MPC - Marathon Petroleum: A Deep Value Play Yielding 14%

2023-05-21 07:40:50 ET

Summary

- Marathon Petroleum is the biggest player in its industry. It runs a tight ship, producing profits in almost all market types.

- We think crack spreads are likely to stay higher for longer due to chronic underinvestment in the sector.

- The company is very undervalued in light of this.

- The stock is volatile, and the best way to reduce risk and earn yield is by selling put options on the stock.

Recently, in an article titled " PBF Energy: Earn A 13.6% Yield With This Deep Value Gem ", we covered PBF Energy ( PBF ) and its stock in detail, analyzing the company's financial results, valuation, and potential risks. Ultimately, we posited that a short put strategy was the best way to play the stock, a thesis which is playing out well so far. Since publishing more than a month ago, stockholders are down almost 13% on the underlying, while put sellers who took the trade, we mentioned are up just over 1%; a big spread in performance.

At the present moment, Marathon Petroleum ( MPC ) offers a very similar setup to PBF Energy in the above article.

Marathon offers long term investors a strong value proposition, based on its history of operational success, as well as its attractive multiple. With a track record of turning top line results into bottom line cash flow, in addition to the recent selloff, we think it's time to begin building a position.

The main difference here vs. PBF is that MPC is even larger and more well diversified, so the risks are further mitigated and the underlying financial strength is also improved.

For those looking to get involved, a short put strategy presents the most attractive way to deploy capital. By selling put options on MPC stock, investors can generate yield while mitigating risk, all while potentially acquiring a stake in a robust company at a good price.

Financial Results

We will talk about the specifics of the aforementioned option trade in a minute, but first let's take a look at MPC's recent financial performance.

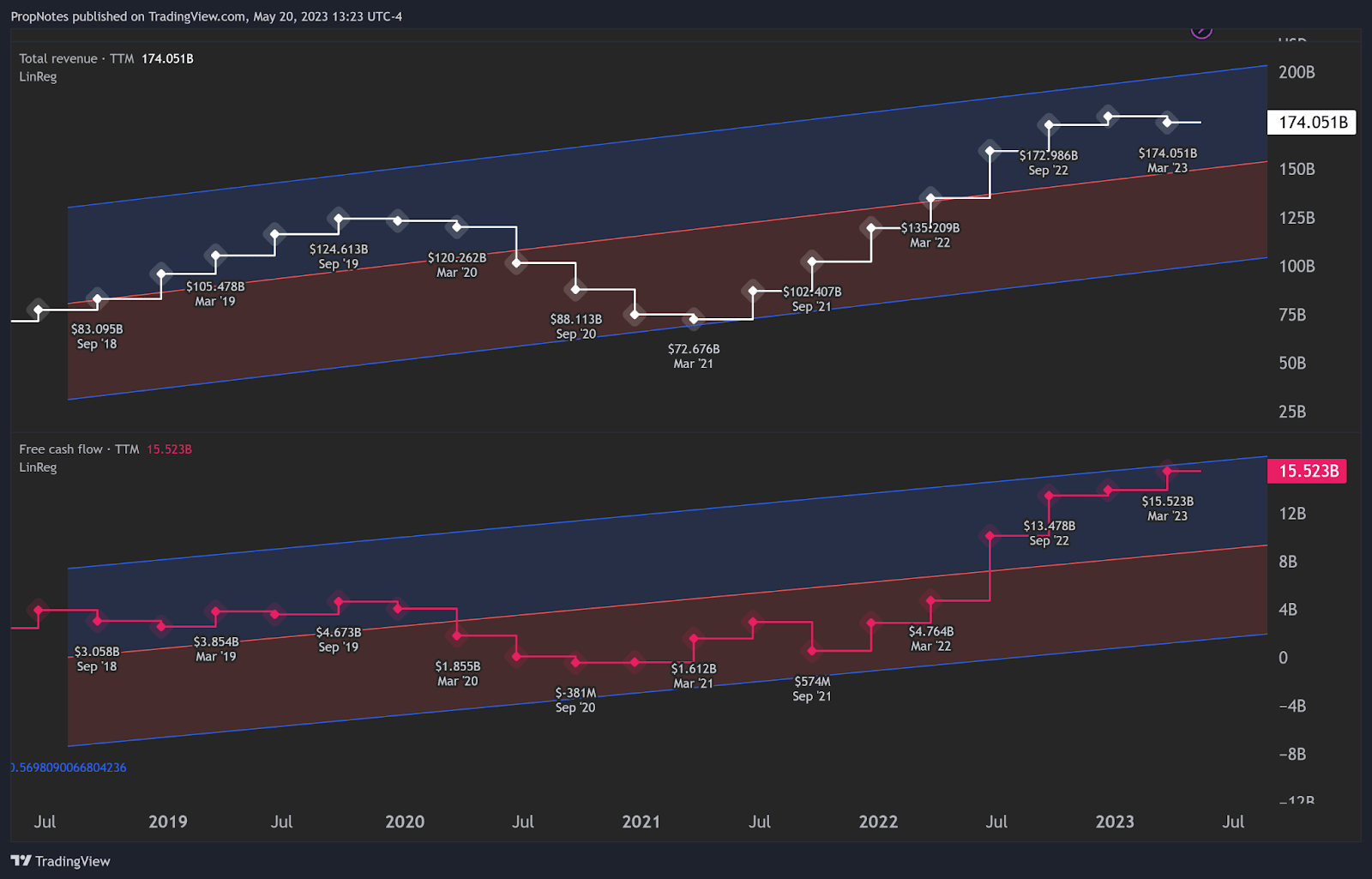

Over the last twelve months, Marathon reported ~$174 billion dollars in revenue, and managed to keep $15.5 billion as free cash flow. That's a healthy 8.9% cash flow margin and similar to other peers in the refining industry.

Impressively, these results follow a period one year before where the company reported ~$135 billion in revenue, and $4.6 billion in free cash flow ("FCF"):

{kind=link}

This high growth rate can be explained by the price shock in energy markets over the last 14 months that was driven by Russia's invasion, a continued rise in consumption, and weakened refining capacity given chronic underinvestment. As an energy company, it should be no surprise that higher crack spreads and reduced competition is good for business.

However, the most encouraging thing about MPC is actually its historical performance. Any energy company can do well in a boom, but it takes real strength and operational efficiency to stick around through cycles.

Luckily, long term results have been great.

In the 5 years prior to the energy shake ups in 2020, MPC averaged $79.6 billion in revenue, and $2.52 billion in net income. They accomplished this with no years in the red. This stands in stark contrast to other energy companies in the space that suffered losses or went out of business during the energy slump that was present for most of that time frame.

While MPC wasn't immune to this, and those numbers are less impressive than the recent results in both nominal amount and margin percentage, it validates that MPC can stick around in lackluster markets while remaining nimble enough to capitalize on good ones. The source of this strength is the company's size, and diverse lines of business which range from refining revenues, to midstream fees, to retail gas stations. This size and strength acts as a buttress to market volatility.

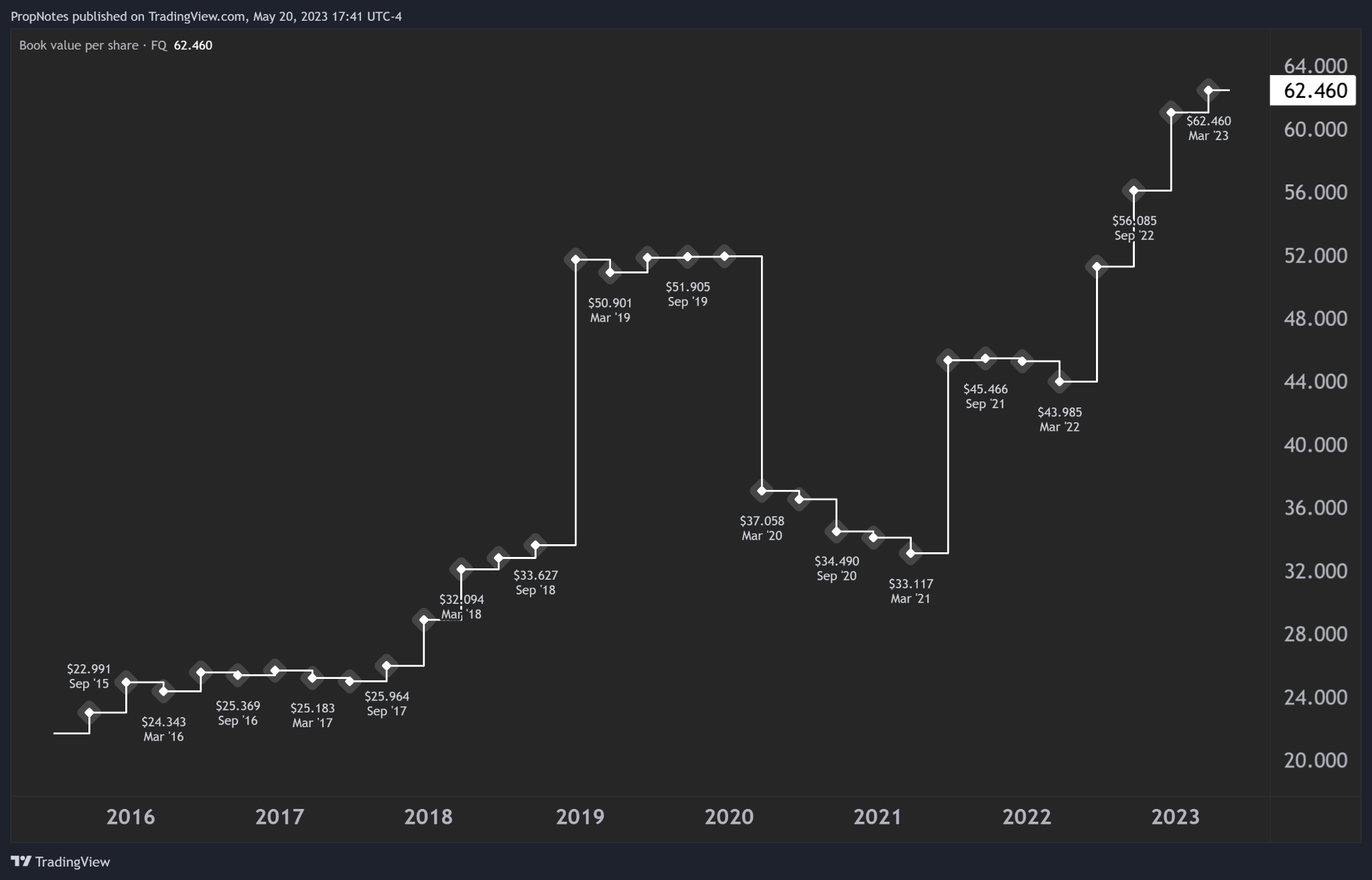

From a liquidity perspective, MPC is also in good shape. The company's total assets far outweigh its liabilities, and book value has grown over the last decade from $11 billion to more than $33 billion; just check out this chart of book value per share:

{kind=link}

Additionally, MPC's cash position is robust, with current assets of $32 billion vs. current liabilities of only $17 billion. Finally, long term debt (which lies around $26 billion) is easily serviced by the company's cash flows. There don't appear to be any major red flags on the liquidity front.

Valuation

Recent results have been strong, but the valuation is what has us paying attention. Similar to PBF a month ago, both "current" and "normalized" multiples seem highly attractive and provide a big margin of error for those entering the story now.

Looking at "current" multiples, the numbers show an "incredible" deal. We have "incredible" in quotes, because the multiple is very, very low at only 3.1x free cash flow. Normally this would be a huge red flag, but in this case, it is simply the market anticipating some mean reversion in profits. As crack spreads come down and the market stabilizes, most are predicting a slowdown in MPC's profits.

We agree that profits will come down, but we also think crack spreads will stay higher for longer as a result of the underinvestment we mentioned earlier. Unless end customer demand falls substantially, refinery capacity will still be in high demand for the foreseeable future, doubly so because building new refining capacity is politically unpalatable as the country tries to make the transition to renewable energy. We think the company has the ability to generate more profit than the market is expecting over the medium term, which makes the current price a bargain.

However, even if results come back down to historical norms in short order, MPC still looks attractive. Using the pre-2020 data we mentioned before, if you calculate a "normalized" net income multiple, you'll still end up with ~18x, which seems reasonable for a company that returns capital to shareholders, and that is as large, diversified, and stable as MPC.

Add it all up, and we think MPC is being undervalued by the market and presents significant value.

The Trade

Alright - it's time to talk about how to take advantage of MPC's solid underlying operations but inherently volatile stock: by selling put options. Sure, buying the stock outright would be more straightforward, but selling puts is preferable because it mitigates risk and generates income.

How?

In essence, selling a put involves selling an option that states that you will be willing to buy shares of MPC stock, should the stock drop below a certain price - the Strike Price - before a certain date - the Expiration Date. In return for committing to buying the stock at that price, the seller receives a cash premium, which acts as income generated from the transaction.

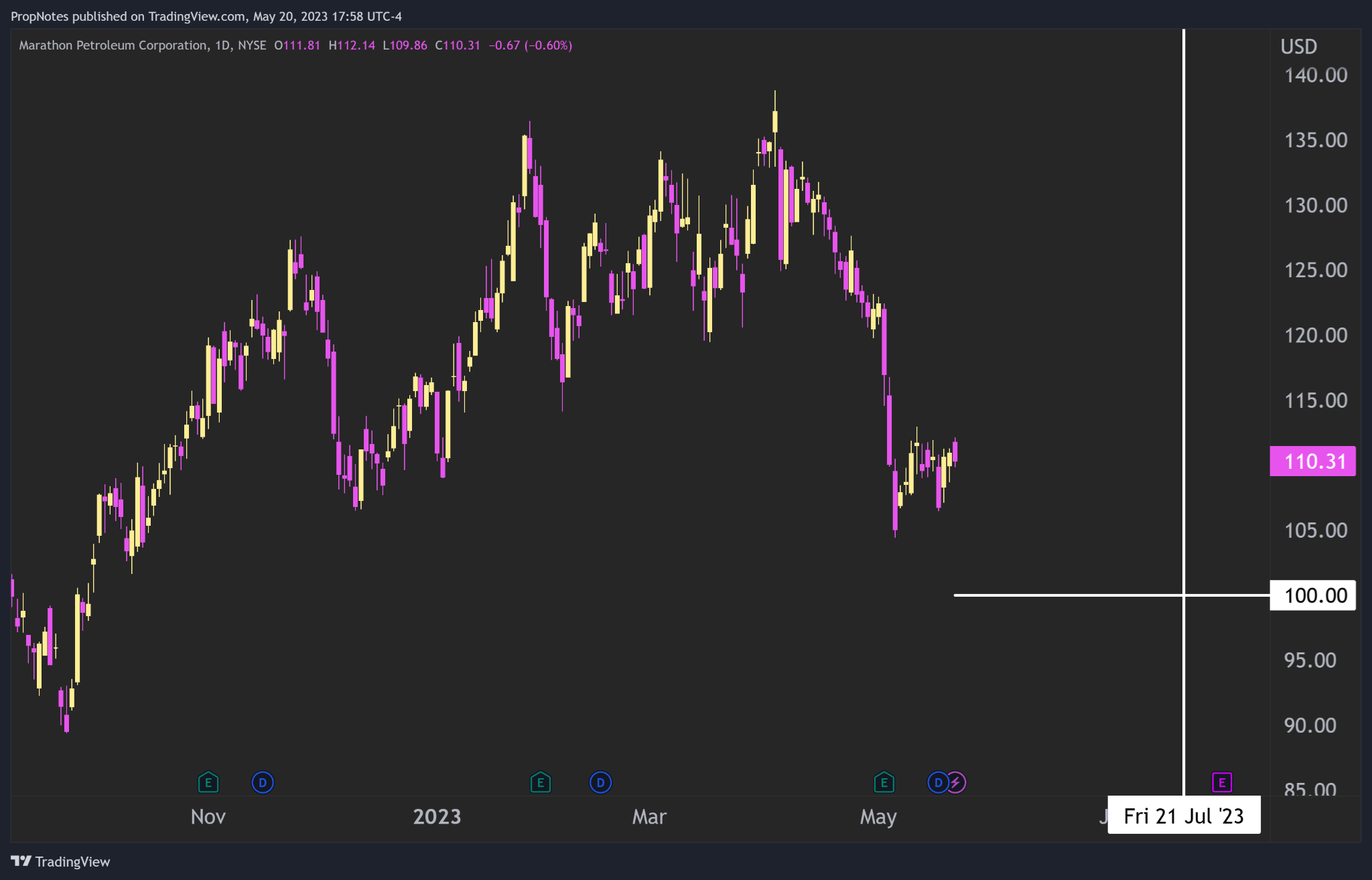

For our trade, we like the July 21st, $100 strike put options:

{kind=link}

Given that the stock is trading at ~$110 per share as of writing, the option premium of $2.35 per share would yield a 2.41% return on invested capital over the next 61 days. This annualizes to approximately 14%, which is robust.

When the option expires, sellers will either be assigned the stock at $100 per share (if the stock finishes below $100, or get to keep the cash as income no strings attached. If assigned, put sellers would be getting shares at an 11% discount to current market fair value.

In sum, selling put options on MPC allows you to generate income and mitigate risk while potentially acquiring the stock at a lower price if the option is assigned. Which, to us, seems like a big win-win.

Risks

Similar to the PBF situation we discussed a month ago, this trade idea presents potential rewards, but there are some similar risks to consider as well.

Macro Risk : While MPC does a good job of executing its own business plans, there's less control that it has over interest rates and government policy. It's possible that government regulations could come down harder on the politically unpopular energy industry, which may hurt profits or increase compliance costs.

Commodity Risk : As MPC has a substantial oil refining business, their profit margin is somewhat determined by the prices of the raw products they take in (crude oil), and the refined products they put out (Gasoline, Heating Oil, etc.). All of these markets are highly liquid and exchange-traded, and thus unfavorable spreads could hurt margins or even cause losses. That said, Marathon also operates midstream assets and end-market gas stations, which diffuse this risk somewhat.

Technical Risk : On the weekly timeframe, some technical analysts may argue that MPC stock is overbought, according to a number of different technical indicators. We think there is room to continue higher, or at least chop sideways, but it's possible that a technical correction (sentiment based) may strike and cost investors some losses.

Summary

In conclusion, options seem like the best way to capitalize on Marathon's attractive valuation and stable financial performance. By selling put options on MPC stock, investors can generate income, mitigate risk, and potentially acquire shares at a lower price if the option is exercised. With an -11% breakeven point, or a 77% chance of a 14% annualized return, it's hard to argue it's not a win-win trade and a great way to deploy capital in an uncertain environment.

For further details see:

Marathon Petroleum: A Deep Value Play Yielding 14%