MPC - Marathon Petroleum: Gasoline Crack Spread Plunges 2024 Earnings Outlook In Question

2023-10-19 13:50:45 ET

Summary

- Retail gas prices have fallen to near $3.50 per gallon, impacting profitability for energy refiners as crack spreads have retreated.

- Marathon Petroleum Corporation has strong momentum and a fair valuation, but macro risks are a concern.

- MPC's earnings beat expectations in Q2 2023, driven by strong throughput volumes and contributions from MPLX.

- I outline key price levels to watch ahead of Q3 earnings due out on Halloween.

It’s “pleasure at the pump” these days. The average retail price for a gallon of regular unleaded has fallen to near $3.50. Many states, away from the West Coast, are closer to the $3 mark. This is not the best news for refiners as the retail gas price slide comes along with falling gasoline crack spreads – a key profitability indicator among energy refiners.

According to Reuters: "Gasoline inventories are up 7.7% from the same period last year, but the four-week average of U.S. gasoline demand is down 6%, according to the U.S. Energy Information Administration. As a result, profit margins to produce gasoline from crude oil, known as the gasoline crack, have dropped by 83% since August to as low as $7.04 a barrel this month, according to LSEG data."

I have a hold rating on Marathon Petroleum Corporation (MPC). The stock has tremendous momentum right now and has been among 2023’s biggest winners. The valuation using normalized earnings now looks fair, in my view, and macro risks are a concern.

Gasoline Crack Spread Dips in September and Early October

@Oilcfd

Marathon Petroleum Corporation is a leading, integrated, downstream energy company. The company operates the nation's largest refining system. MPC's marketing system includes branded locations across the US, including Marathon brand retail outlets. Marathon also owns the general partner and majority limited partner interest in MPLX LP, a midstream company that owns and operates gathering, processing, and fractionation assets, as well as crude oil and light product transportation and logistics infrastructure, according to the company website.

The Ohio-based $62 billion market cap Oil and Gas Refining and Marketing industry company within the Energy sector trades at a low 5.5 trailing 12-month GAAP price-to-earnings ratio and pays a near-market 2.0% forward dividend yield. Ahead of earnings due out on Halloween, shares trade with a moderate implied volatility percentage of 33%, while short interest on the stock is low at just 2.7% as of October 18, 2023.

Back in August, Marathon reported a very strong second quarter. Per-share profits verified at $5.32, topping analysts’ estimates of just $4.58. Revenue of $36.8 billion was also better than expected , though the figure was down 32% on a year-on-year basis. It is important to remember that Q2 of 2022, the comparable quarter, was unusually strong due to Russia’s invasion of Ukraine and the resulting spike in energy prices.

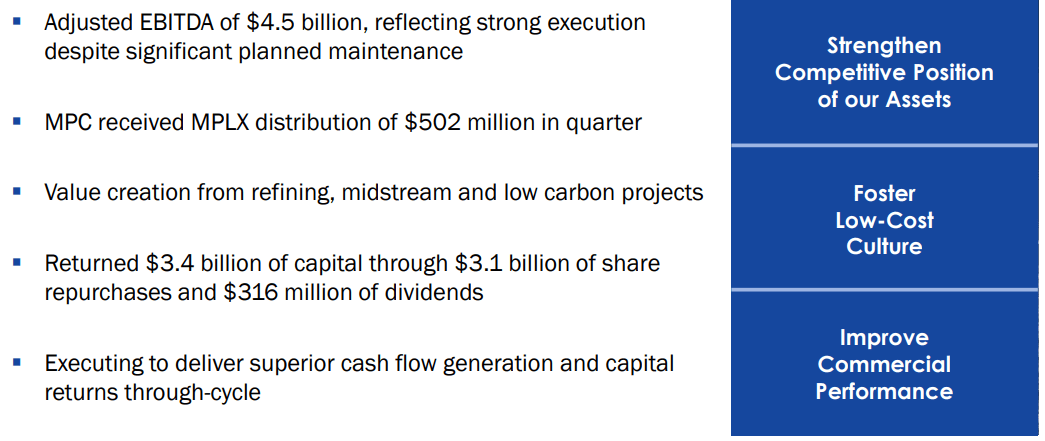

Investors continue to enjoy a rising, though modest, dividend while MPC’s management team remains committed to repurchasing shares ($3.4 billion of capital was returned to shareholders in the quarter, with $3.1 billion coming via buybacks). Overall, strong throughput volumes, contributions from MPLX, and reduced expenses drove the big EPS beat and robust free cash flow in the quarter. Amid outages at the Galveston Bay Refinery, execution was strong, and a dip in crack spreads lately is the primary risk heading into the next earnings report.

Bullish, however, is that margins could improve as turnaround expenses dip and as unplanned outages end. Other risks include weaker gasoline demand should a macro slowdown take place or if ongoing geopolitical tensions keep oil prices elevated relative to gasoline, which would pressure margins. Operational and capital expenditures as well as higher taxes are also threats to profitability.

Q2 2023 Earnings Summary & Business Outlook

{kind=link}

On valuation , analysts expect full-year EPS near $23 as crack spreads had been running at very high levels earlier this year. Normalized per-share profits must be used when determining the fair value of shares. As such, EPS is seen as falling to under $16 next year, with further earnings drops by 2025. Still, there have been a slew of profit upgrades on the stock in the last few months, while MPC’s trailing and forward earnings multiples appear low.

Income investors won’t be particularly attracted to MPC, though the firm raised its dividend from $2.32 on an annualized basis to $2.49 last year. There is also ample free cash flow over the last four quarters given the favorable operating environment – total FCF per share is a whopping $27.78 - a more than 18% FCF yield.

Marathon Petroleum: Earnings, Valuation, and Earnings Revisions

Seeking Alpha

If we assume normalized EPS of $13 and apply a low teens multiple, then we arrive at a stock price near $160. While many of the valuation gauges appear very compelling, sales growth is expected to be negative on a year-on-year basis over the coming quarters.

MPC: Compelling Valuation Metrics, but Growth Outlook Soft

Seeking Alpha

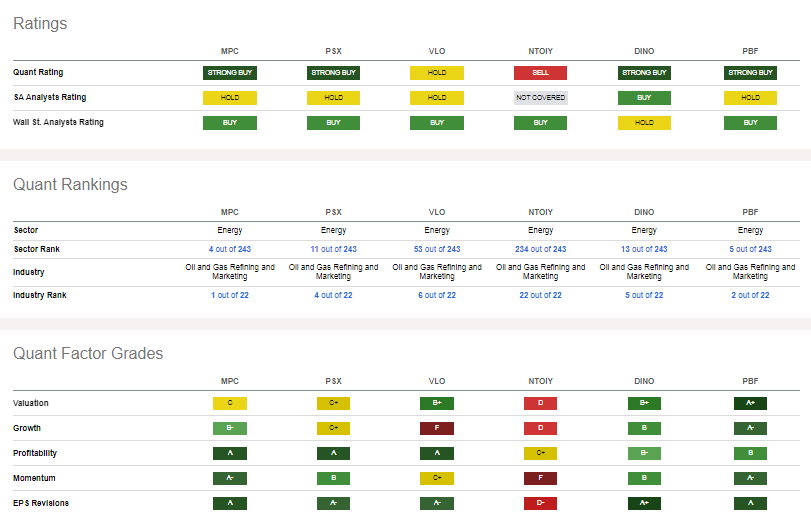

Compared to its peers , MPC features a lukewarm valuation score, while its growth outlook is somewhat favorable. I take a different stance on that – the valuation is decent to me, but both top-line and bottom-line growth are not favorable today given volatility and normalization in the industry. Still, MPC is highly profitable and extremely free cash flow generative, with strong share-price momentum . Moreover, analysts have been turning more bullish on Marathon’s earnings outlook. The company has topped consensus EPS estimates in each of the previous 12 quarters.

Competitor Analysis

{kind=link}

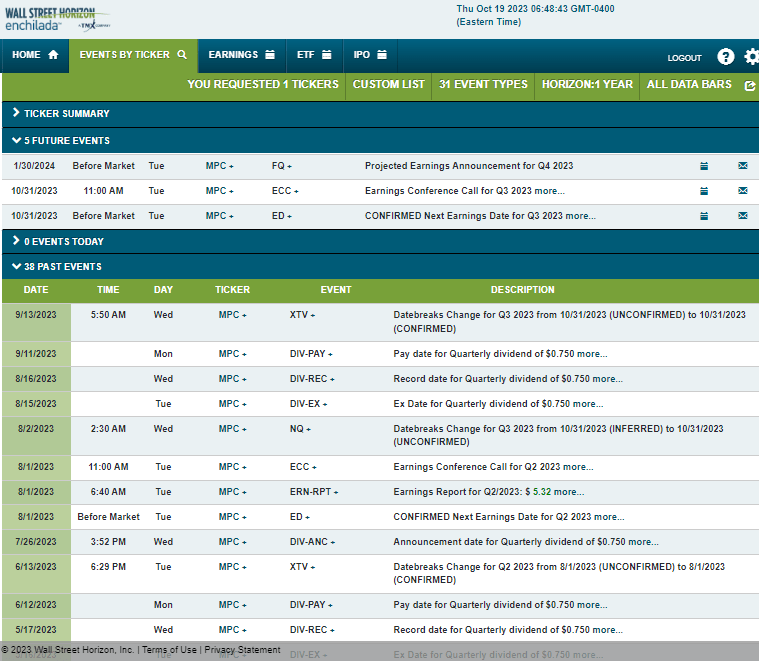

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q3 2023 earnings date of Tuesday, October 31 BMO with a conference call later that morning. You can listen live here . No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

{kind=link}

The Technical Take

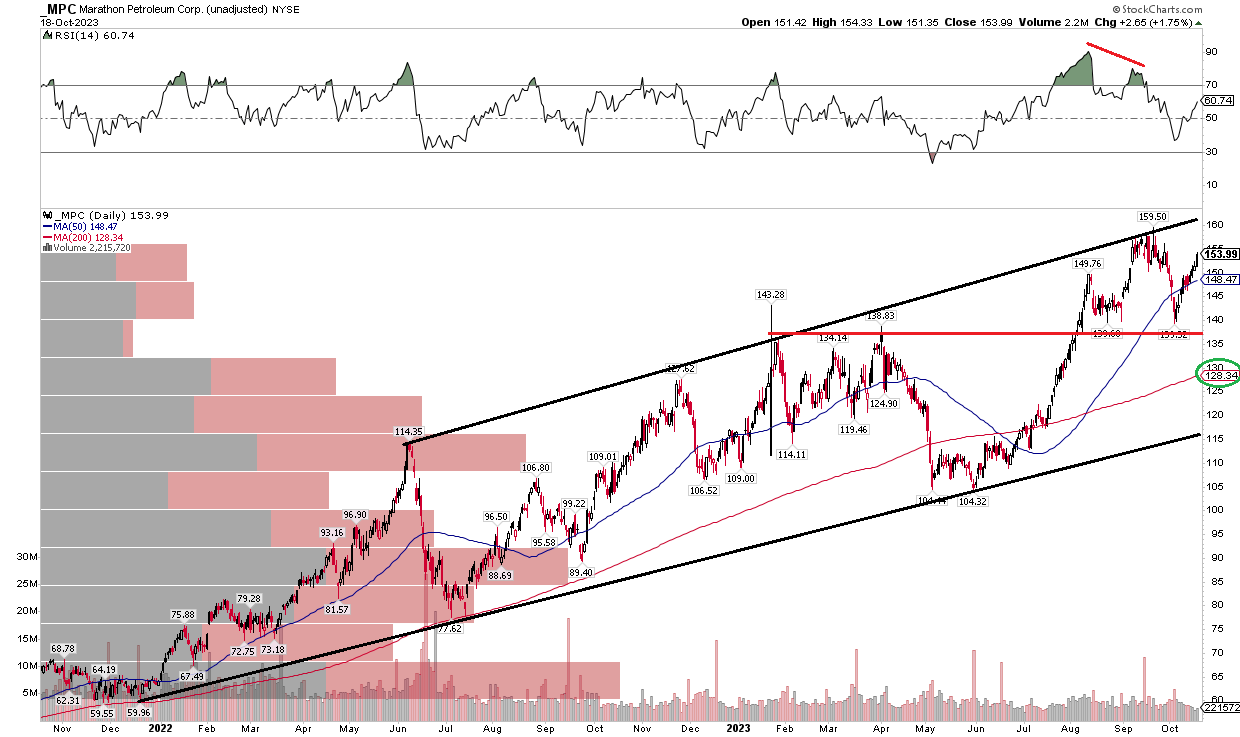

With the stock near fair value and the company potentially near a peak in the earnings cycle, the technical situation appears strong at first blush. Notice in the graph below that MPC has traded in a steady uptrend channel for more than two years. The bulls took profits on a recent approach to the upper end of the channel, but I also see key support in the $138 to $140 zone. This was an area that was met with selling pressure during the first half of 2023, but ‘old resistance becomes new support’ proved right as the bulls took MPC to new highs in August. $139 was then defended late in Q3 and just recently.

Also take a look at the RSI momentum indicator at the top of the chart – there was bearish RSI divergence when the stock notched a new all-time high in September. So, there are some cracks in the trends, so to speak. Still, with an upwardly sloped long-term 200-day moving average, the bulls appear in control. Long here with a stop under $135 may make sense. Below that, significant support is in the $104 to $114 zone.

Overall, the chart is constructive, with the bearish RSI divergence being the primary blemish. One last chart - the seasonal trend on MPC is strong right now, so that's something to consider as year-end approaches. The stock has on average rallied through early February, according to seasonal data from Equity Clock .

MPC: Solid Uptrend, Monitoring Bearish RSI Divergence

{kind=link}

Strong Late-Year Seasonal Trends

Equity Clock

The Bottom Line

I have a hold rating on MPC. I like the technical situation and its high profitability, but the valuation appears about right given the strong share-price run-up in the last two years. With a dip in crack spreads lately and earnings perhaps near a peak for the cycle, downside risks are rising.

For further details see:

Marathon Petroleum: Gasoline Crack Spread Plunges, 2024 Earnings Outlook In Question