MPC - Marathon Petroleum: Buy On Upside After 590% Return Since Covid Low

2023-04-19 09:56:22 ET

Summary

- 2022 was a solid year for Marathon Petroleum Corporation, as global refining supply was in constraint, contributing to a solid crack spread, crude differential, and capture environment for the industry.

- The sale of Speedway helped to strengthen the company's balance sheet and return capital to shareholders through buybacks and dividends.

- Martinez is almost near Phase 1 startup while Phase 2 is scheduled for the second half of 2023.

- Since Mike Hennigan became CEO in March 2020, Marathon Petroleum has executed very well in a volatile environment and generated best-in-class returns for investors.

- My 1-year price target for Marathon Petroleum is $151, based on a 12.5x 2024F EV/FCF or 8% FCF to EV yield.

Marathon Petroleum Corporation ( MPC ) has had a good run since its covid-19 low, returning 590% since then. A member of Outperforming the Market asked what should they do with the position in the company given how strong stock performance will be. Where will Marathon Petroleum head next? This article will look into how the company performed in 2022, what it is doing to invest in its future, what it is doing to generate additional returns for shareholders, and how it has been successful in reducing operating expenses and being disciplined on capital expenditures.

Marathon Petroleum share price performance (Marathon Petroleum)

{kind=link}

2022 was a record year for global refiners

As a result of a constraint on supply and rising global breakeven, 2022 was a good year for refiners like Marathon Petroleum.

During the 2019 to 2022 period, global refining supply was constrained as a result of reductions in capacity.

This was contributed by the poor economics during the covid-19 troughs, physical damage that would have been expensive to repair, and conversions towards Renewable Diesel.

For Marathon Petroleum, as a result of the difficult operating environment in the covid-19 trough, it made the decision to indefinitely idle the Gallup Refinery. This is based on the assessment of the impact from the covid-19 situation as well as the company's competitive position of its assets.

In addition, the fire at Philadelphia Energy's refinery in 2019 was an example of capacity that was reduced as a result of the damage caused by the fire that was deemed too expensive to repair by the company, resulting in the additional loss of global refining supply. Lastly, as Marathon Petroleum is increasingly looking to move towards Renewable Diesel, this has led to lower incremental global refining supply. This is an initiative by Marathon Petroleum, called Martinez Renewable Fuels Project, which is its joint venture with Neste, where they are planning to ramp up and reposition its Martinez refinery to become a renewable fuels manufacturing and terminal facility. The Martinez facility is expected to be able to produce about 730 million gallons of renewable fuels annually.

On top of a constraint on supply, as the covid-19 pandemic waned, demand was starting to return as the refined product market tightened rapidly in early 2022. With insufficient capacity to service this rapidly increasing demand, this led to a very tight market for refiners like Marathon Petroleum.

To make things worse, as a result of the invasion of Ukraine, it led to skyrocketing natural gas prices in Europe. This led to higher breakeven from European refineries and lower hydrocracker runs, taking out diesel supply. Diesel supply was further reduced from the self-sanctioning of Russian refined product that took out further diesel supply. Last but not least, the higher natural gas prices in Europe led to a preference for light sweet crude due to the higher costs of desulfurization, resulting in more sour barrels in the market.

All these factors added together led to record crack spreads in 2022 as well as high heavy and medium sour differentials in 2022. Apart from these, capture rates were also enhanced by higher cracks. With a solid crack spread, crude differential and capture environment, refiners like Marathon Petroleum had a solid 2022 with a record earning year.

Sale of Speedway and shareholder return

In 2021, Marathon Petroleum announced the sale of Speedway to 7-Eleven for $21 billion.

The sale was significant in multiple ways.

The first was that the sale of Speedway helps to improve the competitive position of Marathon Petroleum's portfolio and to focus its efforts on core activities and be disciplined on operating costs.

The second is that the sale of Speedway helps to strengthen Marathon Petroleum's balance sheet and return capital to shareholders.

As a result of the sale, management expects that the cash proceeds can be returned to shareholders.

The company expects that $10 billion of its common stock can be repurchased. It will begin with a cash tender offer of $4 billion or 10% of its market capitalization. The remainder will be executed over the next 12 to 18 months.

Another $2.5 billion of the cash proceeds will be used to reduce long-term structural debt. The rest of the cash proceeds will then be used to reduce debt to help strengthen the balance sheet further to maintain its investment grade profile.

In the third quarter of 2022, the company also announced a 30% increase to its dividend, increasing it to 75 cents per share after completing its $15 billion share buyback.

The dividend level was decided based on the ability to be competitive with the market, ability to continue to grow over time and be sustained across cycles, which leaves me confident that the dividend support for Marathon Petroleum remains strong.

Today, the company has $11 billion of cash on its balance sheet. $10 billion of this can be used for share buybacks as management has previously communicated a minimum $1 billion cash it plans to keep on its balance sheet. Should the $10 billion cash buffer be in excess of free cash flows, the company could use it for more share buybacks.

Martinez progressing well

As stated earlier, Martinez is expected to have a 730 million gallons per year projected capacity, which puts it as one of the largest renewable diesel facilities in the world. With the Martinez focus, Marathon Petroleum is showing that it is positioning its business for the future as sustainability becomes an increasing priority. As a result, it continues to innovate for the future to ensure it remains relevant in a world that prioritizes decarbonization and the net zero transition.

Martinez is almost near Phase 1 startup, with the LA low-carbon project detailed. The commissioning of phase 1 for the conversion of Martinez conversion is in progress, and fresh feed was recently started with finished product expected to go into storage.

The startup phase should be completed by the first quarter of 2023 and this should bring online capacity of 260 million gallons per year.

Phase 2 which is the PTU startup, is scheduled for the second half of 2023 and the capacity will then increase to 730 million gallons per year.

In LA, Marathon Petroleum expects to spend about $150 million in 2023 to start a project to address the upcoming regulations around will NOx in the LA basin . The startup is expected to be aligned with the change in regulations in 2025, and the project is expected to lower operating expenses and future maintenance costs.

Solid execution under the leadership of Mike as CEO

In March 2020, Mike Hennigan was appointed as the CEO of Marathon Petroleum. That was also the beginning of the covid-19 pandemic.

Since then, Marathon Petroleum has been the top performing refiner, as Hennigan has executed well in a volatile environment.

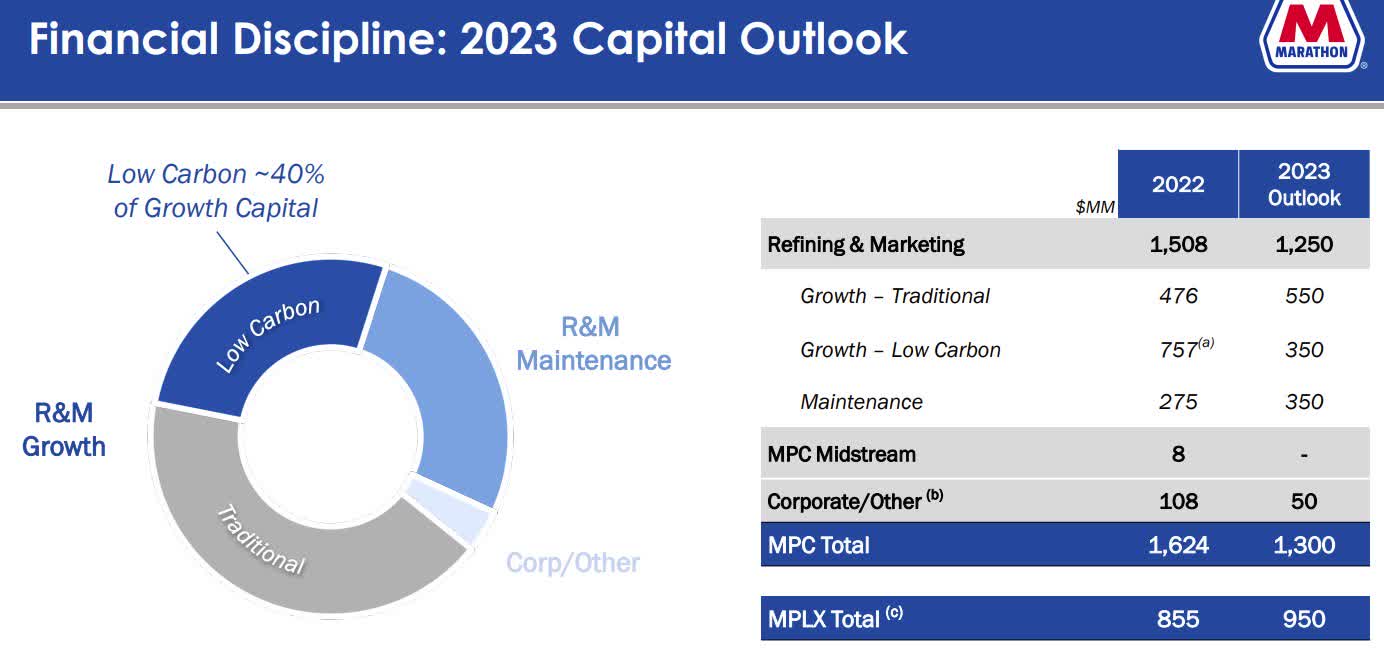

Apart from the well-executed sale of Speedway, Hennigan also led $1 billion in reductions in operating costs and improved discipline in capital expenditures. I like that the company is disciplined in capital spending, making sure it spends about 40% on low carbon investments.

Financial discipline on capex (Marathon Petroleum)

{kind=link}

All in all, this led to Marathon Petroleum having a top tier balance sheet and total return of capital yield.

I am of the opinion that we will see $10 billion in share buybacks each year from 2023, resulting in return on capital yields of 20% to 25%. This is the best in its peer group and outperforming the next best returning refiner.

While there could be a refining downturn in the near-term, I think that the fact that the company is executing well and has huge capital return potential is a reason to hold the course on Marathon Petroleum.

Valuation

Marathon Petroleum is trading at 12% 2024F free cash flow ("FCF") to EV yield or 8x 2024F EV/FCF.

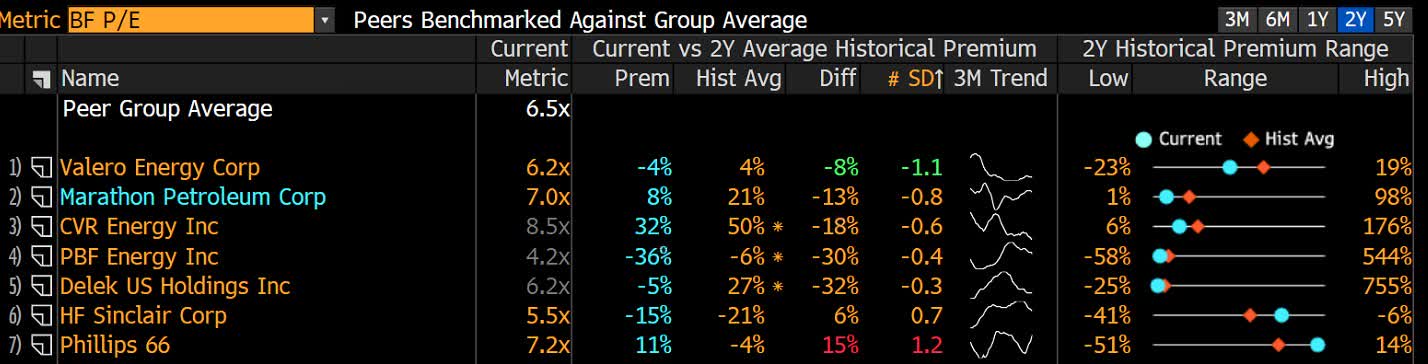

Based on a P/E perspective, Marathon Petroleum is currently trading at a slight premium to its peer group average. That said, I do think that is reasonable given its excellent execution and capital return thus far since the start of the covid-19 pandemic.

Peer group valuation analysis (Bloomberg)

{kind=link}

My 1-year price target for Marathon Petroleum is $151, based on a 12.5x 2024F EV/FCF or 8% FCF to EV yield. This is in line with the peers' 2024F peer average, and conservative given that Marathon Petroleum should be trading at a premium given a strong track record in execution and capital return.

Risks

Refining downturn

While 2022 was one of the best years for refiners, the industry landscape is changing as the macro backdrop seems uncertain and weak. If demand for refining decreases and the market becomes less tight, we could see a deteriorating operating environment for Marathon Petroleum.

Higher refining cost structure

In a weaker market and less tight market, we could see refining costs increase and fundamentals deteriorate. If the refining costs increase, this will affect the free cash flow of Marathon Petroleum and thus the extent to which it is able to return capital.

Conclusion

I am impressed with Marathon Petroleum after the research into the company. While mindful of a potential refining downturn in the near term, I do see a strong company, fundamentally, in Marathon Petroleum.

With the strong leadership of Mike as CEO, the company has got a top tier balance sheet and best-in-class total return of capital yield. With an expectation that the company could buyback $10 billion in shares each year from 2023, this implied return on capital yields of 20% to 25%. This return profile is the best in its peer group and outperforming the next best returning refiner.

I like that Marathon Petroleum Corporation is executing well, not just on its sale of Speedway, but also on its capital discipline and operating cost reductions. In addition, we are seeing the company innovate for the future and investing in newer sustainable businesses like renewable diesel. 40% of its capital expenditures are spent on low carbon opportunities, which will drive the business going forward. As a result, I recommend holding the course for Marathon Petroleum, as it will likely be an outperformer in the years to come within the refining space.

My 1-year price target for Marathon Petroleum Corporation is $151, based on a 12.5x 2024F EV/FCF or 8% FCF to EV yield. This is in line with the peers 2024F peer average, and conservative given that Marathon Petroleum should be trading at a premium given a strong track record in execution and capital return.

For further details see:

Marathon Petroleum: Buy On Upside After 590% Return Since Covid Low