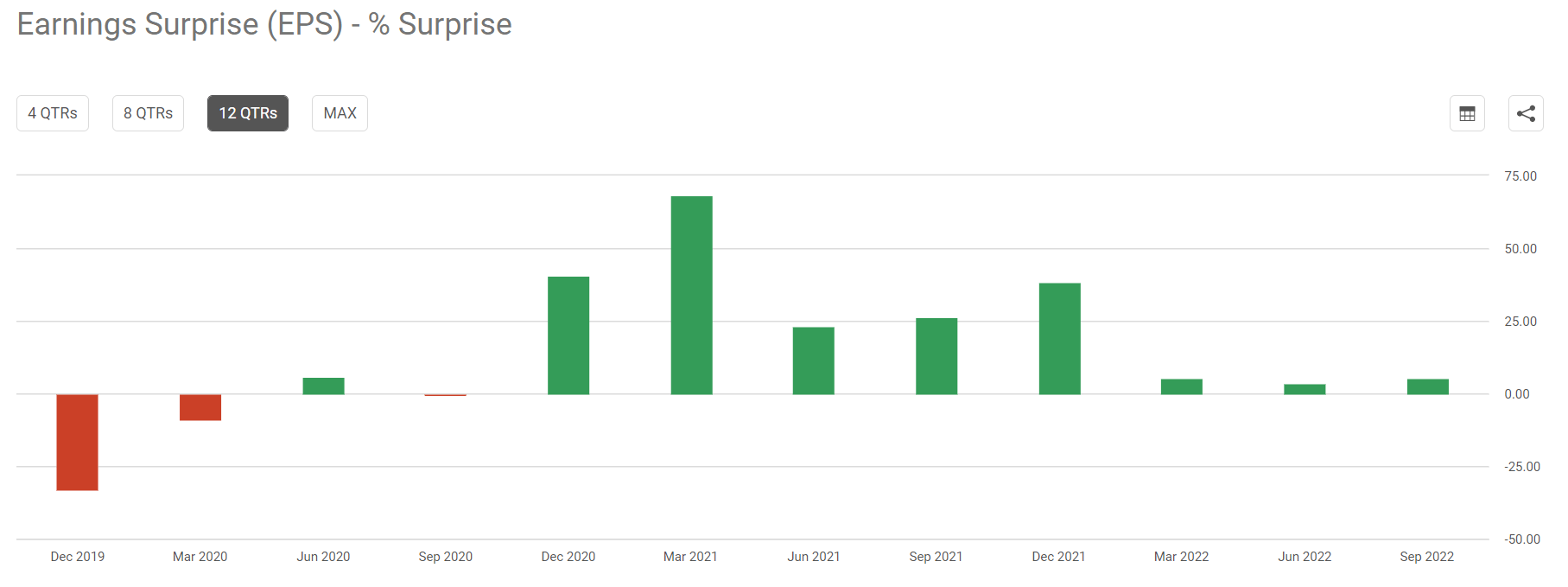

In the shorter term, the company may deliver yet another positive EPS surprise in February as it has done for eight quarters in a row now:

{kind=link}

But I would also expect a significant increase in the 2023 capital program guidance and I don't know how the market will take such an announcement. For me, any Capex increase of less than 40%, without Ensign, would probably be bullish.

For further details see:

Marathon Oil: What To Expect From 2023