MPLX - Marathon Petroleum: Great Performance But Will It Last?

Summary

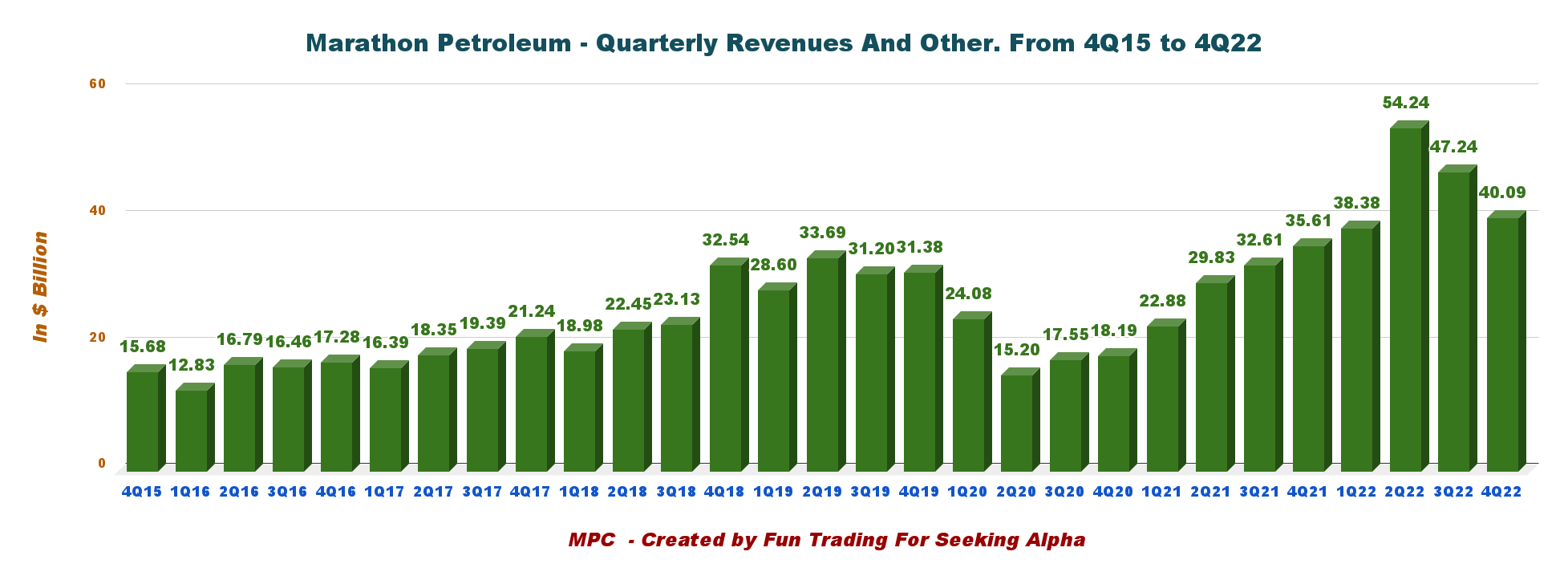

- Marathon Petroleum reported a total income of $40.093 billion in the fourth quarter of 2022, up 12.6% from the same quarter a year ago and down 2.1% sequentially.

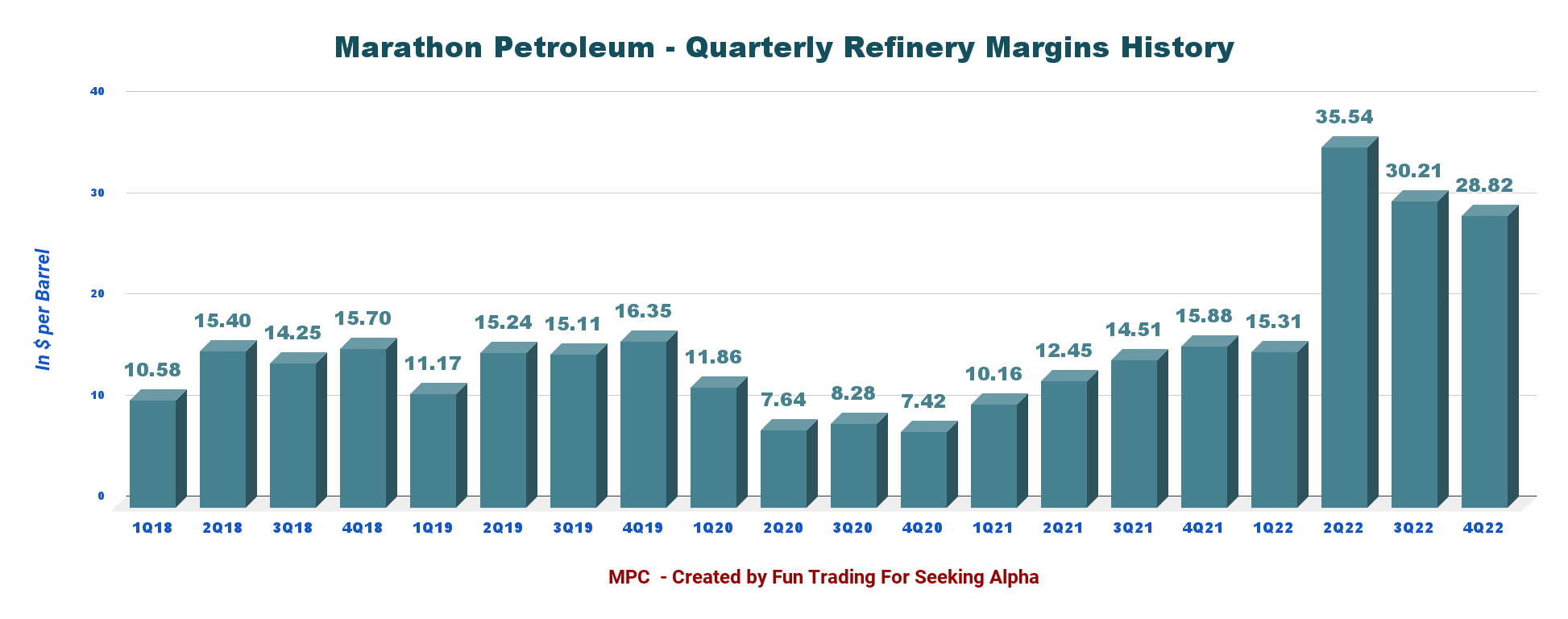

- Marathon Petroleum declared a global R&M margin of $28.82 per Bbl based on throughput per region. Margins are still well above average this quarter, despite dropping from 3Q22.

- I recommend buying MPC between $118.2 and $112.5 to accumulate again, with potential lower support at $108, which is close to the 200MA.

Introduction

The independent US refiner and marketer, Ohio-based Marathon Petroleum (MPC), released its fourth-quarter and FY22 results on January 31, 2023.

Note: I have followed MPC quarterly since 2018. This new article is a quarterly update of my article published on November 24, 2022.

4Q22 and FY22 results snapshot

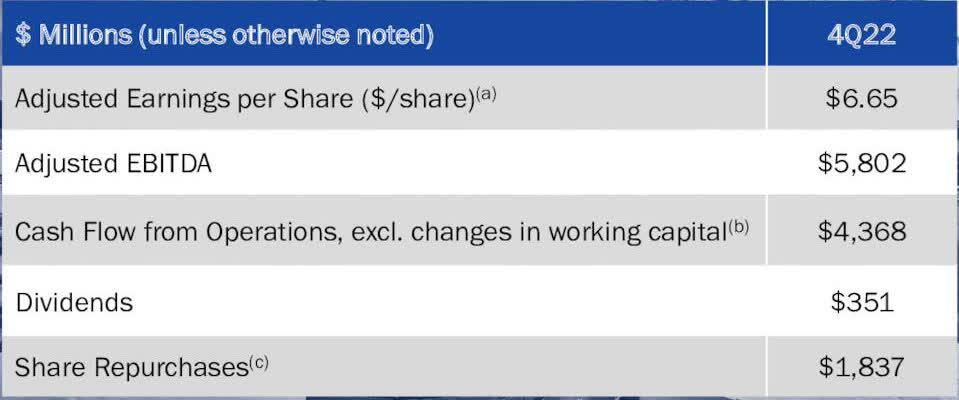

Marathon Petroleum reported a better-than-expected adjusted income of $6.65 per share for the fourth quarter compared with $1.30 last year.

Net income was $3,321 million, compared to $774 million in 4Q21. Revenues increased significantly from $35.61 billion last year to $40.09 billion.

MPC 4Q22 highlights (MPC Presentation)

{kind=link}

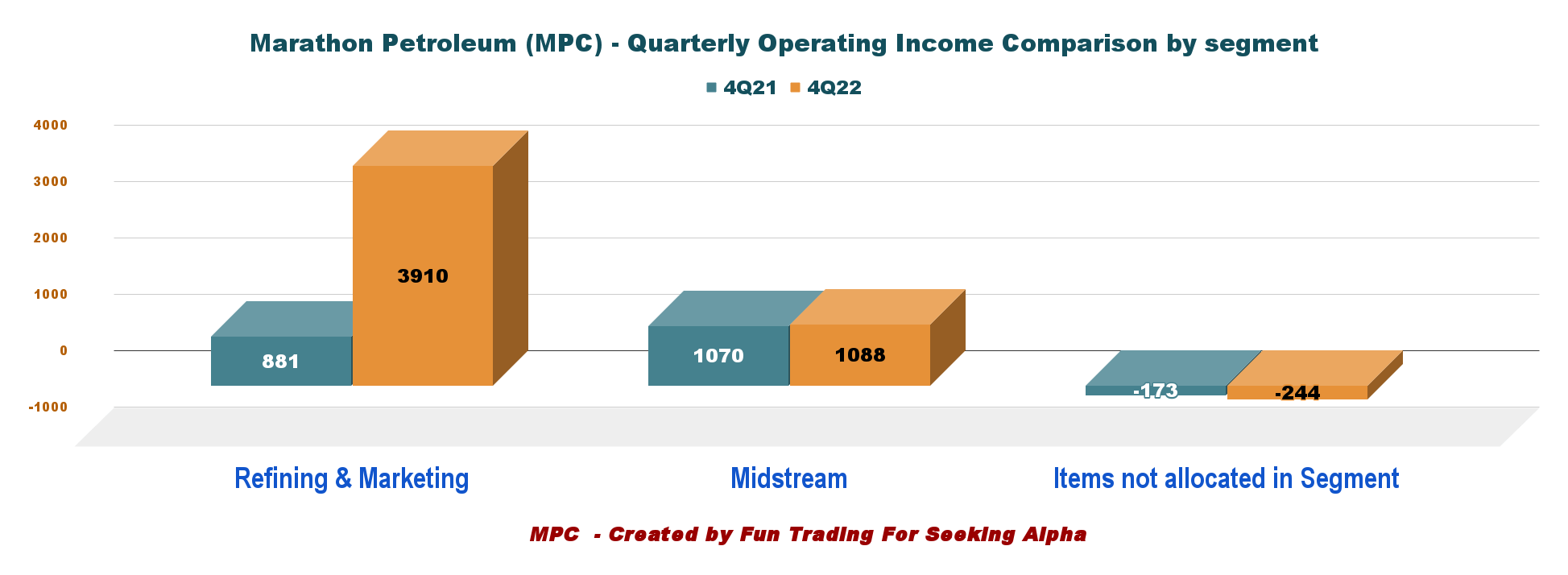

The company's results were boosted by the stronger-than-expected performance of its main Refining & Marketing segment, with income totaling $3,910 million (please see the chart below).

MPC Quarterly Operating income 4Q21 versus 4Q22 (Fun Trading)

{kind=link}

Stock performance

Marathon Petroleum has outperformed Phillips 66 (PSX), Valero Energy (VLO) and VanEck Oil Refiners ETF (CRAK), and is up a whopping 56% on a one-year basis. VLO is a close second, but PSX and CRAK lag well behind.

Investment thesis

As expected, Marathon Petroleum has performed exceptionally well over the past few months. It continues to be the leader of the refiners' group, closely followed by Valero Energy, which is my first choice in this industry.

Marathon Petroleum also owns a majority stake (64.6%) in a midstream partnership called MPLX LP (MPLX). Most of Marathon's midstream segment is handled by MPLX LP. Therefore, the Refining & Marketing, or R&M, segment is MPC’s main operational segment. However, MPC has significantly outperformed MPLX on a one-year basis. MPLX LP is paying a dividend yield of 9%.

The company has shown exceptional performance in 2022 and is likely to perform well in 2023, albeit at a lower level. Profit margins went up to the roof, and energy demand is expected to be strong in 2023 and, more specifically, in 2024. However, oil prices are expected to go down in 2023 even if oil demand is strong now after China decided to restart its economy.

The US Energy Information Administration expects global consumption of liquid fuels such as gasoline, diesel, and jet fuel, to set new record highs in 2024. According to EIA’s January Short-Term Energy Outlook, global liquid fuel consumption will exceed 100 million barrels per day, on average, in 2023 for the first time since 2019, then average more than 102 million barrels per day in 2024.

However, despite a somewhat rosy 2023-2024 period, the profit margins are expected to decrease significantly from the record in 2022, and MPC may experience higher volatility in 2023. Also, analysts are predicting a recession in the second half of 2023, affecting demand.

Thus, it is prudent to trade LIFO for about 50% of your long-term position in case of a steep retracement if the market gets frightened by an increased risk of a painful recession.

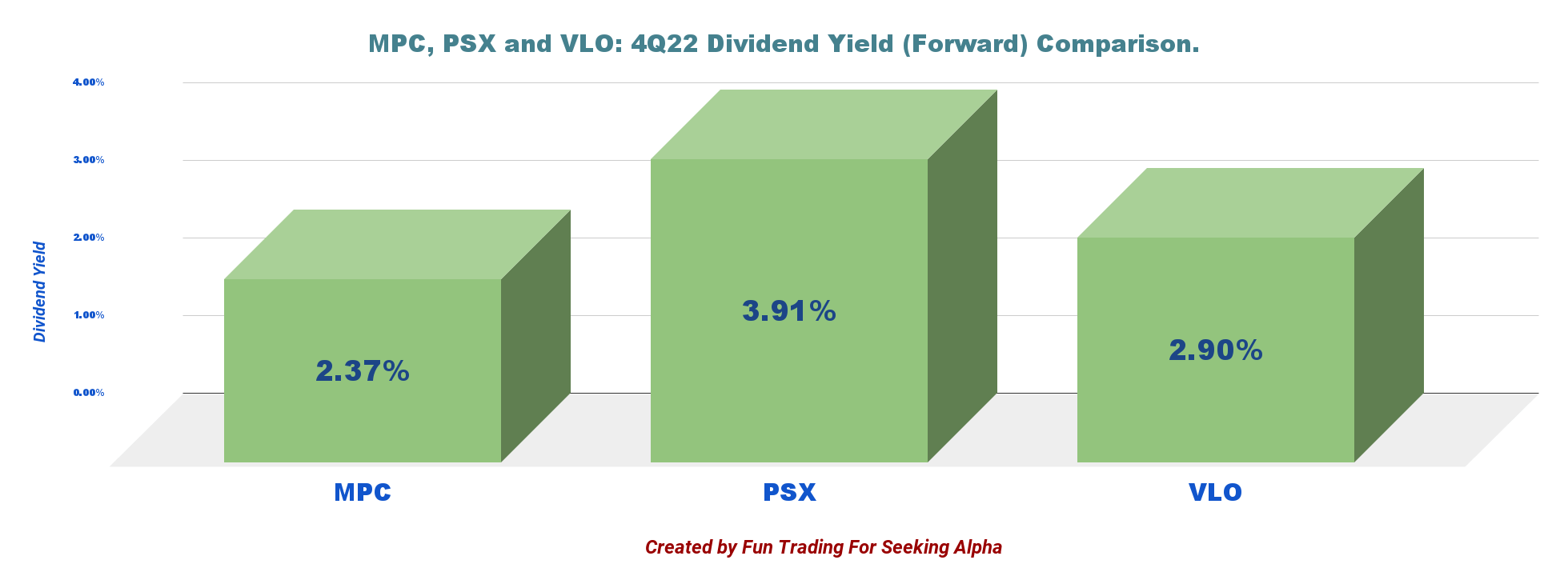

Keeping a long-term holding makes sense from an investor's perspective. MPC pays a dividend yield of 2.37%, which is not negligible but still a little low compared to its peers.

However, the total performance, including stock improvement, is equivalent to Valero Energy and significantly beats Phillips 66.

MPC Dividend comparison: MPC, VLO, PSX (Fun Trading)

{kind=link}

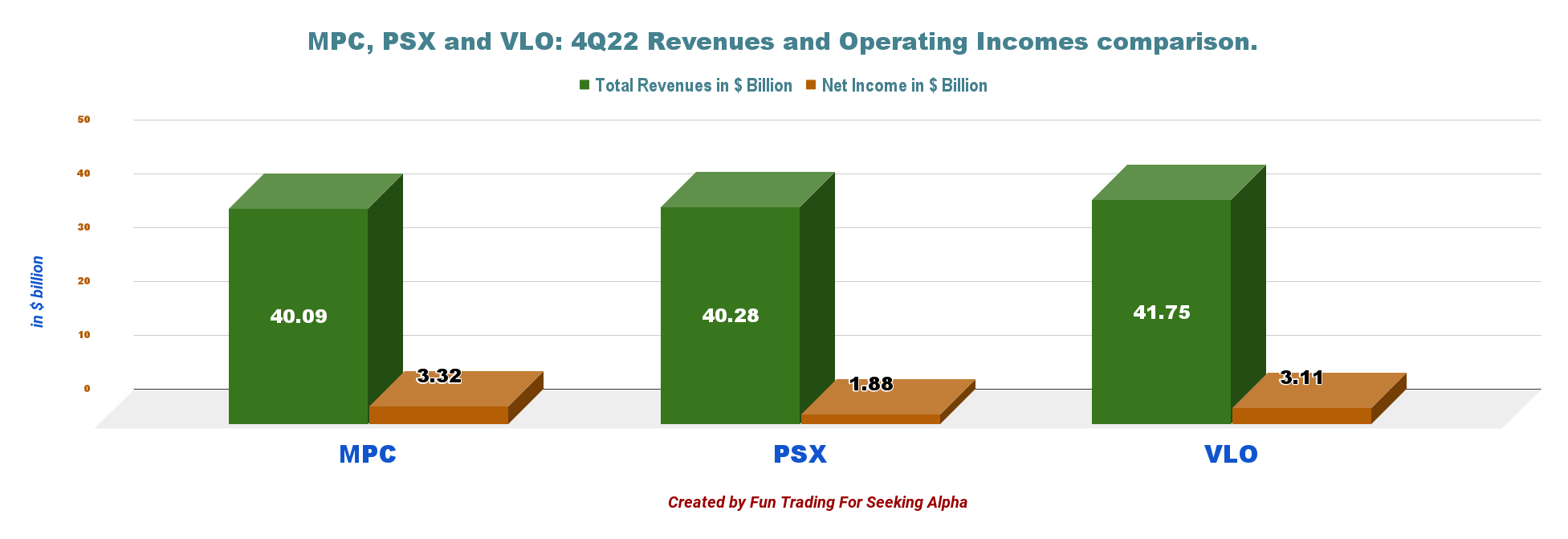

Revenue and net income compared to Valero Energy and Phillips 66 in 4Q22.

MPC Chart comparison Revenue and net income MPC, VLO, PSX (Fun Trading)

{kind=link}

MPC repurchased $1.8 billion of shares in 2022 and added $700 million of shares this year until Jan 27.

The total shares outstanding diluted has been reduced by 22.6% YoY. Marathon also approved an additional $5 billion share repurchase and has a remaining authorization of $7.6 billion.

Margins by Region

Marathon Petroleum declared a global R&M margin of $28.82 per Bbl based on throughput per region. Margins are still well above average this quarter, despite dropping from 3Q22.

Details below:

| Gulf Coast |

| Mid Continent |

| West Coast |

| Total |

| $26.86/per Bbl |

| $29.20/per Bbl |

| $28.63/per Bbl |

| $28.82/ per Bbl |

Marathon Petroleum - Financial History: The Raw Numbers - Ending Fourth Quarter 2022

Note: The 10-K has not been filed yet. Hence, capital expenditure can only be estimated at the moment. Free cash flow and capital expenses will be adjusted when the company files its FY22 10-K.

| Marathon Petroleum |

| 4Q21 |

| 1Q22 |

| 2Q22 |

| 3Q22 |

| 4Q22 |

| Total Revenues in $ Billion |

| 35.34 |

| 38.06 |

| 53.80 |

| 45.79 |

| 39.81 |

| Total Revenues and others in $ Billion |

| 35.61 |

| 38.38 |

| 54.24 |

| 47.24 |

| 40.09 |

| Net Income available to common shareholders in $ Million |

| 774 |

| 845 |

| 5,873 |

| 4,477 |

| 3,321 |

| EBITDA $ Million |

| 2,463 |

| 2,546 |

| 9,134 |

| 7,543 |

| 4,564 |

| EPS diluted in $/share |

| 1.27 |

| 1.49 |

| 10.95 |

| 9.06 |

| 7.09 |

| Operating cash flow in $ Million |

| 3,674 |

| 2,513 |

| 6,952 |

| 2,514 |

| 4,368 |

| CapEx in $ Million |

| 481 |

| 495 |

| 498 |

| 701 |

| 560* |

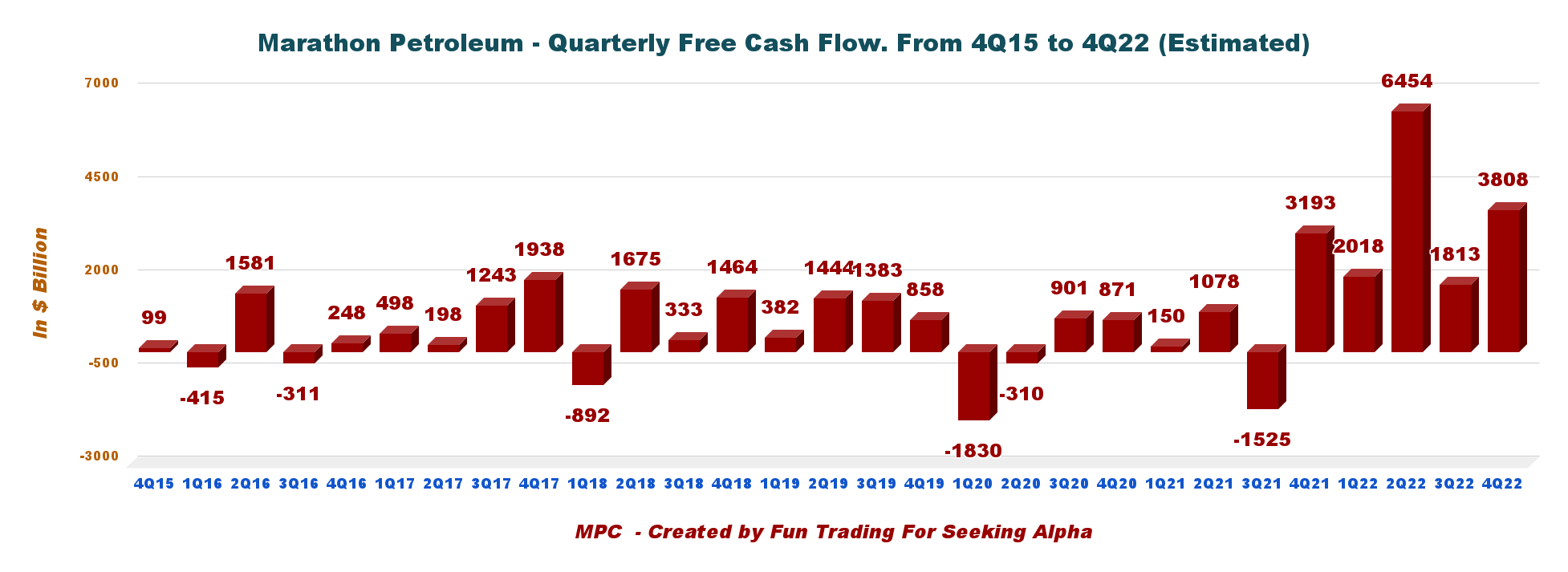

| Free Cash Flow in $ Million |

| 3,193 |

| 2,018 |

| 6,454 |

| 1,813 |

| 3,808* |

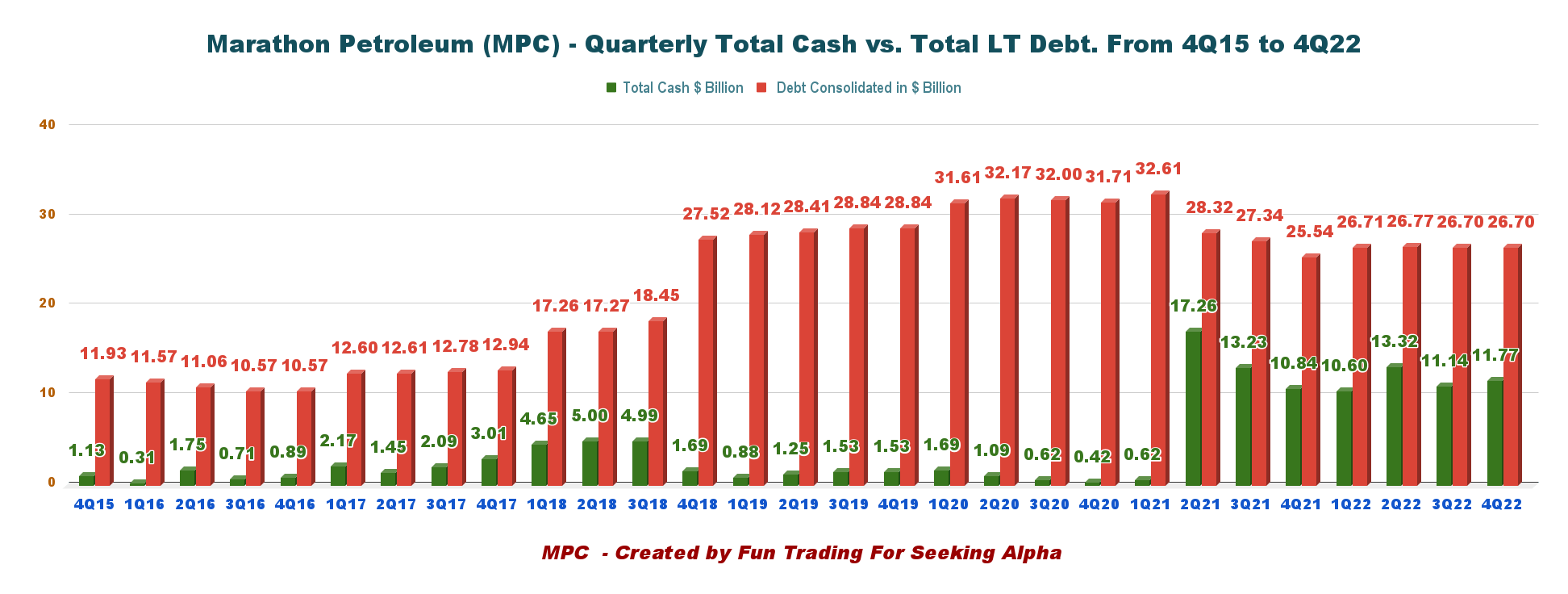

| Total Cash $ Billion |

| 10.84 |

| 10.60 |

| 13.32 |

| 11.14 |

| 11.77 |

| Debt Consolidated in $ Billion |

| 25.54 |

| 26.71 |

| 26.77 |

| 26.70 |

| 26.70 |

| Dividend per share in $ |

| 0.58 |

| 0.58 |

| 0.58 |

| 0.75 |

| 0.75 |

| Shares Outstanding (Diluted) in Million |

| 605 |

| 568 |

| 536 |

| 494 |

| 468 |

| Operating Income per Segment in $ million |

| 4Q21 |

| 1Q22 |

| 2Q22 |

| 3Q22 |

| 4Q22 |

| Refining & Marketing |

| 881 |

| 768 |

| 7,134 |

| 4,625 |

| 3,910 |

| Midstream |

| 1,070 |

| 1,072 |

| 1,126 |

| 1,176 |

| 1,088 |

| Items not allocated in the Segment |

| -173 |

| -161 |

| 68 |

| -173 |

| -244 |

Source: Company News

* MPC debt is $6,923 million, and MPLX debt is $19,779 million in 3Q22.

Analysis: Earnings Details

1 - Revenues and other income were $40.09 billion in 4Q22

MPC Quarterly Revenue History (Fun Trading)

{kind=link}

Note: Basic revenues were $39.813 million.

Marathon Petroleum reported a total income of $40.093 billion in the fourth quarter of 2022, up 12.6% from the same quarter a year ago and down 2.1% sequentially. Net income was $3,321 million or $7.09 per diluted share compared to $774 million in 4Q21, and adjusted net income was $6.65 per share, beating analysts' expectations.

The operating income from the Refining & Marketing and the Midstream units totaled $3,910 million and $1,088 million, respectively, exceeding expectations. However, operating income is slowly falling from the record-2Q22.

1.1 - Refining & Marketing

The company reported an operating income of $3,910 million compared to $881 million in the same quarter a year ago. The significant improvement was due to higher year-over-year margins but partially offset by lower throughputs and refined product sales. The refining margin was $28.82 per barrel in 4Q22, up from $15.88 a year ago.

Throughput decreased from 2,936 mbp/d in the year-ago quarter to 2,895 mbp/d, lower than expected. Capacity utilization during the quarter was the same as last year at 94%. Finally, operating costs per barrel increased by 4.9% from last year.

Below is the Refinery margins history:

MPC global R&M Margin history (Fun Trading)

{kind=link}

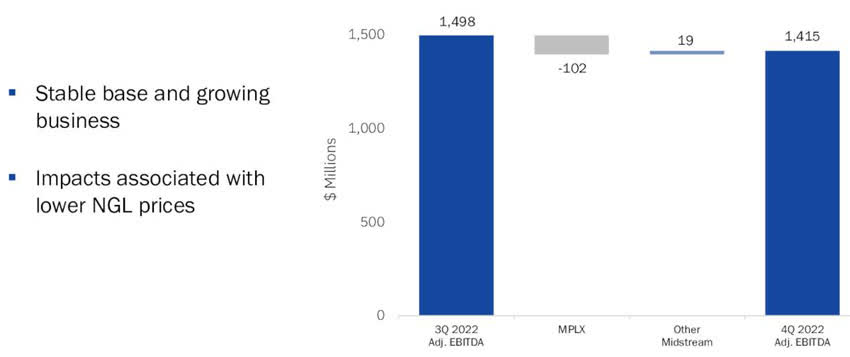

1.2 - Midstream

Marathon Petroleum's general and limited majority partners are MPLX LP. Segment profitability was $1,088 million, up 1.7% from $1,070 in 4Q21. MPLX has largely underperformed MPC on a one-year basis. However, the company is now paying a higher dividend yield than MPC of 9.00%.

MPC MPLX adjusted EBITDA 3Q22 versus 4Q22 (MPC Presentation)

{kind=link}

CFO Maryann Mannen said in the conference call:

This morning MPLX also announced their 2023 capital investment plan of $950 million. Their plan includes approximately $800 million of growth capital and $150 million of maintenance capital. The capital spending plan focuses on adding new gas processing plants and smaller investments targeted at expansion and debottlenecking. of existing assets to meet customer demand.

MPLX's lower EBITDA is primarily due to impacts associated with lower NGL prices, which may accelerate in 1Q23.

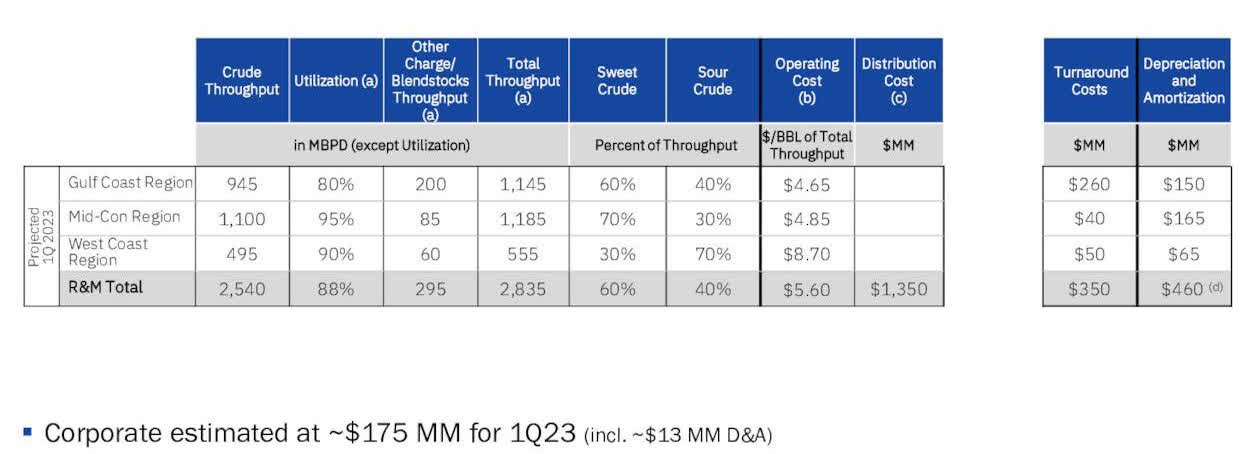

2 - 1Q23 Outlook

MPC 1Q23 outlook (MPC Presentation)

{kind=link}

3 - Free cash flow was estimated at $3,808 million in 4Q22 (subject to change after the 10-K filings)

MPC Quarterly Free cash flow history (Fun Trading)

{kind=link}

Note: Generic free cash flow is the cash from operations minus CapEx. The company has a different way of calculating it.

The trailing 12-month free cash flow was $14,093 million, with approximately $3,808 million in 4Q22. The dividend payout ($3.00 per share) is $1.404 billion annually, which is covered by Free cash flow.

4 - The total debt is $26.7 billion (consolidated) in 4Q22

MPC Quarterly Cash versus Debt history (Fun Trading)

{kind=link}

Note: The graph above indicates the debt on a consolidated basis.

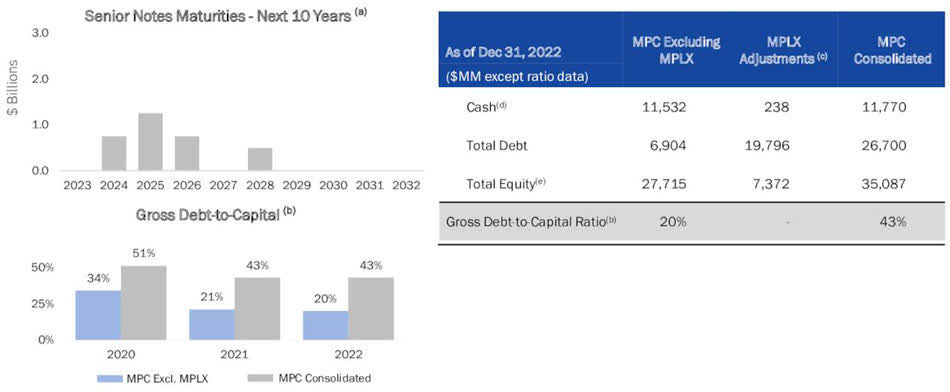

MPLX's debt is $6.904 billion. As shown below, the debt is $19.80 billion on a standalone basis, with a debt-to-capital ratio of 20% and 43% on a consolidated basis. Total cash is $11,770 million (MPC standalone cash was $11,532 million).

MPC Balance sheet 4Q22 (MPC Presentation)

{kind=link}

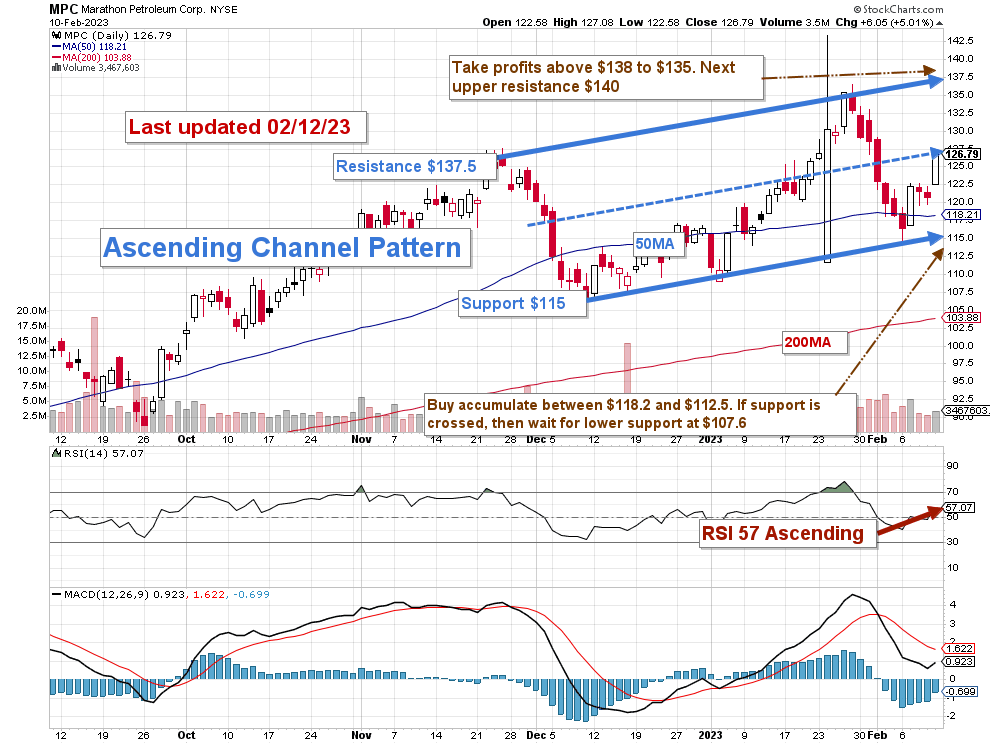

Technical Analysis (Short Term) and Commentary

MPC TA Chart short-term (Fun Trading StockCharts)

{kind=link}

Note: The chart is adjusted for the dividend.

MPC forms an ascending channel pattern with resistance at $137.5 and support at $115.

Ascending channel patterns are generally short-term bullish, moving higher within an ascending range, but these patterns usually form within longer-term downtrends as continuation patterns. Thus, I expect a retracement during H1 2023, and we should focus on the 200MA as the first support.

The overall strategy that I suggest in my marketplace, "The Gold And Oil Corner," is to keep a long-term position and use about 50% to trade LIFO (see note below) while waiting for a higher final price target for your core position between $140 and $145.

The trading strategy is to sell above $135 and $138 with possible higher resistance at $140. I suggest waiting for a retracement between $118.2 and $112.5 to accumulate again, with potential lower support at $108, which is close to the 200MA.

Warning: The TA chart must be updated frequently to be relevant. It is what I am doing in my stock tracker. The chart above has a possible validity of about a week. Remember, the TA chart is a tool only to help you adopt the right strategy. It is not a way to foresee the future. No one and nothing can.

For further details see:

Marathon Petroleum: Great Performance, But Will It Last?