MPC - Marathon Petroleum: Downturn On The Horizon With Banks Collapsing

2023-03-21 17:28:24 ET

Summary

- Marathon Petroleum benefitted immensely during 2022 as the global energy shortage sent margins surging to never-before-seen levels.

- Going forwards into 2023, this could change dramatically with the recent weeks seeing red flags for a downturn on the horizon.

- As everyone knows, the banking sector is facing a crisis with multiple banks collapsing.

- This likely foretells weaker economic conditions and thus there is a very real possibility of a downturn in the refining industry.

- Since MPC is trading near-record highs, I believe that a sell rating is appropriate as they are vulnerable to a large and painful sell-off.

Introduction

The refining industry leader, Marathon Petroleum ( MPC ) benefitted immensely during 2022 as the global energy shortage sent margins surging to never-before-seen levels. Despite this very strong base heading into 2023 that helped build their present near-record share price, recent weeks have seen a wave of red flags for a downturn on the horizon with banks collapsing.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

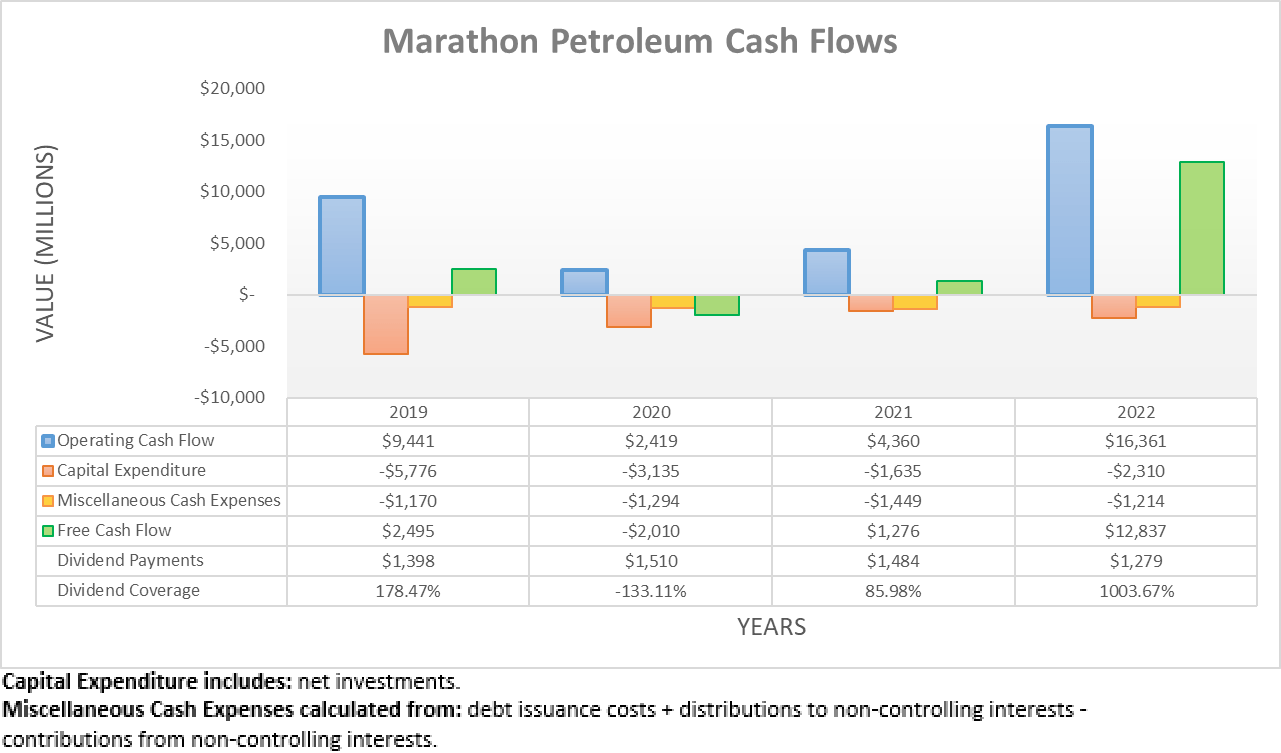

Following a sluggish recovery during 2021 that saw a mixture of both strong and weak quarters, the Russia-Ukraine war and resulting global energy shortage gave the company a massive cash windfall during 2022. As a result, their operating cash flow ended the year at a once-unthinkable $16.361b that is almost four times higher year-on-year versus their previous result of $4.36b during 2021. To little surprise, their modest capital expenditure saw the majority translated into free cash flow, thereby amounting to a massive $12.837b during 2022.

{kind=link}

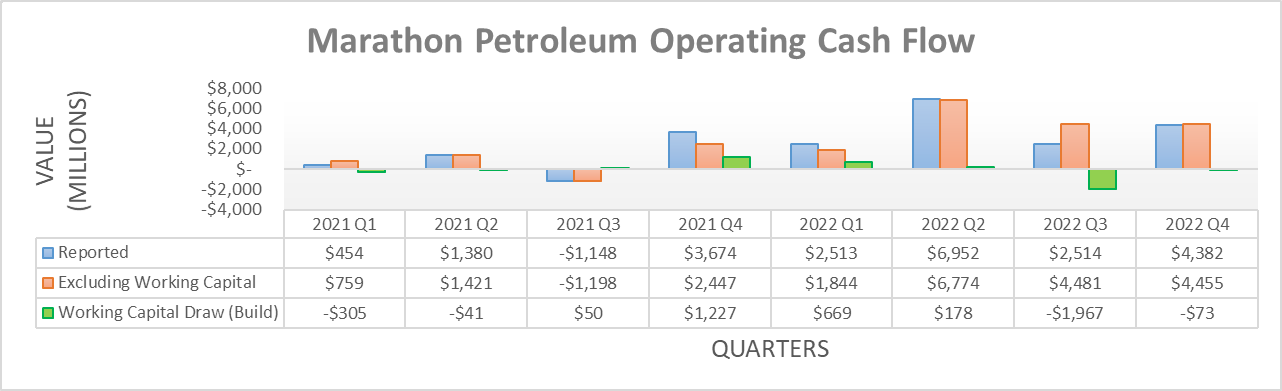

When viewing their operating cash flow on a quarterly basis, the second quarter of 2022 directly following the Russian invasion of Ukraine saw a massive reported result of $6.952b that by itself is almost an annual result during more routine years. Even though operating conditions subsequently eased during the third and fourth quarters, they still continued to post very strong results with the latter in particular seeing a result of $4.382b. Whilst interesting, the far more important topic right now is their outlook going forward into 2023, especially in light of red flags for a downturn that are seemingly growing in number by the day with banks collapsing.

In part due to the booming energy prices of 2022, once subdued inflation came roaring back to life and proved hotter and more persistent than originally hoped and in turn, the Federal Reserve had no choice but to rapidly tighten monetary policy in a highly indebted economy. Naturally, hopes then switched over to a soft landing, whereby inflation cools without causing too much damage to the economy. Alas, it seems the probability of this happening is looking increasingly unlikely each day with the last two weeks seeing concerns over the stability of the banking sector take center attention and arguably even develop into a crisis.

Even though risks were building for months, it seems the watershed moment was the failure of the Silicon Valley Bank ( SIVB ) who suffered a dramatic fall from grace. Unfortunately, this started rippling across the banking sector and exposing weaknesses elsewhere, such as the beleaguered First Republic Bank ( FRC ) that saw its credit rating cut to junk last week with a further downgrade likely forthcoming in the next few days as concerns remain over their solvency.

Even more concerning than these smaller regional banks is the large international player, Credit Suisse ( CS ) that saw its long-running troubles begin spiraling, despite the Swiss National Bank injecting more than $50b of liquidity to help fend off a bank run. As of the time of writing, it appears they will be taken over by UBS ( UBS ) to avert this crisis from turning into a full-blown catastrophe. Whether this works remains to be proven but even if so, it still does not resolve the severe issues faced by other banks nor guarantee there will not be a repeat elsewhere in the banking sector in future months.

In a matter of weeks, this saw future interest rate expectations drop with more economists now expecting the Federal Reserve could slow or even pause interest rate hikes much sooner than was previously envisioned as recently as the beginning of March. On the surface, the prospects of looser monetary policy may sound positive but in this situation, this would stem from weaker economic conditions and possibly a recession, which is anything but helpful for most companies.

Most recently as of the time of writing, the major central banks are ‘ taking coordinated action ’ to shore up liquidity within capital markets, which is another ominous red flag for economic conditions across the world. This is a complex situation and the main point of this article is not to assess the nuts and bolts of the banking sector but rather, to assess the implications for the refining industry and thus by extension, Marathon Petroleum who quite oddly sees a near-record share price as of the time of writing.

Whilst yes, they are obviously not a bank themselves nor should they require extensive access to capital markets during 2023 as subsequently discussed but unfortunately, the economy as a whole does not have this luxury. Sadly, this banking crisis presents red flags that weaker economic conditions and possibly even a severe recession are on the horizon. Since the refining industry is reliant upon strong economic conditions to underpin fuel demand, this foretells the very real possibility of a downturn that would see a change of fortunes.

The extent of any downturn remains impossible to quantify but a banking crisis is never a good leading indicator for the year ahead. In fact, this is actually a very scary situation that could spread rapidly and if not brought under control quickly, it could lead to a severe downturn such as back during the global financial crisis of 2008-2009. Even if not this severe, every passing day is nevertheless seemingly making even a modest downturn ever more likely, which almost certainly would see refining margins plunge along with their financial performance.

A downturn would be less concerning for shareholders if their share price had already suffered heavy losses and thus reflected this concerning outlook. Although as of the time of writing, it remains at near-record highs and thus, it seems the market is pricing a reasonably bullish outlook despite these red flags.

In turn, I suspect that shareholders are vulnerable to a large and painful sell-off in the coming year ahead, if not even as soon as in the coming weeks. The downside risks are amplified by their subsequently discussed lack of deleveraging as well as their low dividend yield of circa 2.50%, which does not provide a desirable source of income absent of accompanying capital gains.

{kind=link}

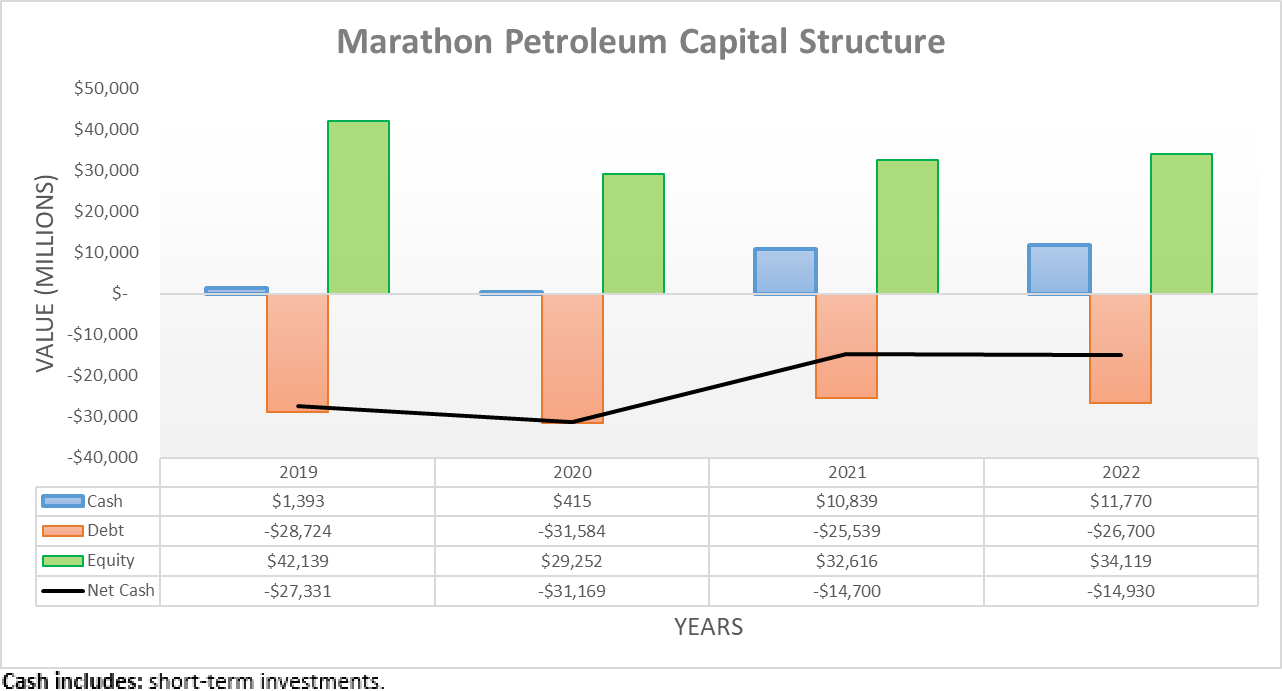

Despite reaping a massive cash windfall during 2022, interestingly their net debt was essentially unchanged versus the end of 2021. In fact, at the end of 2022 its level of $14.93b was ever-so-slightly higher than its previous level of $14.7b at the end of 2021. The reason pertains to their shareholder returns because apart from their relatively modest dividend payments of $1.279b during 2022, they also conducted share buybacks totaling a staggering $11.922b.

Going forwards into 2023, it is difficult to ascertain the extent their net debt will change but given their actions during 2022, it seems unlikely to decrease, regardless of whether the aforementioned red flags actually materialize into a downturn. Whilst this leaves their cash inflows impossible to predict with accuracy, thankfully their capital expenditure during 2023 is forecast to be lower year-on-year versus 2022, thereby limiting their cash outflows and in turn, helping mitigate damage in a bad scenario.

It also stands to reason that any downturn would see their share buybacks cease or if not, they would at least wind back dramatically versus their staggering pace during 2023. This would limit their cash outflows and thus also help keep their net debt under control but at the same time, it would expose shareholders to even greater downside risk in the short-term. Not only would their shares lose buying support from new investors as their appeal fades from a downturn but additionally, they would also lose this sizeable buying support from their share buybacks.

{kind=link}

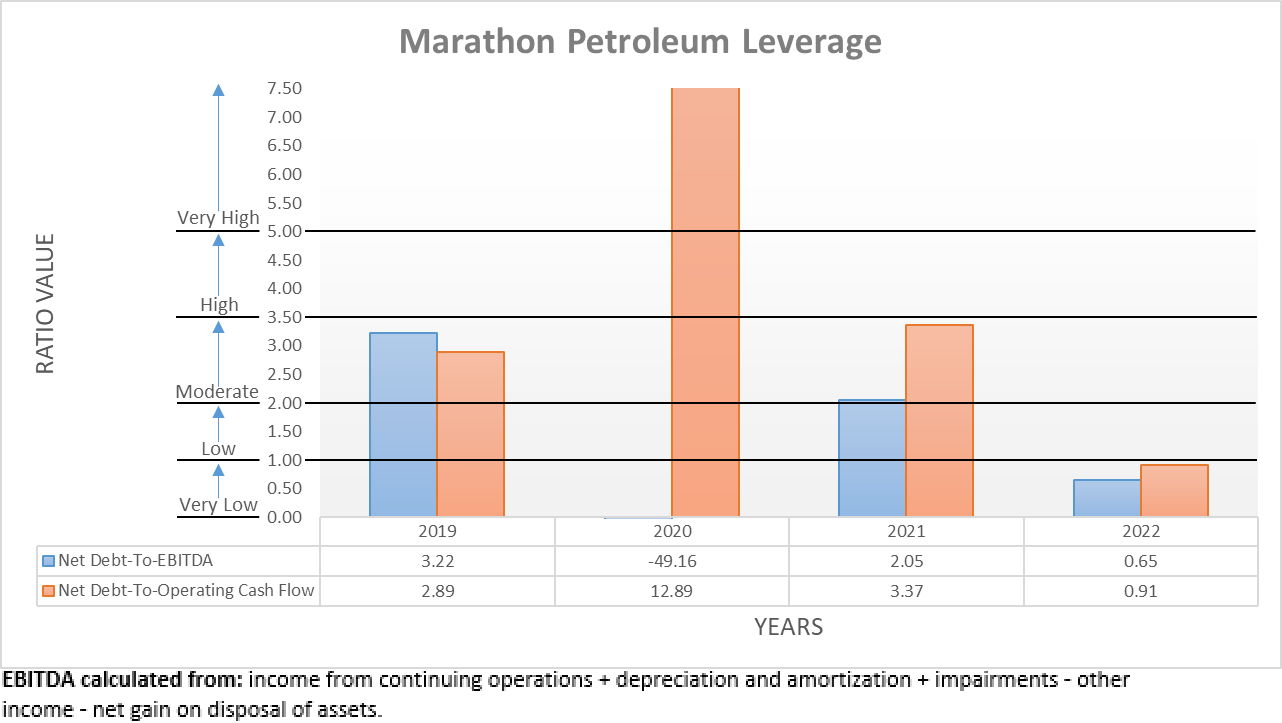

Even though their net debt remained essentially unchanged during 2022, their booming financial performance still ensured their leverage plummeted. As a result, their net debt-to-EBITDA is now 0.65 versus its previous result of 2.05 at the end of 2021, whilst their net debt-to-operating cash flow also followed with results of 0.91 and 3.37 across these same two points in time, respectively. Whilst both of their results are now beneath the threshold of 1.00 for the very low territory, the more important consideration is not necessarily their leverage right now but rather, what would happen if they see a downturn.

Due to their lack of deleveraging during 2022, weaker financial performance would have a sizeable influence on their leverage. The extent would depend on the severity of the downturn but even looking back at 2021, which saw a mixture of both strong and weak quarters, their net debt-to-operating cash flow of 3.37 would already see their leverage near the threshold of 3.51 for the high territory. Whilst not necessarily bad, it is also certainly not good and therefore, as they have not transformed nor even improved their capital structure during 2022, there is no selling point here to mitigate a downturn and thus by extension, help justify their near-record share price in the face of a downturn.

{kind=link}

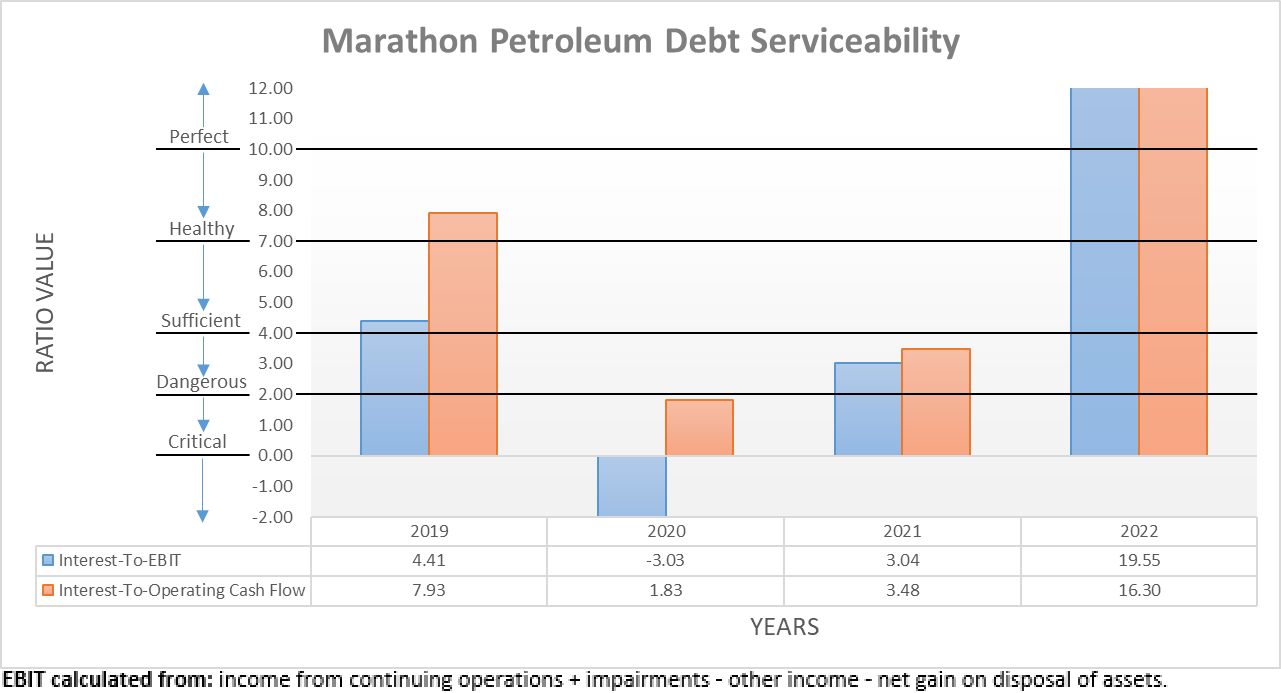

To little surprise, their booming financial performance also helped their debt serviceability during 2022, despite their net debt remaining essentially unchanged. To this point, their interest coverage is now perfect with results of 19.55 and 16.30 when compared against their respective EBIT and operating cash flow, which are far above their previous respective results of 3.04 and 3.48 at the end of 2021. Similar to their leverage, this marks a massive improvement but at the same time, it also once again highlights weaker financial performance would have a sizeable influence due to their lack of deleveraging and thus by extension, it once again does not provide any improvement to help justify their near-record share price.

{kind=link}

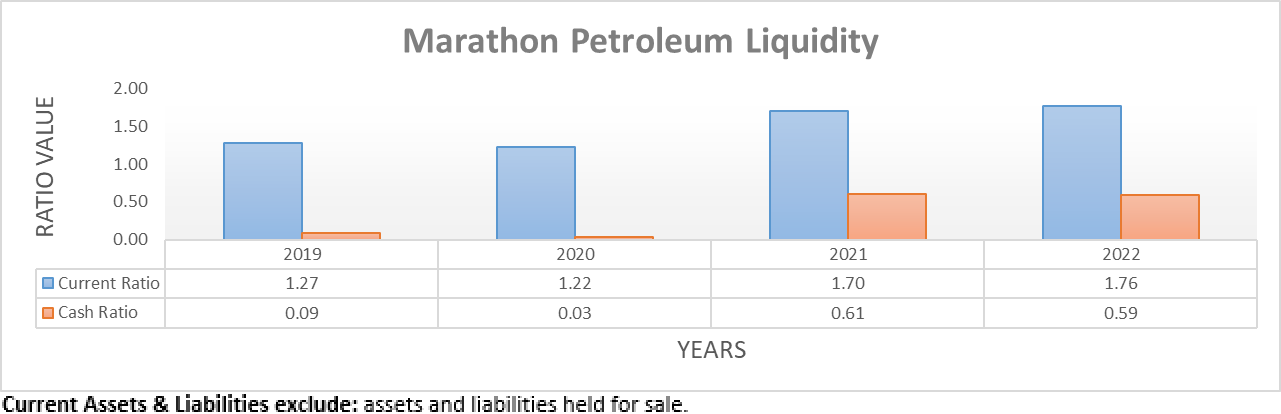

When it comes to their liquidity, it remains strong following 2022 as they retained their massive $11.77b cash balance that facilitates their current and cash ratios having respective results of 1.76 and 0.59, which are essentially unchanged versus their previous respective results of 1.70 and 0.61 at the end of 2021. Even if they face a downturn during 2023 as the aforementioned red flags indicate is likely forthcoming, this largely removes their need to access capital markets and thus, it would serve them very well by ensuring they can navigate any upcoming turbulence, regardless of where monetary policy heads.

Conclusion

To the best of my knowledge, there was never a recession whereby the refining industry actually benefitted relative to the prior year and thus, it is concerning to see a wave of red flags with banks collapsing. That said, I am certainly not saying that a return to the dark days of 2020 are coming as these were due to Covid-19 lockdowns. More so, I am saying that it is very difficult to imagine MPC's strong refining margins persisting throughout weaker economic conditions and therefore, I believe that a sell rating is appropriate given their near-record share price that leaves virtually no margin of safety to account for even a mild downturn, let alone what could transpire if more banks continue collapsing. Further supporting this rating is their lack of deleveraging during 2022 and their low circa 2.50% dividend yield, which does not offer much appeal unless accompanied by further capital gains on their share price.

Notes: Unless specified otherwise, all figures in this article were taken from Marathon Petroleum’s SEC Filings , all calculated figures were performed by the author.

For further details see:

Marathon Petroleum: Downturn On The Horizon With Banks Collapsing